Sierra closed a $950 million Series E at a $15.8 billion post-money valuation on May 4, 2026, led by Tiger Global and Google's GV with participation from Benchmark, Sequoia Capital and Greenoaks. The company, founded in 2023 by OpenAI chairman Bret Taylor and former Google VR lead Clay Bavor, sells AI customer service agents and reports more than 40% of the Fortune 50 as paying customers. Annual recurring revenue went from $100 million in November 2025 to $150 million in February 2026 — eight quarters from launch to $150M ARR — and the new round lifts the valuation from $10 billion in fall 2025 to $15.8 billion today.

TL;DR — what just happened

- $950 million Series E closed on May 4, 2026 at a $15.8 billion post-money valuation per TechCrunch reporting.

- Lead investors: Tiger Global, Google's GV. Participating investors: Benchmark, Sequoia Capital, Greenoaks Capital and existing investors.

- Valuation jump: from $10 billion in fall 2025 to $15.8 billion in May 2026 — a 58% increase in roughly six months.

- Annual recurring revenue: $150 million in early February 2026, up from $100 million in late November 2025. Eight quarters from founding to $150M ARR.

- Customer base: more than 40% of the Fortune 50 are Sierra customers per company disclosure. Agents handle billions of interactions across mortgage refinancing, insurance claims, returns and nonprofit campaigns.

- Founders: Bret Taylor (CEO Sierra, chairman OpenAI, ex-co-CEO Salesforce, ex-CTO Facebook) and Clay Bavor (ex-VP Google VR, ex-Google Labs).

- Total capital raised: over $1 billion across all rounds.

- Strategic role: Sierra breaks the “Anthropic monocluster” in OpenAI-orbit enterprise AI — running on a constellation of OpenAI and Anthropic models with Sierra-fine-tuned proprietary layers on top.

What happened: $950M, $15.8B, 90 days

Sierra announced its Series E on Monday, May 4, 2026. The round size is $950 million, the valuation is $15.8 billion post-money, the lead investors are Tiger Global and Google's venture arm GV, and the participating investors include Benchmark, Sequoia Capital and Greenoaks. Per CNBC and TechCrunch, the round brings total capital raised across all Sierra rounds to over $1 billion.

The speed of the valuation walk is the part that should be flagged. Sierra was reportedly valued at $10 billion in its previous round in fall 2025. Six months later, it is at $15.8 billion. That is a $5.8 billion mark-up in approximately 90 days from the company's late-November 2025 ARR disclosure to the early-February 2026 ARR figure that anchored the new round. In a market where most AI valuations stalled in early 2026, Sierra's continued mark-up signals that AI-customer-service-agent revenue is being priced as the most durable segment of the enterprise AI stack.

Sierra's valuation timeline

| Date | Valuation | Round | Lead investors | Notes |

|---|---|---|---|---|

| 2023 | Founded | — | Bret Taylor + Clay Bavor (founders) | 4 design partners |

| 2024 | ~$1B | Series B | Sequoia, Benchmark | First public valuation |

| Q1 2025 | ~$4.5B | Series C | Sequoia (lead) | Reported on rapid growth |

| Fall 2025 | ~$10B | Series D | Greenoaks (lead) | $100M ARR milestone |

| May 4, 2026 | $15.8B | Series E | Tiger Global + GV | $150M ARR |

The four-round walk in roughly 24 months places Sierra in the same growth-velocity bracket as the foundation labs themselves. What is different is that Sierra is not building a model — it is building the application layer on top of someone else's models. That distinction matters for the rest of this analysis.

Why it matters: the application layer just got priced like a model lab

For most of 2024 and 2025, the venture investing thesis on AI was that the foundation models — OpenAI, Anthropic, Google, xAI, Mistral — would capture the bulk of the value, while the application layer would commoditize. The argument was simple: if anyone can call GPT-4 or Claude through an API, what stops customers from cutting out the application company and going direct?

Sierra's $15.8 billion valuation on $150 million ARR — a 105x revenue multiple — is the loudest market signal yet that the application-layer-commoditization thesis is wrong, at least for verticalized agent companies with deep enterprise integration. Three structural reasons matter.

First, the integration moat is real. A Sierra customer-service agent does not just call Claude or GPT once. It routes across multiple models, runs Sierra-fine-tuned proprietary layers, integrates with the customer's CRM, ticketing, billing, knowledge base, identity provider and call-center workforce-management system. Ripping that out and replacing it with a direct OpenAI integration is a 9-12 month engineering project for the customer. Most CIOs will not run that project to save 30% on inference costs.

Second, the deployment data is the moat. Sierra agents have run billions of customer interactions per Sierra disclosure. Every interaction is training data, prompt-tuning data and quality-eval data that improves the next interaction. A new entrant has none of that. The data flywheel is the same one Salesforce used in CRM — every customer makes the product better for every other customer — and Bret Taylor co-led Salesforce, so this is not accidental.

Third, the buying motion is solved. Sierra is selling into the Chief Customer Officer / VP of Customer Service buyer, not the Chief AI Officer. That buyer cares about deflection rate, customer satisfaction, cost per contact and retention — not which underlying model is running. Sierra's 40%-plus Fortune 50 customer base is a function of solving the buying motion as much as solving the technology.

Financial details: ARR, multiples and the $400B prize

The numbers Sierra has disclosed publicly form a coherent picture of what is being priced.

| Metric | Value | Source / context |

|---|---|---|

| ARR (early Feb 2026) | $150M | Reported alongside the Series E |

| ARR (late Nov 2025) | $100M | Sierra's prior public milestone |

| ARR growth (90 days) | +50% | Implied from disclosures above |

| Founding | 2023 | Eight quarters to $150M ARR |

| Fortune 50 penetration | 40%+ | Per Sierra disclosure |

| Annual interactions handled | Billions | Per Sierra disclosure |

| Total capital raised | $1B+ | Across all rounds |

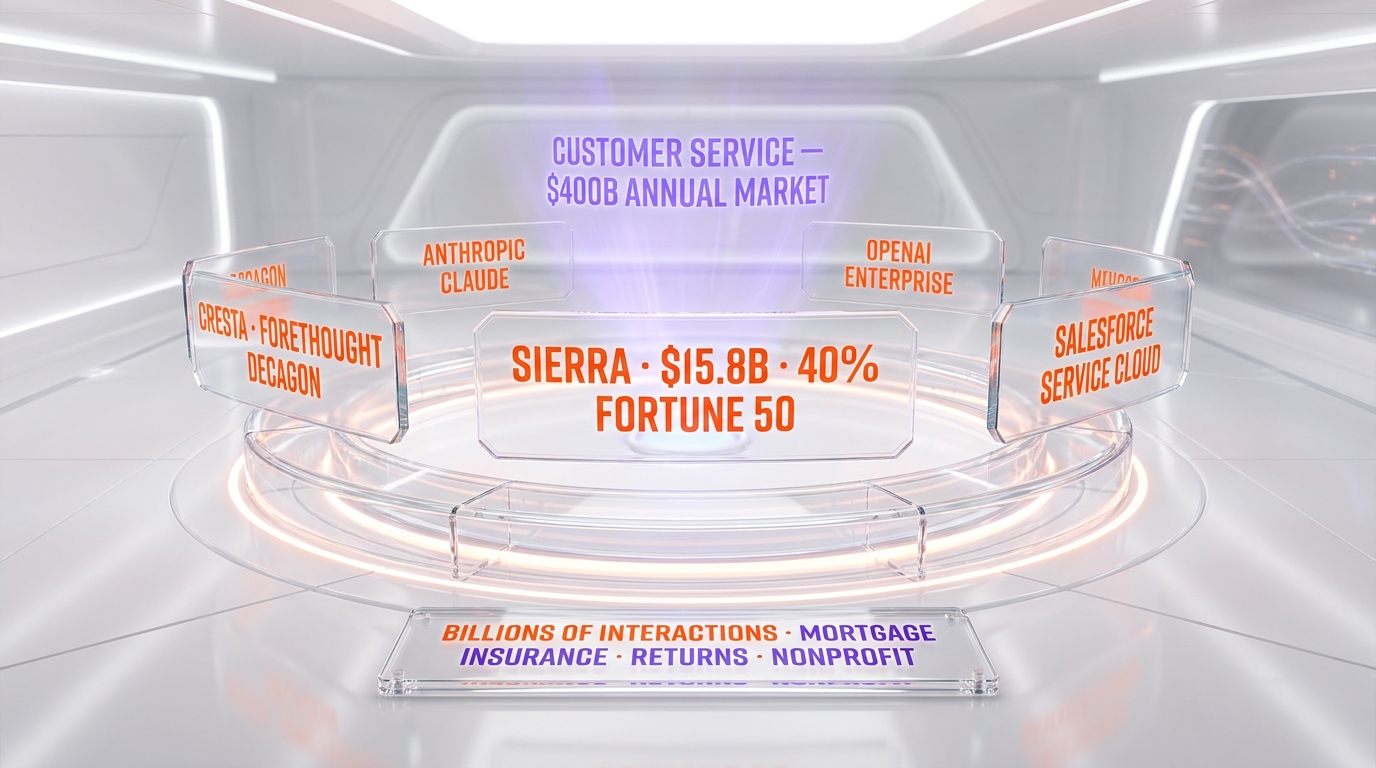

| Customer service market size | ~$400B annual spend | Per Bret Taylor's reported estimate |

| Series E revenue multiple | ~105x ARR | $15.8B / $150M ARR |

| Valuation increase since fall 2025 | +$5.8B (+58%) | $10B → $15.8B in approximately 6 months |

Bret Taylor told TechCrunch that there is “a really big addressable market and immediate opportunity” and described the customer service segment as the “last remaining analog channel” — the telephone line — that AI is now digitizing. He also noted that “there's just a lot of competition” and that Sierra is “multiples larger than the next biggest” in the segment, while warning that “when there's this much authentic excitement about a market, you end up with too much capital.”

The 105x ARR multiple is the headline number for the venture community to chew on. Pure-play SaaS at the same revenue scale typically prices at 15-25x ARR in 2026. Sierra is being priced at 4-7x that range — which only makes sense if the buyers are pricing in either (a) hyper-growth that takes ARR from $150M to $1B+ inside three years, (b) a structural margin advantage as Sierra moves from being a wrapper to having proprietary models in production, or (c) optionality on a tier-1 IPO or strategic acquisition. The actual answer is probably all three.

Customer service vertical: the $400B opportunity

Bret Taylor's framing is precise: customer service is the last remaining analog channel. Most enterprise digital transformation budgets have already been spent on web, mobile, e-commerce, payments, identity and back-office automation. The phone line — and the human-staffed contact center attached to it — is the largest remaining cost center that has resisted automation, partly because old-school IVR systems were so bad that they damaged the brand more than they saved.

The $400 billion annual customer service spend figure that Taylor referenced sets the addressable market. Even at a deeply discounted 5% software-capture rate over the next decade, that is a $20 billion software opportunity — multiples of Sierra's current valuation. The question is not whether the segment is real. The question is which company captures it and at what economics.

Sierra's competitors fall into four categories.

| Category | Examples | Threat to Sierra |

|---|---|---|

| CRM incumbents | Salesforce Service Cloud, Microsoft Dynamics, Zendesk, ServiceNow | High — deep account control, bundled pricing |

| AI-agent specialists | Cresta, Forethought, Decagon, Crescendo, Lindy | Medium — smaller scale, Sierra has integration lead |

| Foundation labs going direct | OpenAI ChatGPT for Customer Support, Anthropic Claude | Medium-high — pricing pressure on inference |

| BPO / call-center incumbents adopting AI | Concentrix, Teleperformance, Conduent | Low — structurally weaker GTM for software |

The single biggest threat in this list is Salesforce. Bret Taylor co-led Salesforce as co-CEO until 2022 and knows precisely how Service Cloud is built and sold. Sierra's $15.8B valuation is in part a bet that Taylor can outflank his former employer by shipping AI-native customer service agents faster than Salesforce can retrofit Service Cloud to do the same job. That is a personal contest worth watching for the next 18 months.

The Bret Taylor OpenAI conflict-of-interest question

Bret Taylor's day jobs are the most unusual structural feature of this story. He is simultaneously:

- CEO of Sierra, an enterprise AI agent company that runs on a “constellation of models” including both OpenAI and Anthropic foundation models.

- Chairman of OpenAI's board, the supplier of one of the two foundation models Sierra uses, and the company that announced its own competing enterprise AI services JV called The Development Company on the same day, May 4, 2026.

The conflict-of-interest implications are real and not trivial.

Procurement. When Sierra negotiates inference pricing with OpenAI, the OpenAI counterparty is reporting up to a board chaired by Sierra's CEO. The fiduciary symmetry runs in both directions: Taylor must serve OpenAI shareholders' interest in maximizing inference revenue, while serving Sierra shareholders' interest in minimizing it. Most companies would set up a recusal protocol; whether Sierra and OpenAI have done so publicly is unclear.

Strategic information. As OpenAI chairman, Taylor sits on top of the company's strategic roadmap, including its enterprise services strategy. As Sierra CEO, he is competing in adjacent enterprise AI segments. The Development Company JV announced May 4 with TPG, Brookfield, Advent and Bain Capital is structurally aimed at the same enterprise services market Sierra is selling into — albeit at a broader scope than customer service alone.

Market signaling. When OpenAI launches an enterprise services JV on the same day Sierra closes a $950M round at $15.8B, the market reads that as coordinated rather than coincidental. That is not necessarily wrong — both companies benefit from the legitimization of enterprise AI as the dominant 2026 narrative — but it is a coordination that almost no other industry would tolerate at the chairman level.

Sierra has not publicly disclosed how the conflict is managed at the board or governance level. OpenAI has not commented either. The arrangement is workable as long as no Sierra-OpenAI commercial dispute reaches a level that would force a recusal disclosure. If one does, it would be one of the most awkward governance moments in tech in 2026.

Market context: Sierra inside the OpenAI power bloc

The Series E investor list places Sierra inside what is now visibly an “OpenAI power bloc” of high-velocity application-layer companies running on OpenAI infrastructure with overlapping board members and capital sources. Tiger Global, GV, Sequoia, Benchmark and Greenoaks are all repeat investors across the OpenAI-adjacent application layer — including Cursor, Harvey, Granola, Decagon and others. The signal is that the same Wall Street pools backing Anthropic's enterprise JV (Blackstone, Goldman, Hellman & Friedman) are not the same pools backing Sierra. The capital allocation has bifurcated cleanly along the OpenAI-vs-Anthropic axis.

For Anthropic specifically, this is a structural problem. Sierra's customer base — 40%+ of the Fortune 50 — is the exact buyer Anthropic's new $1.5B enterprise services JV is also targeting. The difference is that Sierra is already inside those accounts, with billions of interactions of operational history, and Sierra runs on a model-agnostic stack that uses Anthropic's models alongside OpenAI's. If Sierra wins more enterprise deployment share, it accrues to Sierra's valuation, not Anthropic's. The Anthropic JV announced three days earlier is in part a structural response to exactly this dynamic: Anthropic has decided it cannot rely on the application layer to be its enterprise channel.

What to watch next

Three threads will define whether Sierra delivers on the $15.8B valuation.

First, ARR trajectory through Q4 2026. The implicit thesis baked into a 105x ARR multiple is that Sierra hits $300M-$500M ARR by year-end 2026 and trends toward $1B by 2027. The market will be watching the next two quarterly disclosures with intensity.

Second, the Salesforce counter-move. Salesforce is the structural threat with the deepest account control in the segment. The Service Cloud roadmap for 2026 will be a direct test of whether Sierra's lead is durable or whether the incumbent can absorb the AI-native segment by bundling.

Third, the OpenAI governance question. If Bret Taylor's dual role becomes commercially uncomfortable — through pricing disputes, strategic divergence between Sierra and OpenAI, or the trajectory of The Development Company JV — the resolution will be one of the highest-profile governance moments of the AI era. The likeliest outcome is that Taylor steps down from one role within the next 12-18 months. Which one he steps down from will signal where the value capture in AI is actually accruing.

Our take

Sierra's $15.8 billion valuation on $150 million ARR is either the most overvalued application-layer company in AI or the most under-priced one, depending on whether you believe customer service is a $400B addressable market that gets meaningfully captured by software in the next five years. The bull case is straightforward: 40% of the Fortune 50 is a customer; the integration moat is real; Bret Taylor and Clay Bavor have a Salesforce-and-Google operator pedigree that is rare in AI; and the Tiger Global / GV / Benchmark / Sequoia / Greenoaks investor stack is the most sophisticated application-layer buyer pool in venture.

The bear case is that Salesforce eventually ships Service Cloud + AI agents at competitive parity, or that the foundation labs (especially OpenAI through The Development Company) take direct enterprise share, or that customer service automation hits a quality ceiling that prevents the segment from scaling beyond 30-40% of human-handled contacts. Any one of those compresses the multiple.

What is not in dispute: Sierra has built one of the fastest enterprise software businesses of the AI cycle, and it has done it inside an OpenAI power bloc that is now visibly competing with Anthropic's $1.5B Wall Street JV for the same enterprise dollars. The only thing more interesting than what Sierra builds next is which side of the AI cold war the Bret Taylor dual-role question gets resolved in.

Frequently asked questions

What is Sierra's valuation after the May 2026 Series E?

Sierra's post-money valuation after its Series E announced on May 4, 2026 is $15.8 billion. The round size is $950 million, led by Tiger Global and Google's GV, with participation from Benchmark, Sequoia Capital and Greenoaks Capital. The valuation is up from approximately $10 billion in the company's previous funding round in fall 2025 — a $5.8 billion mark-up in roughly six months.

Who founded Sierra and when?

Sierra was founded in 2023 by Bret Taylor, who serves as CEO, and Clay Bavor, a former Google vice president who oversaw VR and Google Labs. Bret Taylor is also the chairman of OpenAI's board and previously served as co-CEO of Salesforce and Chief Technology Officer of Facebook (now Meta). The founding team's pedigree from Salesforce, Google and Facebook is widely cited as a key reason Sierra has been able to win Fortune 50 customers at unusual velocity.

What does Sierra build?

Sierra builds AI customer service agents that deploy inside enterprise customers to automate phone, chat, email and messaging interactions. The agents handle workflows including mortgage refinancing, insurance claims processing, returns management, customer support and nonprofit fundraising. Sierra runs its agents on a “constellation of models” including foundation models from OpenAI and Anthropic, with Sierra-fine-tuned proprietary layers for enterprise-grade performance.

How much annual recurring revenue does Sierra have?

Sierra reported $150 million in annual recurring revenue in early February 2026, up from $100 million in late November 2025. That is approximately 50% ARR growth in roughly 90 days, and represents the trajectory from launch in 2023 to $150 million ARR in eight quarters — one of the faster ARR ramps among enterprise software companies in the AI cycle. Total capital raised across all rounds is over $1 billion.

How many Fortune 50 companies use Sierra?

More than 40% of Fortune 50 companies are paying Sierra customers as of May 2026, per Sierra's own disclosure. The agents running on Sierra's platform handle billions of customer interactions annually across multiple verticals. Specific Fortune 50 customer names have not been publicly disclosed by Sierra, which is consistent with enterprise software disclosure norms.

Who are the investors in Sierra's Series E round?

The Series E round announced May 4, 2026 was led by Tiger Global Management and Google's GV. Participating investors include Benchmark Capital, Sequoia Capital and Greenoaks Capital, along with existing investors from prior rounds. Sierra's prior fall 2025 round at a $10 billion valuation was led by Greenoaks. The investor base places Sierra inside the OpenAI-adjacent application-layer cluster of investors that also back Cursor, Harvey, Decagon and similar enterprise AI companies.

Why is Bret Taylor's dual role at Sierra and OpenAI a conflict of interest?

Bret Taylor is simultaneously the CEO of Sierra and the chairman of OpenAI's board. Sierra is a paying customer of OpenAI's API while also competing structurally with OpenAI's enterprise services initiatives, including The Development Company joint venture announced on the same day as Sierra's Series E. Procurement negotiations between Sierra and OpenAI involve a reporting line that ultimately reaches Taylor in his OpenAI capacity, raising fiduciary symmetry questions. Neither Sierra nor OpenAI has publicly disclosed how the conflict is managed at the governance level.

How does Sierra compare to Salesforce Service Cloud?

Salesforce Service Cloud is the dominant customer service platform with deep account control across Fortune 500 companies and bundled pricing through the broader Salesforce CRM stack. Sierra's structural advantage is that it ships AI-native customer service agents from a clean architectural starting point, while Salesforce is retrofitting AI into a 25-year-old platform. Bret Taylor co-led Salesforce as co-CEO until 2022, so he understands Service Cloud's roadmap and weaknesses better than any outside competitor. The Salesforce-vs-Sierra contest will define the customer service segment over the next 18 months.

What is the customer service market opportunity Sierra targets?

Bret Taylor has reportedly estimated the global customer service market at approximately $400 billion in annual spend across enterprise contact centers, business process outsourcing and in-house support functions. Even at a conservative 5% software capture rate over the next decade, that represents a $20 billion software opportunity — multiples of Sierra's current valuation. Taylor describes customer service as the “last remaining analog channel” that AI is now digitizing.

How does Sierra's Series E connect to the Anthropic Wall Street JV?

Sierra's Series E announced May 4, 2026 is part of the same enterprise AI funding cycle as Anthropic's $1.5 billion enterprise services joint venture announced the same day. The two rounds split capital cleanly between the OpenAI-adjacent application layer (Sierra, Tiger Global, GV, Benchmark, Sequoia, Greenoaks) and Anthropic's direct deployment channel (Blackstone, Goldman Sachs, Hellman & Friedman, Apollo, GIC, Sequoia overlap). The two ventures will compete for the same Fortune 50 buyers but with structurally different go-to-market models — Sierra through application-layer software, Anthropic through embedded engineering services.