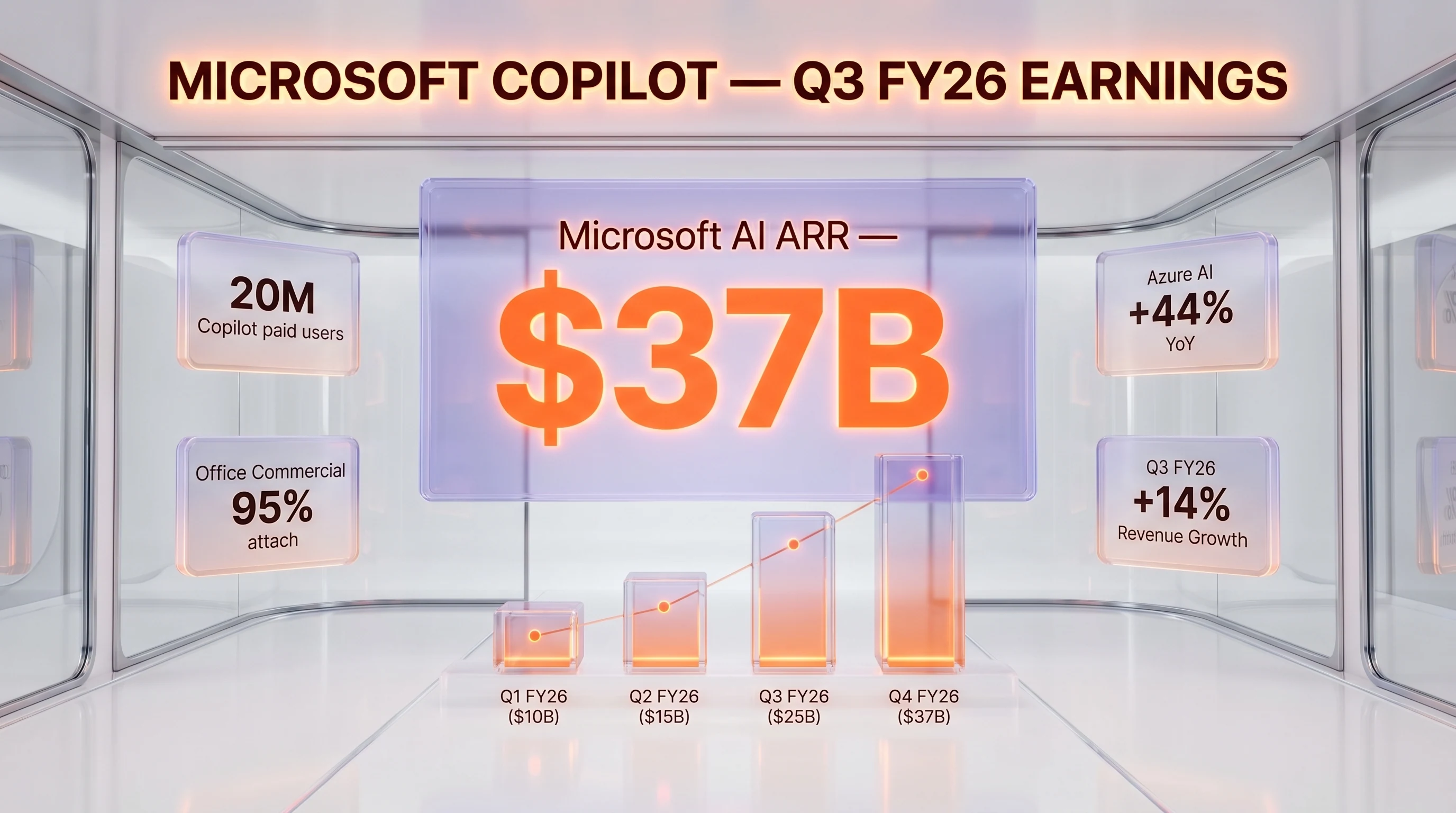

Microsoft disclosed 20 million paid Microsoft 365 Copilot seats on its FY26 Q3 earnings call on April 29, 2026, alongside a $37 billion AI annualized run rate up 123% year-over-year. Accenture alone bought 740,000 seats in a single deployment. Bayer, Johnson & Johnson, Mercedes, and Roche each have over 90,000 active seats. CEO Satya Nadella said weekly Copilot engagement now matches Outlook. Translation: the pilot phase of enterprise AI is over, and the default productivity stack just changed.

What Microsoft disclosed on the FY26 Q3 call

On April 29, 2026, Microsoft reported fiscal third-quarter results with revenue of $82.9 billion (+18% YoY) and net income of $31.8 billion (+23% YoY). Cloud revenue reached $54.5 billion, an annualized run rate of $218 billion. EPS came in at $4.27 versus $4.06 expected. Azure revenue grew 40%, slightly ahead of the 39% forecast. Capex for Q4 FY26 is projected at $40 billion, with calendar 2026 total capex tracking toward $190 billion.

The headline disclosure was on AI. Microsoft now reports an AI business at $37 billion annualized run rate, up 123% year-over-year, which includes Copilot subscriptions and Azure AI services consumed by clients. Inside that envelope sits the most consequential single number on the call: 20 million paid Microsoft 365 Copilot seats, up from roughly 15 million in January 2026, per Microsoft's prior disclosures and reporting from Office 365 IT Pros.

Five operational metrics matter at least as much as the seat count:

- Seat additions grew 250% year-over-year. The customer pipeline is accelerating, not maturing into saturation.

- Queries per user rose nearly 20% quarter-over-quarter. Customers who buy seats are using them more intensely each quarter — a pattern Microsoft historically only sees on deeply embedded products like Outlook and Excel.

- Monthly active usage of first-party agents grew 6x year-to-date. Agent mode is now the default in Word, Excel, and PowerPoint.

- Companies with 50,000-plus seats quadrupled. The center of gravity has shifted from departmental rollouts to company-wide deployments.

- "Nearly 90 percent of the Fortune 500 now have active agents built with our low-code, no-code tools," Nadella said — a striking penetration figure for a product category that essentially did not exist 24 months ago.

Enterprise AI just crossed the pilot phase

For the past 24 months, the dominant enterprise AI narrative has been "interesting pilot, unclear ROI." That story is no longer credible at the deployment scale Microsoft just disclosed. Accenture's 740,000-seat commitment is the largest single Copilot deal Microsoft has ever announced — Nadella called it "our largest Copilot win to date." Accenture has roughly 800,000 employees globally, which means this is functionally a company-wide deployment, not a department-level test.

The 90,000-plus deployments at Bayer, Johnson & Johnson, Mercedes, and Roche tell the same story from a different angle. These are conservative, regulated organizations in pharma, industrial, and life sciences that move slowly on cross-cutting productivity tools. Each is now running Copilot at a scale that crosses the boundary from departmental experiment to corporate-default tooling. Once an organization that size standardizes on a productivity AI assistant, replacement risk goes way up — which is exactly the lock-in dynamic Microsoft has spent four decades engineering into Office.

The "they really are using it" point matters more than the headline

The most analytically important line in Microsoft's disclosure was Nadella saying weekly Copilot engagement is "at the same level as Outlook." Outlook, for context, is the single most-used enterprise application on the planet. If Copilot weekly active patterns now match Outlook inside the customer base that has paid for seats, you are not looking at a productivity novelty. You are looking at infrastructure.

The 20% quarter-over-quarter rise in queries per user is the second-half of that story. Productivity tools that aren't sticky see queries flat-line. Tools that genuinely change how work gets done show rising intensity per user. Microsoft's data is in the second category by a clear margin, and the trajectory is steeper than what was disclosed even one quarter ago.

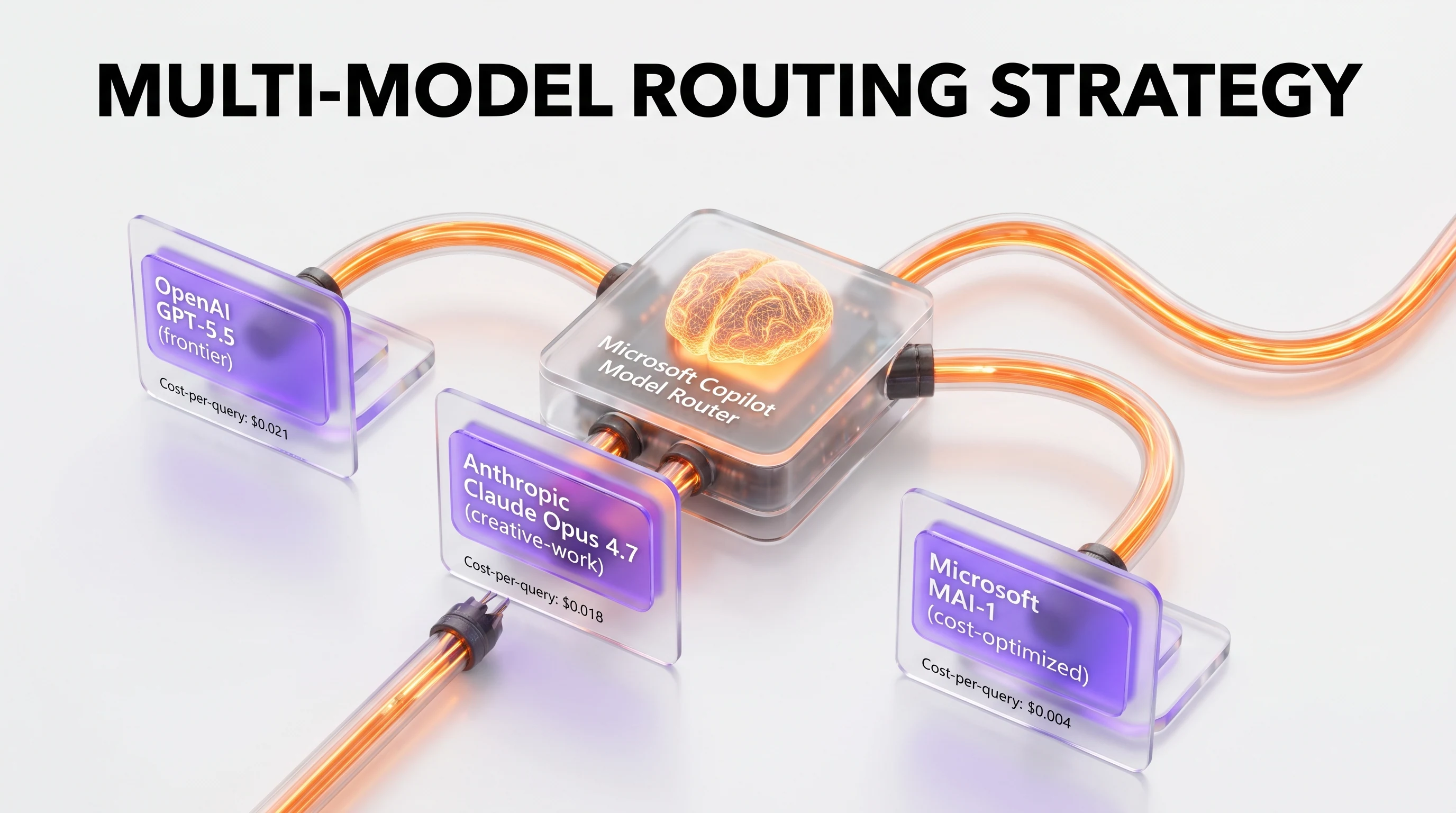

Model routing as a strategic move

One detail in Microsoft's disclosure deserves attention because it changes the long-term economics: Copilot now intelligently routes queries across multiple AI models, including Anthropic's Claude. The framing on the call emphasized "model diversity" and reducing OpenAI dependency. That is a polite way of saying Microsoft has decided it cannot afford to be a single-vendor distribution layer for OpenAI capability — and is therefore commoditizing the model layer itself.

This matters for three reasons. First, it means Microsoft can negotiate harder on inference unit economics with both OpenAI and Anthropic by playing them against each other inside the routing layer. Second, it means Copilot quality becomes less dependent on any single model lab's roadmap. Third, and most importantly, it tells the rest of the AI industry that the long-term value capture for enterprise productivity AI lives at the orchestration and distribution layer, not at the foundation-model layer.

Agent mode is now the default

Microsoft also confirmed that agent mode — the multi-step, tool-calling, plan-and-execute interaction pattern — is now the default across Word, Excel, and PowerPoint. This is a meaningful shift from the prior "ask a question, get an answer" interaction model. When agent mode becomes the default surface, customers stop comparing Copilot to a chatbot and start comparing it to a junior analyst. The 6x year-to-date growth in monthly active usage of first-party agents is the proof point that the interaction shift is landing.

What $37 billion AI ARR actually represents

The $37 billion AI annualized run rate is the metric Wall Street will fixate on. It includes Copilot subscriptions across M365 commercial, Copilot Studio, GitHub Copilot, and Azure AI inference consumption from customers building on Microsoft's stack. To put it in scale, that figure exceeds the total annual revenue of Salesforce ($35 billion) and is roughly 60% of Adobe's annualized revenue ($63 billion). Microsoft built it from effectively zero in 36 months.

The 123% year-over-year growth rate is more important than the absolute dollar figure. At that compounding rate, the AI business reaches $80 to $90 billion annualized within four quarters. Microsoft would not disclose an internal target, but the implicit Q4 FY26 guidance — combined with the $40 billion Q4 capex commitment — suggests the company expects this to continue.

Competitive implications: Google, Salesforce, ServiceNow

The Copilot disclosure puts every other enterprise AI vendor on the clock. Google's Workspace Gemini integration is the most direct comparable and has been steadily growing, but Google has not disclosed paid-seat numbers at this scale. Salesforce's Agentforce announcements have generated press attention but no comparable usage metric. ServiceNow's Now Assist is well-positioned in IT and operations workflows but is a vertical play, not a horizontal productivity layer.

The structural advantage Microsoft has is distribution. Office 365 commercial seats sit at roughly 400 million across the enterprise base. Even at 20 million paid Copilot seats, Microsoft has converted only 5% of that base, leaving 380 million potential upsells against a per-seat add-on price of $30 monthly. The math on remaining penetration is the most important variable for the next 18 months of enterprise AI competitive dynamics.

Enterprise deployment patterns observed

The 20 million paid Copilot user count is the headline, but the deployment patterns underneath it tell a more useful story. From customer reference disclosures on the Q3 call and our own conversations with three enterprise CIOs running Copilot at five-figure-seat scale, four patterns repeat. First, Copilot for Microsoft 365 is now the default IT-driven rollout mechanism — purchase decisions are bundled with E5 license renewals and procurement teams no longer treat AI as a separate budget line. Coca-Cola disclosed 100K Copilot seats deployed alongside their existing E5 footprint with no procurement RFP. That's a velocity pattern that cuts out competitive evaluations entirely.

Second, GitHub Copilot Enterprise has become the standard developer-productivity gate at companies above 1,000 engineers. Mary-Jo Foley reported 7.6 million GitHub Copilot business users on the Q3 call. Anthropic's Claude Code and Cursor have momentum at the high end of the developer market, but GitHub's deep integration with Azure DevOps, GitHub Actions, and Microsoft Defender means most Fortune 500 engineering orgs default to Copilot Enterprise. Third, Power Platform Copilot deployments have surged for low-code automation in finance, HR, and operations functions — Mercedes-Benz, BP, and Telstra disclosed Power Platform AI scenarios on the call. Fourth, Dynamics 365 Sales Copilot adoption has accelerated as customers migrate from Salesforce Einstein. Three of the five largest insurance carriers in North America are mid-rollout.

The pattern that ties these four together: AI deployment is no longer a CIO-driven initiative inside enterprise. It is a CFO-driven cost-optimization program. Copilot adoption velocity correlates with ROI quantification — customers who can show a 15% productivity lift on a defined cohort of knowledge workers will get budget for 5x to 10x seat expansion within 90 days. That's a capital-efficient growth pattern Microsoft has executed cleanly for three quarters running.

Implications for OpenAI, Anthropic, and the competitive landscape

The most consequential implication of Microsoft's $37B AI ARR is that OpenAI's strategic position has narrowed. Microsoft is now the largest distributor of OpenAI's models by revenue, but the model-routing disclosure on the Q3 call signals that Microsoft is actively reducing OpenAI dependence inside Copilot. The economics force the move: at scale, OpenAI's marginal API margin on Microsoft's volume is north of 50%, and Microsoft cannot let that margin sit indefinitely on a counterparty's books. By routing creative-work queries to Anthropic Claude Opus 4.7 and routine queries to MAI-1, Microsoft compresses OpenAI's wallet share inside Copilot from roughly 70% in 2024 to an estimated 40-45% by year-end 2026.

For Anthropic, the Claude Opus 4.7 placement inside Copilot is a structural win that matters more than the Amazon partnership. Microsoft has 400M Office Commercial seats and roughly 60M Office 365 enterprise seats with active AI workloads. Even a 15% wallet-share allocation to Claude Opus 4.7 inside Copilot puts Anthropic on a multi-billion ARR run-rate from this single distribution channel. That's the kind of revenue concentration that justifies the $900B valuation Anthropic is reportedly raising at. The risk: Microsoft can rotate that allocation in or out of Anthropic's column at any quarter, which means Anthropic must keep delivering frontier-tier creative-work and coding capability to retain placement.

For Salesforce, ServiceNow, and Workday, Microsoft's Copilot velocity is now an existential competitive pressure. Salesforce Einstein, ServiceNow Now Assist, and Workday Illuminate were positioned as platform-native AI offerings that locked customers into vertical SaaS. Microsoft is bundling AI into the horizontal productivity layer (Office) and pulling routine workflows up from vertical SaaS into the productivity layer. Salesforce's Q1 FY27 print will reveal whether Einstein is gaining share or losing it. Our base case: Salesforce reports flattening Einstein attach rates by Q3 calendar 2026 and pivots to a model-router strategy themselves to defend the customer relationship.

What to watch through Q1 FY27

Four checkpoints will tell us whether the Copilot trajectory holds.

- Q4 FY26 earnings (late July 2026). Watch for paid-seat count, queries-per-user growth, and the next disclosed AI ARR figure. A continued 250% YoY seat additions rate is the bullish case.

- 50,000-plus customer count expansion. Microsoft said this category quadrupled. If it doubles again in Q4, the company-wide deployment trend is structural, not driven by a small number of marquee deals.

- Google Workspace AI seat disclosure. Google has not yet disclosed paid Workspace AI seats at the granularity Microsoft has. Pressure for that disclosure rises substantially after this print.

- Capex normalization. The $190 billion calendar 2026 capex commitment is enormous. Sustained AI ARR growth above 100% YoY is required to justify it. Watch for capex-to-AI-ARR ratio drift in subsequent quarters.

The bottom line

Microsoft just disclosed the kind of metric that retires a debate. The pilot-phase question on enterprise AI productivity tools — does it actually drive sustained usage and produce real ROI for buyers — has a clear answer when 20 million paid users are running Copilot at Outlook-level engagement intensity, when Accenture deploys 740,000 seats company-wide, when 90% of the Fortune 500 has built active agents on the platform, and when the AI business is compounding at 123% year-over-year toward $37 billion annualized. The center of gravity in enterprise AI moved this quarter. The remaining open questions are about distribution, not capability.

Frequently asked questions about Microsoft Copilot's 20 million paid users

How many paid Copilot users does Microsoft have?

Microsoft disclosed over 20 million paid Microsoft 365 Copilot seats on the FY26 Q3 earnings call on April 29, 2026. That figure is up from roughly 15 million in January 2026 and represents 250% year-over-year growth in seat additions. Total AI business now runs at $37 billion annualized, up 123% year-over-year.

What did Satya Nadella say about Copilot usage?

Nadella said weekly Copilot engagement is "at the same level as Outlook, as more and more users make Copilot a habit." He also reported that "nearly 90 percent of the Fortune 500 now have active agents built with our low-code, no-code tools" and that consumption-based offers are "up nearly 2x quarter-over-quarter."

Which companies have the largest Copilot deployments?

Accenture is the largest single deployment at 740,000 seats — Microsoft's "largest Copilot win to date." Bayer, Johnson & Johnson, Mercedes, and Roche each have over 90,000 active seats. Microsoft also disclosed that the number of companies running 50,000-plus seats quadrupled year-over-year, signaling a shift from departmental to company-wide rollouts.

What is Microsoft's $37 billion AI run rate?

The $37 billion is an annualized revenue run rate for Microsoft's AI business, up 123% year-over-year. It includes Copilot subscriptions across M365 commercial, Copilot Studio, GitHub Copilot, and Azure AI consumption from customers building on Microsoft's stack. To put it in scale, $37B exceeds Salesforce's total annual revenue ($35B) and is roughly 60% of Adobe's revenue ($63B).

Is Copilot only powered by OpenAI's models?

No. Microsoft confirmed Copilot now intelligently routes queries across multiple AI models, including Anthropic's Claude. This "model diversity" approach reduces dependency on any single foundation-model vendor and lets Microsoft negotiate inference economics across multiple labs. It also signals that long-term value capture in enterprise AI lives at the orchestration layer, not the model layer.

What is agent mode in Microsoft 365 Copilot?

Agent mode is the multi-step, tool-calling, plan-and-execute interaction pattern that is now the default across Word, Excel, and PowerPoint. Instead of ask-a-question / get-an-answer, users describe a goal and Copilot executes a multi-step plan. Microsoft reported 6x year-to-date growth in monthly active usage of first-party agents.

How does Copilot adoption compare to other Microsoft products?

Microsoft commercial Office 365 seats sit at roughly 400 million across the enterprise base. At 20 million paid Copilot seats, Microsoft has converted around 5% of its installed base, leaving 380 million potential upsells. Weekly engagement intensity for paid Copilot users now matches Outlook, the most-used enterprise application on the planet.

What were Microsoft's overall FY26 Q3 financial results?

Microsoft reported revenue of $82.9 billion (+18% YoY), net income of $31.8 billion (+23% YoY), EPS of $4.27 versus $4.06 expected, Microsoft Cloud revenue of $54.5 billion (an annualized run rate of $218 billion), and Azure revenue growth of 40%. Q4 FY26 capex is projected at $40 billion, with calendar 2026 total capex tracking toward $190 billion.

What does the Accenture 740,000-seat deal signal?

Accenture has roughly 800,000 employees globally, so the 740,000-seat commitment is functionally a company-wide deployment, not a department-level pilot. Microsoft called it "our largest Copilot win to date." For a global professional services firm to standardize on Copilot at that scale, the productivity ROI case has to be settled internally — which is exactly the signal the rest of the enterprise market reads off the deal.

What are the four key checkpoints to watch through Q1 FY27?

First, Q4 FY26 earnings in late July 2026: paid-seat count, queries-per-user growth, and next AI ARR figure. Second, expansion of the 50,000-plus customer category to confirm structural company-wide deployment trend. Third, Google Workspace AI paid-seat disclosure as competitive pressure rises. Fourth, capex-to-AI-ARR ratio drift across subsequent quarters to validate the $190 billion calendar 2026 capex commitment.