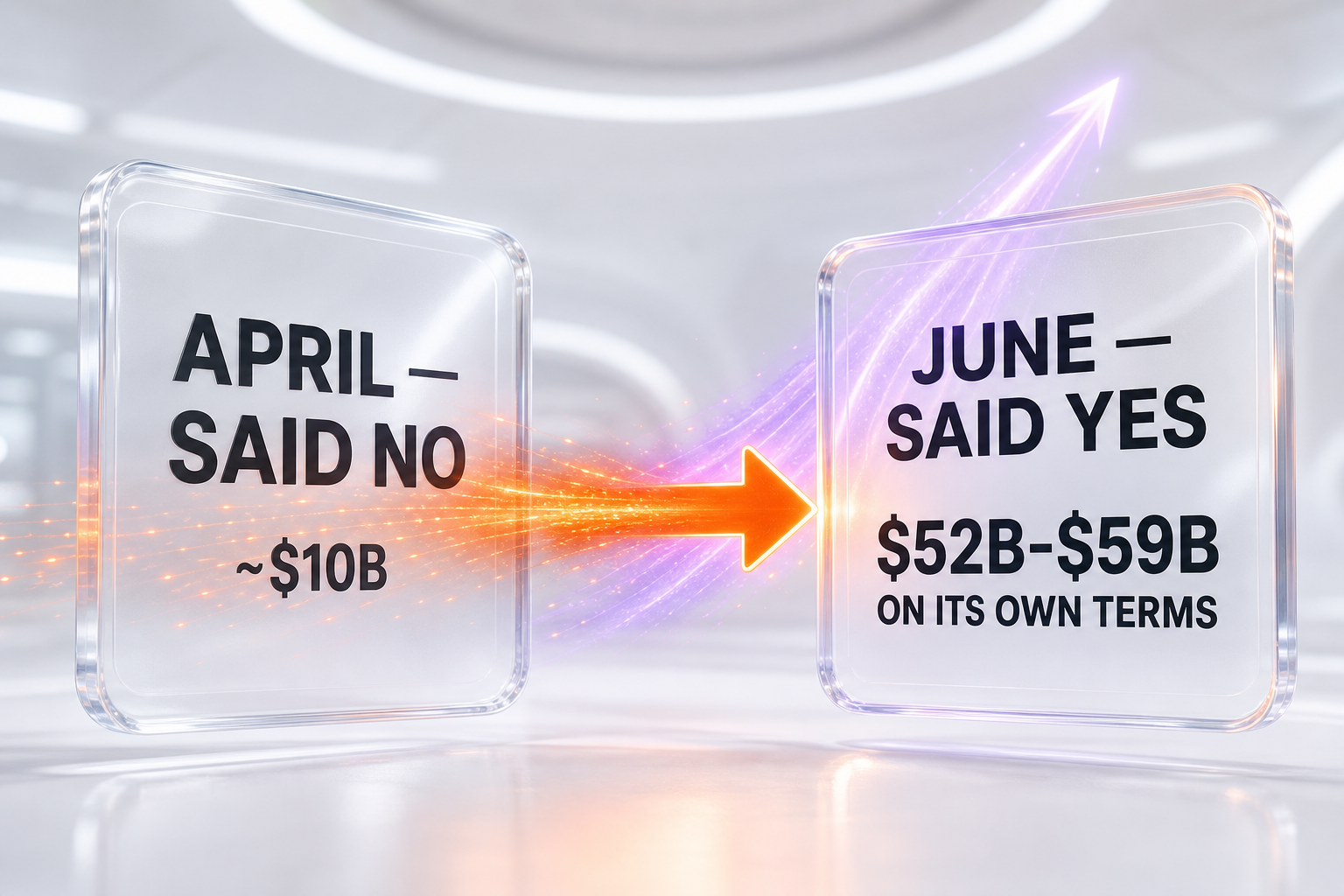

DeepSeek has closed its first-ever external funding round, raising approximately 50 billion yuan (around $7.4 billion) at a valuation reported between $52 billion and $59 billion, according to Reuters and The Information. The lab was previously self-funded entirely by founder Liang Wenfeng's quant hedge fund High-Flyer, with zero venture capital. The headline number is large, but the real story is the structure: external investors route their money into a limited partnership managed by Liang, accept a five-year lock-up, and receive no voting rights. Only China's state-backed National AI Industry Investment Fund gets direct equity and a vote. Two months earlier, in April 2026, DeepSeek had refused a similar approach at roughly a $10 billion valuation.

DeepSeek Said No in April. In June It Said Yes — On Its Own Terms

In April 2026, we covered the moment Tencent and Alibaba reportedly wanted a 20% stake in DeepSeek and DeepSeek said no. The lab had spent its entire existence allergic to outside money, bankrolled by High-Flyer, the quantitative hedge fund Liang Wenfeng built before DeepSeek existed. Refusing capital was the brand.

Two months later, that posture has changed — but not in the way a normal "founder caves to investors" narrative would suggest. DeepSeek is now reported to be raising approximately 50 billion yuan, around $7.4 billion, in what multiple outlets describe as its first external funding round. The reversal is real. The terms, however, look less like a capitulation and more like a founder writing the rules of his own auction.

We are not going to re-litigate the April episode here — if you want the full backstory of who approached whom and why the lab walked, that is in our earlier analysis. What matters now is what changed, what stayed the same, and why this round is structured so unusually that it may be the most interesting governance document in Chinese AI this year.

The short version: DeepSeek took the money. Liang kept the control. And the mechanism he used to do both at once is the part worth slowing down for.

What Happened: The Numbers, Hedged the Way They Should Be

Here is what tier-one reporting has established, with the caveats that a finance story like this demands.

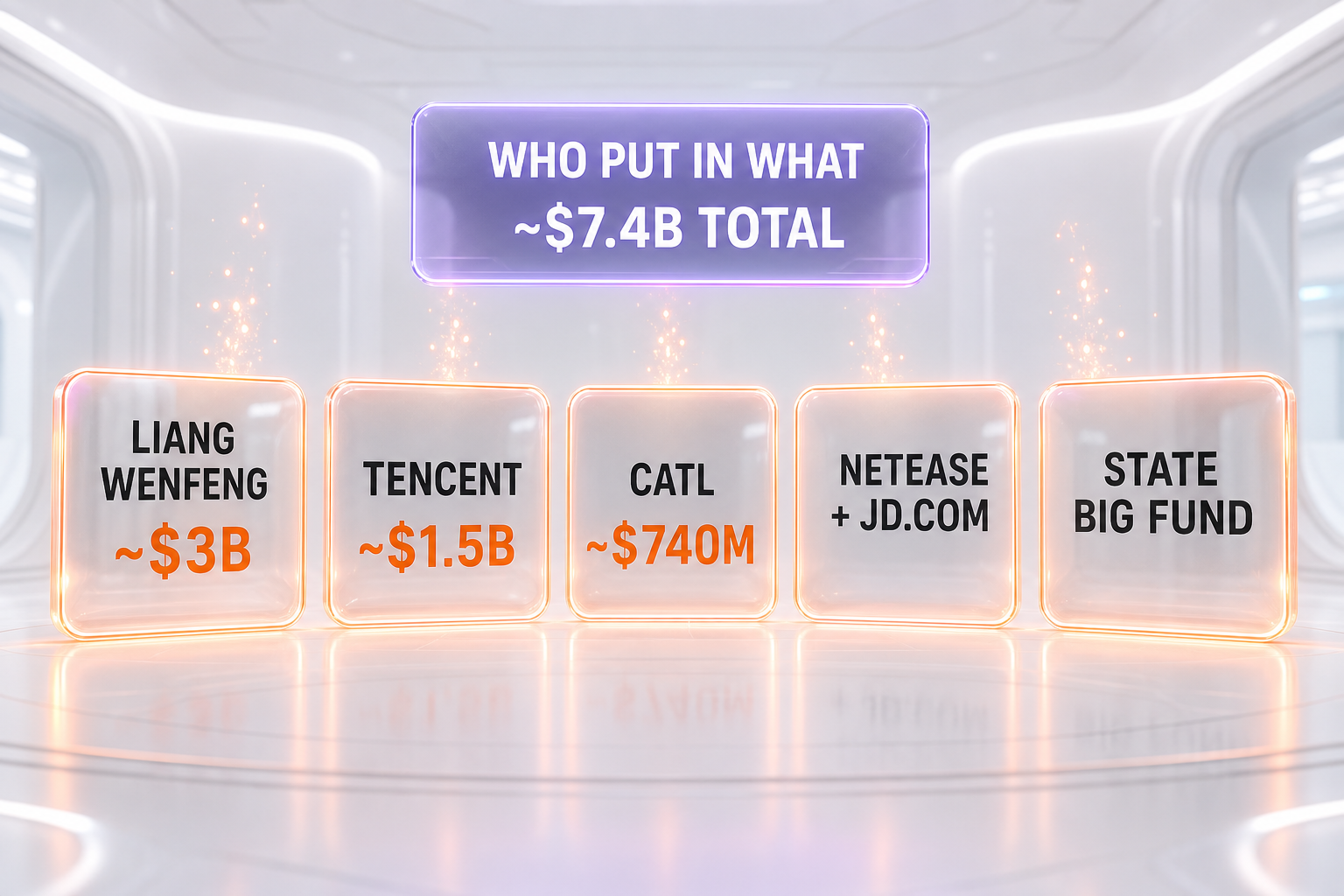

The amount. DeepSeek is raising approximately 50 billion yuan, which converts to roughly $7.4 billion at an implied rate near 6.76 yuan per dollar (yuan-to-dollar conversions move daily; treat the dollar figure as approximate and dated to early June 2026). Reuters first reported the round, with CNBC carrying the wire.

The valuation. This is where precision matters most. The reported post-money valuation is a range, not a single figure: roughly 350 billion to 400 billion yuan, or between $52 billion and $59 billion. Anyone quoting a clean "$59 billion DeepSeek" is cherry-picking the top of the band. The honest framing is the interval. Against the roughly $10 billion valuation implied during the April talks, even the floor of this range represents something close to a sixfold step-up in two months — a velocity that itself deserves scrutiny, which we get to below.

The investors. According to Reuters, the cap table reads like a roll call of corporate China plus the state:

- Liang Wenfeng (founder): reported to commit around 20 billion yuan (~$3 billion) of his own capital — which, against a ~50 billion yuan round, is an estimated ~40% of the total. Treat the percentage as an estimate; the exact split has not been formally disclosed.

- Tencent: approximately 10 billion yuan (~$1.5 billion) — the largest external corporate check.

- CATL (the battery giant): approximately 5 billion yuan (~$740 million).

- NetEase (gaming) and JD.com (e-commerce): each reported in the ~3 billion yuan range.

- The National AI Industry Investment Fund — China's state-backed "Big Fund" — alongside venture firms including IDG Capital, Monolith Capital, Loyal Valley Capital, and Shixiang Capital.

Note the composition: this is not a Sand Hill Road syndicate. It is China's strategic industrial base — a hedge fund founder, a social-and-gaming conglomerate, a battery champion, two e-commerce-and-content giants, and the state — pooling capital behind a research lab. That mix tells you what DeepSeek is to Beijing: not a startup, an asset.

The Real Scoop: A Limited Partnership, a Five-Year Lock-Up, and One Vote

If you only remember one thing from this round, make it this. The money is the headline. The structure is the story, and it was first detailed by The Information.

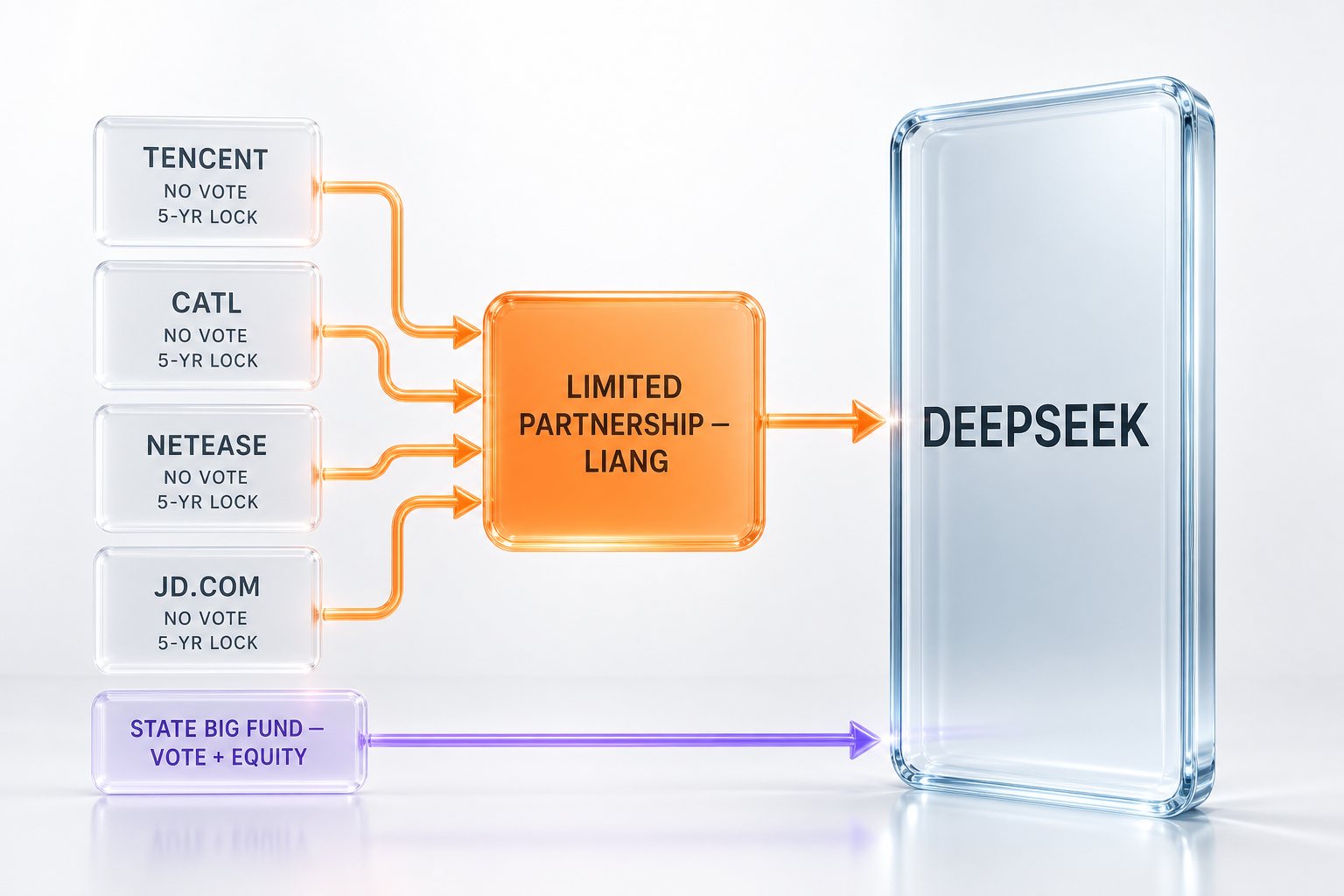

External investors are not buying shares in DeepSeek the company. They are putting their capital into a limited partnership managed by Liang Wenfeng. Inside that vehicle, they are bound by two extraordinary terms:

- A five-year lock-up. No selling, no liquidity, no early exit for half a decade.

- Zero voting rights. They write the check and they go quiet. No board seats translated into control, no governance leverage.

There is exactly one exception. The National AI Industry Investment Fund — the state vehicle — invested directly into DeepSeek, and it alone retains both voting rights and freedom from the lock-up. Read that again: in a round stuffed with Tencent, CATL, NetEase, and JD.com, the only outside party with an actual say is the Chinese state.

The effect is surgical. Liang Wenfeng raised roughly $7.4 billion, handed himself an estimated ~40% of the round in personal capital, and engineered the remaining external money into a structure where it carries no governance weight at all. He gets the war chest without surrendering the lab. For a founder who built his reputation on refusing capital precisely because he feared losing his research-first culture, this is the move that lets him have it both ways.

This is not how Silicon Valley does it. A typical US mega-round at this size would hand investors preferred shares, board representation, information rights, and pro-rata protections. DeepSeek's version inverts that: the capital comes in, the control does not flow out. It is closer to how some family-controlled conglomerates raise money than to how a frontier-AI startup normally does.

Why It Matters: Capital Without the Usual Strings

Three things make this round consequential beyond the dollar figure.

1. It funds the compute problem without the control problem. Frontier model training is brutally expensive, and DeepSeek's open-weights strategy — releasing model weights publicly rather than gating them behind an API-only paywall — generates influence and adoption far more than it generates revenue. We covered the technical side of that ambition when DeepSeek V4 launched in April 2026 with Flash and Pro variants, hybrid attention, and a 1M-token context window, and the broader trajectory in our look at the trillion-parameter open-weights push. Training the next generation of those models needs capital at a scale High-Flyer alone could not indefinitely supply. This round solves the funding question while the LP structure neutralizes the usual cost of taking outside money: dilution of control.

2. It signals state endorsement, explicitly. The fact that the National AI Industry Investment Fund is the only investor with direct equity and a vote is not a footnote — it is a statement. Beijing is not a passive LP here; it is the single outside entity Liang allowed into the cap table with real rights. For a lab whose models are downloaded worldwide, that is a meaningful signal about who ultimately sits closest to the table.

3. It resets the valuation conversation for Chinese AI. A range between $52 billion and $59 billion places DeepSeek in a different tier than it occupied two months ago. Whether that step-up is justified by fundamentals or inflated by strategic and political demand is a fair question — and one we would not answer with false confidence. What is clear is that the number now anchors expectations for what a leading Chinese open-weights lab is "worth," and that anchor will be referenced in every subsequent raise in the sector.

How It Compares: The Pragmatism Gap

It is tempting to slot DeepSeek's $52 billion to $59 billion band next to the valuations of US frontier labs and declare a winner or a bubble. We would caution against the reflex. The two ecosystems are pricing different things.

US mega-rounds increasingly price revenue trajectory and platform lock-in — API consumption, enterprise contracts, the expectation of eventual pricing power. DeepSeek's open-weights model deliberately gives away the thing that would generate that lock-in. Its value proposition to investors is harder to model in a spreadsheet: strategic importance, national-champion status, talent density, and the optionality of a lab that has repeatedly shipped frontier-adjacent models at a fraction of the reported cost.

That is the gulf several commentators have flagged: Chinese AI is being financed with a more pragmatic, industrial logic — back the strategic asset, accept the control structure, take the five-year horizon — while the Valley's valuation machine runs on growth multiples and exit timelines. Neither framing is automatically correct. But comparing the raw valuation numbers as if they measure the same thing would be a category error, and we are flagging it precisely so you do not make it.

Our Take: The Structure Is the Strategy

We have been following DeepSeek closely since the original April standoff, and the throughline is consistent: Liang Wenfeng treats control of the lab as non-negotiable, and he is creative about preserving it.

In April, preserving control meant saying no — refusing a 20% stake when the price of capital was governance. In June, preserving control means saying yes to a far larger sum, but only after building a vehicle where the capital is structurally muted. The lock-up and the voting carve-out are not investor-friendly terms; they are founder-protective ones. Investors accepted them anyway, which tells you how badly corporate China wants exposure to this asset.

What genuinely impresses us is the discipline of the design. It would have been easy to take Tencent's $1.5 billion on Tencent's terms. Instead, the round is engineered so that the one party with a vote is the state — the entity whose alignment a Chinese frontier lab arguably needs most and fears least. Whether you read that as savvy or as a quiet acknowledgment of where the real leverage sits, it is internally coherent.

What would make us reconsider. We are reporting a round that, per multiple outlets, is closing or near-closing — but terms can shift before final documents, the exact founder percentage is an estimate, and the valuation is a band, not a fact. If the final structure dilutes the lock-up, if the founder's contribution lands materially below the reported ~40%, or if the state fund's role turns out to be smaller than The Information's reporting suggests, the "founder keeps absolute control" read weakens. We will update this analysis if the closing terms diverge from what has been reported.

What's Next

The immediate question is what DeepSeek does with roughly $7.4 billion. The obvious answer is compute — the capital expenditure required to keep its open-weights models competitive with the frontier. We would watch for three things over the coming quarters:

- Compute commitments. Concrete chip and data-center spending would confirm the "war chest for training" thesis.

- The next model. A successor to the V4 line, trained on freshly funded infrastructure, would be the first tangible product of this raise.

- Whether the structure becomes a template. If other Chinese labs copy the founder-managed-LP-with-state-exception model, this round will be remembered less for its size and more for the governance pattern it pioneered.

For now, the takeaway is simple. DeepSeek raised an enormous sum on terms most founders could never command — and the reason it could is the same reason it said no in April. Control was always the point. This round just proved Liang Wenfeng can have the capital and keep it too.

Disclosure: ThePlanetTools.ai has no financial relationship with DeepSeek, High-Flyer, or any investor named in this article. This is editorial analysis, not investment advice. All financial figures are as reported by tier-one outlets (Reuters, The Information) and are subject to change before the round formally closes; dollar conversions from yuan are approximate and dated to early June 2026.

Frequently Asked Questions

How much did DeepSeek raise in its first funding round?

DeepSeek raised approximately 50 billion yuan, around $7.4 billion at an implied rate near 6.76 yuan per dollar, in what Reuters reports as the company's first-ever external funding round. The lab had previously been self-funded entirely by founder Liang Wenfeng's quant hedge fund, High-Flyer, with no venture capital.

What is DeepSeek's valuation after the funding round?

The reported post-money valuation is a range, not a single number: roughly 350 billion to 400 billion yuan, or between $52 billion and $59 billion. That is approximately a sixfold increase from the roughly $10 billion valuation implied during talks in April 2026. Quoting only "$59 billion" cherry-picks the top of the band; the honest figure is the interval.

Who invested in DeepSeek's funding round?

According to Reuters, founder Liang Wenfeng committed around 20 billion yuan (~$3 billion) of his own capital. Tencent invested approximately 10 billion yuan (~$1.5 billion) and CATL approximately 5 billion yuan (~$740 million), the largest external corporate checks. NetEase and JD.com participated in the ~3 billion yuan range, alongside China's state-backed National AI Industry Investment Fund and venture firms including IDG Capital, Monolith Capital, Loyal Valley Capital, and Shixiang Capital.

Why is DeepSeek's deal structure unusual?

Per The Information, external investors do not buy shares in DeepSeek directly. They place capital into a limited partnership managed by founder Liang Wenfeng, accept a five-year lock-up, and receive zero voting rights. This lets Liang raise roughly $7.4 billion while keeping full control of the lab — capital comes in, governance does not flow out.

Does any DeepSeek investor get voting rights?

Yes, but only one. China's National AI Industry Investment Fund — the state-backed "Big Fund" — is the sole exception: it invested directly into DeepSeek and retains both voting rights and freedom from the five-year lock-up. Every corporate investor, including Tencent, CATL, NetEase, and JD.com, has no vote.

How much of DeepSeek does Liang Wenfeng own after the round?

His exact stake has not been formally disclosed. He is reported to contribute around 20 billion yuan of the roughly 50 billion yuan round, an estimated ~40% of the total capital raised. Combined with the limited-partnership structure that strips external investors of voting rights, this leaves Liang firmly in control of the company.

Why did DeepSeek refuse funding in April 2026 but accept it in June?

In April, DeepSeek reportedly declined a 20% stake sought by Tencent and Alibaba because the price of that capital was governance — board influence and control. The June round changed the terms, not the principle: external money flows into a Liang-managed limited partnership with a five-year lock-up and no voting rights, so Liang takes a far larger sum while preserving the control he protected in April.

What will DeepSeek do with the $7.4 billion?

The capital is widely expected to fund compute — the chips and data-center capacity needed to keep its open-weights models competitive with the frontier. DeepSeek's strategy of releasing model weights publicly generates influence and adoption more than revenue, so training the next generation of models, building on its V4 line, requires capital at a scale High-Flyer alone could not indefinitely supply.