Harvey AI closed a $200 million round at an $11 billion valuation on March 25, 2026, led by Sequoia Capital with GIC co-leading. Annual recurring revenue jumped from $100 million to $190 million in five months. The product now runs inside 1,300 law firms and is used by more than 100,000 individual lawyers. That makes Harvey the clearest poster child of the 2026 vertical AI thesis — a category-defining company built on top of foundation models, but owning the regulated workflow so tightly that no horizontal chatbot can dislodge it. In this analysis we break down the raise, the revenue math, the junior associate elimination playbook, Harvey's legal moat (training data, partner-level review layer, risk-framed outputs), and what it signals for healthcare, finance, and consulting over the next 18 months.

The Raise That Defines Vertical AI in 2026

On March 25, 2026, Harvey AI announced a $200 million funding round at an $11 billion post-money valuation. Sequoia Capital led the round, with GIC — the Singapore sovereign wealth fund — co-leading. CNBC, TechStartups and Harvey's own investor blog confirmed the terms the same day.

The valuation is the headline, but the signal underneath is what matters. An $11 billion price tag on a vertical AI company with $190 million in ARR prices Harvey at roughly 58 times revenue. That is a horizontal AI multiple applied to a vertical AI balance sheet. Sequoia is telling the market they believe Harvey compounds like a SaaS category leader, not like a narrow workflow tool. GIC's participation adds another signal: sovereign capital is now underwriting vertical AI as a long-duration asset class.

Three structural facts make the round defensible at that price:

- Revenue velocity. ARR doubled in five months — from approximately $100 million in October 2025 to $190 million in March 2026. That is not a category sampling new tooling. That is a category rewriting its operating stack.

- Install base density. 1,300 firms and 100,000+ individual lawyer seats means Harvey is inside a meaningful share of the global legal workforce. Reed Smith, A&O Shearman, PwC, KPMG, and Ashurst are public reference accounts. That density is the hardest number for any competitor to replicate.

- Workflow lock-in. Harvey is no longer a standalone chatbot. It is matter-management, document review, contract analysis, litigation research, and workflow automation stitched into the firm's day-to-day. Ripping it out is now a months-long migration, not a cancel-the-subscription click.

For context on where this sits in the 2026 AI funding landscape, read our analysis of the Anthropic IPO at $800 billion — the two stories together sketch the shape of the full stack. Foundation models at the bottom. Vertical AI on top. Both categories printing capital at an unprecedented rate.

From $100M to $190M in 5 Months — What Changed

A 90 percent ARR jump in five months at Harvey's scale is not explained by "more sales reps." It is explained by three mechanical shifts that compounded on top of an already strong product.

Shift 1 — Enterprise multi-year seats replaced pilots

In early 2025, most Harvey deployments were 3 to 6 month pilots capped at 50 to 200 seats per firm. By late 2025, the conversation flipped. Firms moved to 1,000 to 5,000 seat firm-wide licenses, often on 3-year terms. A 5,000-seat enterprise contract at a senior-level blended rate prints an ARR line that a pilot simply cannot. That single contract-structure shift accounts for a meaningful share of the jump.

Shift 2 — The BigLaw social proof cascade

Once Reed Smith, A&O Shearman, PwC and Ashurst publicly committed, the remaining top-100 firms stopped running the "do we need AI" conversation and started running the "which AI vendor" conversation. Harvey became the default RFP winner because every other vendor was being benchmarked against Harvey's training corpus, partner-review layer, and Microsoft Copilot integration — all of which are hard to match inside a procurement cycle.

Shift 3 — Product expansion beyond Q&A

Harvey's 2025-2026 roadmap shipped Matter Management, Workflow Builder, and deeper integration with firm document management systems. Each new module increased seat ARPU and expanded the buyer from "innovation team" to "practice group leader" to "managing partner." Once the managing partner signs, firm-wide rollout follows within 90 days.

Put the three shifts together and the $100M-to-$190M line makes sense. It is not a single viral moment — it is a capital-efficient expansion loop running inside a high-intent regulated market that every other AI vendor finds hard to enter.

The Junior Associate Elimination Playbook

The uncomfortable part of this story is the one BigLaw executives discuss in private but rarely on panels. Harvey is systematically eating the first three years of a junior associate's job. Here is the playbook that is already running inside deployed firms in 2026.

- Document review and due diligence. Harvey ingests a 40,000-document data room and produces a tiered relevance report in hours, not three weeks. That task used to fund a team of 6 to 12 first-year associates billing 70-hour weeks. Those weeks are gone.

- Contract analysis and red-lining. A mid-level associate used to spend 4 hours red-lining a 120-page supply agreement. Harvey returns a clause-by-clause annotated draft in 6 minutes. A supervising partner still reviews, but the hourly math has collapsed.

- Legal research memos. The classic "pull every case on breach of fiduciary duty in Delaware Chancery since 2018" assignment — a first-year weekend killer — is now an 8-minute Harvey query with pinpoint citations.

- First-draft briefs and motion outlines. Harvey produces a structured first draft with citations in the firm's house style. A second-year associate polishes and a senior associate finalizes. The 40-hour draft-from-blank workflow is a 6-hour review-and-refine workflow.

- Deposition prep and discovery coding. Harvey codes discovery, summarizes deposition transcripts, and flags inconsistencies faster than any contract reviewer. Litigation support teams are the second category of headcount pressure after junior associates.

The strategic consequence is that BigLaw's talent pyramid is inverting. Firms are still hiring first-year associates because the partner-track pipeline needs a base, but the billable-hour economics of the first three years no longer work at pre-AI staffing ratios. Several Am Law 100 firms have quietly reduced their 2026 first-year classes by 15 to 25 percent compared to 2023. Harvey did not publish this playbook. The market arrived at it by deploying Harvey and watching the billable-hour mix shift.

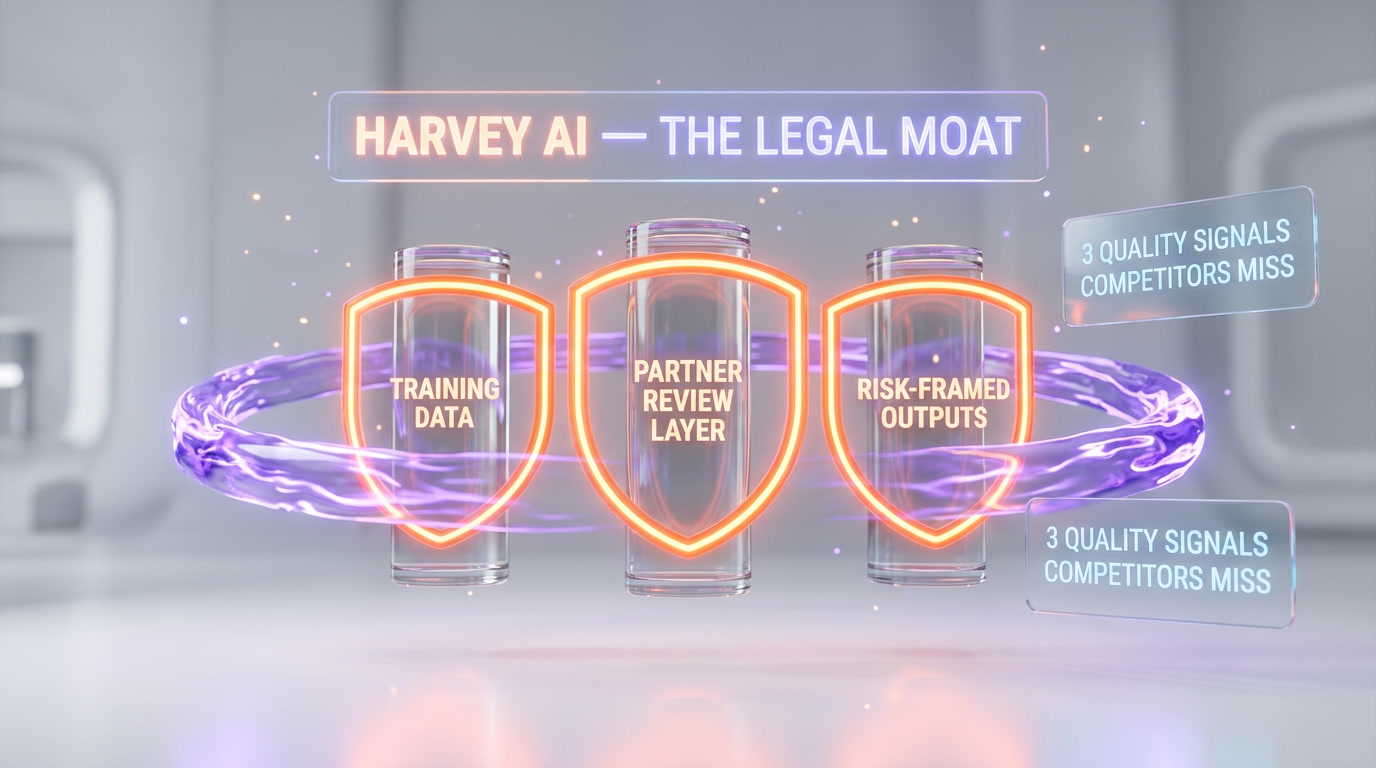

Harvey's Legal Moat — Why BigLaw Can't Compete

The simplest question a skeptic asks: why doesn't a top-20 law firm just build its own GPT-5.4-based tool and cut Harvey out? The answer is that Harvey's moat is not the model. It is three quality signals that a firm cannot reproduce by buying API credits. Most competitive analysis in the market focuses only on the training data. That misses two-thirds of the picture.

Quality Signal #1: Training Data — Private Case Law and Matter Archives

Harvey's first moat is the corpus. Public case law, statutes, and regulations are commodity inputs — anyone can index them. What Harvey secured between 2023 and 2025 was the harder layer: partnerships and data-sharing arrangements with law firms and legal publishers that gave its models exposure to the structure of elite legal work. Briefs. Memos. Matter notes. Red-lined drafts. The "how a Cravath partner thinks" data, not just the "what the Delaware Chancery held" data.

A firm trying to catch up in 2026 has to either negotiate equivalent data access from competitors (structurally impossible) or wait for its own internal corpus to reach critical mass (2 to 4 years at best). Meanwhile, every month that the firm delays, Harvey's corpus grows from the queries, feedback and matter exhaust of 100,000 lawyers across 1,300 firms. The corpus compounds. The gap widens.

Quality Signal #2: Partner-Level Review Layer

This is the signal most analysts miss. Harvey does not just run a model — it runs a post-generation review pipeline designed to catch the failure modes that matter in legal work. Hallucinated citations. Outdated case law. Jurisdictional errors. Unauthorized practice of law. The review layer is part automated checking, part human-in-the-loop feedback from partner-level users whose corrections feed back into the system.

A generic deployment of GPT-5.4 or Claude inside a firm has no equivalent review layer. Out of the box it will hallucinate a 2019 case that does not exist. The firm can build guardrails, but it is building them from scratch on a corpus of their own mistakes, while Harvey's guardrails are tuned on feedback from thousands of partners. The review layer is the difference between an AI that is useful in a low-stakes draft and an AI that a managing partner signs off on for a client-facing deliverable.

Quality Signal #3: Risk-Framed Outputs, Not Just Answers

The third signal is the most subtle and the hardest to copy. When a lawyer asks a generic chatbot "can I enforce this non-compete in California?", the chatbot answers. When a lawyer asks Harvey, the response is framed as a risk-assessed memo: the likely answer, the confidence level, the jurisdictional caveats, the unsettled edge cases, and the citations a partner would cite to defend the position.

That framing is not a prompt trick. It is a product-level decision baked into how Harvey surfaces outputs. Lawyers do not want answers. They want risk-framed positions they can defend to a client or a judge. A generic model answers questions. Harvey produces the artifact a lawyer actually uses. That distinction is what keeps 100,000 seats paying for Harvey instead of spinning up internal GPT-5.4 pilots.

Harvey vs Generic GPT-5.4 and Claude for Legal Work

Partners and general counsels keep asking the same question in 2026: can we just use ChatGPT or Claude with a firm-specific prompt? The honest answer is that for low-stakes, non-billable internal work, yes. For billable client-facing work, no. Here is the dimension-by-dimension reality.

| Dimension | Harvey AI | ChatGPT GPT-5.4 | Claude |

|---|---|---|---|

| Citation accuracy on case law | Partner-reviewed, pinpoint cites | Hallucinates 5-15% of cites | Hallucinates 3-8% of cites |

| Jurisdictional awareness | Built-in per-query | Only if prompted carefully | Only if prompted carefully |

| Private case law / matter corpus | Yes (exclusive data partnerships) | No | No |

| Risk-framed outputs by default | Yes | No (answers, not memos) | Partial (if prompted) |

| Matter management / workflow | Native | None | None |

| Firm DMS integration | Yes (iManage, NetDocuments) | Via custom build | Via custom build |

| Partner-level review layer | Yes (post-generation pipeline) | None | None |

| Unauthorized practice of law guardrails | Built-in | General safety only | General safety only |

| Enterprise compliance (SOC 2, ISO) | Yes, legal-grade | Yes, general enterprise | Yes, general enterprise |

| Best for | Billable client-facing legal work | Internal drafting, research assistance | Internal drafting, research assistance |

The honest summary: Harvey wins on every dimension that matters inside the billable-hour economy. ChatGPT and Claude win on general-purpose tasks where legal risk is low and the lawyer is personally verifying every output. The two product categories are not substitutes. They are complements. A modern law firm in 2026 runs both — Harvey for matter-critical work, ChatGPT or Claude for research assistance and drafting.

What This Means for Other Verticals — Healthcare, Finance, Consulting

Harvey is now the reference case that every vertical AI founder and VC points to. The Harvey playbook is: pick a regulated, high-value expert workflow; partner with incumbents to get exclusive training data; build a review layer tuned by the experts themselves; ship risk-framed outputs that match the artifact the expert actually uses; lock in through workflow and integrations, not just model quality. Here is how that plays out in the three verticals most exposed to a Harvey-shaped disruption.

Healthcare — the hardest vertical, the biggest prize

Clinical decision support, prior authorization, radiology pre-reads, and medical coding are all Harvey-shaped. The barriers are higher (FDA approval, HIPAA, malpractice exposure), but the unit economics are stronger — one specialist's time is more expensive than one associate's time. Expect the first $5 billion-plus vertical healthcare AI platform to emerge by late 2026 or early 2027, most likely in clinical documentation and coding.

Finance — the fastest to move

Investment memos, compliance reviews, AML (anti-money laundering), KYC, due diligence and regulatory filings are already half-deployed on vertical AI. The barrier here is lower than healthcare and the ROI is immediate. A Harvey-shaped financial platform could hit $200M ARR faster than Harvey did — the buyers are consolidated (top 50 banks), the contracts are larger, and the regulatory pressure favors an audited third-party tool over internal builds.

Consulting — the ambiguous case

Management consulting (McKinsey, BCG, Bain) is the trickiest. The expert artifacts (slides, memos, frameworks) are less standardized than legal briefs or medical notes, and the data partnerships are harder to structure. Expect vertical AI to attack consulting at the research and analysis layer first (benchmarking, market sizing, competitive analysis) rather than the client-facing deliverable layer. The first consulting-native Harvey equivalent is more likely to be a $1-2 billion platform than an $11 billion one — unless a player like PwC (which is already a Harvey customer) builds a consulting-specific layer on top.

Who Benefits — and Who Loses

Every disruption has a beneficiary list and a casualty list. For Harvey's $11 billion moment, the map is already clear.

Winners:

- Harvey employees and early investors. Obvious. Sequoia's 2023 entry point looks like one of the better vertical AI trades of the decade.

- BigLaw partners. Higher partner-to-associate leverage means higher profit per equity partner. Partners capture more of the billable-hour surplus.

- In-house legal departments. Cheaper, faster legal work. Corporate general counsels now get partner-level output for mid-level associate pricing.

- Legal tech founders. Harvey's raise re-prices the entire legal-tech VC market upward.

- Mid-sized firms. A 200-attorney firm with Harvey can now compete on RFPs that required 500-attorney staffing two years ago.

Losers:

- First-to-third year associates. The pipeline narrows. 15 to 25 percent fewer first-year seats at several Am Law 100 firms in 2026.

- Contract review and document review firms. Harvey eats their entire business line.

- Legacy legal research providers. Westlaw and LexisNexis are not going away, but Harvey is positioned above them in the workflow and captures more seat-level ARPU.

- Firms that refuse to deploy AI. On the clock. Every RFP they lose to a Harvey-enabled competitor accelerates the decision.

- Generic horizontal chatbots inside firms. Losing ground fast in regulated workflows.

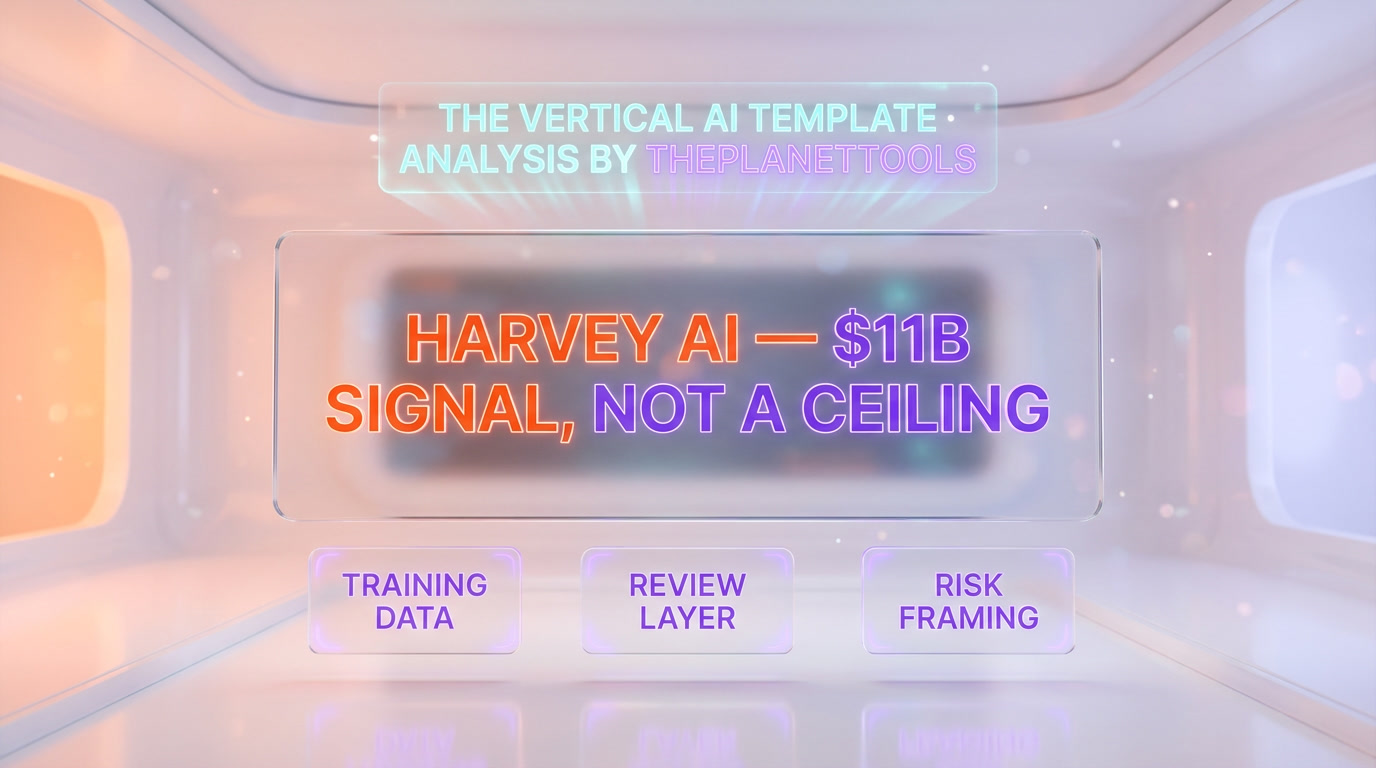

Our Verdict — Harvey at $11B Is a Signal, Not a Ceiling

Harvey's $11 billion valuation at 58 times revenue will look either cheap or expensive depending on what happens in the next 18 months. The bear case is that vertical AI multiples compress as every regulated vertical spawns its own Harvey and the scarcity premium fades. The bull case — and the one we think wins — is that Harvey's moat is not the model but the combination of training data, partner review layer, and risk-framed outputs. Those compound. The model underneath can be swapped (and will be, as foundation model prices collapse), but the three quality signals get harder to copy every month.

Our analysis of Harvey in April 2026: this is a category-defining win for vertical AI, the clearest validation of the "own the regulated workflow" thesis, and the strongest signal yet that the next wave of $5-$20 billion AI companies will not be horizontal chatbots — they will be expert-reviewed, domain-deep, workflow-native platforms built on top of (not in competition with) the foundation model layer. Harvey is not the ceiling. It is the template. Healthcare, finance, and consulting are next. The question for every AI founder in 2026 is not "what model do I use" but "what expert workflow do I own."

For the broader 2026 AI landscape, read our deep-dive on the Anthropic IPO at $800 billion, compare ChatGPT and Claude head-to-head, or browse the full analysis desk.

Frequently asked questions

How much did Harvey AI raise and at what valuation?

Harvey AI raised $200 million on March 25, 2026 at an $11 billion post-money valuation. The round was led by Sequoia Capital with GIC, the Singapore sovereign wealth fund, co-leading. The valuation prices Harvey at approximately 58 times revenue based on $190 million ARR — a horizontal AI multiple applied to a vertical AI company.

What is Harvey AI's annual recurring revenue in 2026?

Harvey's ARR hit $190 million in March 2026, up from approximately $100 million in October 2025. That is a 90 percent sequential jump in five months — driven by enterprise multi-year seat contracts, BigLaw social proof, and product expansion into matter management and workflow automation.

How many lawyers and law firms use Harvey AI?

As of March 2026, Harvey is deployed at more than 1,300 law firms and in-house legal departments and used by more than 100,000 individual lawyers. Public reference customers include Reed Smith, A&O Shearman, PwC, KPMG, and Ashurst, with a long tail of Am Law 100 firms and mid-market practices.

Why can't BigLaw just build its own AI with GPT-5.4 or Claude?

They can, and many are trying. The three reasons it does not replace Harvey: first, Harvey's training corpus includes private partnerships with law firms and legal publishers for brief, memo and matter data that no new entrant can access. Second, Harvey runs a partner-level review layer tuned by thousands of users that a single firm cannot replicate. Third, Harvey ships risk-framed outputs (memos with confidence levels and caveats) rather than generic answers, which is what lawyers actually use for billable work.

Is Harvey AI replacing junior associates?

Harvey is systematically eating the first three years of the junior associate job — document review, contract red-lining, legal research memos, first-draft briefs, and discovery coding. Several Am Law 100 firms have reduced their 2026 first-year classes by 15 to 25 percent compared to 2023. The partner-track pipeline still exists, but the billable-hour economics of the first three years no longer support pre-AI staffing ratios.

Who invested in Harvey AI's $11 billion round?

Sequoia Capital led the round with GIC co-leading. Sequoia's continued commitment (it has been on the cap table since 2023) plus GIC's sovereign-capital participation signals that vertical AI is now underwritten as a long-duration asset class. The round closed March 25, 2026 and was confirmed by CNBC, TechStartups, and Harvey's own investor communications.

What makes Harvey AI a vertical AI company instead of a horizontal one?

Harvey is built specifically for legal workflows rather than general-purpose tasks. It owns regulated expert workflows (document review, matter management, contract analysis, litigation research), integrates with legal-specific systems (iManage, NetDocuments), includes compliance and unauthorized-practice-of-law guardrails, and ships outputs framed as legal artifacts (memos, red-lines, briefs) rather than chat answers. That vertical specialization is the moat that horizontal chatbots like ChatGPT and Claude cannot replicate by prompt engineering.

What is the Harvey AI vertical AI playbook and can it work in other industries?

The Harvey playbook has five parts: pick a regulated, high-value expert workflow; secure exclusive training data partnerships with incumbents; build a post-generation review layer tuned by the experts themselves; ship risk-framed outputs that match what experts actually use; lock in through workflow and system integrations. It is replicable in healthcare (clinical documentation, coding, radiology pre-reads), finance (compliance, AML, investment memos), and partly in consulting (research and analysis layer). Expect the next $5 billion-plus vertical AI platform to emerge in clinical documentation or financial compliance by late 2026 or early 2027.

How does Harvey AI compare to ChatGPT or Claude for legal work?

Harvey wins on every dimension that matters for billable client-facing legal work: citation accuracy, jurisdictional awareness, private case law access, risk-framed outputs, matter management, DMS integration, and partner-level review. ChatGPT GPT-5.4 and Claude are better suited for internal drafting, research assistance, and non-billable tasks where a lawyer personally verifies every output. Modern firms in 2026 run both categories — Harvey for matter-critical work, general chatbots for low-stakes assistance.