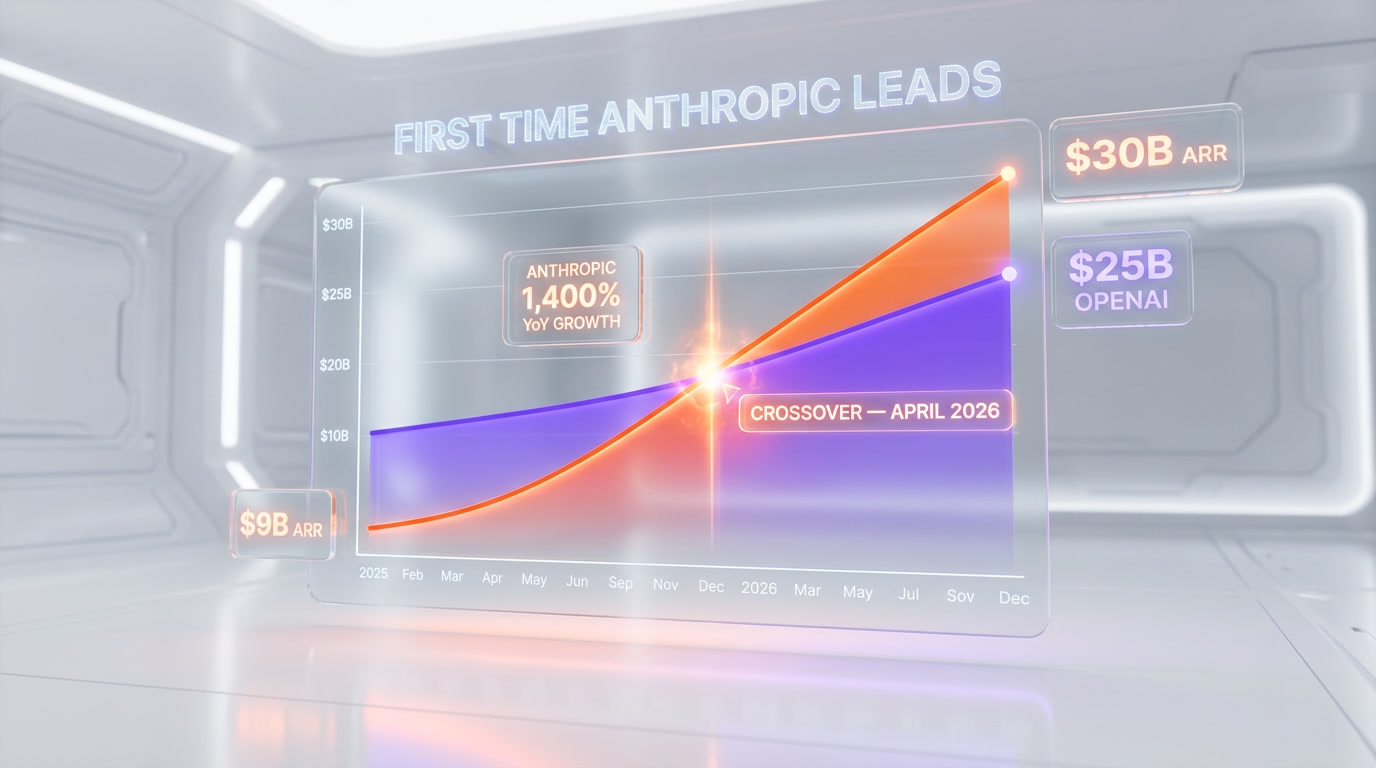

Anthropic crossed $30 billion in annualized revenue in April 2026, passing OpenAI's $25 billion for the first time in the two companies' history. By late May 2026, the company had closed a $65 billion Series H round at a $965 billion post-money valuation — roughly 2.5 times its $380 billion Series G from February — and on June 1, 2026 it confidentially submitted a draft Form S-1 to the SEC, the first formal step toward going public. An IPO could price as early as fall 2026, with the company already valued at close to $1 trillion — a listing that could rank among the largest technology IPOs ever. Chris Liddell, the former Microsoft CFO who engineered General Motors' $23 billion IPO, joined the board in February 2026 as the final governance signal. For the first time since ChatGPT's November 2022 launch, the revenue crown has changed hands. Here is the anatomy of the silent coronation — the three levers that moved Claude from plucky challenger to category leader in 18 months.

The silent coronation

There was no keynote. No product launch. No viral demo. And yet, sometime in the first week of April 2026, the AI industry's center of gravity shifted. Anthropic's annualized revenue had crossed $30 billion — more than tripling from $9 billion at the end of 2025. By the end of May 2026, that run-rate had climbed past $47 billion, a roughly fivefold jump from the $9 billion the company posted at the close of 2025. Over the same window, OpenAI sat at approximately $25 billion in annualized revenue. For the first time since ChatGPT kicked off the generative AI era, the revenue leader in the foundation-model race was not OpenAI.

Weeks later, Anthropic closed a $65 billion Series H round that pushed its post-money valuation to $965 billion — roughly 2.5 times the $380 billion Series G it closed in February 2026, and a figure that puts the company within striking distance of a $1 trillion valuation. The round was co-led by Altimeter Capital, Dragoneer, Greenoaks, Sequoia Capital, Capital Group, Coatue, and D1 Capital Partners. Then, on June 1, 2026, the company confirmed the next step: a confidential draft Form S-1 filed with the SEC.

Meanwhile, the IPO machinery is already running. Bloomberg reported in March 2026 that Goldman Sachs, JPMorgan, and Morgan Stanley are in early discussions as potential lead underwriters. The target window is as early as October 2026. The S-1 is now confidentially on file. The governance signal — the appointment of Chris Liddell, who took General Motors public in a $23 billion IPO in 2010 — was published in February. Everything is pre-wired.

How did this happen? Not in 18 months, actually. The shift was three years of compounding decisions, but it became unmistakable in the first quarter of 2026. Three levers did the work.

The numbers that broke the record

Start with the raw data, because the number is the story.

| Metric | Anthropic (April 2026) | OpenAI (April 2026) |

|---|---|---|

| Run-rate revenue | $47 billion+ | $25 billion |

| Revenue end of 2025 | $9 billion | ~$20 billion |

| YoY growth (approx.) | ~1,400% | ~250% |

| Valuation (current offers / last round) | $965B post-money (Series H) | ~$500B reported |

| Enterprise share of revenue | ~80% | ~30-40% (consumer-heavy) |

| Fortune 10 customers | 8 of 10 | Not disclosed |

| Enterprise accounts spending $1M+ per year | 500+ | Not disclosed |

| Training cost for current flagship | ~$30B peak total (efficient stack) | ~4x higher per model generation |

| IPO status | Targeting October 2026 | Not yet filed |

Three numbers deserve to be read twice. The first is $30 billion in annualized revenue achieved in 16 weeks of 2026 — $9 billion on December 31, $30 billion on April 7. That is not a growth curve. That is a step function. The second is the 80 percent enterprise share of revenue: Anthropic built an enterprise-first business in a market everyone assumed would be won by consumer scale. The third is the training-cost efficiency ratio. Anthropic is shipping a frontier model generation for roughly a quarter of what OpenAI spends to ship its equivalent. That is not an accounting quirk. It is a capex-to-margin story that public-market investors understand instantly.

Why the round repriced to $965B — vs $380B in February

A 2.5x revaluation in roughly three months is not a function of hype. It is a function of three signals that arrived in sequence.

Signal one: the revenue crossover. The $30 billion versus $25 billion number is, for any institutional investor, the first piece of hard evidence that Anthropic is not the number-two player. It is the number-one player by the only metric that matters for a pre-IPO valuation conversation — trailing annualized revenue. Once that number is public, every multiple used to value the comparable tier — OpenAI, xAI, Mistral — repegs.

Signal two: the efficiency ratio. Anthropic is reaching a run-rate north of $47 billion in revenue while spending approximately four times less than OpenAI on model training. That is not a branding line. It is a structural cost advantage rooted in three things — a smaller but more deliberate compute fleet, a research culture that optimizes for capability-per-flop rather than raw scale, and a more disciplined Claude release cadence. Projected profitability around 2028 or 2029 is plausible because the cost structure supports it.

Signal three: the enterprise moat. When 80 percent of revenue comes from business customers — and when that customer base includes 8 of the Fortune 10 and 500-plus accounts spending more than $1 million per year — you have what public-market investors read as a B2B SaaS cash machine wrapped in an AI brand. That is an entirely different valuation conversation than the consumer-API-traffic conversation that priced OpenAI through 2024.

The $380 billion Series G priced Anthropic as the number-two foundation-model company with a great brand and strong enterprise traction. The $965 billion Series H prices Anthropic as the number-one foundation-model company with a durable enterprise moat, a structural cost advantage, and a confidential S-1 already on file at the SEC. Three months. Same company. Different category.

Lever #1: Claude Code domination

The first lever is Claude Code. In 2024 it was a curiosity — a CLI wrapper around Claude that a handful of engineers on Twitter were using instead of Cursor. In 2025 it became a revenue engine. In 2026 it became the reason every serious engineering organization in the Fortune 500 was on a Claude enterprise contract.

The mechanics are simple. Claude Code solved the single most expensive problem in enterprise software development: getting a reasoning model to hold a large codebase in context, make coordinated multi-file changes, run its own tests, and not break. Claude Opus 4.7's 1M-token context window — released earlier this year, covered in our Opus 4.7 analysis — made that real at enterprise scale. A 200,000-line Python monorepo fits in one context. A full TypeScript front-end plus its Go backend plus its Terraform infra plus three weeks of Slack scrollback fits in one context. No agentic choreography. No retrieval-augmented shenanigans. Just a model that sees the whole thing.

The revenue consequence was immediate. Enterprise engineering organizations that had been running pilots on GitHub Copilot, Cursor, and Claude Code side-by-side consolidated onto Claude Code in Q1 2026. The seat math is brutal: a mid-size engineering org running 500 engineers on Claude Code at roughly $150-$200 per seat per month is booking $1M to $1.2M per year against one vendor, before agent usage gets charged separately. Multiply that by the hundreds of enterprise logos Anthropic closed across 2025 and into 2026 and you have most of the run-rate climb from $9B at the end of 2025 to north of $47B by mid-2026.

The competitive dynamic against ChatGPT and OpenAI's developer stack is equally stark. ChatGPT and GPT-4o-class models remain dominant on consumer-grade coding assistance. They are not dominant on enterprise-grade agentic coding, because the enterprise use case is not "help me write a function" — it is "refactor this 80-file legacy module without breaking the build." That is the Claude Code moat. And it is expanding.

Lever #2: Enterprise adoption — the Harvey, Notion, and Fortune 10 story

The second lever is enterprise adoption at the application-layer level. Anthropic did not just sell API access. It seeded and partnered with the vertical leaders who went on to define entire categories.

Harvey, the legal AI company used by virtually every top-tier law firm, is a Claude-first shop. The reason is not marketing — it is that Claude's reasoning on long, dense legal documents is measurably better than the alternatives, and the safety and refusal behavior fits a legal workflow where hallucinating a citation is a career-ending event. Notion, one of the largest productivity platforms in the world, runs its AI stack on Claude for the same reason — the reasoning quality on long-context summarization and writing tasks justifies the premium. When these two companies scale, Anthropic's API revenue scales with them without Anthropic spending a dollar on GTM.

Then there is the Fortune 10 number: 8 of 10. That means the largest enterprises on the planet — the ones with compliance and procurement functions that take 18 months to approve a new vendor — have signed multi-year, multi-million-dollar Claude contracts. That is not a trend. That is infrastructure. Once a Fortune 10 compliance team green-lights Claude as the enterprise-approved foundation model, the downstream procurement inside that organization runs for a decade.

The 500-plus accounts spending over $1 million per year is the number that breaks the old narrative. For two years the consensus was "Anthropic has great tech but OpenAI has the distribution." The 500-plus number means Anthropic has both. The distribution was just quieter — built through API integrations, system integrators, and vertical AI applications rather than ChatGPT's consumer funnel.

Lever #3: The safety brand premium

The third lever is the one that outside observers underestimate and enterprise buyers quietly love: the safety brand premium. Anthropic was founded in 2021 by Dario and Daniela Amodei and a group of former OpenAI researchers with one explicit differentiator — a research agenda centered on AI safety, interpretability, and Constitutional AI. For years that looked like a research positioning rather than a commercial strategy. In 2026 it looks like the single most valuable enterprise moat in the category.

Here is why. Every Fortune 500 procurement team running an AI risk assessment in 2025 or 2026 started the conversation the same way: what happens when this model refuses correctly? What happens when it is jailbroken? What is the vendor's track record on alignment research, red-teaming, and responsible release? Anthropic had a direct answer — published interpretability papers, Constitutional AI documentation, public safety policies, and a brand that compliance officers could defend in front of a board of directors.

That was not available from any other frontier-model vendor at the same level of depth. OpenAI had (and has) a strong safety program but carries the brand residue of the November 2023 governance crisis and a series of public safety-team departures. xAI explicitly positioned itself as a less-filtered alternative, which is a feature for some markets and a dealbreaker for Fortune 500 procurement. Google has the safety research but does not sell it as a brand at the front of the conversation. Anthropic does. And Fortune 500 procurement teams pay a premium for that clarity.

Combine the three levers — Claude Code's developer moat, enterprise application-layer dominance, and the safety brand premium — and you have three independent, compounding revenue engines. Pull out any one and the story still works. Pull out two and the story still closes the gap. With all three engaged, the result is a run-rate north of $47 billion and a $965 billion valuation. The math is not coincidence.

Chris Liddell — why this CFO hire matters

Governance matters in the last mile to an IPO. In February 2026, Anthropic announced that Chris Liddell had joined its board of directors. The announcement was quiet. The implications were loud.

Liddell's resume is the resume you hire when you are seven to nine months from an IPO. He was the chief financial officer of Microsoft from 2005 to 2009, during which he oversaw a period of aggressive cloud investment and shareholder returns. He was vice chairman and CFO of General Motors during its 2010 return to public markets — a $23 billion IPO that was at the time the largest in U.S. history and a textbook example of taking a structurally complex, regulatorily sensitive company public successfully. He was later deputy White House chief of staff for policy coordination during the first Trump administration, which gives him a rare combination of public-markets experience, Fortune 50 operating chops, and Washington fluency.

That is the precise skill combination Anthropic needs for a fall 2026 IPO at a valuation approaching $1 trillion. The company is not just taking a software business public — it is taking a company with a nationally strategic technology profile public, against the backdrop of an AI policy environment in which U.S. and Chinese regulators are both highly attentive. Our reporting on the joint OpenAI-Anthropic-Google industrial espionage pact earlier this year made clear how geopolitically salient these companies have become. Liddell has spent the last fifteen years navigating exactly that kind of surface area. The board appointment was an early pre-IPO signal, and the June 1 confidential S-1 filing confirmed the timeline was real.

The June 2026 S-1 filing — what just happened

On June 1, 2026, Anthropic confirmed what the funding cadence had telegraphed for months: the company confidentially submitted a draft registration statement on Form S-1 to the U.S. Securities and Exchange Commission for a proposed initial public offering of its common stock. A confidential submission is the modern playbook for large pre-IPO companies — it lets the company and the SEC work through the review process privately before the prospectus becomes public, typically several weeks ahead of a roadshow.

Anthropic was careful with the language, and so are we. In its own words, the proposed offering "will depend on market conditions and other factors," and "the number of shares to be offered and the price have not yet been set." In other words: the S-1 is a starting gun, not a finish line. There is no confirmed listing date, no confirmed raise size, and no confirmed offering price. What the filing does confirm is intent and timing — Anthropic is now formally in the IPO pipeline, ahead of rival OpenAI, which is reportedly preparing its own listing.

The filing lands against a backdrop of hard numbers. Anthropic's run-rate revenue crossed $47 billion earlier in the month, the Series H round closed at a $965 billion post-money valuation in late May, and the company is now widely described as approaching a $1 trillion valuation. Stack those together and the S-1 reads less like a gamble and more like the logical next move for a business that has compounded faster than any enterprise-software company in recent memory.

The IPO timeline — what to expect

Here is the realistic sequence, as currently telegraphed by the June 1 confidential S-1 filing and reporting from TechCrunch, CNBC, and Fortune through early June 2026.

- Q2 2026 (happening now). S-1 drafting with Goldman Sachs, JPMorgan, and Morgan Stanley, who are in early discussions as potential lead underwriters. Legal and audit preparation. Board finalizes governance structure. Expect a large analyst-day event in late Q2 to pre-brief the buy side.

- Summer 2026. The confidential S-1 (filed June 1) moves through SEC review. A public S-1 typically follows several weeks before the roadshow. Pricing negotiations with the lead underwriters set the valuation range.

- Fall 2026 target (not confirmed). Public listing, likely on a major U.S. exchange given the capital markets depth for an offering of this scale. The number of shares and the price are not yet set. At a valuation approaching $1 trillion, the listing could rank among the largest technology IPOs ever — though the final size will depend on market conditions.

- 2027 onward. Secondary offerings likely as insider lockups expire. Expect Anthropic to use public-market cash to aggressively capex-scale compute and, plausibly, to acquire one or more vertical AI companies to deepen the application-layer moat.

Two risks are worth naming. The first is macro — an October IPO requires public equity markets to be open and receptive in October, which is not guaranteed. The second is competitive — OpenAI is reportedly preparing its own IPO, and a competitive dual-track listing would complicate pricing for both. Anthropic going first has real advantages in capturing the "first pure-play large-model stock" narrative.

What this means for OpenAI

The implications for OpenAI are more nuanced than "Anthropic is winning, OpenAI is losing." OpenAI at $25 billion ARR is still a generational business. The consumer-facing ChatGPT franchise remains dominant in its category. The API developer footprint is enormous. What has changed is that OpenAI is no longer the unquestioned revenue leader, and the narrative premium that went with that title is now Anthropic's.

Three practical consequences for OpenAI. First, any pre-IPO valuation conversation is now pinned to a smaller multiple than it would have been six months ago, because Anthropic's revenue growth rate is materially higher. Second, enterprise procurement teams that had standardized on OpenAI will re-evaluate in 2026 and 2027 as multi-vendor AI strategy becomes the default. Third, the internal competitive pressure inside OpenAI — on model quality, on release cadence, and on enterprise GTM — goes up by at least one notch. Expect a visible product response by Q3 2026.

What this means for developers

For developers, the practical takeaways are short and useful.

- Claude Code is not a niche tool anymore. It is the enterprise-standard agentic coding surface for the Fortune 500. If you have not integrated it into your workflow yet, you are behind the curve. Start with our Claude Code tool overview.

- Claude Opus 4.7's 1M context window is underused. Most developers are still using Claude for chat-style tasks at 10K to 50K tokens. The step-change use cases are at 500K-plus tokens. See our deep dive on Opus 4.7 for what actually changes at that scale.

- Multi-vendor AI strategy is now the enterprise default. If you are an enterprise architect, your job for the next 12 months is to build routing and evaluation infrastructure that lets you pick the right model per task. Claude for long-context reasoning and coding. GPT-class for consumer interfaces. Open models for cost-sensitive batch jobs.

- The Claude API is durable. An IPO-funded Anthropic is a long-horizon vendor. API investment decisions made today will compound through the decade.

Compare the full ecosystem in our reviews of Claude, Claude Code, and ChatGPT, or browse the broader AI news desk for the ongoing coverage.

Our verdict

Anthropic beating OpenAI in annualized revenue is the first structural shift in the foundation-model industry since the category began. The three levers — Claude Code's developer moat, the enterprise application-layer dominance in verticals like legal and productivity, and the safety brand premium with Fortune 500 compliance teams — compound independently. The $965 billion Series H valuation is not a speculative blip. It is the market pricing in what the revenue number, the cost-efficiency ratio, and the now-confidential S-1 already made visible: Anthropic is about to become the first public pure-play large-model stock.

For operators, the takeaway is simple. The AI procurement conversation in 2026 has two anchor vendors — Anthropic first, OpenAI second — and the gap is structural, not cyclical. For developers, Claude Code and Claude's 1M-token reasoning are the highest-leverage tools in the stack, and the ecosystem investment thesis around them just got a decade-long tailwind. For investors, a fall 2026 listing at a valuation approaching $1 trillion would be one of the most consequential technology IPOs in years, and the reason the entire capital markets apparatus is already on rails.

The silent coronation is official. The only remaining question is what Anthropic builds with the public-market capital. Based on the pattern so far — disciplined compute spend, relentless enterprise execution, and a brand built on credibility rather than virality — the answer is probably more of the same. Which is exactly why the number is $965 billion and climbing — not the $380 billion of just a few months ago.

Frequently asked questions

Did Anthropic really pass OpenAI in revenue?

Yes. In early April 2026, Anthropic announced that its annualized revenue had crossed $30 billion, more than tripling from $9 billion at the end of 2025. Over the same window, OpenAI's annualized revenue was approximately $25 billion. This is the first time Anthropic has overtaken OpenAI in revenue scale since the two companies began competing in the foundation-model market.

What is Anthropic's valuation after the Series H round?

Anthropic closed a $65 billion Series H round in late May 2026 at a $965 billion post-money valuation — roughly 2.5 times the $380 billion Series G it closed in February 2026. The round was co-led by Altimeter Capital, Dragoneer, Greenoaks, Sequoia Capital, Capital Group, Coatue, and D1 Capital Partners. That figure puts Anthropic within striking distance of a $1 trillion valuation.

When is the Anthropic IPO expected?

Anthropic confidentially submitted a draft Form S-1 to the SEC on June 1, 2026, the first formal step toward an IPO. The company says the offering will depend on market conditions, and the number of shares and the price have not yet been set. A listing could price as early as fall 2026. At a valuation approaching $1 trillion, it could rank among the largest technology IPOs ever, though the final size is not yet confirmed.

Who is Chris Liddell and why did Anthropic add him to the board?

Chris Liddell is a veteran executive who served as chief financial officer of Microsoft from 2005 to 2009, vice chairman and CFO of General Motors during its $23 billion IPO in 2010, and deputy White House chief of staff for policy coordination during the first Trump administration. Anthropic appointed him to its board of directors in February 2026. His combination of public-markets experience, Fortune 50 operating experience, and Washington fluency makes him a standard pre-IPO governance hire for a company planning a large and politically sensitive public listing.

Why is Anthropic growing so fast — what are the three levers?

Three levers compound to produce the growth. First, Claude Code has become the enterprise-standard agentic coding surface for Fortune 500 engineering organizations. Second, Anthropic has seeded vertical application-layer leaders — Harvey in legal, Notion in productivity, and others — that drive API consumption at scale, with 8 of the Fortune 10 now Claude customers and over 500 accounts spending more than $1 million per year. Third, Anthropic's safety brand positioning — rooted in Constitutional AI, interpretability research, and published alignment work — commands a premium with Fortune 500 procurement and compliance teams.

How does Anthropic spend less than OpenAI on training?

Anthropic is reaching $30 billion in annualized revenue while spending approximately four times less than OpenAI on model training, according to reporting from SaaStr and corroborating sources. The efficiency comes from a more deliberate compute fleet, a research culture that optimizes for capability-per-flop rather than pure scale, and a more disciplined Claude release cadence. The company projects profitability around 2028 or 2029, which the cost structure plausibly supports.

What does this mean for OpenAI?

OpenAI at $25 billion in annualized revenue is still a generational business, and ChatGPT remains the dominant consumer AI product. What has changed is that OpenAI is no longer the unquestioned revenue leader in the foundation-model category. Practical consequences include tighter pre-IPO valuation multiples, increased competitive pressure on model quality and enterprise GTM, and accelerated multi-vendor AI procurement strategies among Fortune 500 buyers. Expect a visible OpenAI product and commercial response by the third quarter of 2026.

Should I switch from ChatGPT to Claude in 2026?

For consumer-grade chat and creative tasks, ChatGPT remains excellent and switching is not urgent. For enterprise-grade agentic coding, long-context reasoning, and document-heavy workflows in regulated verticals like legal and finance, Claude — and specifically Claude Code with Opus 4.7's 1M-token context — is the stronger tool in 2026. The emerging best practice for serious teams is multi-vendor AI routing, picking the right model per task rather than standardizing on a single vendor. See our Claude, Claude Code, and ChatGPT tool reviews for task-level comparisons.

What is Constitutional AI and why does it matter for enterprise buyers?

Constitutional AI is Anthropic's training methodology for aligning large language models with a written set of principles, published in research papers since 2022. It matters commercially because Fortune 500 compliance and procurement teams running AI risk assessments can point to a documented, published alignment approach when defending the vendor choice to a board of directors or regulator. Anthropic's depth on published safety and interpretability research is a measurable differentiator in enterprise procurement — and one of the three levers behind the $965 billion Series H valuation.