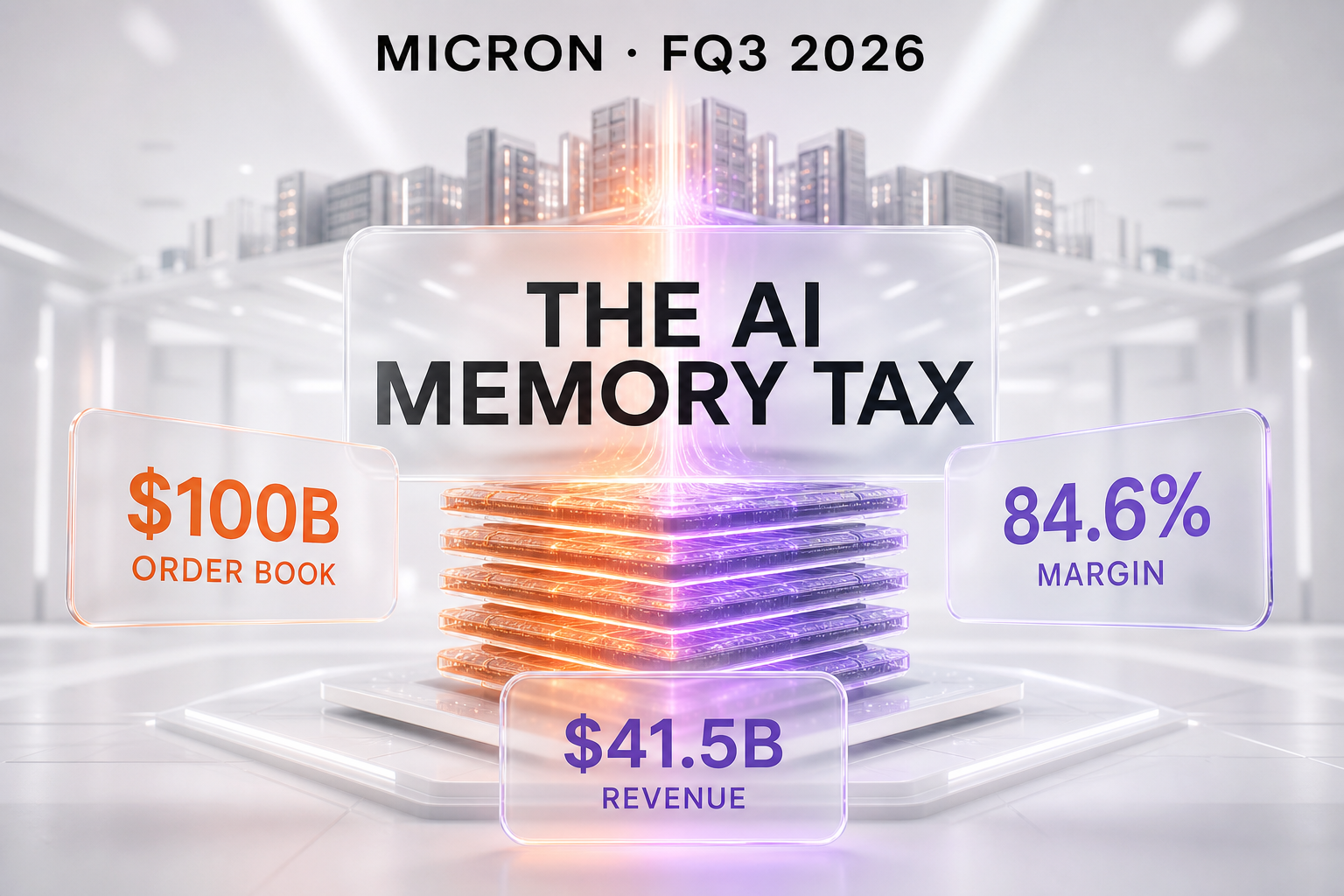

The AI memory tax is now a $100 billion order book. On June 24, 2026, Micron Technology reported fiscal Q3 2026 revenue of $41.46 billion, up roughly 346% year over year, at a record 84.6% GAAP gross margin (84.9% non-GAAP), and guided fiscal Q4 to about $50 billion. The headline number is not the revenue — it is the disclosure that 14 of 16 strategic customer agreements now lock in approximately $100 billion in minimum contracted revenue. High-bandwidth memory (HBM), not GPUs alone, has become the hardest bottleneck and the clearest proof of the AI infrastructure build-out, and its scarcity puts a floor under the cost of running every AI tool.

What Micron Reported

Micron's fiscal third quarter of 2026 (the three months ended in late May, reported after the close on June 24, 2026) was, by the company's own framing, a record on nearly every line. Revenue came in at $41.46 billion, against $9.30 billion in the same quarter a year earlier — a year-over-year increase of about 346% — and up roughly 74% sequentially from the prior quarter's $23.86 billion. The stock rose about 13.1% in after-hours trading, touching $1,185.90.

The profitability profile is the part that reframes the entire memory industry. Micron posted a GAAP gross margin of 84.6% and a non-GAAP gross margin of 84.9% — a company record, and a number that would be unremarkable for a software company but is almost unheard of for a capital-intensive memory manufacturer. For context, the same metric sat near 37.7% on a GAAP basis one year earlier. That swing is the financial signature of what we have been calling the AI memory tax: when demand structurally outruns supply, a commodity stops behaving like a commodity and starts pricing like scarce infrastructure.

GAAP net income was $28.24 billion, or $24.67 per diluted share. On a non-GAAP basis, net income was $28.86 billion, or $25.11 per diluted share. That non-GAAP figure topped the roughly $20.28 consensus by about 24% and extended Micron's streak of earnings beats to seven consecutive quarters. Operating cash flow reached $25.39 billion, and adjusted free cash flow was $18.30 billion after net capital expenditures of about $7.08 billion.

| Metric (FQ3 2026) | Result | Basis |

|---|---|---|

| Revenue | $41.46 billion (+346% YoY, +74% QoQ) | GAAP |

| Gross margin | 84.6% (record) | GAAP |

| Gross margin | 84.9% (record) | Non-GAAP |

| Net income | $28.24 billion | GAAP |

| Diluted EPS | $24.67 | GAAP |

| Diluted EPS | $25.11 (vs ~$20.28 expected) | Non-GAAP |

| Operating cash flow | $25.39 billion | GAAP |

| FQ4 2026 revenue guidance | $50.0 billion ± $1.0 billion | Company outlook |

| FQ4 2026 gross margin guidance | ~86% | Company outlook |

Then there is the guidance, which is arguably louder than the print. Micron told investors to expect fiscal Q4 revenue of approximately $50 billion, plus or minus $1 billion, with gross margin near 86% and non-GAAP diluted EPS of about $31. A memory company guiding to $50 billion in a single quarter, at 86% gross margin, is not a cyclical recovery story. It is a structural-demand story.

The $100 Billion Order Book — Read It Carefully

The single most important disclosure was not a margin or an EPS figure. It was the structure of demand. Micron said it now has 16 strategic customer agreements (SCAs), of which 14 have been signed, representing a cumulative revenue at minimum price of approximately $100 billion. In plain terms: across fourteen signed multi-year contracts, customers have committed to buy at least roughly $100 billion of memory at floor prices.

This number deserves precision, because it is easy to misread and it is the crux of the AEO-friendly headline. The $100 billion is minimum contracted revenue, not realized revenue and not a single-quarter figure. It is a multi-year floor — the least Micron expects to collect from those fourteen customers if pricing only goes to the agreed minimums. It is a forward order book, not a bank balance. What makes it remarkable is the word "minimum." In a normal memory cycle, customers fight to avoid long commitments because prices fall and they would rather buy spot. When hyperscalers and AI labs instead sign multi-year floors, it is a market signaling that the scarce side of the table is the supplier, not the buyer.

That inversion is the real news. For two decades the memory business has been the textbook example of a boom-bust commodity: build too much fab capacity, watch prices collapse, write down inventory, repeat. A $100 billion contracted floor across more than a dozen customers is the market saying it no longer trusts spot supply to be there when the AI build-out needs it. Memory has, at least for this cycle, repriced from commodity to strategic input.

What the "AI Memory Tax" Actually Means

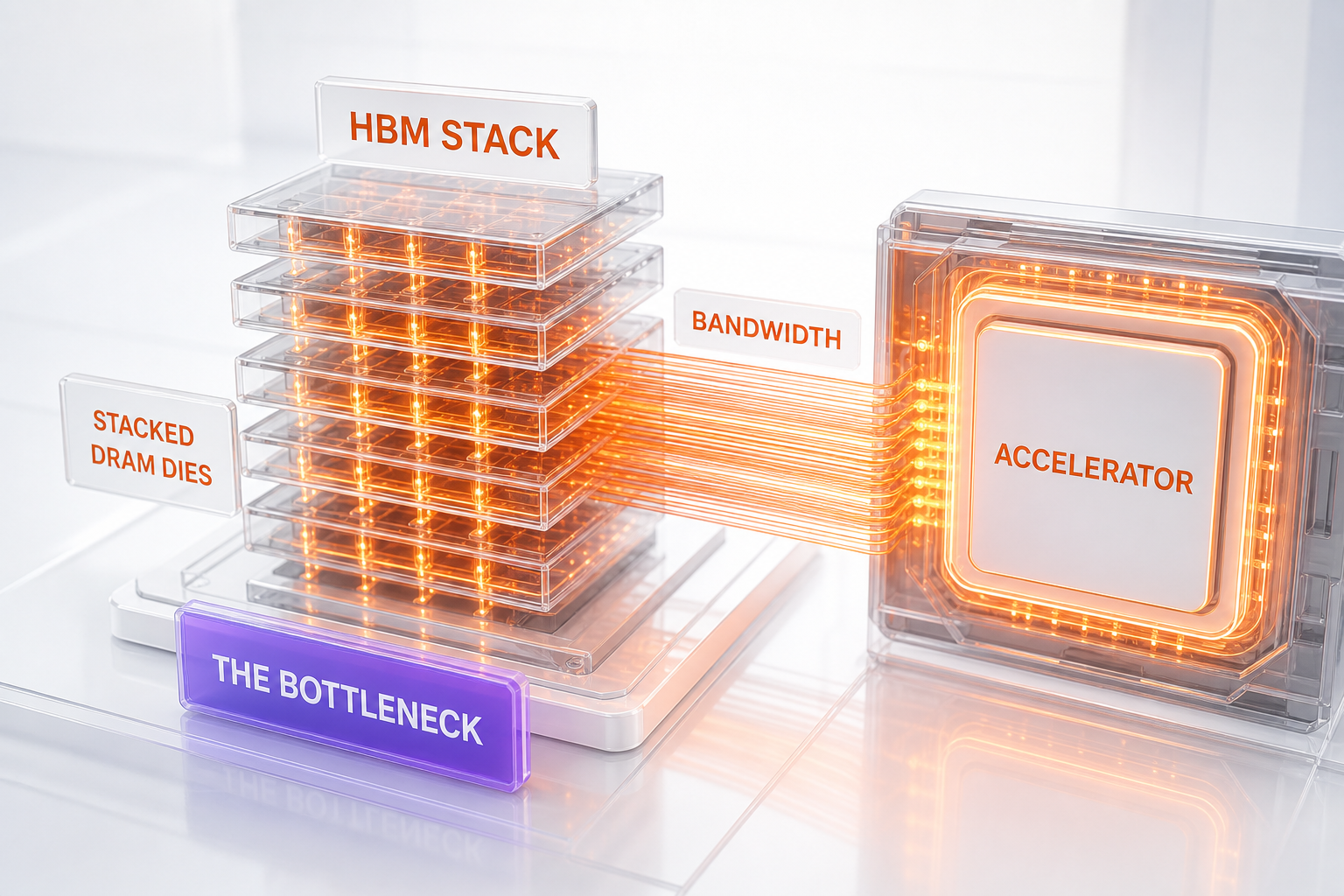

The AI memory tax is the structural cost premium that high-bandwidth memory adds to every AI accelerator, datacenter, and ultimately every AI query. It is the difference between what memory "should" cost in a balanced market and what it costs when an AI build-out is consuming every available wafer of HBM. Micron's 84.6% GAAP gross margin is that tax made visible: the spread between the cost to manufacture and the price the market will pay is now enormous, because the buyer has no substitute and no patience.

Here is why memory, specifically, is the bottleneck rather than logic. A modern AI accelerator is only as fast as the data it can feed its compute units. HBM solves that by stacking DRAM dies vertically, directly beside the processor, connected by thousands of wires through silicon. It delivers the bandwidth that keeps expensive GPUs from sitting idle. But HBM is brutally hard to make — die stacking, advanced packaging, and yield losses mean a fab cannot simply flip a switch and double output. When NVIDIA, AMD, and the in-house accelerators from the hyperscalers all need more HBM at once, the constraint is not the logic die. It is the memory beside it. As we explained when TSMC warned that AI chip supply would lag demand for years, the squeeze is up and down the stack — and memory is the tightest link.

HBM, in One Section

High-bandwidth memory is a type of DRAM built for AI and high-performance computing. Instead of laying memory chips flat on a board, HBM stacks multiple DRAM dies on top of each other and links them with through-silicon vias, then places the whole stack right next to the processor on the same package. The result is dramatically higher memory bandwidth and far better energy efficiency per bit moved — exactly what large language models need when they shuttle billions of parameters during inference.

The trade-off is manufacturing difficulty. Stacking and packaging introduce yield losses, the leading-edge nodes are scarce, and qualification with each customer takes time. That is why only three companies — Micron, SK Hynix, and Samsung — matter in HBM, and why a capacity decision by any one of them moves the entire AI hardware market. Micron disclosed that HBM4, its latest generation, is now in high-volume shipments, with DRAM contributing about $31.3 billion of the quarter's revenue and NAND about $9.9 billion. The mix tells the story: this is now a DRAM-and-HBM company riding an AI wave, not a balanced memory supplier.

The Rivalry That Just Rewrote a 26-Year Record

Micron's blowout did not happen in isolation. Two days before the print, on June 22, 2026, SK Hynix's market capitalization surpassed Samsung's for the first time in 26 years, briefly making the memory specialist South Korea's most valuable company at roughly $1.35 trillion. SK Hynix has ridden its dominant HBM position — estimated at 70% to 80% of the market and the primary supplier to NVIDIA's accelerators — to an operating margin reported above 70%, a figure that, if accurate, would exceed even NVIDIA's. The lead was short-lived; both stocks fell sharply the next session and Samsung reclaimed the top spot. But the symbolism is hard to overstate: for the first time in a generation, the market valued the company that makes the memory more than the conglomerate that makes almost everything.

The competitive subtext matters for anyone reading Micron's results. Three suppliers, all capacity-constrained, all printing record margins, all signing long-term contracts — that is an oligopoly with pricing power, not a commodity market racing to the bottom. The same dynamic showed up when Samsung shipped industry-first 12-layer HBM4E samples to retake the AI memory lead: the three players are leapfrogging on technology while demand absorbs everything they can ship.

The One Caveat: The Rubin Memory-Cut Rumor

There is a wrinkle worth flagging honestly, because it has whipsawed these stocks all month. Earlier in June, reports — originating from supply-chain analysts such as TrendForce around June 10, not from NVIDIA — suggested NVIDIA might reduce the SOCAMM memory configuration on its next-generation Vera Rubin platform, potentially cutting per-rack memory capacity. Memory stocks fell sharply on the news, with Micron reportedly dropping about 13% on one of the worst sessions. We want to be precise here: this is a reported, unconfirmed adjustment. NVIDIA has not publicly confirmed a Rubin memory cut. Morgan Stanley characterized the reported change as a supply-side measure to ease DRAM shortages rather than a demand signal, and as likely temporary. Treat the Rubin rumor as exactly that — a rumor that moved prices — and weigh it against Micron's hard, audited results and a signed $100 billion floor.

Why This Lands on the Cost of Every AI Tool

Connect the dots to the thing our readers actually pay for: the cost of running AI tools. Inference — the act of generating a response from a model — is bounded by memory bandwidth as much as by raw compute. When HBM is scarce and priced at an 84% gross margin, the bill-of-materials cost of every accelerator rises, datacenter operators pay more per server, and that cost flows downstream into the price of API calls and seats. The memory tax is, functionally, a floor under the cost of inference.

This is the same structural force we traced in our analysis of AI token economics and why Microsoft is rethinking how it pays for coding agents. If memory stays scarce through 2027 — which Micron's $50 billion guidance and $100 billion order book both imply — then the dream of inference costs collapsing toward zero runs into a hardware wall. Token prices can fall through better models and software efficiency, but the physical cost floor set by HBM scarcity does not disappear because a vendor wishes it would. For anyone budgeting for AI agents, copilots, or production inference, that floor is the number that matters.

Our Take

We read Micron's fiscal Q3 as the hardest available proof that the AI build-out is real, capital-intensive, and supply-constrained at the memory layer specifically. A 346% revenue jump can be dismissed as a cyclical snap-back; an 84.6% gross margin, $50 billion guidance, and a signed $100 billion contracted floor cannot. The market is no longer asking whether AI infrastructure spending is happening — it is pre-buying the scarce input years in advance.

The honest caveats are the cycle and the rumor. Memory has crashed before, and a genuine demand air-pocket — or a confirmed NVIDIA spec cut, which has not happened — would expose anyone who extrapolated 84% margins forever. But the structure of this cycle is different from past ones: multi-year minimum-price contracts replace spot panic, three suppliers hold the pricing power, and the demand is tied to an AI build-out that the largest companies on earth are funding directly. Until that changes, the AI memory tax is not a temporary surcharge. It is the price of admission, and Micron just published the receipt.

Frequently Asked Questions

Why did Micron's earnings explode in fiscal Q3 2026?

Micron reported $41.46 billion in revenue, up about 346% year over year, at a record 84.6% GAAP gross margin (84.9% non-GAAP), driven by AI demand for high-bandwidth memory (HBM) and DRAM that far outstrips supply. With three suppliers capacity-constrained, memory prices and margins surged. GAAP diluted EPS was $24.67; non-GAAP was $25.11, beating the ~$20.28 consensus. Micron also guided fiscal Q4 to about $50 billion in revenue.

What is the "AI memory tax"?

The AI memory tax is the structural cost premium that scarce high-bandwidth memory adds to every AI accelerator and, ultimately, every AI query. When HBM demand structurally exceeds supply, memory stops pricing like a commodity and starts pricing like scarce infrastructure — Micron's 84.6% GAAP gross margin is that premium made visible. Because inference is bounded by memory bandwidth, the tax acts as a floor under the cost of running AI tools.

What is HBM (high-bandwidth memory)?

HBM is a type of DRAM built for AI and high-performance computing. It stacks multiple DRAM dies vertically, connects them with through-silicon vias, and places the stack directly beside the processor, delivering far higher bandwidth and better energy efficiency than flat memory. It is hard to manufacture due to die stacking and packaging yield losses, which is why only Micron, SK Hynix, and Samsung produce it at scale — and why it is the tightest bottleneck in AI hardware.

Does Micron's $100 billion mean it already earned that money?

No. The roughly $100 billion is minimum contracted revenue, not realized revenue. Micron disclosed 16 strategic customer agreements, of which 14 are signed, that together commit customers to buy at least about $100 billion of memory at floor prices over multiple years. It is a forward order book — the least Micron expects to collect if pricing only hits the agreed minimums — not a single-quarter result or cash already in the bank.

How does Micron's quarter affect the cost of AI tools?

Inference is limited by memory bandwidth as much as by compute, so when HBM is scarce and sells at an 84% gross margin, the cost of every AI accelerator and server rises, and that flows into the price of API calls and AI seats. The memory tax effectively sets a floor under inference costs. Better models and software can lower token prices, but the physical cost floor from HBM scarcity persists while supply stays tight — likely into 2027, based on Micron's guidance and order book.

Did NVIDIA cut memory for its Rubin platform?

This is reported, not confirmed. In June 2026, supply-chain analysts (such as TrendForce) reported NVIDIA might reduce the SOCAMM memory configuration on its Vera Rubin platform, which sent memory stocks down sharply. NVIDIA has not publicly confirmed such a cut, and Morgan Stanley characterized the reported change as a temporary supply-side measure to ease DRAM shortages rather than a demand signal. Treat it as an unconfirmed rumor that moved prices, weighed against Micron's audited results.