At its June 4, 2026 annual shareholders meeting in Hsinchu, TSMC CEO C.C. Wei warned that global chip supply will "lag behind" AI-driven demand "for years," calling this year's demand growth "insane." TSMC, the world's largest contract chipmaker, reaffirmed revenue growth of more than 30% for 2026 in US dollar terms after a Q1 reportedly up about 35% year over year. Advanced-node capacity is reportedly sold out through at least 2027, with demand running roughly 25 to 30% above capacity per press estimates. The takeaway: AI chips stay scarce and expensive through 2027.

That sentence — "for years" — is the one that should reset expectations across the AI economy. Not "for a quarter or two." Not "until the next fab ramps." Years. When the company that manufactures the silicon underneath Nvidia, Apple, AMD, Broadcom, and nearly every frontier AI accelerator says it cannot keep up with demand on a multi-year horizon, the scarcity stops being a supply-chain footnote and becomes the central economic constraint of the AI buildout.

What Wei Actually Said

Speaking to shareholders in Hsinchu on June 4, 2026, Wei was unusually direct for a CEO who normally hedges. He described the year's AI demand as "insane" and said that, even with TSMC's expanding manufacturing footprint in the United States, the company "cannot satisfy demand led by American customers." The structural message: chip supply will continue to lag AI-driven demand "for years."

Two phrases there are direct quotes from Wei — "insane" and supply lagging demand "for years." Almost everything else circulating in coverage is press paraphrase of his broader remarks, and it is worth keeping that distinction clear, because the numbers are where reporting and official disclosure diverge slightly. What TSMC confirmed on the record is the financial guidance. What reporters extracted from the meeting are the capacity estimates.

On the confirmed side: TSMC reaffirmed its forecast for full-year 2026 revenue growth exceeding 30% in US dollar terms, and pointed to a first quarter widely reported around 35% year over year. Capital spending guidance for the year runs up to roughly $56 billion — a figure consistent with a company spending aggressively to chase a demand curve it still cannot catch. Wei also told shareholders the company is raising staff bonuses by more than 30%, a small but telling signal of how flush 2026 looks from inside Hsinchu.

On the reported side, the figures that traveled fastest: demand at TSMC's leading nodes is estimated to exceed capacity by roughly 25 to 30% in 2026, and that gap is not expected to ease until 2027 at the earliest. Advanced-node capacity is described as sold out through at least 2027. We treat these as press estimates attributed to the meeting rather than hard numbers TSMC printed in a slide, because that is exactly what they are — and the difference matters for anyone modeling 2027 supply.

The Numbers That Matter

Here is the snapshot, with the official figures separated from the reported estimates so nothing gets laundered into false precision.

| Metric | Figure | Source basis |

|---|---|---|

| 2026 revenue growth (USD) | More than 30% | TSMC official guidance |

| Q1 2026 revenue growth (YoY) | ~35% | Widely reported |

| 2026 capex guidance | Up to ~$56B | TSMC official guidance |

| Leading-node demand vs capacity | ~25 to 30% above capacity | Press estimate |

| Shortage relief timeline | 2027 at the earliest | Press paraphrase of meeting |

| Advanced-node capacity status | Sold out through 2027+ | Reported |

The single most important line in that table is the bottom one. "Sold out through 2027" is not a marketing flourish — it is the entire reason the other rows exist. When the most advanced manufacturing capacity on Earth is fully booked more than 18 months out, every downstream price, every product roadmap, and every AI startup's gross margin inherits that constraint.

Why It Matters: The Bottleneck Moved

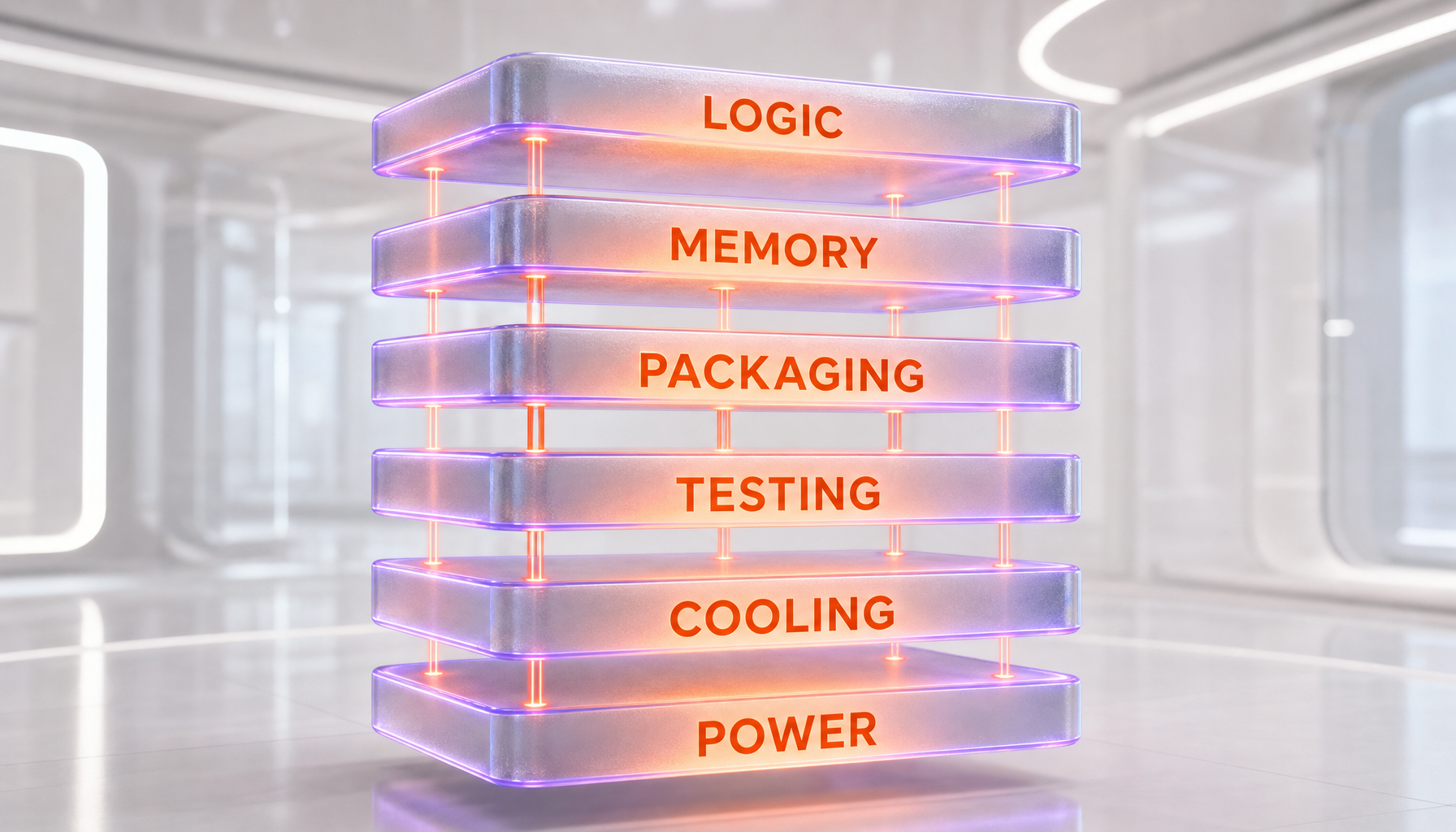

For most of 2024 and 2025, the AI hardware story was a GPU story. Could you get Nvidia H100s, then Blackwell, then enough of them? Wei's framing in Hsinchu quietly redefines the problem. He reportedly described constraints running across the entire ecosystem — logic chips, memory, advanced packaging, testing, cooling, and power. The bottleneck is no longer a single component. It is the whole stack.

That shift is the real news. A GPU shortage can be solved by one vendor ramping one product. A systemic shortage across logic, memory, and packaging cannot. It means that even if Nvidia could ship infinite Blackwell and Rubin dies tomorrow, the advanced packaging needed to assemble them — TSMC's CoWoS lines, by most reporting the tightest link in the chain — would still gate output. Several outlets covering the meeting framed CoWoS advanced packaging as a primary constraint; TSMC did not present it that way in a confirmed quote, but the structural logic is hard to argue with.

This is why "for years" lands so heavily. Building new fabs takes years and tens of billions of dollars. Building advanced packaging capacity, qualifying it, and ramping yield takes years too. There is no overnight fix to a constraint that spans this many process steps, which is precisely why TSMC is guiding to up to $56 billion in capex and still telling shareholders it will fall short of demand.

What This Means for Nvidia, Apple, and Everyone Downstream

Start with Nvidia. Nvidia does not own fabs; it designs accelerators and TSMC builds them. When TSMC says advanced-node and packaging capacity is sold out through 2027, that is a ceiling on how many Blackwell and Rubin systems Nvidia can physically deliver, regardless of order book. We have covered Nvidia's reported $1 trillion in Blackwell and Rubin orders — Wei's comments are the supply-side counterweight to that demand number. A trillion in orders means little if the foundry can only build a fraction of it per year.

Apple sits in a different but equally exposed seat. Apple is historically TSMC's largest customer and typically commands first access to each new leading-edge node for iPhone and Mac silicon. In a sold-out environment, Apple's privileged allocation becomes a competitive moat against AI customers fighting for the same wafers — but it also means Apple's own on-device AI ambitions are now competing internally for the same scarce capacity. Our read on Apple's local-AI push, which we explored in Apple's $8.4B Mac surprise and the local LLM thesis, gets more interesting when the chips powering that thesis are themselves rationed.

Then there is everyone else: AMD, Broadcom, the hyperscalers building custom accelerators, and the wave of startups designing their own silicon. We have written about Mistral exploring its own chips while still running on Nvidia, and the uncomfortable truth Wei's comments expose is that designing your own chip does not get you out of the queue. Everyone — Nvidia, Apple, hyperscalers, and aspiring chip designers alike — ultimately lines up at the same handful of TSMC leading-edge and packaging lines.

Memory deserves its own mention because it is the part of the shortage that has its own pricing dynamics. High-bandwidth memory is as gating to AI systems as logic is, and the competition there is fierce — we covered Samsung's 12-layer HBM4E samples retaking the AI memory lead from SK Hynix. Wei's point that constraints span memory too means HBM tightness compounds the logic and packaging crunch rather than offsetting it.

The Pricing Question — Disciplined, Not Brutal

The most reassuring thing Wei said, if you are a customer, is what he said about pricing. TSMC has begun raising prices on its most advanced chips, with further increases reported for the second half of 2026 — but Wei explicitly signaled the company will not impose sudden, memory-style price spikes. That distinction is deliberate and worth understanding.

The memory market is the cautionary tale here: when DRAM and HBM tighten, prices have historically whipsawed upward violently, then crashed when capacity catches up. TSMC's posture is the opposite — measured, predictable increases designed to fund the $56 billion capex without torching the customer relationships it will depend on for the next decade. In a genuine shortage, a monopoly-adjacent supplier could gouge. TSMC is signaling it would rather raise prices like a utility than like a commodity trader.

For AI builders, that is the difference between a manageable cost-of-goods creep and an existential margin shock. It does not make chips cheap. It makes them predictably more expensive, which is something a CFO can at least model.

The Geopolitical Undertone

Wei's remark that TSMC "cannot satisfy demand led by American customers" even with new US capacity is more loaded than it first appears. TSMC is in the middle of a massive US expansion — its Arizona footprint represents one of the largest foreign manufacturing investments in American history. The CEO is essentially telling Washington that on-shoring helps, but it does not make the math work on a 2026 to 2027 timeline. Fabs are slow; demand is not.

That tension matters because the entire US chip policy thesis assumes domestic capacity can meaningfully reduce dependence and scarcity. Wei's framing is a polite reality check: even the world's best fab operator, building as fast as it can on US soil, cannot out-run AI demand this decade. Meanwhile, the competitive landscape keeps shifting — we have tracked how Huawei is closing the AI-chip gap without EUV, a reminder that scarcity at the leading edge is also a strategic opening for everyone trying to route around it.

Follow the Capital

If you want to understand how seriously the industry takes Wei's "for years," watch where the money is going. The capex commitments across the ecosystem only make sense if you believe demand stays ahead of supply for an extended period. TSMC's up-to-$56-billion plan is one data point. The data-center buildout is another — we covered SoftBank's up-to-€75 billion bet on French AI data centers, capital that assumes the chips to fill those buildings will eventually exist.

There is also a circularity worth flagging. We examined the circular-financing critique around Nvidia's $40 billion in equity bets — the concern that demand is partly being manufactured by the same players supplying it. Wei's "insane" demand, taken at face value, is the bull case against that critique: if a neutral foundry with no incentive to inflate the AI narrative is genuinely sold out through 2027, the demand is probably real, not just financially engineered.

Our Take

We read Wei's "for years" as the single most important macro signal for the AI sector in the first half of 2026 — more consequential than any individual model release. It reframes the entire investment debate. The question stops being "is AI demand real?" and becomes "who gets the silicon, at what price, and in what order?"

The honest read is that scarcity is now a feature of the AI economy, not a bug to be engineered away by next quarter. That favors the incumbents with allocation — Nvidia, Apple, the largest hyperscalers — and squeezes everyone without a seat at TSMC's table. It also validates the strategic logic behind custom silicon, alternative architectures, and efficiency-first model design: if you cannot buy your way out of the queue, your next best move is to need fewer, smaller, or different chips.

What would change our view: a clear sign that the demand-capacity gap is narrowing faster than the "2027 at the earliest" guidance suggests, or evidence that the reported 25 to 30% capacity gap is softer than the meeting implied. Until then, the base case is straightforward — AI chips stay rare and stay expensive, and the companies that planned for that will out-execute the ones that assumed the shortage was temporary.

What's Next

The near-term tells to watch: TSMC's Q2 2026 results and whether management nudges the full-year growth figure higher; any concrete CoWoS packaging capacity expansion announcements, since packaging is the reported choke point; and Nvidia's next set of delivery commitments, which will reveal how much of that $1 trillion order book is physically buildable in 2026 and 2027. If the gap is structural, expect the largest buyers to keep signing multi-year capacity reservations — the surest sign that everyone with money believes Wei meant "for years" literally.

Editorial note: ThePlanetTools.ai has no commercial relationship with TSMC, Nvidia, Apple, or any company referenced in this article. Figures attributed as official come from TSMC's June 4, 2026 shareholders meeting disclosures; capacity-gap estimates are press paraphrase and are labeled as such throughout.

Frequently Asked Questions

What did TSMC say at its June 2026 shareholders meeting?

At its June 4, 2026 annual shareholders meeting in Hsinchu, TSMC CEO C.C. Wei warned that global chip supply will lag behind AI-driven demand for years and described this year's demand growth as insane. He said TSMC cannot satisfy demand led by American customers even with new US manufacturing capacity, while reaffirming full-year 2026 revenue growth of more than 30% in US dollar terms.

How long will the AI chip shortage last according to TSMC?

TSMC's CEO framed the shortage as lasting for years, not quarters. Press estimates from the meeting put leading-node demand roughly 25 to 30% above capacity in 2026, with no relief expected until 2027 at the earliest. Advanced-node capacity is reported to be sold out through at least 2027.

What was TSMC's 2026 revenue growth guidance?

TSMC reaffirmed its forecast for full-year 2026 revenue growth exceeding 30% in US dollar terms, supported by AI infrastructure demand. The first quarter of 2026 was widely reported up about 35% year over year, and 2026 capital spending guidance runs up to roughly $56 billion.

Why are AI chips still scarce and expensive in 2026?

The bottleneck has moved from a single GPU shortage to a systemic one. TSMC describes constraints across the entire stack — logic chips, memory, advanced packaging, testing, cooling, and power. Building new fabs and packaging capacity takes years, so demand keeps outrunning supply even as TSMC spends up to $56 billion on capacity in 2026.

How does TSMC's warning affect Nvidia?

Nvidia designs accelerators but relies on TSMC to manufacture and package them. With advanced-node and packaging capacity reported sold out through 2027, TSMC's output is a hard ceiling on how many Blackwell and Rubin systems Nvidia can physically ship, regardless of its reported $1 trillion order book.

What does the shortage mean for Apple's chip supply?

Apple is historically TSMC's largest customer and usually gets first access to each new leading-edge node. In a sold-out environment that allocation is a competitive advantage, but Apple's own on-device AI ambitions now compete internally for the same scarce capacity, tightening its roadmap as much as anyone else's.

Is CoWoS advanced packaging the main bottleneck?

Several outlets covering the meeting framed CoWoS advanced packaging as a primary constraint, since accelerators must be assembled on these lines before they can ship. TSMC did not present packaging as the bottleneck in a confirmed quote, so it is best treated as reported context, but the structural logic — packaging gating logic and memory output — is consistent with a multi-year shortage.

Will TSMC raise chip prices in 2026?

Yes, but measured. TSMC has begun raising prices on its most advanced chips, with further increases reported for the second half of 2026. Wei signaled the company will avoid sudden, memory-style price spikes, favoring predictable increases that fund its capex without damaging long-term customer relationships.

How is this different from a memory chip shortage?

Memory prices have historically whipsawed up violently during shortages, then crashed when capacity catches up. TSMC is signaling the opposite: disciplined, utility-style increases rather than commodity-trader spikes. For AI builders that is the difference between a manageable cost-of-goods creep and an existential margin shock.

Can building chips in the US solve the shortage?

Not on a 2026 to 2027 timeline. Wei said TSMC cannot satisfy demand led by American customers even with new US capacity. Fabs and advanced packaging take years to build, qualify, and ramp, so on-shoring helps strategically but does not out-run AI demand this decade.

Which AI chip alternatives could ease the dependence on TSMC?

Custom silicon from hyperscalers, high-bandwidth memory advances such as Samsung's 12-layer HBM4E, and alternative architectures like Huawei's EUV-free approaches all aim to route around the bottleneck. But designing your own chip does not move you out of the queue — most leading-edge designs still depend on the same handful of TSMC manufacturing and packaging lines.