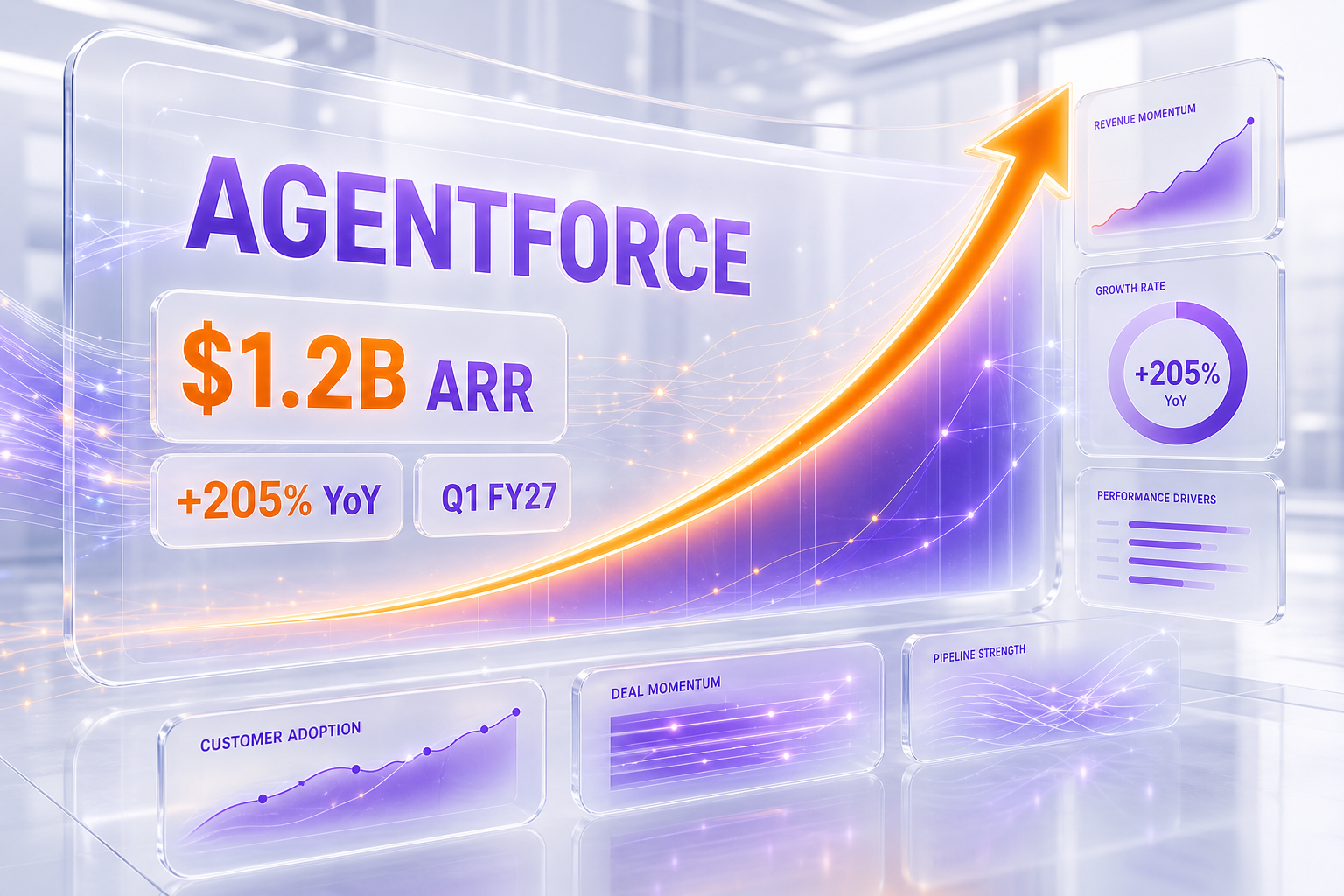

On June 15, 2026, Salesforce signed a definitive agreement to acquire Fin, the customer agent company formerly known as Intercom, for approximately $3.6 billion. Fin runs a proprietary model called Apex, purpose-built for customer support, and serves more than 30,000 companies across live chat, email, WhatsApp, SMS, phone, and Slack. The acquisition feeds Agentforce, Salesforce's AI agent platform, which reached $1.2 billion in ARR in Q1 FY27, up 205 percent year over year. The deal is expected to close in the fourth quarter of Salesforce's fiscal year 2027, subject to regulatory clearances.

The short version: a customer relationship management giant just paid $3.6 billion for a company that builds AI agents to answer support tickets. On the surface that looks like a CRM buying a help-desk tool. Read it as a strategy and it is something else entirely. This is the moment the enterprise AI agent category stopped being a land grab of well-funded startups and started becoming a market that incumbents buy their way into. Fin is the first nine-figure-times-thirty-six acquisition of the consolidation wave, and it will not be the last.

Fin is a customer agent company. Its software resolves complex customer queries end to end, autonomously, across every channel a business uses to talk to people. Agentforce is Salesforce's platform for building and deploying AI agents inside the systems where enterprise work already happens. The reason these two fit together is the same reason the deal is expensive: Salesforce has the distribution and the data, Fin has a battle-tested agent and 30,000 customers who already trust it to talk to their own customers. We have been tracking the agentic enterprise category closely, and this is the first acquisition where the price tag, the buyer, and the timing all point in the same direction at once.

The $3.6 billion deal in context

Salesforce announced the acquisition through an official press release on June 15, 2026, describing it as a definitive agreement to acquire Fin for "approximately $3.6 billion, subject to customary purchase price adjustments." That phrasing matters. A definitive agreement is a signed, binding commitment to buy, not a letter of intent or an exploratory talk. The purchase-price-adjustment language is standard for deals of this size and simply means the final number can move slightly based on cash, debt, and working capital at close.

According to Salesforce's announcement, the transaction is expected to close in the fourth quarter of Salesforce's fiscal year 2027. Salesforce runs on a fiscal calendar that ends in late January, so Q4 FY2027 lands roughly in the opening weeks of the 2027 calendar year. That is a multi-quarter runway, which is normal for an acquisition of this scale because of the regulatory work involved.

What still has to happen before close

The deal is contingent on "satisfaction of customary closing conditions, including the receipt of required regulatory clearances." In plain terms, antitrust and competition regulators in the jurisdictions where both companies operate need to sign off. For a transaction in the low single-digit billions involving a CRM leader and a customer-support agent vendor, this is unlikely to be a marquee antitrust fight, but it is also not a formality. Until those clearances land, Fin and Salesforce operate as separate companies.

Why the price is defensible at this number

Three point six billion dollars is a serious check, but it is not an outlier in the current AI agent market. As context, AI agents are the fastest-growing software category of 2026, and the top 25 companies in the space have collectively raised more than $25 billion. Against that backdrop, buying an established agent platform with more than 30,000 customers and a proprietary model is priced in line with where private valuations in the category already sit. We will get to those comparable valuations later, because they are the key to understanding who Salesforce might be bidding against next time.

What Fin actually is, and why the Intercom history matters

Fin is the company most of the industry knew for fifteen years as Intercom. Intercom built its reputation on customer messaging and support software, the kind of chat widget that sits in the corner of a SaaS product. The rebrand to Fin reflects the company's pivot from a messaging suite to an AI-first customer agent business, naming the company after the product that now defines it.

Salesforce describes Fin as "an industry-leading customer agent company." The distinction between a chatbot and a customer agent is the whole point. A chatbot follows scripts and decision trees. A customer agent reasons about a problem, takes actions across systems, and closes the loop without a human handoff. Fin's AI Agent, per Salesforce, "resolves complex customer queries end-to-end across every channel," and that end-to-end resolution is what enterprises are actually paying for in 2026.

The Apex model, purpose-built for support

Underneath Fin is a proprietary model Salesforce calls "Apex," described as "purpose-built for customer support." That phrase is doing strategic work. The dominant narrative in AI is that general-purpose frontier models will eat every vertical. Fin's bet, and now Salesforce's, is the opposite: a model tuned specifically on the patterns, tone, escalation logic, and edge cases of customer service can outperform a general model on the one job that matters. Buying a purpose-built support model is a hedge against the idea that one giant model wins everything.

The six channels Fin covers

Fin's agent operates across live chat, email, WhatsApp, SMS, phone, and Slack. That channel coverage is not a feature list, it is a moat. Most support automation tools handle one or two channels well and fake the rest. An agent that genuinely resolves issues over WhatsApp and over a phone call and inside Slack is solving a fragmentation problem that every large consumer-facing company has. The breadth is part of what justified the price.

The 30,000-plus customer base

Fin serves "more than 30,000 companies." For Salesforce, that installed base is arguably worth as much as the technology. Each of those companies is a relationship, a deployment, and a potential on-ramp into the broader Salesforce ecosystem. Acquisitions in enterprise software are frequently about distribution as much as product, and 30,000 customer relationships is distribution you cannot build overnight.

Why a CRM pays $3.6B for a support agent

The cleanest way to understand this deal is through Agentforce's numbers. Salesforce's AI agent platform hit "$1.2 billion in ARR in Q1 FY27, up 205% year-over-year." A platform tripling its annual recurring revenue in a single year is not a side project, it is the growth engine the entire company is being repositioned around. When a line item is growing 205 percent, you feed it. Fin is feed.

Marc Benioff, Chair and CEO of Salesforce, framed the logic in the announcement: "We're thrilled to welcome Fin to Salesforce as we enable every company to become an agentic enterprise." Strip the corporate gloss and the thesis is that the next phase of enterprise software is not humans using software, it is companies running on agents, and Salesforce intends to be the platform those agents run on.

Packaged speed versus platform flexibility

There is a strategic tension inside every enterprise AI buying decision, and this deal resolves it for Salesforce by owning both sides. On one side is the fast-to-value packaged agent: deploy Fin, point it at your support channels, and it starts resolving tickets in days. On the other side is the customizable platform: build exactly what you need on Agentforce, integrate it with your CRM data, and own the whole stack. Buyers who want speed and buyers who want control are different customers. By owning Fin and Agentforce, Salesforce gets to sell to both without losing the deal to a specialist.

The data advantage Salesforce brings

The reason this combination is more than the sum of its parts is the CRM data. An agent is only as good as its context, and Salesforce sits on the customer records, case histories, and account data that make a support agent's answers accurate instead of generic. Eoghan McCabe, Chief Executive Officer and Co-Founder of Fin, pointed at exactly this when he said, as reported by TechCrunch: "With the resources of Salesforce this will only accelerate. And yet little will practically change." The "little will practically change" line is a signal to Fin's 30,000 customers that the product they rely on is not getting torn apart, while "this will only accelerate" is the pitch to everyone evaluating whether Salesforce-backed agents will outpace independent ones.

The founder perspective on the category

McCabe was unusually direct about how he sees Fin's place in the market. In the announcement he said: "This is a major win for consumers of the world. Our technology has defined this category and set the new standards for what great customer service looks like today." Founders are not neutral narrators, and a claim to have "defined this category" is the kind of statement an acquired CEO makes on announcement day. But it points at something real: the customer agent category did not exist as a distinct, fundable software segment a few years ago, and the companies that built the first genuinely autonomous support agents got to write the early playbook.

The build-versus-buy signal

Here is where the deal gets analytically interesting, and where it is worth being precise rather than dramatic. Salesforce is building Agentforce in house and buying Fin at the same time. Read in isolation, that can look contradictory. Read as strategy, it is a deliberate two-track approach: build the platform you control, and buy the established agent and customer base you cannot replicate fast enough organically. Plenty of the largest software companies run build and buy in parallel. It is a positioning choice, not a confession.

The timing layer is what makes it worth examining. On June 10, 2026, a few days before the Fin announcement, a WARN notice in California disclosed that Salesforce was eliminating 86 positions across sales, general and administration, and technology and product functions. Reporting indicated the affected teams touched Agentforce, MuleSoft, and Marketing Cloud, though the reports also noted that the core Agentforce teams were not among those cut, with a listed payroll end date of August 7, 2026. A few months earlier, Salesforce had already reduced roughly 1,000 positions as part of a restructuring oriented toward AI investments.

Reading the restructuring as strategy, not contradiction

The factual picture is a company reallocating capital: trimming some internal headcount, including roles adjacent to its agent platform, while writing a $3.6 billion check for an external agent business. That is a capital-allocation decision. The strategic read is that Salesforce has concluded it can acquire mature agent capability and a 30,000-customer base more efficiently than it can grow every piece of it internally, and it is funding that acquisition partly by streamlining. Whether that proves to be the right call depends entirely on integration, which we cannot judge yet. What we can say is that the layoff-plus-acquisition pattern is increasingly the default shape of how large software companies fund their AI repositioning in 2026, and Salesforce is running the standard play.

The agentic consolidation wave

The Fin acquisition does not happen in a vacuum. It is the most visible data point in a consolidation that has been building for a year. The clearest precedent is Cognigy, a conversational AI and customer-service automation company that NICE acquired for $955 million in July 2025. That deal showed that established contact-center and CX vendors were willing to pay close to a billion dollars to own agentic technology rather than build it. Cognigy is not a future target, it is already off the board, and it is the template Salesforce just followed at nearly four times the size.

The broader market context makes the logic obvious. AI agents are the fastest-growing software category of 2026, and the top 25 companies in the space have collectively raised more than $25 billion. When a category attracts that much capital that fast, two things happen in sequence: a wave of startups reaches escape velocity, and then the incumbents with distribution start buying the winners before they become competitors. We are now firmly in phase two.

Why incumbents buy instead of build

For a company like Salesforce, the math on buy-versus-build in a hot category is straightforward. Building a customer agent to Fin's maturity means years of model work, channel integration, and customer trust. Buying it means writing one check and inheriting the model, the channels, and the 30,000 customers immediately. In a market growing as fast as this one, time is the scarcest resource, and acquisition buys time. That is why the consolidation is accelerating rather than slowing.

Who is next: the acquisition targets

The natural question after a deal like this is which company gets bought next. The customer-service agentic category has a clear set of well-funded independents, and their valuations tell you who is in range for whom.

Sierra

Sierra is the heavyweight. Founded by Bret Taylor, the former co-CEO of Salesforce and former chair of OpenAI's board, alongside Clay Bavor, formerly of Google, Sierra raised $950 million and reached a valuation above $15 billion as of May 2026. It is generating roughly $150 million in ARR and has been adopted by about half of the Fortune 50. At a $15 billion valuation, Sierra is arguably too expensive for most acquirers and is more likely to stay independent or eventually go public than to be absorbed. The Taylor connection to Salesforce makes it a fascinating what-if, but the price tag puts it in a different tier.

Decagon

Decagon is the one to watch. It raised $250 million and saw its valuation triple to $4.5 billion in early 2026, adding more than 100 corporate customers including Avis Budget Group and Deutsche Telekom. At a $4.5 billion valuation, Decagon is squarely in the range of what a large incumbent could acquire, and its enterprise logo growth maps almost exactly onto the kind of customer base that justified the Fin deal. If the consolidation wave produces a second major acquisition in this category, Decagon is one of the most logical candidates.

The rest of the field

Beyond the two leaders, the customer-service agentic category includes Crescendo, Cresta, Ada, Parloa, PolyAI, and Moveworks, among others. Each occupies a slightly different position, from contact-center automation to employee-facing support, and each is a plausible target for an acquirer that wants agent capability without paying Sierra-tier prices. The depth of this field is exactly why the consolidation is unlikely to be a one-deal event. There are simply too many fundable, acquirable companies in a category this hot for Salesforce to be the only buyer.

What this means for enterprises evaluating AI support agents

If you are inside a company choosing an AI support agent right now, this deal changes your risk calculus in a few concrete ways. First, the vendor you pick today may belong to a much larger company by the time your contract renews, which can be good for stability and bad for product focus. Second, picking an independent specialist increasingly means betting on a possible acquisition rather than a permanent independent. Third, the platform-versus-point-solution decision now has a new option: buy from a giant that owns both, like Salesforce will once Fin closes.

The questions buyers should ask now

The practical questions worth asking any agent vendor in this climate are about continuity and ownership. Will the model and channel coverage you are buying today be supported and improved in two years, or frozen after an acquisition? Is the vendor pricing for growth or for an exit? Does the agent integrate with the CRM and data systems you already run, or does it assume you will switch? None of these questions have a universally right answer, but in a consolidating market they are the ones that protect you from a deployment that gets orphaned.

Risks and open questions

For all the strategic clarity of this deal, several things remain genuinely uncertain, and it is worth naming them rather than papering over them.

Regulatory clearance

The acquisition is explicitly contingent on required regulatory clearances. While a deal of this size and shape is not the most likely candidate for a drawn-out antitrust battle, the regulatory environment for large technology acquisitions has been unpredictable, and a delay or a conditional approval is possible. Nothing is final until those clearances are in hand.

Integration risk

The hardest part of any acquisition is what happens after the signing. Merging a 30,000-customer agent platform with a proprietary model into the Agentforce stack, while keeping existing Fin customers happy, is a substantial integration program. McCabe's "little will practically change" is reassuring on day one, but the history of enterprise software acquisitions is full of products that changed a great deal over the following two years. How well Salesforce preserves what made Fin work is the open question that will define whether this was a good deal.

The closing timeline

With a close expected in Salesforce's Q4 FY2027, roughly the start of the 2027 calendar year, the two companies operate independently for the better part of a year. In a category moving as fast as this one, a lot can shift in that window, from competitor moves to new model releases. The gap between signing and closing is itself a small strategic risk.

The bigger picture: the agentic enterprise thesis

Pull back from the deal mechanics and the throughline is Benioff's phrase: every company becoming an agentic enterprise. Salesforce is betting that the next decade of enterprise software is defined by autonomous agents doing work that humans used to do inside software, and that the company controlling the platform those agents run on captures enormous value. Agentforce at $1.2 billion in ARR growing 205 percent is the evidence the bet is landing, and the Fin acquisition is Salesforce putting $3.6 billion behind accelerating it.

What makes this a genuine inflection point rather than just a big check is the signal it sends to the rest of the market. When the company that arguably invented modern SaaS spends $3.6 billion to buy its way deeper into AI agents, every other enterprise incumbent has to ask whether it can afford to build rather than buy. The Cognigy and NICE precedent suggested the consolidation was coming. The Fin and Salesforce deal confirms it has started. The only real question left is how many more of these we see before the category settles, and based on the number of fundable independents still standing, the answer is almost certainly several.

How much did Salesforce pay to acquire Fin?

Salesforce agreed to acquire Fin for approximately $3.6 billion, subject to customary purchase price adjustments. The definitive agreement was announced on June 15, 2026.

What was Fin called before the rebrand?

Fin was previously known as Intercom, the name it operated under for fifteen years. The company rebranded to Fin, after its AI agent product, as it pivoted from customer messaging software to an AI-first customer agent business.

What is the Apex model?

Apex is Fin's proprietary AI model, described by Salesforce as purpose-built for customer support. Rather than relying on a general-purpose frontier model, Fin tuned Apex specifically for the patterns and edge cases of customer service.

When is the Salesforce and Fin deal expected to close?

The acquisition is expected to close in the fourth quarter of Salesforce's fiscal year 2027, which falls around the start of the 2027 calendar year. Closing is contingent on customary conditions, including required regulatory clearances.

Is Salesforce laying off employees while it acquires Fin?

Yes. A WARN notice in California on June 10, 2026, disclosed Salesforce was eliminating 86 positions across sales, general and administration, and technology and product functions, with a listed payroll end date of August 7, 2026. Reports indicated the core Agentforce teams were not among those cut. Earlier in the year, Salesforce had already reduced roughly 1,000 positions as part of a restructuring oriented toward AI investments. The simultaneous cuts and acquisition reflect a capital reallocation toward AI rather than a contradiction.

What channels does Fin's AI agent operate across?

Fin's AI agent resolves customer queries end to end across six channels: live chat, email, WhatsApp, SMS, phone, and Slack.

How many customers does Fin have?

Fin serves more than 30,000 companies. That installed base of customer relationships was one of the key assets Salesforce acquired in the deal.

What is Agentforce's ARR?

Agentforce, Salesforce's AI agent platform, reached $1.2 billion in annual recurring revenue in Q1 FY27, up 205 percent year over year. That growth rate is the central reason Salesforce is investing heavily in expanding the platform.

Who are Fin's main competitors?

Fin competes in the customer-service agentic AI category against companies including Sierra, Decagon, Crescendo, Cresta, Ada, Parloa, PolyAI, and Moveworks. Sierra is valued above $15 billion and Decagon at $4.5 billion as of early 2026.

Who is the most likely next acquisition target in the AI agent space?

Decagon is one of the most logical candidates. It is valued at $4.5 billion, within range of a large incumbent acquirer, and added more than 100 corporate customers including Avis Budget Group and Deutsche Telekom. Sierra, at a valuation above $15 billion, is likely too expensive for most acquirers and more likely to stay independent.

Has there been a similar acquisition in this category before?

Yes. NICE acquired Cognigy, a conversational AI and customer-service automation company, for $955 million in July 2025. That deal was an early precedent for incumbents buying agentic technology rather than building it, and the Salesforce and Fin deal follows the same logic at nearly four times the size.

What did Marc Benioff say about the Fin acquisition?

Marc Benioff, Chair and CEO of Salesforce, said in the announcement: "We're thrilled to welcome Fin to Salesforce as we enable every company to become an agentic enterprise." The statement reflects Salesforce's thesis that the next phase of enterprise software is built around autonomous AI agents.