Robinhood's Agentic Trading is a beta feature, announced on May 27, 2026, that lets a US user connect an AI agent to Robinhood's AI-native MCP (Model Context Protocol) servers so the agent can place equity trades on the user's behalf. Alongside it, Robinhood unveiled an Agentic Credit Card: a dedicated virtual Robinhood Gold Card whose spending limits the user alone controls, with optional manual approval on every transaction. Agentic Trading launches equities-only, US-only, and routes orders through a separate account funded only with pre-loaded funds — the first time a US retail broker has turned MCP into a payments and trading rail rather than a developer convenience.

What Robinhood Announced

On May 27, 2026, Robinhood published a newsroom post titled "Robinhood is now open to agents," introducing two products that let autonomous software act inside a brokerage and banking account: Agentic Trading and an Agentic Credit Card. The connective tissue for both is the Model Context Protocol (MCP) — the open standard, originally published by Anthropic in late 2024, that lets large language models and agent runtimes call external tools through a structured server interface.

The pitch is blunt. CEO Vlad Tenev framed it as a continuation of the company's founding line: "Our mission has always been to democratize finance for all, and now, that mission extends to AI agents." VP of Product Abhishek Fatehpuria pointed to customer demand to "bring their own tools, LLMs, and agents" — language that matters, because it signals Robinhood is not building a captive in-house assistant. It is exposing MCP endpoints and letting whatever agent you already use connect in.

Robinhood describes the design as agents being "brought from anywhere." In practice, that means a user points a compatible agent at Robinhood's MCP server, authenticates, and the agent gains a constrained set of capabilities: read account state, place orders within limits, and — for the card — initiate spending up to a ceiling the human set. The framing here is the whole story. Robinhood is not shipping a chatbot. It is shipping infrastructure that turns MCP into a financial control surface.

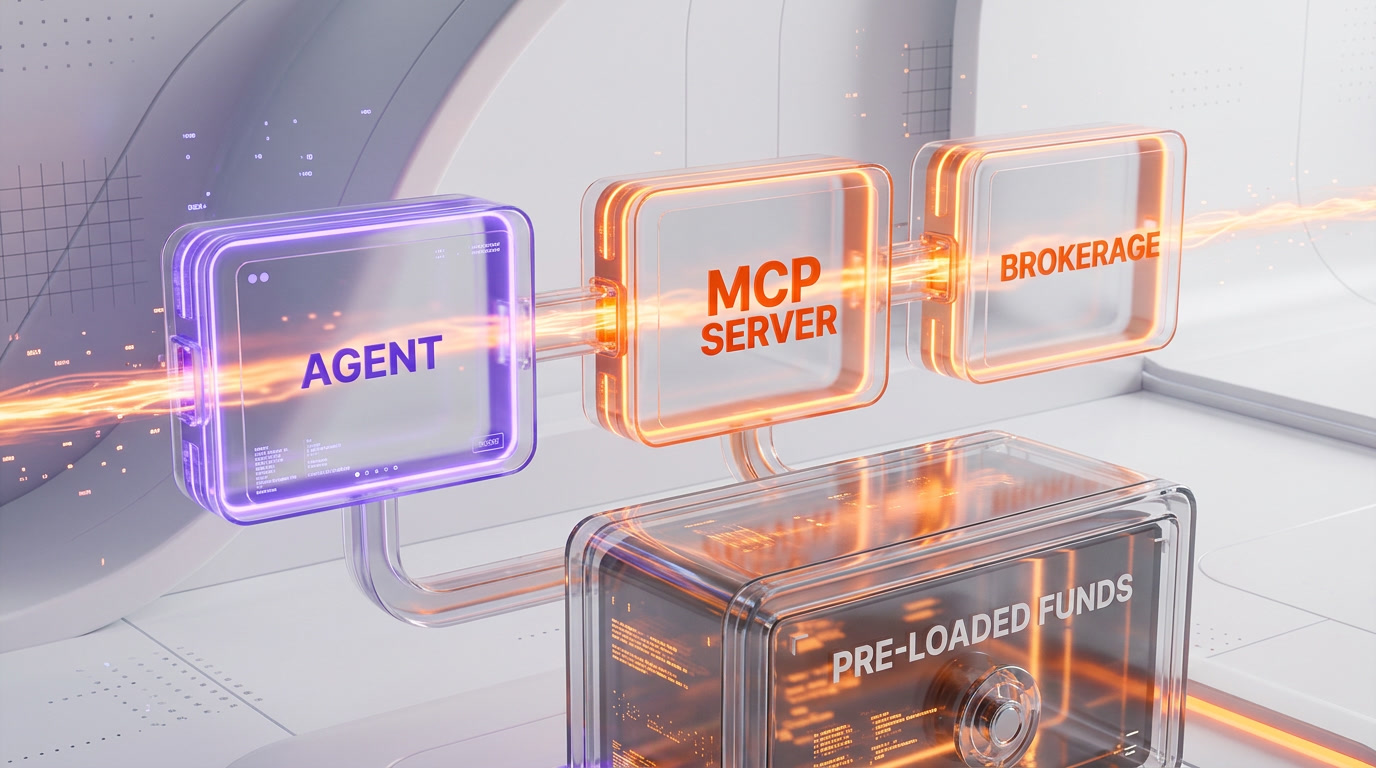

Two guardrails define the launch and deserve to be stated up front, because they are what separate "interesting" from "reckless." First, Agentic Trading is restricted to equities only at launch — options, crypto, event contracts, and futures are listed as "coming soon," not live. Second, the agent operates inside a separate account, or dedicated wallet, and can only deploy pre-loaded funds. An agent cannot reach into your main brokerage balance, your retirement account, or your bank. It plays inside a sandbox you fill on purpose.

Agentic Trading: What the Beta Actually Does

Agentic Trading is the headline. A user connects an AI agent to Robinhood's MCP server, and the agent can then execute trades. At launch the scope is deliberately narrow: US equities only, in beta, in the United States only. Robinhood lists options, crypto, event contracts, and futures as future additions rather than current capabilities, and we are treating those as roadmap, not product, until they ship.

The architecture is the part worth slowing down on. The agent does not trade out of your primary account. It trades out of a separate account — a dedicated wallet — that holds only the money you move into it. Robinhood describes this as the agent operating with pre-loaded funds. The practical effect: if an agent misbehaves, hallucinates a thesis, or gets prompt-injected by a malicious web page, the maximum blast radius is the balance you chose to expose. Your core holdings are not on the table.

That single design decision is the difference between a feature a serious person would touch and one they would not. Autonomous trading is a category that has terrified compliance teams for a decade, for obvious reasons: software placing real orders with real money at machine speed. By walling the agent into a funded sandbox, Robinhood converts an existential risk ("the bot drained my account") into a budgeting risk ("the bot lost the $500 I gave it"). It is the same logic that makes pre-paid cards safer than handing someone your debit card.

It is worth being precise about what "agent" means here. Robinhood is not running the model. You bring it. The MCP server is the contract; the intelligence lives in whatever agent runtime you connect — a coding-style agent, a chat assistant with tool access, or a custom workflow. Robinhood's job is to define what the agent is allowed to ask for and to enforce the limits. For readers tracking how MCP has spread from developer tooling into production infrastructure, this is the same plumbing story we covered when Anthropic acquired Stainless to own the SDK layer behind OpenAI, Google, and Cloudflare — except now the endpoint on the other side is a brokerage.

The Agentic Credit Card: A Spending Rail for Agents

The second product is, in some ways, the more radical one. The Agentic Credit Card is a dedicated virtual Robinhood Gold Card built so an agent can spend on your behalf. The controls are explicit: the user sets spending limits that only the user can change, and the user can require manual approval on every individual transaction. The card runs as a virtual instrument distinct from your physical Gold Card, which keeps the agent's spending lane separate from your everyday card.

On rewards, accuracy matters and the nuance is easy to garble. The 3% cash back figure that has circulated belongs to Robinhood's existing Gold Card program — it is the established Gold Card benefit, not a special agent-only reward invented for this launch. We are flagging that explicitly because the temptation in coverage is to imply Robinhood is paying you 3% to let a bot shop. It is not. You get the same Gold Card economics; the new part is that an agent can now be the one initiating the charge, inside limits you control. Robinhood has also said Platinum Card support is planned for later.

Mechanically, payments work by connecting an agent to the MCP server of Robinhood Banking. This is the line that should make every fintech and payments person sit up. We have spent two years watching MCP grow as a way for AI coding tools to read repos and call APIs. Here, the same protocol becomes a way for an agent to move money. The agent does not get your card number; it gets a permissioned ability to initiate a transaction that your limits and approvals gate. That is a meaningfully different security posture than handing an agent raw credentials — and it is the posture the entire "agentic commerce" wave is converging on.

Why This Matters: MCP Becomes a Financial Rail

Strip away the branding and the significance is structural. For most of its short life, MCP has been understood as a developer convenience — a clean way to give a model access to files, databases, and SaaS APIs. Robinhood's move reframes it. Once a regulated US broker-dealer and a bank exposes MCP endpoints for trading and spending, MCP stops being "dev tooling" and starts being a settlement and execution rail. The protocol that lets an agent read your codebase is now the protocol that lets an agent buy a stock and put a charge on a card.

This is the agentic-commerce thesis arriving in the one vertical where it has the highest stakes: money. We have watched the adjacent moves stack up over the past quarter. When ChatGPT linked to bank accounts through Plaid across 12,000 institutions, that was an assistant reading your finances. When Anthropic slid native skills into QuickBooks, PayPal, and HubSpot for small businesses, that was an agent touching operational tools. Robinhood closes the loop: an agent that can both decide and transact, with real settlement on the other side.

The strategic read for the rest of fintech is uncomfortable. If agents become a primary interface for spending and investing, then the institution that owns the agent-facing endpoint owns a new front door — and the brokerages and banks that do not expose one risk being intermediated away. Robinhood, a company that has always positioned itself as the disruptor's disruptor, is trying to be early to a surface that incumbents like the big custodians and card networks have been slow to touch. Being first to a standard like MCP is a land-grab move, not a feature release.

There is also a quieter signal here about who controls the model. By letting users "bring their own" agent, Robinhood sidesteps the trap of building and maintaining a proprietary assistant that has to compete with frontier labs. It bets on being the most-connected endpoint rather than the smartest brain. In a world where the agent layer is consolidating around a handful of runtimes, owning the rail and staying model-agnostic is arguably the stronger position.

Which Agents Can Connect

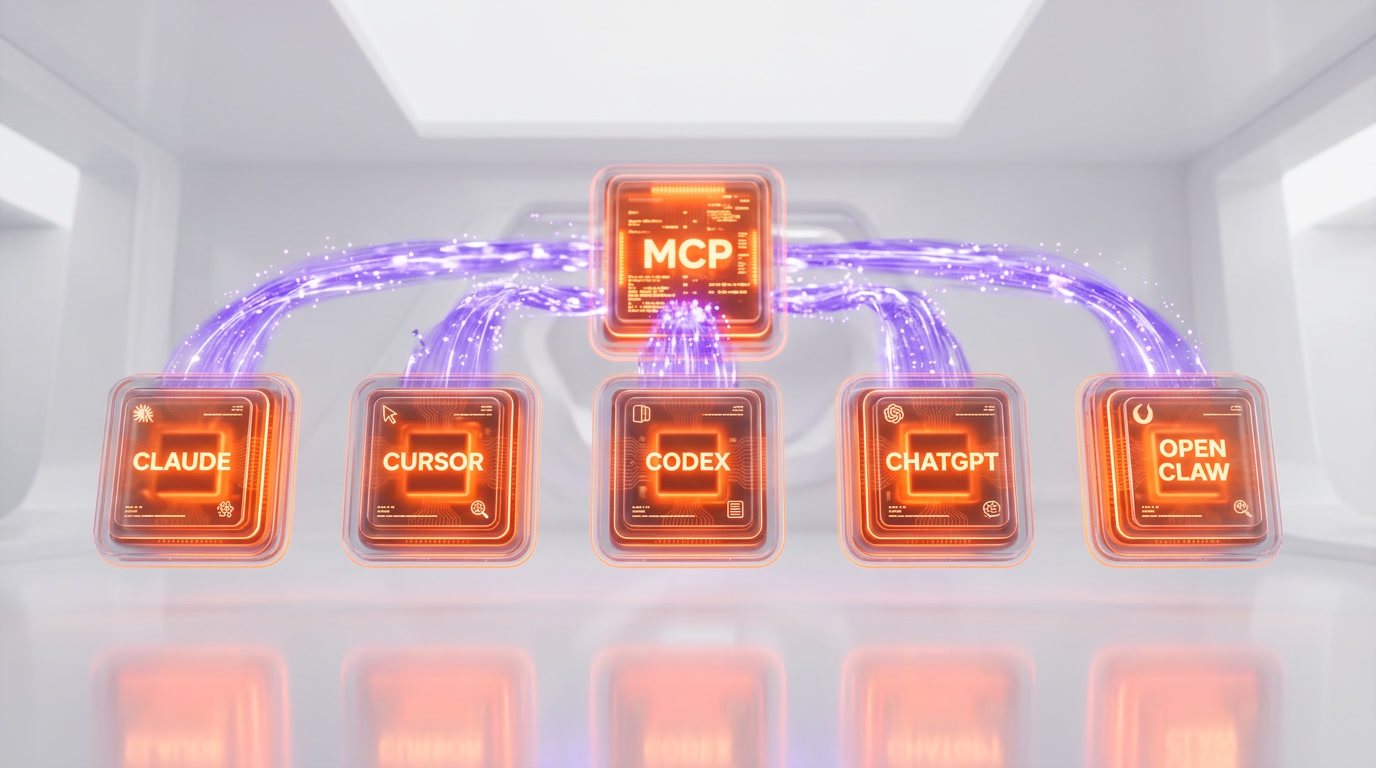

This is the part to handle carefully, because the source quality differs. Per Robinhood's product pages and TechCrunch's coverage of the launch, the list of MCP-compatible agents includes Claude, Cursor, Codex and Codex CLI, ChatGPT, and Open Claw. We want to be transparent: that compatibility list is sourced from Robinhood's product pages and TechCrunch's reporting, not from the main newsroom announcement, so we present it as reported rather than as a guarantee, and the exact set may shift as the beta evolves.

The composition of that list tells you something. It is dominated by agents that started life as coding tools — Cursor, Codex, Codex CLI, Claude in its agentic mode. That is the tell that MCP's center of gravity is moving. The same runtimes engineers used to refactor code are now being pointed at a brokerage. It also explains the design choice to keep agents in a funded sandbox: the people most likely to wire up an agent first are exactly the developers who understand both the power and the failure modes of autonomous tool use.

The inclusion of Open Claw is its own footnote. The open-source agent ecosystem has had a rough security quarter — we documented how a single OpenClaw CVE put tens of thousands of agents one click from takeover. Connecting that class of agent to a money-moving endpoint is precisely why Robinhood's guardrails — separate account, pre-loaded funds, manual approval — are not optional niceties. They are the load-bearing safety layer for a category that has already proven it can be compromised.

The Guardrails, Read Closely

Robinhood's safety model rests on three pillars, and it is worth evaluating each as a skeptic rather than a press release reader.

1. The separate account and pre-loaded funds. The agent trades only with money you deliberately move into a dedicated wallet. This is the strongest of the three controls because it is structural, not behavioral. It does not depend on the agent behaving well or the model being aligned. The cap is enforced by where the money physically is. If you fund the agent account with $1,000, that is the most an agent can lose at the table — full stop.

2. User-set spending limits the user alone controls. On the card side, the limit is yours and only yours to change. An agent cannot raise its own ceiling. This matters because the classic failure mode of autonomous systems is privilege escalation — a clever or compromised agent talking its way into more authority. Hard-coding the limit outside the agent's reach closes that door.

3. Optional manual approval per transaction. You can require a human tap on every charge. This is the slowest setting and the safest, and it is the one we would default to for anyone connecting an open-source or experimental agent. It turns the agent from an actor into a proposer: it suggests, you confirm.

What the guardrails do not fully solve is the decision-quality problem. A perfectly contained agent that makes consistently bad trades will still lose your sandbox money, slowly and within the rules. Containment limits the downside; it does not create alpha. Anyone reading "AI can trade for me now" as "AI can make me money now" is making a category error. The guardrails protect you from catastrophe, not from a bad strategy.

The Bigger Pattern: Agentic Commerce Is Here

Robinhood is not acting in isolation. The first half of 2026 has been one long accumulation of evidence that agents are moving from talking to doing, and specifically to doing things that involve money and identity. Consumer assistants are linking to bank data. Enterprise agents are landing inside accounting and payments software. Marketplace agents are being pointed at shopping — we covered how the rebuilt Meta AI app shipped a marketplace shopping agent to 3.4 billion users. Each of these is a piece of the same picture: the interface to commerce is shifting from a human clicking buttons to an agent calling tools.

MCP is emerging as the connective standard for that shift, and that is the deeper reason Robinhood's announcement matters beyond Robinhood. A standard wins when serious institutions in high-stakes domains adopt it. A broker-dealer and a bank wiring trading and spending through MCP is a far stronger signal of durability than another developer tool adding an integration. It is the kind of adoption that pulls the rest of the market toward the standard, because now there is a regulated, money-moving reference implementation to point at.

The competitive pressure this creates is real. If "connect your agent" becomes a checkbox users expect from a brokerage or a card, the institutions without an MCP endpoint will feel it first in the segment most likely to adopt agents: technically sophisticated, younger, mobile-first users — which is precisely Robinhood's base. The company is playing to its demographic strength and to its historical instinct to be early and loud on a new surface.

The Risks Nobody Should Wave Away

Honest analysis means naming the failure modes, not just the upside. The guardrails are strong, but the category is genuinely new, and new financial surfaces tend to get probed hard by attackers and stressed by edge cases.

Prompt injection into a money endpoint. An agent that reads web content, email, or documents can be manipulated by malicious instructions embedded in that content. When the agent's tools were "read a file," the worst case was data leakage. When the tool is "place a trade" or "make a payment," the worst case is financial. Pre-loaded funds and per-transaction approval are the right mitigations, but they only work if users actually turn approval on rather than chasing the convenience of full autonomy.

Open-source agent exposure. Allowing agents "brought from anywhere," including open-source runtimes with uneven security track records, expands the attack surface. The recent OpenClaw vulnerability is a live reminder that the agent on the other end of the MCP connection may itself be the weak link.

Regulatory ambiguity. Autonomous trading sits in territory that securities regulators have not fully mapped. Who is responsible when an agent executes a trade the user later disputes? Beta, equities-only, US-only is not just a product choice — it reads as a deliberate way to start narrow while the legal and compliance questions get worked out. Expanding to options, crypto, and futures will raise the regulatory temperature considerably.

The "set it and forget it" temptation. The safest configuration is the most annoying one. The product's real-world risk profile depends heavily on whether typical users keep manual approval on or, predictably, switch it off for convenience after the novelty of confirming each action wears thin.

What to Watch Next

A few markers will tell us whether this is a genuine inflection or an early experiment. First, the asset-class expansion: options, crypto, event contracts, and futures are promised. The moment crypto and futures go live through an agent is the moment the risk and the addressable use cases both jump. Second, Platinum Card support, which Robinhood has flagged for later, would signal the card side is graduating from pilot to product. Third, and most telling, whether other brokers and card issuers respond with their own MCP endpoints. If they do, MCP-as-financial-rail stops being a Robinhood story and becomes an industry standard.

The clearest signal of all will be adoption among the developer-adjacent users who own the compatible agents today. If engineers and technical users start routing real trades and real spending through Claude, Cursor, Codex, and ChatGPT into Robinhood, the agentic-commerce era will have its first concrete, money-moving proof point in US retail finance. If they treat it as a toy and keep their serious money far from the sandbox, it will have been an important but premature swing.

Our Take

We have been tracking MCP since it was a niche developer protocol, and the through-line of 2026 has been watching it escape the IDE. Robinhood's announcement is the most consequential step in that escape so far, because finance is the domain where giving an agent real authority is simultaneously the most valuable and the most dangerous. The design — separate account, pre-loaded funds, user-only limits, optional per-transaction approval — is the right instinct, and it is notably more conservative than the marketing energy around "Robinhood is now open to agents" might suggest. That gap between cautious engineering and bold framing is, we think, intentional and smart.

The strategic bet underneath is the one to respect. By staying model-agnostic and letting users bring any compatible agent, Robinhood is wagering that the durable advantage is owning the rail, not the brain. In an agent layer that is consolidating fast, being the most-connected, money-moving MCP endpoint is a defensible position — and being early to it is exactly the kind of move that built Robinhood in the first place. The honest caveat is that beta, equities-only, US-only is a small door, and the cash-back economics are the existing Gold Card's, not a new agent bribe. Read past the headline and what is here is infrastructure, deployed carefully, in front of a wave that is clearly coming. We will be watching the asset-class expansion and the regulatory response far more closely than the launch tweet.

Frequently Asked Questions

What is Robinhood Agentic Trading?

Robinhood Agentic Trading is a beta feature announced on May 27, 2026 that lets a US user connect an AI agent to Robinhood's MCP (Model Context Protocol) servers so the agent can place equity trades on the user's behalf. At launch it is equities-only, US-only, and the agent trades from a separate account funded only with pre-loaded funds.

What is the Robinhood Agentic Credit Card?

The Agentic Credit Card is a dedicated virtual Robinhood Gold Card that an AI agent can use to spend on your behalf. The user sets spending limits that only the user can change, and can require manual approval on every transaction. Payments work by connecting an agent to the MCP server of Robinhood Banking. Platinum Card support is planned for later.

What is MCP and why does it matter here?

MCP, the Model Context Protocol, is an open standard that lets AI models and agents call external tools through a structured server interface. It was originally published by Anthropic. Robinhood's launch matters because it turns MCP from a developer convenience into a financial rail: the same protocol used to give agents access to code and APIs now lets an agent place trades and initiate payments.

Which AI agents are compatible with Robinhood?

Per Robinhood's product pages and TechCrunch's coverage, compatible MCP agents include Claude, Cursor, Codex, Codex CLI, ChatGPT, and Open Claw. This list comes from Robinhood's product pages and reporting rather than the main newsroom post, so it should be treated as reported, and the exact set may change as the beta evolves.

Can an AI agent access my entire Robinhood account?

No. For Agentic Trading, the agent operates inside a separate account, or dedicated wallet, and can only use pre-loaded funds you deliberately move into it. It cannot reach your main brokerage balance. For the Agentic Credit Card, spending is capped by limits only you can change, with optional manual approval on each transaction.

What assets can an agent trade on Robinhood?

At launch, Agentic Trading is equities only. Robinhood lists options, crypto, event contracts, and futures as coming soon, meaning they are roadmap items rather than currently live capabilities. The launch is also limited to the United States and is in beta.

Does the Agentic Credit Card offer special cash back for agent spending?

No. The 3% cash back figure belongs to Robinhood's existing Gold Card program — it is the established Gold Card benefit, not a special reward created for agent spending. The new element is that an agent can initiate the charge inside limits you control, not a new rewards rate.

Who said what about the launch?

Robinhood CEO Vlad Tenev said, "Our mission has always been to democratize finance for all, and now, that mission extends to AI agents." VP of Product Abhishek Fatehpuria cited customer demand to bring their own tools, LLMs, and agents, signaling that Robinhood is exposing MCP endpoints rather than building a captive in-house assistant.

How does an agent make payments through Robinhood?

Payments work by connecting an AI agent to the MCP server of Robinhood Banking. The agent does not receive your raw card number; instead it gets a permissioned ability to initiate a transaction that your spending limits and optional per-transaction approval gate. Robinhood says agents can be brought from anywhere.

Is it safe to let an AI agent trade or spend my money?

Robinhood's guardrails — a separate funded account, user-only spending limits, and optional manual approval — are designed to cap the downside, and the strongest of these is structural: an agent can only lose the pre-loaded funds you exposed. However, containment does not solve decision quality (a contained agent can still make bad trades) and new money-moving endpoints face risks like prompt injection, so keeping manual approval on is the safest configuration.

Why is Robinhood doing this now?

Robinhood is moving early on agentic commerce, a 2026 wave that has seen AI assistants link to bank accounts and enterprise agents land in accounting and payments tools. By exposing MCP endpoints and staying model-agnostic, Robinhood bets that owning the money-moving rail — rather than building a proprietary assistant — is the durable advantage as the agent layer consolidates.

What does this mean for the rest of fintech?

If connecting an agent becomes an expected feature, brokerages and card issuers without an MCP endpoint risk being intermediated away from technically sophisticated, mobile-first users. A regulated broker-dealer and bank wiring trading and spending through MCP is a strong signal of the standard's durability, which could pull other institutions to adopt MCP-based financial rails.