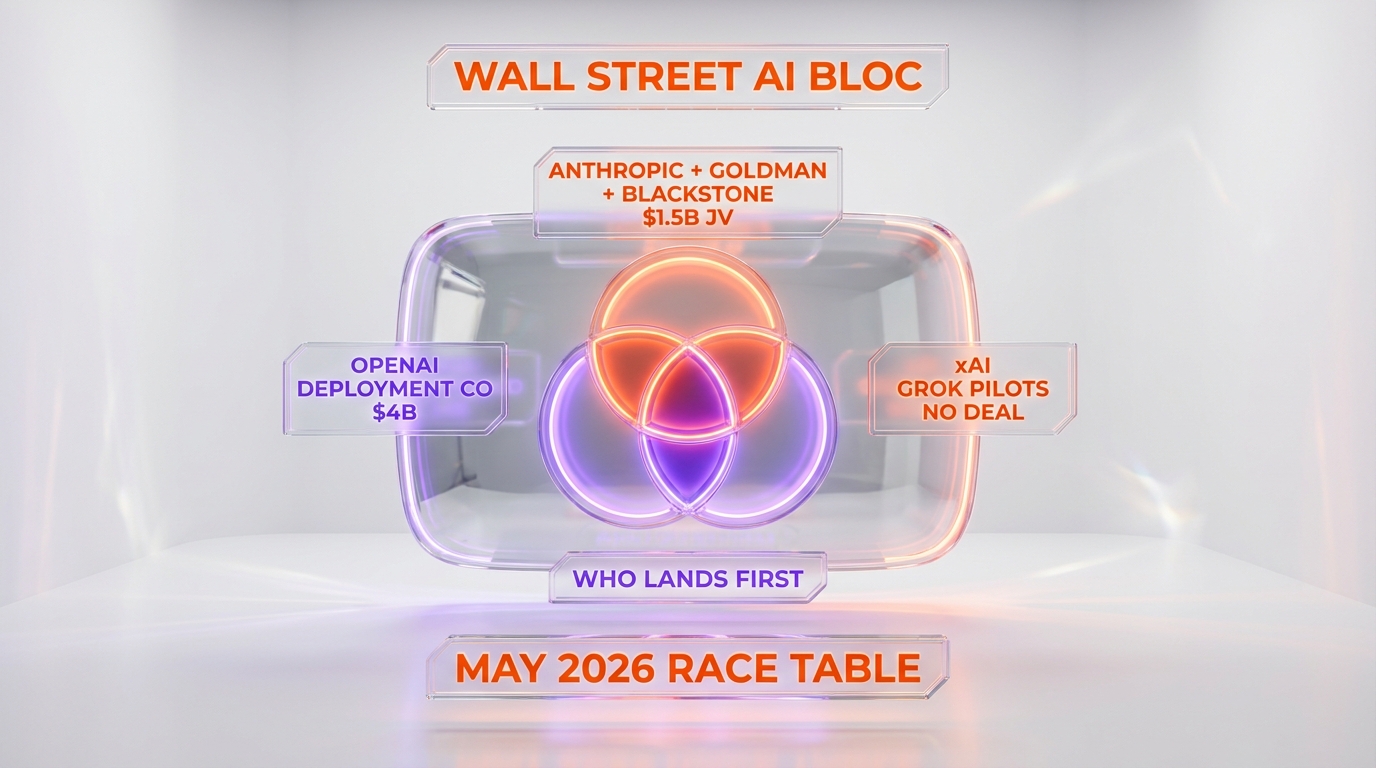

xAI signed up three Wall Street firms — Apollo Global Management, Morgan Stanley, and Valor Equity Partners — to internally test Grok, Bloomberg reported on May 13, 2026, as the company races to build pre-IPO enterprise traction ahead of the looming SpaceX public-markets pathway. The three pilots remain at the internal-evaluation stage rather than at signed commercial contracts, and Bloomberg insiders described uptake as tepid against the velocity that Anthropic locked in with Goldman Sachs and Blackstone through a $1.5 billion AI services joint venture and that OpenAI assembled through the $4 billion OpenAI Deployment Company with Bain, McKinsey, Capgemini, and Tomoro. The xAI push arrives in the same week that the company folded into SpaceXAI under Elon Musk's combined empire and silently throttled the SuperGrok $30 per month paid tier, layering procurement-friction signals on top of the Wall Street pitch.

We have tracked Grok across every release since the v3 cycle, and the May 13 Bloomberg report is the cleanest data point on the gap between xAI's enterprise ambition and its current enterprise traction. Apollo Global Management, Morgan Stanley, and Valor Equity Partners are three of the most recognizable names in alternative assets and capital markets, and securing internal pilots at the three firms is a non-trivial business-development achievement on the xAI sales-motion timeline. The structural complication is that the same three firms — and the broader Wall Street procurement universe they sit inside — have already begun standardizing on Claude through the Anthropic 10-agent finance bundle that Citadel, BNY, and Carlyle deployed and on ChatGPT through the OpenAI Deployment Company's services arm. The xAI pitch lands during the Wall Street AI procurement cycle's mid-point, not at the opening, and Bloomberg's tepid-adoption framing is consistent with that timing disadvantage.

What Bloomberg reported on May 13, 2026

Bloomberg's May 13 reporting identified three Wall Street firms running internal Grok evaluations. Apollo Global Management, the alternative-assets manager with approximately $700 billion in assets under management, is testing Grok across a subset of internal workflows. Morgan Stanley, the wealth-management and investment-banking franchise, is similarly evaluating Grok inside an internal testing perimeter rather than rolling the model out at scale across the firm. Valor Equity Partners, the growth-equity firm founded by Antonio Gracias that has historically been close to the Musk operating ecosystem, is running internal Grok pilots that the Bloomberg reporting characterized as evaluation-stage rather than production-stage. None of the three firms have signed commercial-contract deployments at the time of reporting.

The "tepid" framing in the Bloomberg piece is the operative editorial signal. The reporting did not characterize adoption as accelerating, expanding, or production-grade — it described the deployments as constrained to internal-evaluation perimeters and noted that adoption velocity inside the three firms has not matched the trajectory of competing Anthropic and OpenAI deployments. For procurement teams reading the Bloomberg dispatch, the takeaway is that xAI has assembled three name-recognition pilots without converting any of the three into the kind of commercial-contract proof point that anchors a Wall Street go-to-market narrative.

The May 13 timing carries additional weight because it sits inside the broader pre-SpaceX-IPO window. The xAI plus SpaceX consolidation announced earlier in 2026 and the more recent SpaceXAI structural reorganization position xAI's revenue trajectory as one of the load-bearing inputs into the SpaceX public-markets narrative. Enterprise pilots at Apollo, Morgan Stanley, and Valor are the proof points that Wall Street banking syndicates use to validate enterprise-AI revenue durability ahead of an IPO roadshow. The Bloomberg report is therefore both a sales-motion update and a pre-IPO positioning data point, and the tepid framing complicates both readings.

Why these three firms specifically

The choice of Apollo Global Management, Morgan Stanley, and Valor Equity Partners as the first publicly named Wall Street pilots reflects xAI's sales-motion priorities and the relationship topology of the Musk operating ecosystem. Apollo represents the alternative-assets vertical, where AI workflows can address private-credit underwriting, secondaries pricing, and portfolio-monitoring use cases that scale into multi-million-dollar annual procurement budgets per firm. Landing Apollo as a reference customer would open a procurement-recognition lane into the entire alternative-assets universe, including Blackstone, KKR, Brookfield, and Ares Management.

Morgan Stanley represents the wealth-management and investment-banking vertical, where the procurement decision typically anchors on either Bloomberg Terminal integration or on Microsoft Copilot's Azure integration through the firm's existing Microsoft enterprise license. xAI competing for Morgan Stanley's evaluation perimeter is a meaningful sales-motion accomplishment because Morgan Stanley has historically been an OpenAI-leaning customer through the ChatGPT-style assistant deployments that the firm publicly rolled out across its financial advisor base in 2024 and 2025. Securing Morgan Stanley's internal evaluation is xAI's attempt to disrupt an established OpenAI account at one of the largest Wall Street targets.

Valor Equity Partners is the relationship anchor. Antonio Gracias, the firm's founder, has been a long-standing member of Elon Musk's operating circle through SpaceX, Tesla, and now xAI directorships and advisory positions. Valor's internal pilot is the warm-introduction account that most enterprise-AI companies use to seed initial deployment proof points and to generate the first round of testimonial content for downstream sales motions. The fact that Valor is named alongside Apollo and Morgan Stanley signals that xAI does not yet have a sufficiently long list of independent Wall Street pilots to leave Valor off the public roster, which is itself a data point on the company's enterprise-pipeline maturity.

The broader Wall Street AI race that xAI is now joining

The Wall Street AI procurement cycle has been running at accelerated velocity since the Q1 2026 wave of joint-venture announcements and is now well past the opening phase. Anthropic locked in the consulting-and-asset-management bloc through the $1.5 billion AI services joint venture with Goldman Sachs and Blackstone, a structure that converts what would otherwise be enterprise-software procurement into a services-firm partnership and that captures multi-year recurring revenue through Goldman and Blackstone's combined client base. The Anthropic Wall Street motion was further reinforced by the 10-agent finance bundle that Citadel, BNY Mellon, and Carlyle Group deployed across operational workflows, which produced exactly the production-grade proof-point depth that xAI's internal pilots are not yet at.

OpenAI moved next through the $4 billion OpenAI Deployment Company joint venture with Bain, McKinsey, and Capgemini plus the Tomoro acquisition. That structure operates on a parallel logic to the Anthropic motion but at roughly 2.7 times the headline capital commitment, and it captures the Big-4 consulting distribution layer that Anthropic's Goldman-and-Blackstone structure does not directly address. Combined, the Anthropic and OpenAI motions have effectively pre-allocated the consulting-distributed and the bank-distributed go-to-market lanes for enterprise-AI deployment across the Fortune 500 financial-services tier.

The xAI pitch into Apollo, Morgan Stanley, and Valor sits inside the residual procurement space that the Anthropic and OpenAI structures have not yet closed. That space exists, but it is narrower than the open-field opportunity xAI would have faced in 2024 or early 2025. For procurement teams at the three target firms, the question is not whether to standardize on enterprise AI but which subset of frontier-model vendors to add alongside the Anthropic or OpenAI primary vendor relationship that the firm's parent-organization treasury and procurement teams have likely already signaled toward. The xAI pilot is therefore competing for a secondary-vendor slot, not for a primary-vendor slot, which structurally caps the near-term commercial-contract value of any successful conversion.

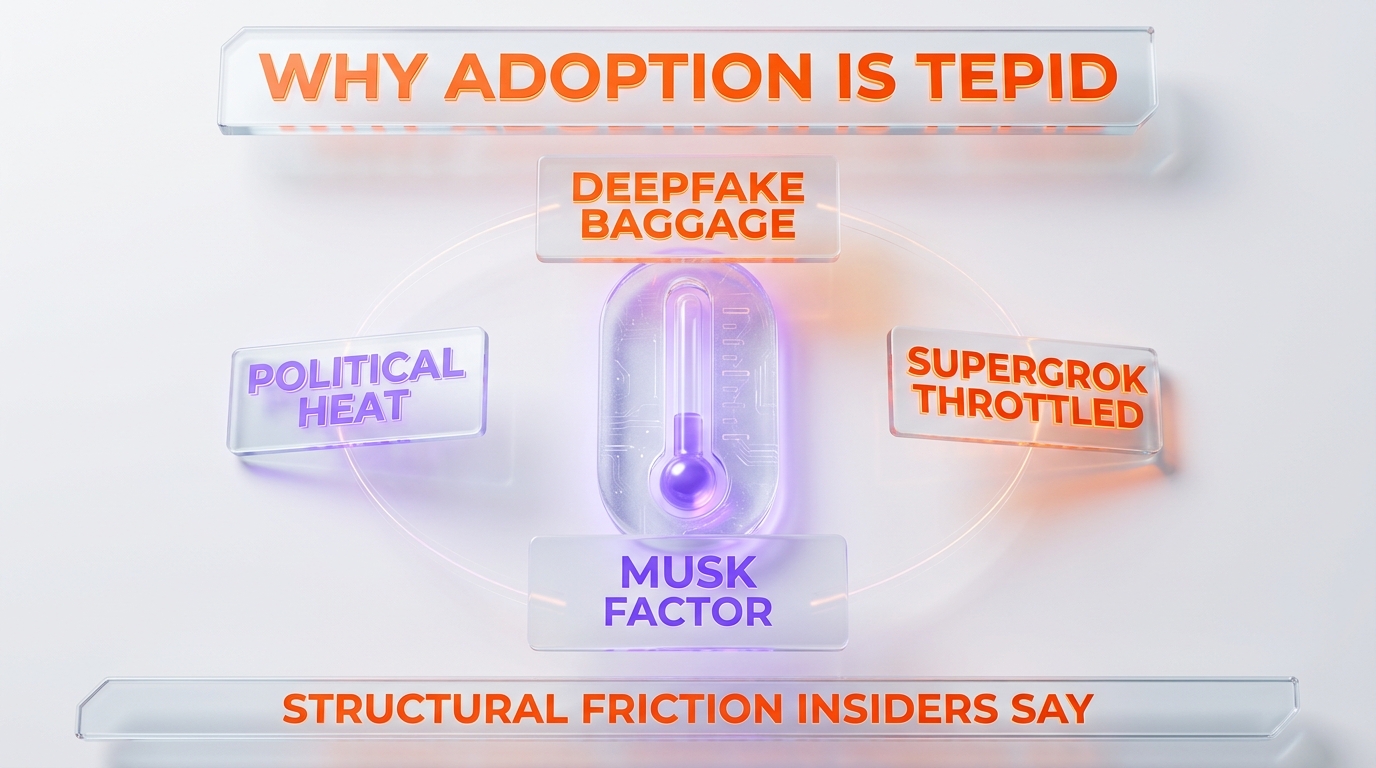

Why insiders describe adoption as tepid — the structural headwinds

The Bloomberg framing of tepid adoption deserves a deconstruction because the underlying factors are specific and identifiable. Four structural headwinds compound against the xAI Wall Street pitch in the May 2026 procurement environment. First, the Grok product line carries documented brand and content-moderation baggage. The Grok deepfake scandal that unfolded across Q1 2026 produced regulatory scrutiny in multiple jurisdictions and class-action litigation that compliance and legal procurement reviewers at Wall Street firms read as inherited reputational risk. Sophisticated procurement reviewers add a documented-litigation-and-regulatory-action filter against vendor selection, and Grok currently sits inside that filter at multiple firms.

Second, the political-content controversy around Grok's endorsement behavior is active and ongoing. Grok is currently the only major chatbot that answers "who should I vote for" prompts with named candidate recommendations, and that posture has drawn editorial coverage and active scrutiny from political-content moderation observers across multiple jurisdictions. Wall Street firms with public-affairs and government-relations exposure read political-content moderation behavior as a procurement-evaluation criterion because the firms have institutional incentives to avoid being associated with vendor-platform political behavior they cannot directly control.

Third, the same-week SuperGrok paid tier throttle event added a consumer-facing data point on xAI's monetization-discipline posture. The May 13 SuperGrok rate-limit tightening — voice mode lockouts after 20 to 30 minutes, daily video caps at 20 clips, daily image edits cut from approximately 100 to 30, and the Heavy tier daily video allowance cut from 500 to 160 — produced a 24-hour Reddit and X backlash that procurement teams read as a signal on vendor communication discipline. The enterprise version of the same concern is whether xAI would unilaterally tighten enterprise rate limits or pricing structures without published notice windows, and the May 13 SuperGrok behavior does not reassure that concern.

Fourth, the Musk factor creates a brand-association friction that some procurement reviewers process explicitly and others process implicitly. Vendor-platform associations with high-profile public-figure owners can be either an asset or a liability in procurement evaluations depending on the firm's institutional posture, and the post-2024 evolution of Musk's public-affairs profile has pushed Wall Street firms with diversified client bases toward greater procurement scrutiny rather than less. The combined effect of the four headwinds is consistent with the Bloomberg tepid-adoption framing.

How Anthropic and OpenAI already locked in the consulting-and-bank bloc

The competitive context that frames the xAI Wall Street pitch is not a level-field procurement environment. Anthropic and OpenAI executed deliberate Wall Street and consulting captures that have effectively pre-positioned both vendors as primary procurement choices across the Fortune 500 financial-services tier. Understanding the structure of those captures is essential for reading the xAI sales motion accurately.

The Anthropic motion combined two structures. The $1.5 billion Goldman Sachs and Blackstone joint venture established a services-firm partnership that bundles Claude deployment into Goldman and Blackstone's combined client offering, which captures a procurement lane that operates outside conventional enterprise-software selection criteria. The 10-agent finance bundle at Citadel, BNY Mellon, and Carlyle established production-grade proof points across the alternative-assets and asset-servicing verticals, which gives Anthropic the reference-customer depth that procurement teams require to default toward Claude on subsequent vendor evaluations.

The OpenAI motion captured the Big-4 consulting distribution layer through the $4 billion OpenAI Deployment Company joint venture with Bain, McKinsey, and Capgemini, augmented by the Tomoro acquisition for delivery capacity. That structure operates on the principle that the consulting firms are the primary integration partner for Fortune 500 AI adoption, so locking the consulting firms into a deployment-arm joint venture pre-allocates the integration partner for downstream enterprise procurement decisions. Wall Street firms that engage Bain, McKinsey, or Capgemini for AI strategy work in 2026 are systematically being routed toward OpenAI Deployment Company's reference architecture, which compounds OpenAI's procurement-default position.

The combined effect is that Anthropic and OpenAI have pre-allocated the two primary go-to-market lanes for Wall Street AI procurement — the bank-distributed lane through Goldman and Blackstone, and the consulting-distributed lane through Bain, McKinsey, and Capgemini. The Apollo, Morgan Stanley, and Valor pilots that xAI assembled are competing for whatever procurement budget remains outside the two primary lanes, which is materially narrower than the budget that would have been addressable in a less-consolidated procurement environment.

The pre-SpaceX-IPO revenue thesis that anchors the xAI push

The strategic logic behind xAI's May 2026 Wall Street push is best read as a pre-IPO revenue-thesis assembly. With xAI now folded into SpaceXAI under Elon Musk's combined operating structure, the company's revenue trajectory is one of the load-bearing inputs into the SpaceX public-markets narrative. SpaceX is reportedly on a near-term IPO timeline, and the public-markets banking syndicates that would lead the roadshow require enterprise-revenue proof points to validate the AI-segment contribution to the consolidated SpaceXAI revenue base.

Enterprise pilots at named Wall Street firms produce the kind of proof-point depth that public-markets banking syndicates use during pre-IPO due diligence to validate enterprise-revenue durability. A pre-IPO disclosure that lists Apollo, Morgan Stanley, and Valor as Grok customers reads materially differently from a pre-IPO disclosure that lists generic enterprise-pilot counts without named anchor customers. The xAI Wall Street motion is therefore optimized for the pre-IPO disclosure timeline, with the named-firm proof points serving a dual purpose — they support the near-term sales motion and they pre-position the company for the IPO roadshow narrative.

The execution complication is that pilot-stage relationships read differently from signed-contract relationships in pre-IPO disclosures, and the Bloomberg reporting characterizes the three pilots as evaluation-stage. Public-markets investors and the banking syndicates that prepare them are sophisticated readers of vendor-relationship depth, and the gap between an internal-pilot disclosure and a signed-commercial-contract disclosure is material to the valuation framework. The xAI motion needs to convert at least one of the three named pilots into a signed commercial contract before the SpaceX IPO timeline closes, otherwise the proof-point disclosure reads as marketing rather than as enterprise-revenue substantiation.

What Grok would need to win the Wall Street procurement cycle

The procurement-evaluation criteria that Wall Street firms apply to enterprise-AI vendor selection are well-understood, even if individual firm rubrics vary in weighting. Five criteria dominate the evaluation rubric, and the Grok product line currently sits at different positions on each. On model performance, Grok 4.20 and the broader Grok line are competitive against Claude and ChatGPT in the consumer benchmark and chat-assistant context but have not yet established the enterprise-workflow benchmark depth that Anthropic and OpenAI have published for finance-specific use cases. Procurement reviewers want to see published evaluation results on use cases relevant to their workflows, and the Grok documentation library is shorter than the Claude and ChatGPT equivalents on finance-specific evaluations.

On data governance and compliance, the Wall Street firms apply heavyweight requirements around data residency, audit logging, model-output explainability, and adversarial-input handling. Anthropic has published detailed governance documentation tied to the Claude finance bundle, and OpenAI has assembled comparable documentation through the Deployment Company services arm. xAI has not yet published an equivalent finance-specific governance dossier, and the absence is a procurement-evaluation friction point that the Apollo, Morgan Stanley, and Valor pilots would need to address before converting to signed commercial contracts.

On total cost of ownership, the xAI pricing posture is competitive at the consumer subscription tier but has not yet been disclosed at the enterprise commercial-contract tier in a way that procurement reviewers can systematically compare against Claude and ChatGPT enterprise pricing. The same-week SuperGrok throttle event adds friction on this criterion because procurement teams that read the consumer-facing tightening as a vendor-discipline signal will apply additional scrutiny to enterprise-tier pricing-and-allowance terms during contract negotiation.

On vendor stability, the xAI corporate structure has evolved meaningfully across 2026, with the consolidation into SpaceXAI and the broader Musk operating-empire restructuring. Procurement reviewers apply vendor-stability criteria to long-term contracts, and corporate-structure volatility — even when the underlying technology and team continuity are preserved — adds a documented risk factor to the evaluation. On strategic alignment with the firm's broader procurement portfolio, the xAI pitch competes against the bundling synergies that Microsoft delivers through Copilot plus Azure, that Google delivers through Workspace plus Vertex, and that AWS delivers through Bedrock plus the broader AWS infrastructure relationship. The standalone xAI procurement decision does not benefit from comparable bundling leverage at most Wall Street firms.

The next 60 days of the xAI Wall Street pitch

The procurement-decision timeline that frames the next 60 days of the xAI Wall Street motion has three sequential gates. Gate one is the internal-evaluation completion across Apollo, Morgan Stanley, and Valor. Each of the three firms will produce internal-evaluation findings that document model performance on firm-specific workflows, data-governance and compliance compatibility, and total cost of ownership against alternative vendors. The internal-evaluation findings will determine whether each pilot progresses to a signed commercial contract, expands into additional internal use cases at the same evaluation perimeter, or sunsets without further procurement activity.

Gate two is the commercial-contract negotiation phase for whichever pilots progress past gate one. Enterprise-AI commercial contracts at the Wall Street tier typically run on multi-year terms with usage commitments that anchor the vendor relationship at a specific deployment-and-pricing envelope. The contracts also include service-level agreements on model uptime, rate-limit predictability, and notice windows for material changes. The same-week SuperGrok throttle event will likely surface as a contract-negotiation topic at all three firms, with the procurement teams demanding explicit service-level commitments that exceed the standard enterprise-tier baseline to neutralize the consumer-tier precedent.

Gate three is the reference-customer disclosure decision. Wall Street firms that sign enterprise-AI commercial contracts are typically reluctant to serve as public reference customers in the first year of deployment because the procurement-decision optics carry institutional risk. The xAI motion will need at least one of the three firms to consent to a public reference-customer relationship to convert the internal-pilot disclosures into the pre-IPO proof-point disclosures that the SpaceXAI roadshow narrative requires. The three-gate timeline through 60 days is aggressive but not impossible, and the May 13 Bloomberg dispatch is the opening signal that the xAI sales motion is targeting that timeline.

The bottom-line strategic read

The May 13 Bloomberg report is a small operational update with an outsized strategic implication. xAI has assembled three name-recognition Wall Street pilots at Apollo Global Management, Morgan Stanley, and Valor Equity Partners in a procurement environment where Anthropic and OpenAI have already pre-allocated the two primary go-to-market lanes through the Goldman and Blackstone joint venture and through the OpenAI Deployment Company. The tepid-adoption framing in the Bloomberg reporting is consistent with the timing disadvantage and with the four structural headwinds — Grok brand baggage, political-content controversy, the same-week SuperGrok throttle, and the Musk factor — that compound against the xAI pitch at compliance and procurement reviewers across the three target firms.

The strategic question for xAI is whether the pre-SpaceX-IPO timeline window is long enough to convert at least one of the three pilots into a signed commercial contract that supports the IPO roadshow narrative. The procurement-decision gates that frame the next 60 days are well-understood and tractable in principle, but the same window is also the window during which Anthropic and OpenAI will move to deepen their existing Wall Street footprint through additional joint-venture or reference-customer announcements. The competitive procurement clock is therefore ticking in both directions, and the xAI motion needs to execute against the gates faster than the competitive bloc expands its footprint to preserve the proof-point lane that the pre-IPO narrative requires.

For our coverage of the broader Wall Street AI procurement cycle that frames the May 13 xAI dispatch, see the Anthropic plus Goldman plus Blackstone $1.5 billion joint venture analysis, the OpenAI Deployment Company $4 billion analysis, the Anthropic 10-agent finance bundle at Citadel, BNY, and Carlyle, and the Sierra Fortune 50 AI agent valuation context. For the xAI structural and product context, see the xAI plus SpaceX merger analysis, the xAI dissolved into SpaceXAI consolidation coverage, and the underlying tool pages for Grok, ChatGPT, and Claude. Bloomberg's original reporting on the Wall Street pilots is available at Bloomberg's May 13, 2026 dispatch.

Frequently asked questions

Which Wall Street firms is xAI courting for Grok in May 2026?

According to Bloomberg's May 13, 2026 reporting, xAI signed up three Wall Street firms to run internal Grok evaluations: Apollo Global Management, the alternative-assets manager with approximately $700 billion in assets under management; Morgan Stanley, the wealth-management and investment-banking franchise; and Valor Equity Partners, the growth-equity firm founded by Antonio Gracias that is structurally close to the Musk operating ecosystem. All three pilots are at the internal-evaluation stage rather than at signed commercial contracts as of the May 13 reporting.

Why did Bloomberg describe the Grok adoption as tepid?

Four structural headwinds compound against the xAI Wall Street pitch in the May 2026 procurement environment. First, the documented Grok deepfake litigation and regulatory action carry inherited reputational risk that compliance reviewers add to their evaluation filter. Second, the active Grok political endorsement controversy adds public-affairs scrutiny. Third, the same-week SuperGrok paid tier throttle on the consumer side surfaced a vendor-communication-discipline concern that procurement teams read as enterprise-tier risk. Fourth, the Musk factor creates a brand-association friction that some procurement reviewers process explicitly. Bloomberg's tepid framing is consistent with the cumulative effect of the four headwinds.

How does the xAI pitch compare to the Anthropic Goldman and Blackstone joint venture?

The Anthropic plus Goldman plus Blackstone $1.5 billion AI services joint venture establishes a services-firm partnership that bundles Claude deployment into Goldman and Blackstone's combined client offering, capturing a procurement lane that operates outside conventional enterprise-software selection. The xAI pitch into Apollo, Morgan Stanley, and Valor competes for procurement budget in the residual space outside the bank-distributed lane that Anthropic has already pre-allocated. The structural advantage Anthropic holds is that the joint venture pre-positions Claude as the default frontier-model vendor across Goldman and Blackstone's combined client base, which compounds the procurement-default position over time.

How does the xAI pitch compare to the OpenAI Deployment Company?

The $4 billion OpenAI Deployment Company joint venture with Bain, McKinsey, and Capgemini plus the Tomoro acquisition captures the Big-4 consulting distribution layer for enterprise AI adoption. The Wall Street firms that engage Bain, McKinsey, or Capgemini for AI strategy work in 2026 are systematically being routed toward OpenAI Deployment Company's reference architecture, which compounds OpenAI's procurement-default position through the consulting-distributed lane. The xAI Apollo, Morgan Stanley, and Valor pilots are competing for procurement budget outside the consulting-distributed lane that OpenAI has already pre-allocated.

What is the connection to the SpaceX IPO timeline?

xAI is now folded into SpaceXAI under Elon Musk's combined operating structure, and the consolidated entity's enterprise revenue trajectory is one of the load-bearing inputs into the SpaceX public-markets narrative. Enterprise pilots at named Wall Street firms produce the proof-point depth that public-markets banking syndicates use during pre-IPO due diligence to validate enterprise-revenue durability. The May 13 Wall Street pilot announcements serve a dual purpose — they support the near-term sales motion and they pre-position the company for the SpaceX IPO roadshow narrative. The execution complication is that internal-pilot disclosures read materially differently from signed-commercial-contract disclosures in pre-IPO due diligence.

Why is Valor Equity Partners included in the named pilots?

Valor Equity Partners is the relationship-anchor account on the named-pilot roster. Antonio Gracias, the firm's founder, has been a long-standing member of Elon Musk's operating circle through SpaceX, Tesla, and now xAI directorships and advisory positions. Valor's internal pilot is the warm-introduction account that most enterprise-AI companies use to seed initial deployment proof points and to generate the first round of testimonial content for downstream sales motions. The fact that Valor is named alongside Apollo and Morgan Stanley signals that xAI does not yet have a sufficiently long list of independent Wall Street pilots to leave Valor off the public roster, which is itself a procurement-pipeline maturity data point.

How does the SuperGrok throttle event affect the Wall Street pitch?

The same-week SuperGrok paid tier throttle on May 13, 2026 — voice mode lockouts after 20 to 30 minutes, daily video caps at 20 clips, daily image edits cut from approximately 100 to 30, and the Heavy tier daily video allowance cut from 500 to 160 — added a consumer-facing data point on xAI's vendor-communication-discipline posture. The enterprise version of the same procurement concern is whether xAI would unilaterally tighten enterprise rate limits or pricing structures without published notice windows. Procurement teams at Apollo, Morgan Stanley, and Valor will likely raise the SuperGrok precedent during commercial-contract negotiations, demanding explicit service-level commitments that exceed the standard enterprise-tier baseline.

What would xAI need to do to convert pilots into signed contracts?

Three actions would materially advance the conversion timeline. First, publishing a finance-specific governance dossier covering data residency, audit logging, model-output explainability, and adversarial-input handling would address the procurement-evaluation friction on data governance. Second, disclosing enterprise-tier pricing structures with explicit usage-allowance terms and notice-window commitments would neutralize the SuperGrok throttle precedent and create the contractual predictability that Wall Street firms require for multi-year commitments. Third, securing a vocal reference-customer disclosure from Valor Equity Partners — the warm-introduction account most likely to consent to public reference status — would convert the internal-pilot disclosures into the pre-IPO proof points that the SpaceXAI roadshow narrative requires.

What use cases are Apollo, Morgan Stanley, and Valor evaluating?

The Bloomberg reporting did not disclose specific use cases inside the internal-evaluation perimeters. The plausible candidate use cases at the three firms fall into categories that frontier models have demonstrated strong performance on across competing deployments. Apollo's alternative-assets context suggests private-credit underwriting, secondaries pricing, and portfolio-monitoring workflows. Morgan Stanley's wealth-management and investment-banking context suggests financial-advisor assistant deployment, research-summary generation, and pitch-deck preparation workflows. Valor's growth-equity context suggests deal-flow screening, portfolio-company diligence, and limited-partner reporting workflows. The exact mapping at each firm will surface in subsequent reporting as the internal evaluations progress.

Could Microsoft Copilot, Google Gemini, or AWS Bedrock complicate the xAI pitch?

Yes, the bundling-synergy competition is a structural complication for the standalone xAI procurement pitch. Microsoft delivers Copilot enterprise alongside the Azure cloud relationship that Morgan Stanley and many Wall Street firms hold as a primary cloud-infrastructure vendor. Google delivers Gemini through the Workspace and Vertex AI bundle that addresses both productivity and model-API procurement in a single vendor relationship. AWS delivers Bedrock with cross-vendor model selection inside the broader AWS infrastructure relationship that anchors many Wall Street cloud architectures. The standalone xAI procurement decision does not benefit from comparable bundling leverage, which raises the threshold on the standalone Grok performance and pricing argument that the company needs to win on the merits.

Is xAI's strategy more about pre-IPO optics or about real enterprise revenue?

The two readings are not mutually exclusive and the strategic logic suggests both. The pre-IPO optics interpretation is that named Wall Street pilots produce the proof-point depth that public-markets banking syndicates require for the SpaceXAI roadshow narrative, which compresses the timeline pressure on converting pilots into reference-customer disclosures. The real enterprise revenue interpretation is that even tepid pilot conversion at Apollo, Morgan Stanley, and Valor would establish recurring-revenue annuities at the Fortune 500 financial-services tier, which compounds across subsequent procurement cycles. The May 13 dispatch is consistent with a company pursuing both objectives simultaneously, with the optics layer running ahead of the revenue layer in the near-term timeline.

Where can I track how the xAI Wall Street pilots progress over the next 60 days?

Three reporting lanes will surface the next 60 days of pilot progression with the most fidelity. Bloomberg's continued coverage of the xAI sales motion provides the journalistic anchor for any pilot-to-contract conversions or competitive-procurement displacements. The financial-services trade press, including American Banker, Institutional Investor, and Financial Times, will cover firm-specific procurement decisions as they surface in Apollo, Morgan Stanley, and Valor public communications. SpaceX pre-IPO disclosures, when they are filed, will document the consolidated SpaceXAI enterprise-revenue base and the named reference customers at the IPO timeline. Our coverage tracks the strategic and procurement-cycle implications, with adjacent context in our Anthropic Wall Street joint venture analysis and our OpenAI Deployment Company analysis.