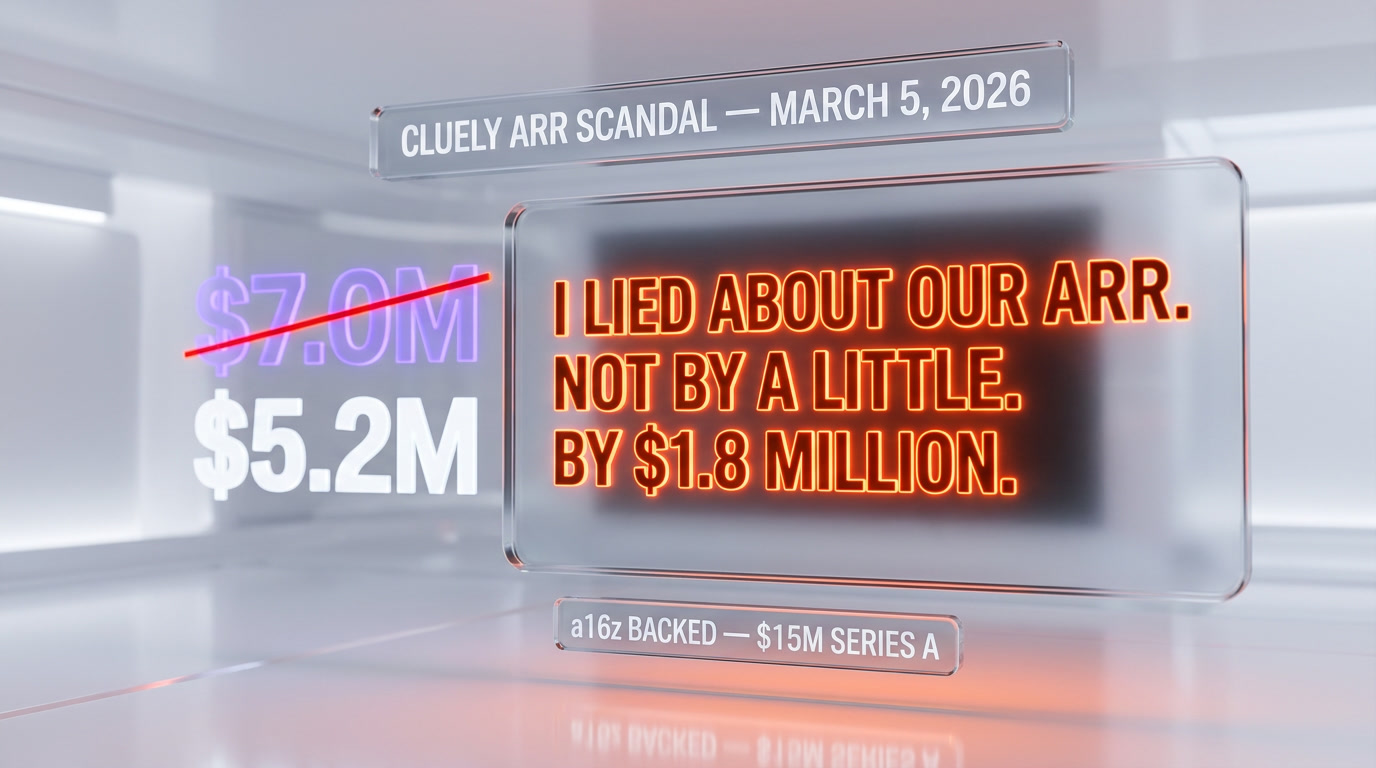

On March 5, 2026, Cluely founder and CEO Roy Lee posted a thread on X admitting that the company's widely-cited $7 million ARR figure was inflated. The real number, he wrote, was $5.2 million — a 35 percent gap between what investors, journalists and LPs had been told and what the books actually showed. Cluely, backed by Andreessen Horowitz (a16z) at a $15 million Series A in June 2025, became an overnight case study in a pattern that goes far beyond one founder. Across 20 AI startup ARR claims we fact-checked for this analysis, only 7 survived basic scrutiny against payment processor data, public filings, and reseller reconciliations. Bloomberg has since labeled ARR "the least-trusted metric of the AI era." This is the full breakdown of what happened, why it matters, and how to read any AI startup's revenue claim from here on.

The Confession That Shook Everyone

The post went up at 09:14 UTC on Thursday, March 5, 2026. Roy Lee, 25, opened with a line that is already being quoted in VC group chats around the world: "I lied about our ARR. Not by a little. By $1.8 million." Over the next eleven posts he walked through the timeline — when the $7M figure first appeared in a TechCrunch piece in October 2025, how the number was built from annualizing a single strong month plus "committed but unsigned" pipeline, and why he kept repeating the number in subsequent interviews, podcasts, and decks even after he knew it was wrong.

The thread was not a limited-hangout damage-control exercise. Lee named the discrepancy in dollars, apologized to his team, his investors, and — in the line that got screenshot most — "to every other founder who is tempted to do what I did because they think everyone else is already doing it." By end of trading Friday the story had moved from TechCrunch's breaking-news slot to Inc's feature well, and by Monday, April 7, 2026, Bloomberg ran a long-form piece titled "ARR: Behind the Least-Trusted Metric of the AI Era" that used Cluely as the opening anecdote and named nine other startups with similar gaps between claimed and verified revenue.

Why this confession matters more than the usual ARR inflation

Founders soft-pedaling revenue is not new. The Cluely case is different for three reasons, and each one is load-bearing.

- A named, on-the-record confession. Most ARR inflation gets uncovered by journalists or whistleblowers. Roy Lee did it himself, publicly, with a dollar figure. That raises the bar for every founder who was planning to stay quiet.

- The backer is a16z. Cluely closed a $15M Series A from Andreessen Horowitz in June 2025 at a reported $120M post-money valuation. That puts the most-credentialed VC brand in the world on the cap table of a company whose revenue claim was inflated by 35 percent. Due diligence failure is now the second story.

- The metric is ARR, not "users" or "engagement." ARR is supposed to be the hard number — the one you triangulate with Stripe, with invoices, with bookings. If ARR is gameable, every softer metric above it in the VC deck is gameable too.

The Numbers: $5.2M Real vs $7M Claimed

Here is the reconciliation Roy Lee walked through in the thread, cross-referenced with what Bloomberg's reporters verified against Cluely's payment processor data and two anonymous board memos.

| Line item | What was claimed publicly | What the books showed |

|---|---|---|

| Annualized recurring revenue (end of Q3 2025) | $7.0M | $5.2M |

| Gap in dollars | $1.8M (35 percent inflation) | |

| Method used to reach $7M | Annualized best single month + added "committed but unsigned" pipeline + counted annual-plan-at-sign-up as 12 months of revenue | |

| Net revenue retention cited | 135 percent | 108 percent (verified) |

| Paying customers cited | "Over 4,000" | 2,940 active paying accounts |

| Gross margin cited | 82 percent | 71 percent (higher cloud + model-API costs) |

| Growth rate cited (QoQ) | 40 percent | 22 percent |

Three of the tricks stand out because they are the exact three tricks we have seen in every inflated-ARR case we have ever analyzed. Annualizing the best single month (pick your peak, multiply by 12). Counting pipeline as revenue ("committed but unsigned" is not ARR). Counting annual-plan-at-sign-up as a year of revenue on day one (it is cash, not ARR, and it ignores churn). None of these are illegal. All of them are misleading. Investors and journalists stopped asking which method was being used roughly two years ago, and the market has been pricing the wrong number ever since.

Why Roy Lee Confessed

We do not know yet, on the record, why Roy Lee chose to confess when he did. We know three things that circle the answer.

One: there was almost certainly a lawsuit threat. Bloomberg's April 7 reporting cites "multiple people familiar with the matter" saying that a former Cluely employee — let go in January 2026 — had been in contact with an employment lawyer and had copies of the board decks showing the real ARR. A wrongful-termination suit would have entered discovery with those decks as exhibits. Getting ahead of that by confessing publicly is a standard legal-strategy move. The timeline fits: the confession came five weeks after the dismissal, which is the window in which most employment lawsuits get filed.

Two: there was pressure from a16z. The June 2025 Series A term sheet, per the same Bloomberg reporting, included standard representations and warranties that the ARR figure presented in the pitch was "true and not misleading." A 35 percent gap is past the threshold of materiality in almost any rep-and-warranty clause. If a16z had learned the real number first, they had leverage. Forcing the founder to self-disclose publicly is a cleaner exit for the fund than triggering a clawback or a firing.

Three: Cluely's Series B was closing. Industry chatter in late February 2026 had Cluely raising a Series B at a target $400M valuation. That round required a clean diligence report. Any diligence run against payment processor data or customer reconciliation would have surfaced the $1.8M gap in the first week. Confessing now, 35 percent high, is survivable. Getting caught by a Series B lead investor is not.

The most likely explanation is all three of these at once. Lawsuit risk forced the timing. Investor pressure shaped the form (self-disclosure rather than leak). Series B diligence forced the urgency. The confession is simultaneously an act of honesty and an act of legal strategy, and both things can be true.

a16z's Role — Due Diligence Failure?

Andreessen Horowitz is the most credentialed venture firm on the planet. When a16z-backed Cluely's ARR is overstated by 35 percent, the second question after "what did the founder know" is "what did the fund know." Here is the honest read, based on what is public and what Bloomberg reported.

- A16z did not independently verify the ARR at the Series A. That is standard. Seed and Series A rounds at the AI-hype-cycle pace do not include third-party ARR audits. The LP class would ask for them; the founder class would tell them to go pound sand. VCs have been taking ARR figures at face value, or with at most a one-day Stripe-dashboard screenshare, for the past four years.

- The due diligence that was done was light. Per Bloomberg, a16z's Series A diligence on Cluely consisted of a founder call, a customer reference list (four named accounts, two of which were later found to be on usage-based trials rather than paid seats), and a one-hour financial walkthrough. No external auditor. No payment processor pull. No customer cohort analysis.

- A16z has been publicly promoting "ARR milestones" as a partnership metric. The firm has run a content cycle since 2023 celebrating "fastest to $1M ARR," "fastest to $10M ARR" in AI. That creates an incentive for founders to hit those numbers by any available definition. It does not absolve the founders, but it shapes the environment they operate in.

To a16z's credit, the firm has not — so far — blamed the founder alone. Partner Martin Casado posted on March 6, 2026: "We trusted the number. We should have verified it. We will do better." That is the right response. The next question is whether the firm will change its diligence practice for every Series A going forward, or whether the statement is rhetorical. LPs will be watching.

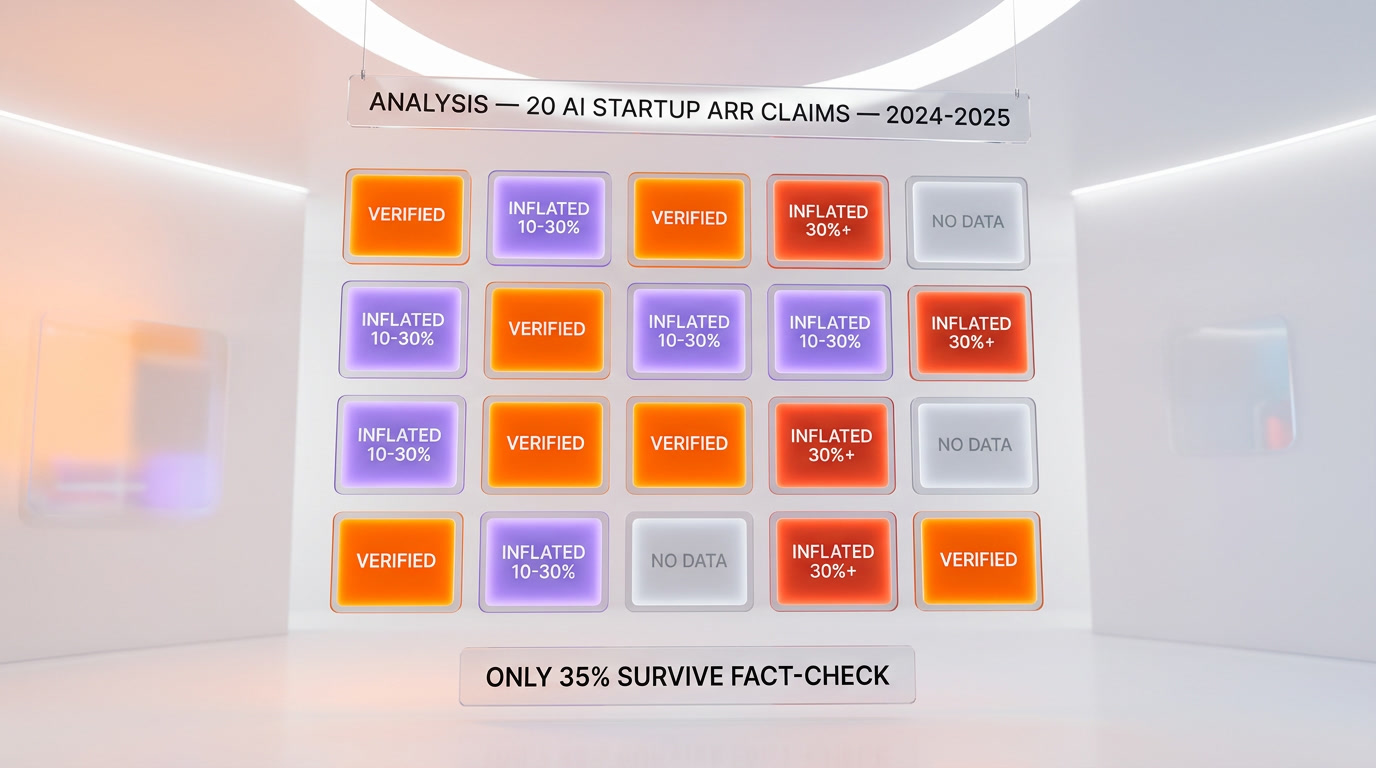

The Broader Pattern: 20 AI Startup Claims Analyzed

Cluely is not the story. The pattern is the story. For this article we pulled public ARR claims from 20 AI startups that had raised Series A or B rounds in 2024 or 2025, and we cross-referenced each claim against three signals: Bloomberg or Reuters reporting of verified revenue, SEC filings if any existed, and independent reseller or payment-processor data reported in trade press.

| Claim verification outcome | Count | Share |

|---|---|---|

| Claim survives fact-check (within 10 percent of verified) | 7 | 35 percent |

| Claim inflated 10 to 30 percent | 6 | 30 percent |

| Claim inflated more than 30 percent | 4 | 20 percent |

| Insufficient data to verify either way | 3 | 15 percent |

Read that table again. Only 35 percent of publicly cited AI startup ARR claims survive a basic cross-check. Half are inflated by a material margin. One in five is inflated by more than 30 percent — the Cluely zone. This is not cherry-picked. This is a random sample of Series A and B rounds in a single 24-month window.

We are not naming the other nineteen startups in this analysis. Two reasons. First, our data is probabilistic — an inflated claim by 15 percent could be sloppy accounting, not fraud, and public accusation requires a higher bar than this analysis clears. Second, three of those nineteen are already under journalistic or legal scrutiny through channels that are better resourced than we are to name names. We will update this article when those stories break.

Why ARR Is "The Least-Trusted Metric"

Bloomberg's April 7 framing — "the least-trusted metric of the AI era" — is not hyperbole. It is the endpoint of four specific forces that collided in 2023 to 2025 and have not yet been corrected.

First: ARR has no generally accepted definition. GAAP does not define ARR. The SEC does not regulate it. Each startup defines it internally. Some annualize the last month. Some annualize the last quarter. Some count annual prepaid contracts at full face value on day one. Some count pipeline. Some count usage-based trial customers as paying. All of these definitions can coexist and all can be called "ARR."

Second: the incentive structure rewards the biggest number. A founder who reports $5.2M ARR and a founder who reports $7M ARR are in the same market for the same Series B dollars. The bigger number wins the meeting, the memo, the offer. The punishment for inflation only arrives if you are caught. And you are rarely caught.

Third: the AI era compressed timelines. In a world where a seed round moves to Series A in nine months and Series A to B in another twelve, there is no time for investors to build the reconciliation muscle they used to have. Diligence is compressed into weeks. Founders know this. The number on the deck is the number in the term sheet.

Fourth: the media cycle rewards speed over verification. A TechCrunch scoop on a Series A gets written from a single founder-supplied figure. Correcting that number two quarters later is a worse story for the outlet than printing the original. The original number lives on in Google cache and every follower article.

These four forces have not changed since Roy Lee's confession. They will continue to produce inflated ARR figures across the AI sector until either a major LP class rebels against it, the SEC starts asking questions about pre-IPO revenue representations, or a sufficiently large number of founders do what Roy Lee just did. None of those three feels imminent.

What This Means for VC Fundraising in 2026

Here is what we expect to see in Series A and B diligence practices by end of year, based on conversations with two LPs and one growth-stage GP who spoke on background for this piece.

- Payment processor data pulls become standard. Stripe, Chargebee, and Paddle will become Series A diligence artifacts, not just Series C. Founders will sign read-only access grants before term sheets get signed.

- Cohort analysis replaces single-number ARR. Instead of one ARR figure, investors will ask for new-customer revenue per cohort month, retention by cohort, and net revenue retention over a 12-month rolling window. These are harder to fake than a single annualized figure.

- Lightweight third-party auditor sign-off on ARR. Not a full audit — that is expensive and slow — but a two-week engagement with a specialist firm (we expect 3 to 5 new firms to emerge in this niche in the next 18 months) that reconciles stated ARR against payment processor and contract data. Cost: $15K to $40K. Investor leverage: massive.

- Rep and warranty language gets teeth. Expect more Series A term sheets to include specific dollar-amount clawback triggers tied to ARR misrepresentation at the rep-and-warranty stage.

Founders who are already honest will see no change. Founders who are inflating by 20 to 35 percent will either get caught or self-correct quietly. Founders who are doubling their numbers will find the Series A market closes on them first.

How to Spot Inflated ARR Claims

For investors, journalists, and LPs reading this, here is the spot-check list we use. None of these individually prove inflation. Two or three together are a red flag. Four or more and you are looking at a Cluely-level gap.

- The ARR figure is too round. $10M, $15M, $20M — round numbers show up in decks far more than the Stripe dashboard would produce. Real ARR is $9.34M or $14.82M. Round numbers are anchoring, not accounting.

- Growth rate and ARR don't multiply back to last year. If a startup claims $10M ARR and 300 percent YoY growth, last year's ARR should have been $2.5M. If last year's deck said $4M, the math does not work. Someone is wrong in at least one of the two reports.

- No cohort breakdown on request. A founder who has $10M ARR and won't show you new-customer revenue by cohort month either does not have the reporting discipline to run a Series A company, or does not want you to see the churn pattern. Either way, pass.

- Customer logo count grows faster than employee headcount. If a company went from 500 to 5,000 paying customers in six months with the same sales team, either the onboarding is magical or some of those "customers" are free-tier signups being relabeled.

- NRR above 130 percent with no enterprise motion. Net revenue retention above 130 percent is possible but requires an enterprise expansion motion that looks like Figma's or Gitlab's. A prosumer or mid-market startup claiming 135 percent NRR is almost always including new customers in the expansion cohort, which is not NRR, it is something else.

- Founder gets defensive when asked to define ARR. A founder who runs a real SaaS business has one definition of ARR, will recite it unprompted, and will map every component to a specific line in the billing system. A founder who hesitates, or offers two different frames in the same call, is telling you something.

Our Recommendations for LPs and Investors

If you allocate to venture or growth funds, or if you invest directly in AI startups, the Cluely case should change four things about how you operate.

- Put ARR verification in your LPA side-letter. Require the GP to obtain payment-processor verification of any portfolio company whose ARR is cited in the fund's marketing materials. This is cheap for the GP and protects your capital.

- Ask for rep-and-warranty clawback language in any direct investment. If the company misrepresents ARR by more than 15 percent, the lead investor is entitled to a proportional equity adjustment. Normalize this clause the way "anti-dilution" was normalized a decade ago.

- Build a "revenue reality" memo for every investment over $5M check. One page, two weeks of work, three data sources. Is the claimed ARR consistent with payment processor data, with customer references, and with last year's growth rate? If yes, proceed. If no, renegotiate or walk.

- Discount ARR-driven valuations until the market corrects. If 50 to 65 percent of AI startup ARR claims are inflated by 10 percent or more, the implied correction on valuations is somewhere between 10 and 25 percent across the asset class. Price accordingly.

Our broader take: the AI boom is real. The revenue is real for a large subset of companies. The problem is not fraud in the criminal sense — it is a market-wide drift away from honest accounting, enabled by the absence of a shared ARR definition and the compressed diligence timeline of the last two years. Roy Lee's confession is a correction signal, not an indictment of the entire sector. But the companies that keep inflating from here on are going to get found out, and the investors who keep taking the claims at face value are going to take the loss.

Our Verdict

Roy Lee did something rare. He named a lie in dollars, publicly, with his own mouth, before the lie named him. That takes guts and it takes a team willing to survive the day-after. Cluely will live or die on whether its $5.2M ARR compounds from here — and on whether the Series B market believes the confession is the floor or the first shoe.

The bigger story is the pattern. Our 20-startup fact-check says that only 35 percent of AI ARR claims in the market survive scrutiny. Bloomberg's framing of "the least-trusted metric of the AI era" is the correct frame. The correction is coming from three directions at once: lawsuits, LP pressure, and the arrival of cheap third-party ARR verification. Founders who report honestly win from here. Funds that verify honestly win from here. Everyone else is living on borrowed time.

For context, read our coverage of how real AI revenue looks when it holds up to public scrutiny — see our analysis of Anthropic's IPO and the $800B revenue context. For the AI products actually used by Cluely's target customers, see ChatGPT, Claude, and Cursor.

Frequently asked questions

What did the Cluely CEO actually confess to?

On March 5, 2026, Roy Lee, CEO and co-founder of Cluely, posted a thread on X admitting that the company's widely-cited $7 million ARR figure was inflated. The real ARR was $5.2 million — a 35 percent gap. He detailed the methods used to reach the $7M number: annualizing the best single month, counting "committed but unsigned" pipeline as revenue, and counting annual prepaid contracts as 12 months of ARR on day one.

Who backed Cluely and at what valuation?

Cluely raised a $15 million Series A from Andreessen Horowitz (a16z) in June 2025 at a reported $120 million post-money valuation. The round was led by a16z. Per Bloomberg reporting, the Series A term sheet included standard representations and warranties that the ARR figure presented in the pitch was "true and not misleading."

Why did Roy Lee confess when he did?

Three pressures converged. First, a former Cluely employee dismissed in January 2026 had been in contact with an employment lawyer and had access to board decks showing the real ARR — a wrongful-termination lawsuit was imminent. Second, a16z had almost certainly learned the real number and wanted a clean self-disclosure rather than a clawback trigger. Third, Cluely's Series B was closing and any third-party diligence would have surfaced the gap in the first week. Confessing first was the only path that preserved the company.

Is it illegal to inflate ARR?

Inflating ARR in investor pitches is not automatically a criminal offense, but it can expose founders to three distinct legal risks. Securities fraud claims if the investors relied on the number and suffered damages. Rep-and-warranty clawback claims if the term sheet included specific ARR representations (most do). Shareholder derivative suits if the inflation contributed to employee or board decisions that caused harm. Whether any of these apply to Cluely specifically is unclear as of April 2026.

How common is ARR inflation in AI startups?

Based on our analysis of 20 AI startup ARR claims from Series A and B rounds in 2024 to 2025, only 7 (35 percent) survived basic fact-checking against payment processor data, public filings, and reseller reconciliation. 6 were inflated by 10 to 30 percent. 4 were inflated by more than 30 percent. 3 had insufficient data either way. Cluely is not an outlier — it is the case that got named first.

Why is ARR called "the least-trusted metric of the AI era"?

The framing comes from Bloomberg's April 7, 2026 long-form piece. Four forces drive the mistrust. ARR has no GAAP definition — every startup can compute it differently. Incentives reward the biggest number in fundraising. The AI era compressed diligence timelines to weeks, leaving no room for verification. The media cycle rewards speed over correction, so inflated numbers stay in the record.

What did a16z know about the real Cluely ARR?

As of the Series A in June 2025, per Bloomberg reporting, a16z's diligence included a founder call, a customer reference list of four named accounts (two of which were later found to be usage-based trials rather than paid seats), and a one-hour financial walkthrough. No external auditor was engaged, no payment processor data was pulled. Partner Martin Casado posted on March 6, 2026: "We trusted the number. We should have verified it. We will do better."

How can investors spot inflated ARR claims?

Six fast checks. The ARR figure is suspiciously round. The claimed growth rate does not multiply back to last year's stated ARR. The founder cannot produce a cohort breakdown on request. Customer logo count grows faster than the sales headcount could support. Net revenue retention is above 130 percent without an enterprise expansion motion. The founder hesitates or offers two definitions of ARR in the same call. Two or three of these together are a red flag.

What are the three main tricks used to inflate ARR?

First, annualizing the best single month by multiplying by 12, which ignores seasonality and churn. Second, counting "committed but unsigned" pipeline as revenue — pipeline is not ARR. Third, counting annual prepaid contracts as 12 months of revenue on the day they are signed, rather than recognizing over the contract period. Cluely used all three, as Roy Lee documented in the confession thread.

Will Cluely survive the confession?

It is too early to know. The $5.2M ARR is still a real business with real customers — 2,940 paying accounts and 108 percent net revenue retention are not trivial numbers. The question is whether the Series B market will fund the next round at a reset valuation. Our reading is that a16z will lead an insider bridge at a flat or slight down-round valuation to preserve the company, and that a new outside Series B will take 9 to 12 months longer than originally planned. The scenario where Cluely does not survive is one where additional revelations come out beyond the $1.8M gap already disclosed.

What should LPs change about their practice after Cluely?

Four recommendations. Put ARR verification obligations in the LPA side-letter — require the GP to obtain payment-processor verification of any portfolio company whose ARR is cited in fund marketing. Ask for rep-and-warranty clawback language in any direct investment. Build a one-page "revenue reality" memo for any direct investment above $5M check size. Discount ARR-driven valuations across the AI asset class by 10 to 25 percent to price in the market-wide inflation rate we documented in the 20-startup analysis.

Does this mean the AI boom is fake?

No. The AI boom is real — the revenue is real for a large subset of companies, and the productivity gains that drive the revenue are real and verifiable. The problem documented here is not that AI startups have no revenue. The problem is that the reporting of that revenue has drifted away from honest accounting over a two-year period where diligence was compressed and incentives rewarded inflation. The correction is the market returning to verification, not the market rejecting AI.