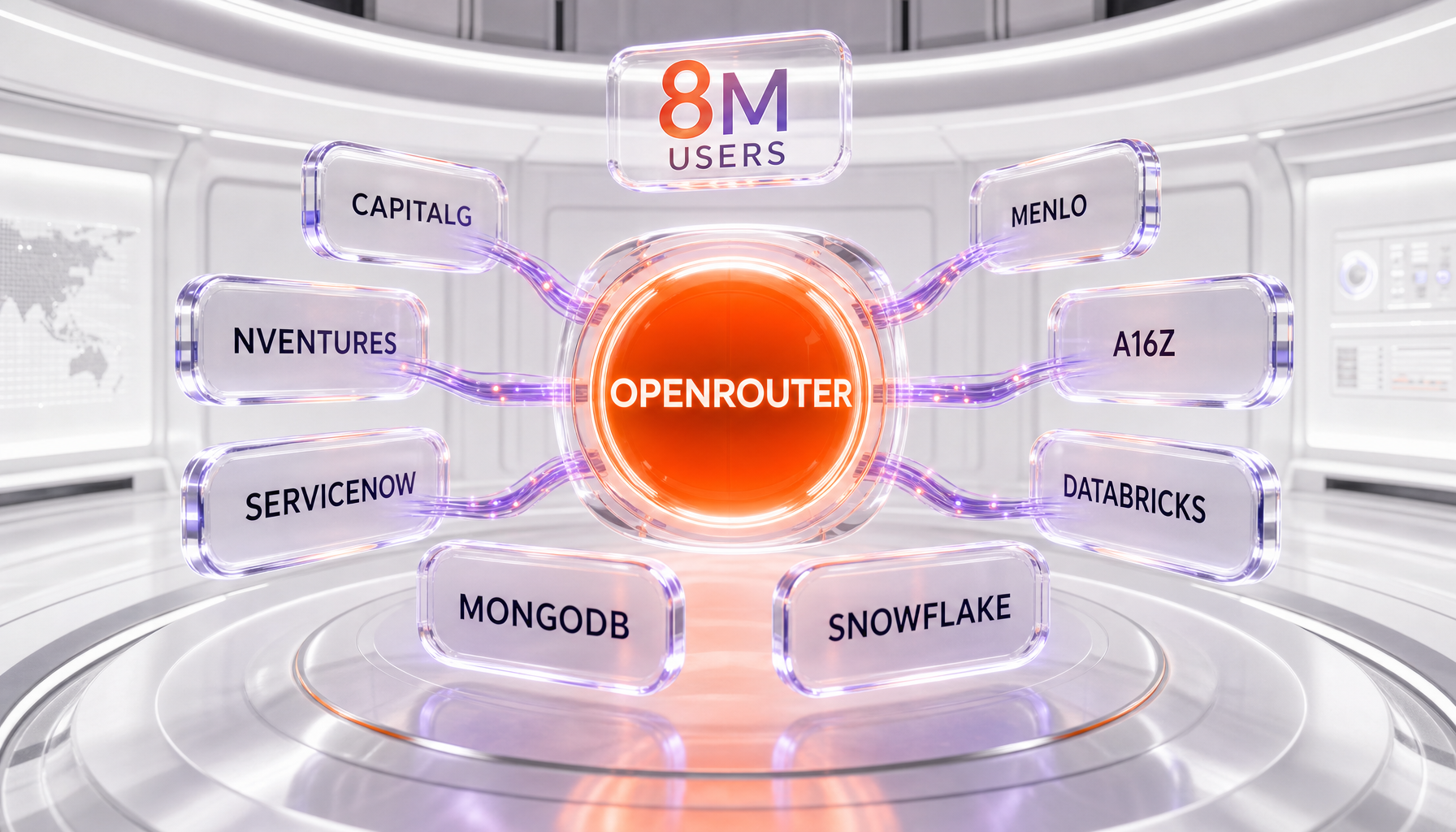

What is OpenRouter's Series B? On May 26, 2026, OpenRouter raised $113 million led by CapitalG (Alphabet) at a roughly $1.3 billion post-money valuation, with weekly volume reaching 25 trillion tokens across more than 400 models. That is up from an estimated $547 million valuation after its $40 million Series A in June 2025 — about a 2.4x markup in 11 months.

OpenRouter is an AI model gateway: a single API that routes requests to hundreds of models from different providers. The Series B is less a story about one company raising money and more a signal about where the AI stack is hardening. The dollars here did not buy a frontier model. They bought the rails between models — the control plane that increasingly decides which model gets each request, at what price, with what fallback.

What Happened

OpenRouter announced its Series B on May 26, 2026. The headline numbers, confirmed in the company's announcement and corroborated by independent coverage:

- $113 million raised, led by CapitalG, Alphabet's independent growth fund.

- ~$1.3 billion post-money valuation, up from an estimated $547 million after the June 2025 Series A.

- 25 trillion tokens per week in volume — about 100 trillion tokens per month — a 5x increase from roughly 5 trillion tokens per week six months earlier.

- 400+ models accessible through one API, spanning Anthropic, Google, OpenAI, xAI, and DeepSeek.

- 8 million global users, from solo developers to enterprises.

The participant list is the part worth slowing down on. Beyond CapitalG, the round drew NVentures (NVIDIA's venture arm), ServiceNow Ventures, MongoDB Ventures, Snowflake Ventures, and Databricks Ventures, with existing backers Andreessen Horowitz and Menlo Ventures returning. Founded in 2023, OpenRouter positions itself as the layer sitting between agents, applications, and the model ecosystem.

Eleven months between rounds, with the valuation more than doubling, is a fast clip even by 2025-2026 standards. But the multiple is downstream of the usage curve. A 5x jump in weekly tokens over six months is the kind of growth that turns a developer convenience into infrastructure that enterprises plan around.

Why It Matters: The Control Plane Is the New Layer

For most of the current AI cycle, the money and the narrative concentrated on the models themselves — who has the smartest frontier system, who wins the next benchmark. OpenRouter's raise points at a quieter shift: as capable models multiply and start to look interchangeable for many tasks, value migrates to the layer that routes between them.

This is the control plane. It decides which model handles a request, enforces budgets, adds fallbacks when a provider is down or rate-limited, and gives teams one billing relationship instead of five. In our reading, the strategic claim embedded in this round is blunt: where the dollars now buy the rails between models, not the models themselves.

Calling a single provider's API directly couples your product to that vendor's SDK, pricing changes, and uptime. A gateway decouples the application from any one model. You can A/B a cheaper model against a stronger one on the same task, fail over automatically, and swap a deprecated model without touching your integration. At 400+ models behind one endpoint, that optionality stops being a nice-to-have and becomes an architecture decision.

The Usage Curve Behind the Valuation

Valuations follow usage, and OpenRouter's usage is the real story. Going from about 5 trillion tokens per week to 25 trillion per week in six months is not linear growth — it is the shape you see when a behavior becomes a default. Roughly 100 trillion tokens per month flowing through one router implies a large share of real production traffic, not just experimentation.

Two forces likely compound here. First, the explosion of agentic workloads: agents make many model calls per task, and they benefit from routing logic that picks the right model per step. Second, cost discipline. As teams move from demos to production, the ability to send cheap tasks to cheap models and hard tasks to frontier models — without rewriting code — directly affects margins. A router is where that discipline lives.

The Strategic Read on CapitalG and the Syndicate

The most interesting line in this round is the lead investor. CapitalG is Alphabet's growth fund, and Alphabet sells Gemini. Backing a provider-neutral router — one that happily sends traffic to Anthropic, OpenAI, xAI, and DeepSeek alongside Google's own models — is a bet on the neutrality of the layer rather than on Gemini's win. It is a position that the routing infrastructure is valuable no matter which model leads on any given week.

That is a defensible thesis, and it is worth naming the tension plainly rather than glossing it. An Alphabet-affiliated fund holding a meaningful stake in the layer that allocates demand across competing models is a strategic question the market will watch. We are not making a claim about how OpenRouter routes traffic; the announced facts do not speak to that. The point is structural: the control plane is now important enough that one of the largest model vendors wants exposure to it.

The rest of the syndicate reinforces the infrastructure framing. NVentures ties the round to the compute layer. ServiceNow, MongoDB, Snowflake, and Databricks are the data and enterprise-workflow companies whose customers are wiring models into existing systems. When that group co-invests in a router, the signal is that orchestration is becoming a planned line item in enterprise architecture, not a hobbyist tool.

How It Compares: Gateways vs Direct APIs vs Coding Tools

It helps to separate three layers that are easy to conflate.

Direct provider APIs (Anthropic, OpenAI, Google) give you the deepest, earliest access to a single vendor's features but maximize lock-in. Gateways like OpenRouter trade a thin layer of abstraction for breadth, unified billing, and failover across 400+ models. Application-layer tools — including coding agents — increasingly let developers bring their own keys or route through a gateway, so the model choice becomes configurable rather than hardcoded.

For developers living in coding tools, this matters. Agentic coding environments such as Claude Code, Cursor, and OpenAI Codex are some of the heaviest per-task token consumers in the ecosystem, because an agent can fire dozens of model calls to plan, edit, and verify a change. A neutral router makes it practical to compare models on the exact same coding task and to avoid betting a whole workflow on one vendor's roadmap. Even Windsurf and similar editors sit in this pattern, where the model is a swappable backend rather than a fixed dependency.

We have seen this dynamic show up elsewhere on the platform: model leaderboards on routers are now a competitive arena in their own right, as our coverage of Hermes Agent topping OpenRouter illustrated. When a router's ranking can shift real traffic, the router becomes a market.

What's Next

A few things are worth watching now. The first is whether the control-plane category consolidates or fragments. With cloud and data vendors funding routing, expect each major platform to push its own gateway story; the open question is whether developers prefer one neutral router or many platform-bound ones.

The second is pricing and economics. Routers monetize on top of model usage, and the announced materials here do not disclose take rates or revenue. We are deliberately not estimating those numbers. What is observable is that 100 trillion tokens per month is a very large base of traffic to build a business on, and the investor mix suggests they believe the unit economics scale.

The third is governance and neutrality. As the control plane grows in importance, so will scrutiny of how routers rank, default, and surface models — especially when a model vendor sits on the cap table. That is a healthy debate for the ecosystem to have early.

The Bottom Line

OpenRouter's $113 million Series B at a ~$1.3 billion valuation is a marker for a structural shift: the AI stack now has a fundable, strategically contested control-plane layer. With 25 trillion tokens per week across 400+ models and a syndicate spanning compute, data, and enterprise software, the round reads as a bet that whoever owns the rails between models holds durable leverage — even as the models underneath keep changing. For builders, the practical takeaway is simple: model choice is becoming a configuration decision, and the routing layer is where that decision increasingly lives.

Disclosure: ThePlanetTools.ai has no affiliate or commercial relationship with OpenRouter or any investor named in this article. Figures are drawn from OpenRouter's May 26, 2026 announcement and corroborating coverage; where a detail (such as fee structure) was not disclosed, we have flagged it rather than estimated it. This is an editorial analysis, not investment advice.

Sources: OpenRouter Series B announcement (BusinessWire, May 26, 2026); TechCrunch coverage.

Frequently Asked Questions

What is OpenRouter's Series B?

On May 26, 2026, OpenRouter announced a $113 million Series B led by CapitalG, Alphabet's independent growth fund. The round valued the company at roughly $1.3 billion post-money, up from an estimated $547 million after its $40 million Series A in June 2025.

How much is OpenRouter worth after the Series B?

OpenRouter's post-money valuation is approximately $1.3 billion. That is about 2.4x its estimated $547 million valuation from June 2025, reached in roughly 11 months.

Who led OpenRouter's Series B and who participated?

CapitalG (Alphabet's growth fund) led the round. Participants included NVentures (NVIDIA's venture arm), ServiceNow Ventures, MongoDB Ventures, Snowflake Ventures, and Databricks Ventures, alongside existing investors Andreessen Horowitz and Menlo Ventures.

How many tokens does OpenRouter process?

OpenRouter reported weekly volume of about 25 trillion tokens, equal to roughly 100 trillion tokens per month. That is a 5x increase from about 5 trillion tokens per week six months earlier.

How many AI models does OpenRouter support?

OpenRouter provides access to more than 400 models through a single API, including models from Anthropic, Google, OpenAI, xAI, and DeepSeek.

How many users does OpenRouter have?

OpenRouter reported about 8 million global users at the time of the Series B announcement, spanning individual developers and enterprises.

What is an AI model gateway or control plane?

A model gateway is a routing layer that sits between applications and many AI providers, standardizing access through one API. It lets teams switch models, control costs, and add fallbacks without rewriting their integration for each provider.

Why did Alphabet's CapitalG invest in a multi-model gateway?

CapitalG backing a provider-neutral router is notable because Alphabet also sells Gemini models. The bet is on the routing layer itself: as models become interchangeable, value accrues to whoever controls the rails between them, regardless of which model wins.

How is OpenRouter different from using a provider API directly?

Calling Anthropic, OpenAI, or Google directly locks you to one vendor's SDK, pricing, and uptime. OpenRouter exposes 400+ models behind one API with unified billing, automatic fallbacks, and per-request model selection, so teams can route each job to the cheapest or strongest model.

Is OpenRouter relevant for developers using Claude Code, Cursor, or OpenAI Codex?

Yes. Coding tools like Claude Code, Cursor, and OpenAI Codex increasingly let developers bring their own model keys or route through gateways. A neutral router makes it easier to compare models on the same task and avoid single-vendor lock-in for agentic coding workflows.

What does the Series B mean for the AI tools market?

It signals that the control-plane layer is now a fundable, strategic category. With cloud and data investors (ServiceNow, MongoDB, Snowflake, Databricks) joining, routing and orchestration are being treated as core infrastructure rather than a thin convenience wrapper.