On May 15, 2026, OpenAI launched ChatGPT Personal Finance, a feature that lets ChatGPT Pro subscribers connect their bank accounts through Plaid across more than 12,000 financial institutions. The system analyzes spending, builds budgets, and answers money questions in plain language, with an Intuit tax integration confirmed as the next step. This is OpenAI's most direct move yet into consumer finance, and it pulls a general-purpose chatbot straight into territory occupied by banks, budgeting apps, and human financial advisors.

What OpenAI Actually Shipped on May 15

ChatGPT Personal Finance is a built-in capability inside ChatGPT, not a separate app. According to OpenAI's announcement, Pro subscribers can now link checking accounts, savings accounts, and credit cards through Plaid, the financial data network that already sits behind apps like Venmo, Robinhood, and Coinbase. Once connected, ChatGPT reads transaction history and can answer questions like "how much did I spend on restaurants last month" or "can I afford a $2,000 trip in August" in conversational language.

The numbers OpenAI put forward are deliberately broad. Plaid connectivity covers 12,000+ institutions, which is effectively the entire US retail banking market plus a long tail of credit unions and fintech accounts. TechCrunch's coverage confirmed the feature is gated to the Pro tier at launch, with the Intuit tax integration positioned as a roadmap item rather than a same-day release.

The Three Capabilities That Define It

Strip away the framing and ChatGPT Personal Finance does three things. First, it ingests and categorizes transactions automatically through Plaid's normalized data feed. Second, it answers natural-language questions about that data without requiring the user to build a spreadsheet or learn an app's UI. Third, it generates forward-looking plans — budgets, savings targets, debt payoff sequencing — based on the actual cash flow it observes.

None of those three capabilities is individually new. Mint did transaction categorization for over a decade. Cleo and Copilot Money do conversational money queries. The strategic shift is that all three now live inside a product that 800 million people already open for unrelated reasons.

Why "Inside ChatGPT" Is the Whole Story

The distribution model is the news here, not the technology. A standalone budgeting app has to win a download, an onboarding flow, and a habit. ChatGPT Personal Finance inherits all three from a product people already use daily for code, email drafts, and homework. That is the same playbook OpenAI ran with the self-serve ChatGPT Ads Manager — bolt a high-intent commercial surface onto existing reach rather than build a new audience from zero.

The Reach Advantage Quantified

ChatGPT's roughly 800 million weekly users dwarf the entire installed base of every dedicated budgeting app combined. Even a low single-digit conversion of that audience into connected-bank users would instantly make ChatGPT one of the largest personal-finance analysis surfaces in the US. That is the strategic asymmetry no standalone competitor can answer with product quality alone.

The Habit Loop OpenAI Inherits

Personal finance apps historically fail on retention, not acquisition. People download, connect an account, check it twice, and never return. ChatGPT does not need to manufacture a return visit for finance — the user is already there for unrelated reasons, and the finance capability surfaces opportunistically inside an existing habit. That structural retention advantage is the quiet core of the entire play.

How the Plaid Integration Actually Works

Plaid is the connective tissue, and understanding its role clarifies both the capability and the risk surface. When a user links an account, Plaid handles the authentication flow with the bank, then issues OpenAI a tokenized, scoped credential rather than the raw username and password. ChatGPT receives a structured stream of transactions, balances, and account metadata — it does not log in to the bank as the user.

What Data Flows, and What Does Not

The Plaid feed typically includes transaction descriptions, amounts, dates, merchant categories, account balances, and account types. It does not, by design, hand over the user's banking password to OpenAI. That separation matters for the privacy conversation later in this analysis, but it is not a complete shield — the transaction data itself is among the most sensitive datasets a person owns, and it now sits in a context window.

The 12,000 Institutions Claim, Decoded

Plaid's institutional coverage is genuinely deep in the US: virtually every major bank, the large credit unions, and most fintech accounts resolve. The practical caveat is reliability rather than coverage. Plaid connections to smaller institutions break more often, require periodic re-authentication, and sometimes return delayed or incomplete transaction data. Anyone who has used a Plaid-powered budgeting app knows the "please reconnect your account" notification. ChatGPT Personal Finance inherits that maintenance burden.

Why OpenAI Chose Plaid Instead of Building Direct Connections

Building direct bank integrations is a multi-year regulatory and engineering slog — it is precisely why Plaid exists as a business. Choosing Plaid let OpenAI ship coverage of the entire US market on day one rather than negotiating bilateral data agreements bank by bank. It is a textbook build-versus-buy decision, and OpenAI bought the hard part. The strategic cost is dependency: OpenAI's finance feature now rests on a third party's uptime, pricing, and data-access agreements with banks.

What ChatGPT Can Actually Do With Your Spending Data

The capability set splits into two categories: descriptive analysis of what already happened, and prescriptive planning for what should happen next. The descriptive side is more reliable. The prescriptive side is where the strategic and trust questions concentrate.

Descriptive Analysis: The Strong Use Case

Asking ChatGPT to summarize where money went is the feature's most defensible function. "What were my three biggest expense categories last quarter," "how much did subscriptions cost me this year," "show me every charge over $200 in April" — these are deterministic queries against structured data, and a language model layered over a clean Plaid feed handles them well. This is the part most users will adopt first and trust most.

Prescriptive Planning: Where It Gets Interesting

Budget construction and savings planning are the headline use case OpenAI is marketing, and they are also the most consequential. When ChatGPT recommends "you can cut $400 a month by reducing dining out and you should redirect it to an emergency fund," it has crossed from data summarization into financial advice. Whether the model's advice is sound, conflicted, or regulated is the strategic question the rest of this analysis examines.

The Natural-Language Advantage Is Real

One thing worth stating plainly: the conversational interface is a genuine improvement over traditional budgeting apps for a large segment of users. Most people never set up Mint categories correctly, never opened YNAB twice, and never built a spreadsheet. "Just ask in plain English" removes the single largest adoption barrier in personal finance software, which is the setup friction. That is a real product advantage, independent of the strategic concerns.

The Intuit Tax Integration Changes the Scope

OpenAI confirmed an Intuit integration is coming, which would connect ChatGPT to tax preparation workflows. This is a meaningful scope expansion. Tax is the highest-stakes, most regulated, most error-sensitive corner of personal finance. An Intuit pipe would let ChatGPT move from "here is what you spent" toward "here is what you owe and how to file it." The timeline and exact scope remain unconfirmed, so this analysis treats it as directional rather than shipped.

Why Tax Is a Different Risk Tier

Spending analysis tolerates approximation — a budget that is roughly right is still useful. Tax does not. A misclassified deduction or a wrong figure carries legal and financial consequences for the user, and at ChatGPT's scale a systematic error would not be an individual problem but a population-level one. Moving toward tax is moving from a forgiving domain into an unforgiving one, and that escalation is the clearest signal of OpenAI's appetite for regulated financial territory.

The Privacy and Data Question Nobody Should Skip

Connecting a bank account to an AI system is one of the most sensitive data decisions a consumer can make, and the strategic implications run deeper than a single privacy policy clause.

What the Architecture Protects

The Plaid intermediation is a real design strength. OpenAI does not receive banking credentials, and the access is tokenized and scoped. This is materially better than a system that asks users to type their bank password into a chat box. Credit where due: the architecture chose the safer pattern.

What the Architecture Does Not Protect

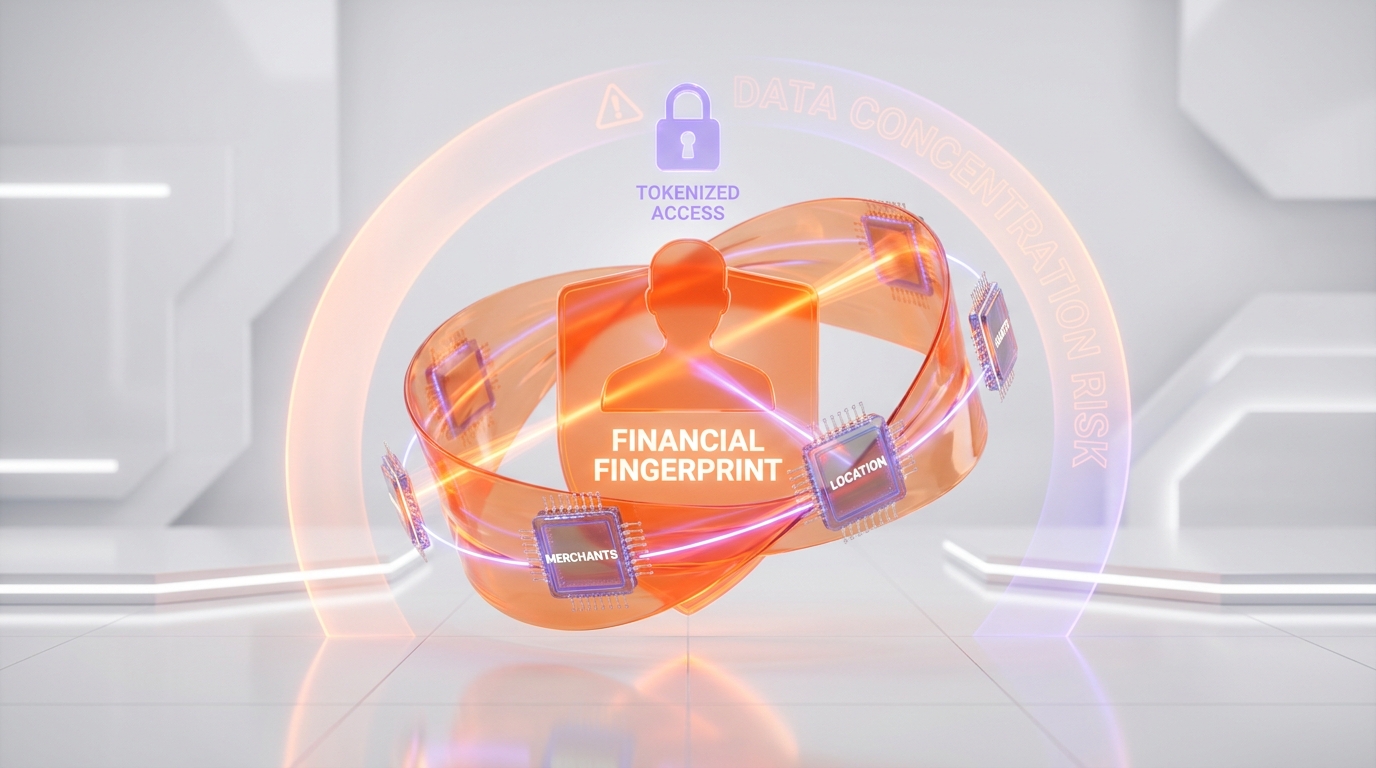

Tokenization protects the login, not the data. The transaction history itself — every merchant, every amount, every recurring payment, every financial habit — flows into a system whose entire value proposition is reading and reasoning over it. Spending data is a near-complete behavioral fingerprint: it reveals health conditions through pharmacy charges, relationships through shared payments, location through merchant geography, and financial vulnerability through overdraft patterns. The strategic question for users is not "can OpenAI see my password" but "am I comfortable with the most revealing dataset I own living inside an AI context."

The Training Data Question

The single question every user should ask before connecting an account is whether financial data is used for model training, and under what controls. OpenAI's enterprise and API tiers have historically offered no-training guarantees, while consumer ChatGPT settings have been more nuanced. The responsible position for any reader is to verify the current data-use settings in their own account before linking, rather than assume. This analysis does not assert OpenAI's exact training policy for this feature because the precise terms were not confirmed at launch — and that uncertainty is itself the point users should weigh.

The Concentration Risk

There is a structural concern beyond any single company's policy. The same account that holds your conversations, your documents, your code, and increasingly your photos would now also hold your complete financial life. Concentration of that much personal data in one consumer account raises the stakes of a single credential compromise. This is a strategic observation about consumer data architecture, not an accusation about any specific OpenAI security failure.

Why This Disrupts Fintech and Financial Advice

The competitive implications are larger than the feature itself. ChatGPT Personal Finance is a distribution event aimed at three different industries simultaneously.

Standalone Budgeting Apps Face the Hardest Hit

The category most exposed is the dedicated budgeting app. Copilot Money, Monarch, YNAB, and the post-Mint successors all sell a conversational or dashboard layer on top of Plaid. ChatGPT Personal Finance offers a comparable conversational layer on the same Plaid plumbing, bundled into a subscription users already pay for. The strategic problem for these apps is not feature parity — several have better-designed finance-specific UX — it is that they now compete against a free-adjacent bundle inside a product with vastly larger reach. Their defensible ground narrows to depth, specialization, and finance-native trust.

Robo-Advisors and the Advice Boundary

Robo-advisors like Betterment and Wealthfront occupy a regulated lane: they are registered investment advisers and they custody assets. ChatGPT does neither at launch — it analyzes and suggests but does not manage money or hold a fiduciary registration. That regulatory boundary is the robo-advisors' moat for now. The strategic watch item is whether OpenAI eventually partners with a custodian or registered adviser to cross that line, because the Intuit tax move signals appetite for deeper, more regulated financial workflows.

Human Financial Advisors: Pressured at the Entry Level

Human advisors are not threatened at the high end — complex estate, tax, and wealth planning still rewards human judgment and accountability. The pressure lands on the entry tier: the advisor whose value was mostly building a first budget and answering basic "can I afford this" questions. That conversation is exactly what ChatGPT now does for free-adjacent inside a subscription. The profession's defensible value moves upward toward fiduciary accountability and genuinely complex situations.

Banks Are the Quiet Stakeholder

Banks sit in an ambivalent position. They benefit from Plaid-enabled engagement but lose the customer relationship layer if the analytical interface their customers actually use is ChatGPT rather than the bank's own app. The strategic risk for banks is disintermediation of the financial-insight relationship — the same dynamic that already played out when fintech apps became the front end and banks became the backend rails.

How This Fits OpenAI's Broader Strategy

ChatGPT Personal Finance is not an isolated product decision. It is one move in a clearly visible pattern of OpenAI converting ChatGPT's reach into commercial surfaces across one vertical after another.

The Super-App Trajectory

The pattern is consistent with the agentic super-app direction OpenAI signaled at the GPT-5.5 launch and the model now powering the default experience via GPT-5.5 Instant. Finance, ads, and an expanding tool surface all point the same direction: ChatGPT as the connective layer across a user's digital and financial life rather than a standalone chat tool.

The Enterprise-to-Consumer Mirror

OpenAI is running parallel expansion plays. On the enterprise side, the $4B deployment-company joint venture with Big Four consulting firms drives AI into corporate workflows. On the consumer side, finance is the equivalent move into personal workflows. Both share one logic: own the integration layer where decisions get made, not just the model that answers questions.

The Vertical Land-Grab Compared to Rivals

Compared to Anthropic's Claude, which has stayed deliberately closer to a general assistant and enterprise positioning, OpenAI is aggressively claiming consumer verticals — health partnerships, finance, ads. The strategic bet is that consumer breadth and integrated workflows create switching costs that a purely capability-led competitor cannot easily match. Whether that bet pays off depends on trust, which in finance is the entire game.

What Would Make This Succeed or Fail

A strategic analysis is incomplete without naming the conditions that decide the outcome rather than just describing the launch.

The Success Conditions

This succeeds if three things hold. Accuracy: the spending analysis has to be reliably correct, because a single visible math error in someone's money destroys trust faster than in any other domain. Privacy clarity: OpenAI has to make data-use terms unambiguous and conservative, or the most valuable users — the financially sophisticated — will refuse to connect. Restraint at the advice boundary: the system has to be careful about prescriptive recommendations in regulated territory, because confidently wrong financial advice at ChatGPT's scale is a systemic, not individual, problem.

The Failure Conditions

It fails if Plaid reliability frustrates users into disconnecting, if a privacy incident or unclear training-data disclosure triggers a trust collapse, or if regulators decide conversational budgeting with prescriptive recommendations constitutes regulated financial advice. Any one of those is plausible. The most likely near-term friction is mundane: Plaid connections breaking and users abandoning the feature the way they abandoned previous budgeting apps.

The Honest Uncertainty

The single largest unknown is regulatory. Financial advice in the US is heavily regulated, and the line between "educational information" and "investment advice requiring registration" is contested. OpenAI is shipping into that gray zone at consumer scale. No one — including OpenAI — can confidently predict how regulators respond, and that uncertainty is the defining strategic variable, not the technology.

The Bottom Line

ChatGPT Personal Finance is a distribution play disguised as a feature. The technology — Plaid connectivity, transaction analysis, conversational budgeting — is well understood and individually unremarkable. What is remarkable is bundling it into a product 800 million people already use, which instantly reframes the competitive landscape for budgeting apps, pressures the entry tier of financial advice, and forces banks to confront disintermediation of the insight layer. The architecture made the right call on credential security through Plaid, but the concentration of a user's complete financial fingerprint inside an AI account is a genuine strategic risk that each user has to weigh for themselves. The Intuit tax integration signals OpenAI intends to push deeper into regulated territory, which makes the unanswered regulatory question the variable that will decide whether this becomes infrastructure or a cautionary tale. We are watching the data-use disclosures and the first regulatory response closely, because in finance, trust is not a feature — it is the entire product.

Frequently Asked Questions

What is ChatGPT Personal Finance?

ChatGPT Personal Finance is a feature OpenAI launched on May 15, 2026, that lets ChatGPT Pro subscribers connect bank accounts through Plaid across more than 12,000 financial institutions. It analyzes spending, builds budgets, and answers money questions in plain language, with an Intuit tax integration confirmed as the next step.

How does ChatGPT connect to my bank account?

It connects through Plaid, the same financial data network behind apps like Venmo and Robinhood. Plaid handles the bank login and issues OpenAI a tokenized, scoped credential rather than your banking password. ChatGPT receives a structured stream of transactions and balances but does not log in to your bank directly.

Is ChatGPT Personal Finance free?

No. At launch it is gated to the ChatGPT Pro subscription tier. There is no separate charge for the feature itself beyond the existing Pro subscription, but it is not available on free ChatGPT.

How many banks does Plaid support for ChatGPT?

OpenAI cites 12,000+ financial institutions through Plaid, which covers effectively the entire US retail banking market plus most credit unions and fintech accounts. Reliability with smaller institutions can be inconsistent and may require periodic reconnection.

Is it safe to connect my bank account to ChatGPT?

The architecture is safer than typing a bank password into a chat box because Plaid brokers tokenized access and OpenAI never receives banking credentials. However, your full transaction history — a near-complete behavioral fingerprint — flows into the AI system. Users should verify their account's current data-use and training settings before linking.

Does OpenAI use my financial data to train its models?

OpenAI's exact training policy for this specific feature was not confirmed at launch. Enterprise and API tiers have historically offered no-training guarantees while consumer settings have been more nuanced. The responsible step is to check the current data-use settings in your own ChatGPT account before connecting any account.

How is ChatGPT Personal Finance different from Copilot Money or YNAB?

Copilot Money, Monarch, and YNAB are dedicated budgeting apps built on the same Plaid plumbing, often with better finance-specific UX. ChatGPT's advantage is distribution: it bundles a comparable conversational layer into a product 800 million people already use, removing the download and setup friction that limits standalone apps.

Is ChatGPT a replacement for a financial advisor?

It is not a registered investment adviser and does not custody assets or carry fiduciary accountability at launch. It can replace the entry-level work of building a first budget and answering basic affordability questions, but complex tax, estate, and wealth planning still rewards human judgment and accountability.

What is the Intuit tax integration?

OpenAI confirmed an Intuit integration is coming that would connect ChatGPT to tax preparation workflows. The exact timeline and scope remain unconfirmed, but it signals OpenAI intends to push from spending analysis toward more regulated, higher-stakes financial workflows.

Which companies are most disrupted by ChatGPT Personal Finance?

Standalone budgeting apps like Copilot Money, Monarch, and YNAB face the most direct pressure. Robo-advisors like Betterment and Wealthfront are partly insulated by their regulated status, and entry-level human financial advisors are pressured while complex advisory work is less exposed.

Does ChatGPT Personal Finance give investment advice?

At launch it analyzes spending and suggests budgets and savings plans, but it does not manage assets or hold an investment-adviser registration. Whether prescriptive budgeting recommendations at consumer scale eventually count as regulated financial advice is an open regulatory question and the defining uncertainty around the product.

How does this fit OpenAI's broader strategy?

It mirrors OpenAI's pattern of converting ChatGPT's reach into commercial surfaces — following the self-serve ChatGPT Ads Manager and the GPT-5.5 super-app direction. Finance is the consumer equivalent of the enterprise $4B deployment-company joint venture: own the integration layer where decisions get made, not just the model that answers questions.