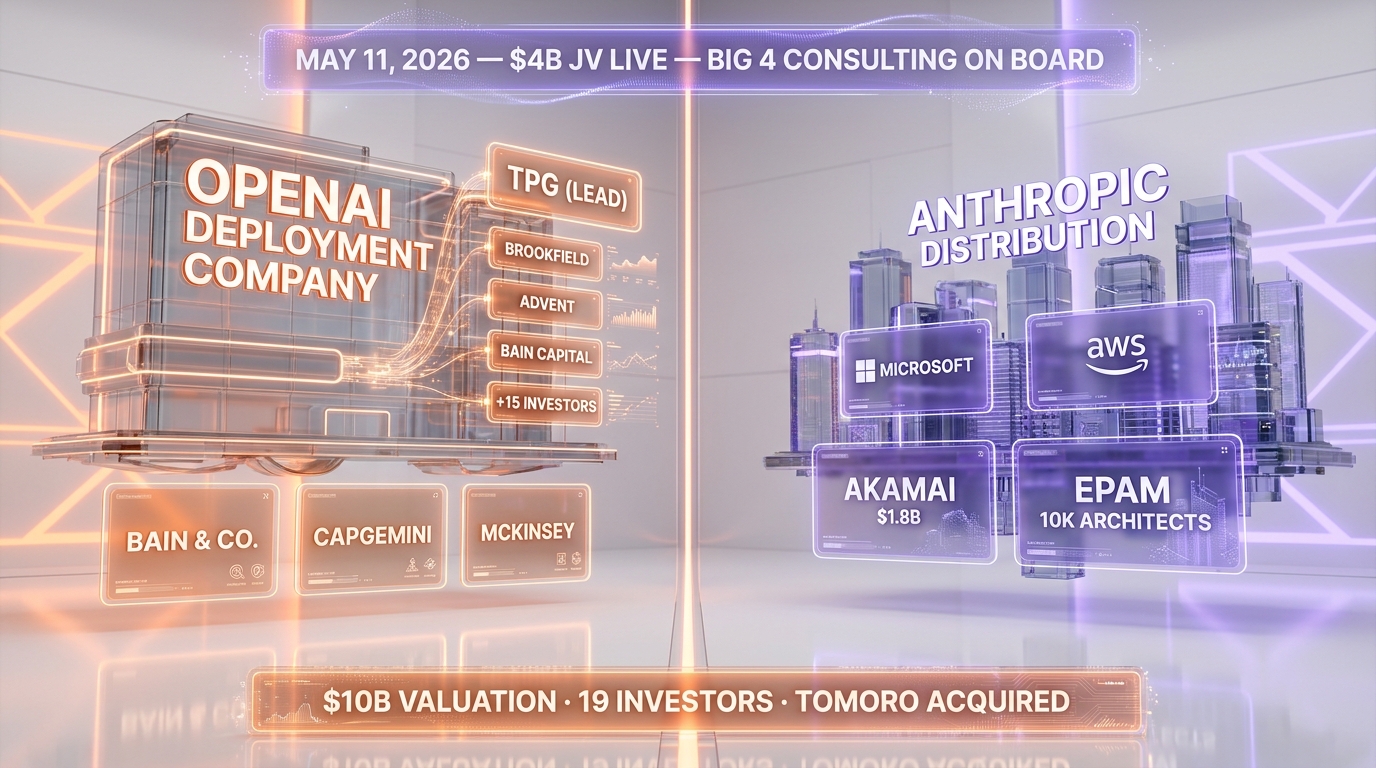

OpenAI officialized OpenAI Deployment Company on May 11, 2026 — a majority-owned joint venture that raised more than $4 billion from 19 global investors, with TPG as lead investor and Brookfield, Advent International and Bain Capital among co-investors, per the OpenAI announcement. Bain & Company, Capgemini and McKinsey signed on as integration partners. The simultaneous acquisition of Tomoro brings roughly 150 Forward Deployed Engineers in-house. The strategic move internalizes the consulting and systems-integration layer that has historically sat between AI vendors and enterprise buyers — a direct contrast with the Anthropic distribution playbook running through Microsoft, AWS and Akamai.

TL;DR — what just happened

- $4 billion+ raised for OpenAI Deployment Company, a majority OpenAI-owned joint venture announced on May 11, 2026 per PYMNTS reporting.

- $10 billion post-money valuation on the JV per Bloomberg coverage cited by PYMNTS — a 2.5x multiple on capital raised.

- 19 global investors total. TPG named as lead. Brookfield Asset Management, Advent International and Bain Capital named as co-investors. Full list not publicly disclosed.

- Integration partners: Bain & Company, Capgemini and McKinsey signed on as the consulting and systems-integration delivery layer.

- Tomoro acquisition announced simultaneously: an applied AI consulting firm founded in 2023 in partnership with OpenAI, bringing roughly 150 Forward Deployed Engineers and deployment specialists in-house.

- Denise Dresser, OpenAI Chief Revenue Officer, framed the launch: “AI is becoming capable of doing increasingly meaningful work inside organizations,” per PYMNTS.

- Anthropic parallel: announced its own $1.5B joint venture with Goldman Sachs, Blackstone and six other Wall Street firms exactly one week earlier on May 4, 2026 — with zero investor overlap.

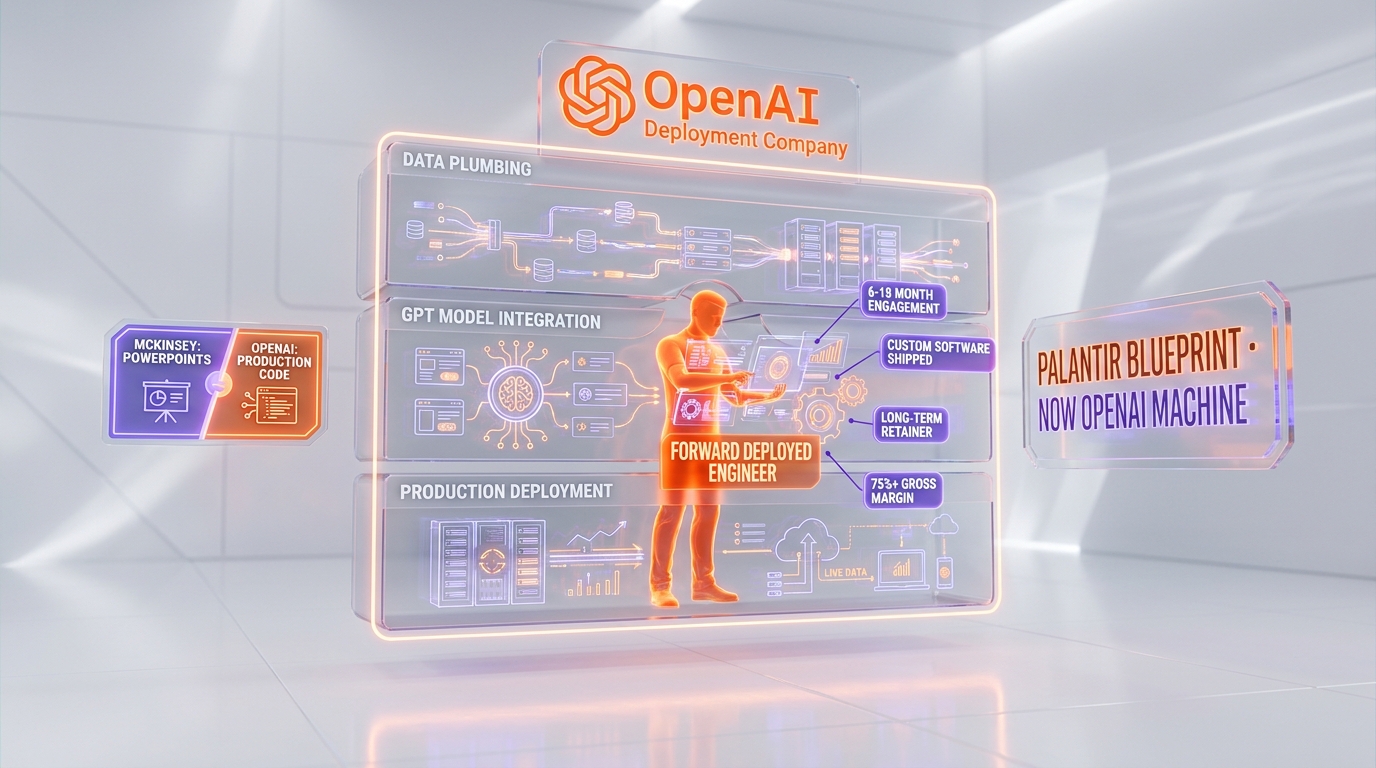

- Strategic frame: OpenAI has decided not to outsource the deployment of GPT-class models. It is buying the integration layer outright and putting Big Four consulting on its cap table.

What happened: $4B, 19 investors, three Big Four firms on the cap table

On May 11, 2026, OpenAI announced via its newsroom post that it had launched OpenAI Deployment Company, a new majority-owned joint venture that had already closed more than $4 billion in capital commitments from 19 global investors. PYMNTS, citing Bloomberg, reported the company was valued at $10 billion post-money. The structure is a JV. The capital is institutional. OpenAI retains majority ownership and operating control.

The investor list is the most strategically interesting piece. TPG, one of the largest alternative asset managers in the world with more than $230 billion in assets under management, was named as lead investor. Brookfield Asset Management ($1 trillion+ AUM), Advent International ($90 billion+ AUM) and Bain Capital ($185 billion+ AUM) joined as co-investors. The remaining 15 investors have not been publicly named as of May 11, 2026. Per PYMNTS, the cohort includes “global investment firms, consultancies and system integrators.”

The integration partners are where the announcement turns from a financing story into a strategic shock. Bain & Company, Capgemini and McKinsey — three of the most powerful management consulting and systems-integration firms in the world — have signed on as preferred integration partners for OpenAI Deployment Company. Bain & Company also took an equity stake in the JV per the firm's press release, extending a three-year existing Bain-OpenAI collaboration.

The simultaneous Tomoro acquisition is the operational backbone. Tomoro was founded in 2023 in partnership with OpenAI as an applied AI consulting and engineering firm. Named clients include Mattel, Supercell, Red Bull, Virgin Atlantic, Fidelity, Tesco and DPD across entertainment, finance, logistics and retail. The acquisition brings approximately 150 Forward Deployed Engineers and deployment specialists into OpenAI Deployment Company on day one, per PYMNTS reporting.

Why Bain, Capgemini and McKinsey are on the cap table

The strategic alignment of three Big Four-tier consultancies behind a single AI lab is the part of this announcement that should be reread carefully. McKinsey, Bain and Capgemini are not historically distribution partners for software. They are the firms that companies hire when they cannot decide what software to buy or how to use it. The fact that all three have placed strategic chips on OpenAI as the AI vendor — rather than Anthropic, Google or any other lab — carries direct implications for enterprise buying behavior over the next 24 months.

The Bain & Company press release is the most detailed public document on the partnership structure. Two senior Bain executives were quoted. Rebecca Burack, who leads Bain's Global Private Equity Practice, framed the rationale this way: “Creating value in portfolio companies today takes both strategic insight, real technical capability, and change management.” The framing is precise. Bain has decided that AI deployment is no longer pure advisory work — it requires the engineering muscle that Bain does not have in-house and that OpenAI Deployment Company can supply.

Chuck Whitten, Bain's Global Head of Digital Practices, was more direct: “The companies that deploy AI fastest and most effectively will pull away from their competitors, and we intend to make sure our clients are among them.” The translation is that Bain views OpenAI Deployment Company as the deployment vehicle through which it will deliver AI value to its private equity portfolio companies — a market segment where Bain has historical strength.

Brad Lightcap, OpenAI's COO, was quoted on the Bain partnership as well: “Bain has been a key partner across our ecosystem.” The reciprocal positioning matters. Bain's PE clients and portfolio companies get priority access for joint Bain-Deployment Company work. The implicit deal: Bain ships demand, OpenAI ships engineers and Claude-class models, both sides take a cut of the resulting deployment revenue.

What is conspicuously not said in any of the public materials is the structure of the McKinsey and Capgemini equity stakes — if any. Bain & Company explicitly took a stake. Whether McKinsey and Capgemini are equity holders or preferred partners on a contractual basis has not been disclosed as of the May 11, 2026 announcement.

The three integration partners in context

| Partner | Type | Revenue (approx.) | Headcount | Role in OpenAI Deployment Company |

|---|---|---|---|---|

| Bain & Company | Top-tier strategy consulting | $8B+ (FY2025) | ~19,000 | Equity stake + PE client channel |

| Capgemini | Global systems integrator | $25B+ (FY2025) | ~360,000 | Integration partner (equity TBD) |

| McKinsey & Company | Top-tier strategy consulting | $16B+ (FY2025) | ~45,000 | Integration partner (equity TBD) |

Three things stand out from this table. First, the combined revenue of the three partners exceeds $49 billion annually — this is the consulting channel that OpenAI Deployment Company now has formal access to. Second, the combined headcount is approximately 424,000 employees, a meaningful fraction of whom touch enterprise AI projects in some capacity. Third, BCG — the third member of the traditional “MBB” consulting trio — is conspicuously absent from the partner list, leaving an obvious opening for BCG to align with Anthropic or another lab in a counter-move.

Tomoro: the Forward Deployed Engineer machine OpenAI just bought

The Tomoro acquisition is the operational core of OpenAI Deployment Company. Without it, the announcement would have read as a financing exercise — capital plus partners but no execution layer. With Tomoro, OpenAI now has roughly 150 Forward Deployed Engineers and deployment specialists who have spent the last three years embedding inside enterprise customer environments and shipping production AI systems.

Tomoro was founded in 2023 in partnership with OpenAI as an applied AI consulting and engineering firm. The company's named client roster — Mattel, Supercell, Red Bull, Virgin Atlantic, Fidelity, Tesco, DPD — spans entertainment, finance, logistics and retail. The firm describes its product as “AI business strategy, custom AI solutions, enterprise infrastructure, and adoption services,” per the company's own website. Tomoro also maintained partnerships with Microsoft and NVIDIA in addition to OpenAI.

The strategic logic of the Tomoro buy is straightforward. OpenAI did not have an in-house Forward Deployed Engineer practice at scale before May 11, 2026. Tomoro had three years of head start. Building 150 FDEs from scratch would have taken OpenAI 18 to 24 months and required organizational muscle the lab does not have. Buying Tomoro accelerates the timeline to day zero and inherits a customer reference list that includes Fortune 500 brands across four sectors.

The Forward Deployed Engineer model itself is no longer experimental. Palantir built a $400+ billion market capitalization on the FDE pattern: engineers embed inside customer organizations, learn the workflows, ship custom integrations and stay on long term as the relationship deepens. ServiceNow and Accenture jointly announced a Forward Deployed AI Engineering practice earlier in 2026. Anthropic's parallel JV with Goldman and Blackstone is explicitly built on the Palantir FDE model. Every AI vendor with enterprise ambition has now adopted the same delivery shape. The question is execution at scale — and Tomoro gives OpenAI a 150-engineer head start.

What the 150 FDEs unlock

- Sector coverage on day one: entertainment (Mattel, Supercell), beverage (Red Bull), aviation (Virgin Atlantic), financial services (Fidelity), retail (Tesco) and logistics (DPD).

- Enterprise reference customers that OpenAI Deployment Company can name in sales motions without having to prove the underlying engineering capability.

- Existing playbooks for AI deployment in production environments, including data plumbing, model selection, evaluation and ongoing maintenance.

- UK and EMEA presence (Tomoro is headquartered in the UK), giving OpenAI Deployment Company a non-US geographic footprint that pure-US JVs cannot match.

- Microsoft and NVIDIA partnership inheritance, which Tomoro maintained separately from OpenAI and which the new entity now absorbs.

The Anthropic contrast: distribution vs. internalization

The most strategically clarifying way to read the OpenAI Deployment Company announcement is alongside Anthropic's enterprise distribution playbook of the same period. Both labs have decided that 2026 is the year enterprise AI deployment becomes the primary revenue channel. They have made structurally opposite bets on how to win that channel.

Anthropic's bet is distribution-led. The lab has signed an $1.8 billion seven-year cloud deal with Akamai, runs its primary commercial channel through Microsoft Azure and AWS, and has built a network of 10,000 Claude-certified architects via EPAM plus an AI-Native Engineering team partnership with NEC Japan. The model is leverage: Anthropic sells the model, partners sell the integration, the channel does the work. Anthropic's own $1.5B JV with Goldman, Blackstone and six other Wall Street firms layers a private equity portfolio company channel on top — the engineers ship through the JV, not through Anthropic directly.

OpenAI's bet is internalization-led. OpenAI Deployment Company sits underneath OpenAI's majority ownership. The 150 FDEs from Tomoro are now OpenAI's engineers, not partner engineers. Bain & Company, Capgemini and McKinsey are integration partners, but the deployment vehicle is OpenAI-controlled. Where Anthropic is building a network of partner channels with the AI lab as supplier, OpenAI is building one large vertically integrated enterprise services company with the AI lab as parent.

| Dimension | OpenAI Deployment Company | Anthropic enterprise stack |

|---|---|---|

| Capital raised (services entity) | $4B+ at $10B valuation | $1.5B JV with 8 investors |

| Ownership structure | OpenAI majority owner of single JV | Network of partnerships + JV |

| FDE engineering layer | ~150 in-house via Tomoro | Partner engineers (EPAM, NEC, JV) |

| Consulting/integration channel | Bain, Capgemini, McKinsey (direct) | Wall Street PE portfolio companies (JV) |

| Cloud distribution | Microsoft Azure (primary) | AWS, Azure, Akamai ($1.8B), GCP |

| Certified architect network | To be built | 10,000 via EPAM (already shipped) |

| Strategic frame | Vertical integration | Distribution leverage |

| Risk profile | Concentration in one vehicle | Diversification across channels |

Neither approach is obviously correct. The vertical integration play wins if OpenAI Deployment Company can scale fast enough to capture the mid-market and Fortune 500 budgets that consulting firms have historically harvested. The distribution leverage play wins if Anthropic's partners can move faster collectively than a single OpenAI-controlled entity can mobilize. The next 18 months of named customer wins on both sides will settle the question.

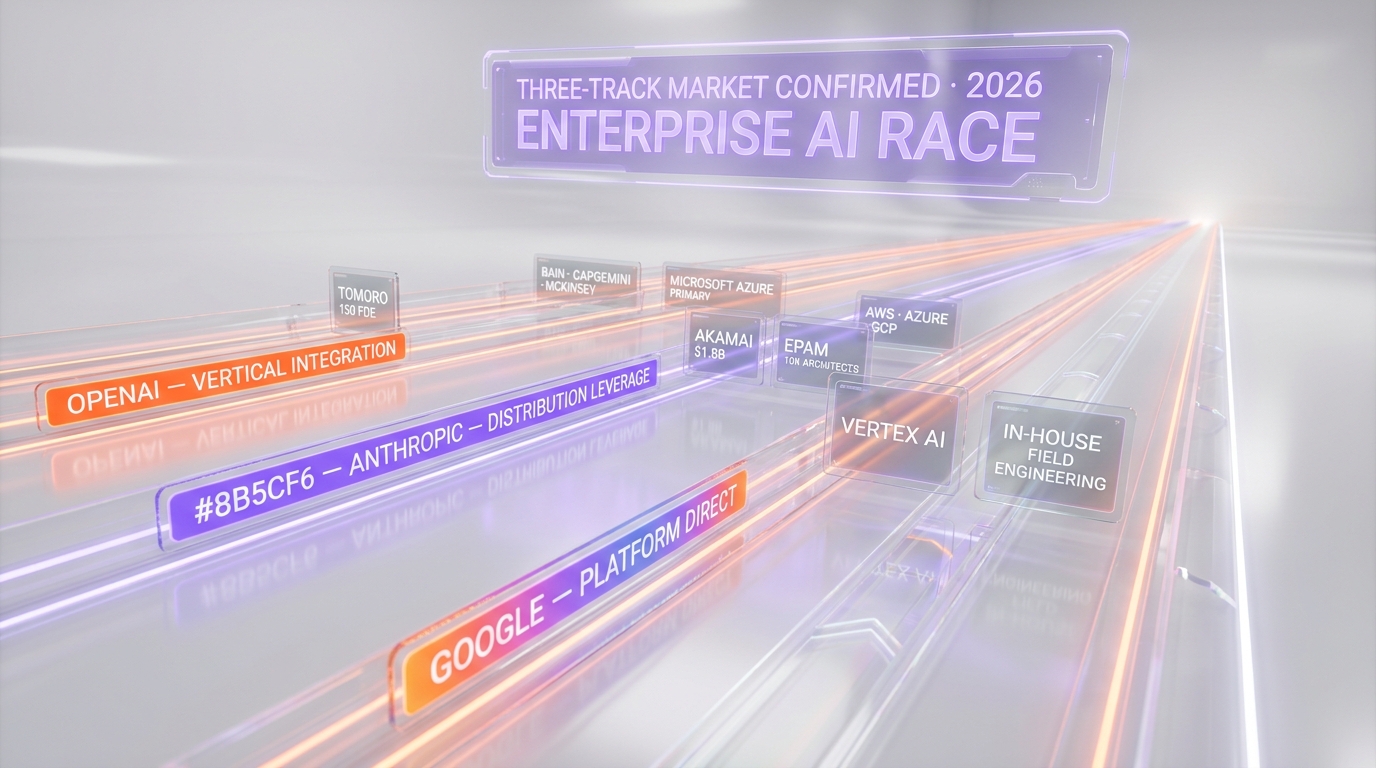

The three-track market thesis confirmed

OpenAI Deployment Company is the announcement that confirms the three-track market thesis we have been tracking on ThePlanetTools.ai since the GPT-5.5 super-app strategy launch in April 2026. The three labs are now visibly running different strategies, with different theories of how enterprise AI gets distributed and monetized over the next five years.

Track one — OpenAI: consumer super-app plus vertical integration in enterprise. ChatGPT remains the dominant consumer surface with hundreds of millions of weekly active users. OpenAI Deployment Company is the enterprise services layer underneath it. Microsoft Azure is the primary cloud distribution. The strategic frame is to own the entire stack from chat interface through enterprise deployment, with as few intermediaries as possible. The Tomoro acquisition is the operational expression of that frame.

Track two — Anthropic: distribution leverage plus vertical depth in specific markets. Claude is the model. Microsoft, AWS, Akamai and GCP are the clouds. EPAM, NEC, Accenture-style integrators are the implementation partners. Goldman/Blackstone-backed JVs are the private-sector services channel. Federal deployment runs through cleared partners. The bet is that Anthropic can move faster by being the model layer for many ecosystems rather than the parent of one vertical stack.

Track three — Google: platform-direct with Vertex AI. Google's Gemini family runs primarily through Google Cloud Vertex AI directly into enterprise customers, with Google's own field engineering and customer success teams. The strategic logic is the same as OpenAI's vertical integration play, but with Google Cloud as the host platform rather than a freestanding services JV. Google's enterprise pitch is “everything in one platform” rather than “everything from one vendor.”

The reason this matters operationally for any enterprise AI buyer in 2026: the three tracks have different cost structures, different speed profiles, different lock-in characteristics and different reference customer pools. The decision of which lab to standardize on is no longer just a model-quality decision — it is also a decision about which deployment shape the buyer wants to live with for the next three years.

Forward Deployed Engineer model: deep dive

The Forward Deployed Engineer pattern has now been formally adopted by Palantir, ServiceNow + Accenture, Anthropic and OpenAI in the span of 12 months. Understanding the model is necessary to understand what OpenAI Deployment Company is actually buying with the Tomoro deal.

An FDE is not a sales engineer, an implementation consultant or a customer success manager. The role combines all three. An FDE physically embeds inside the customer organization — on-site if the customer is large enough, remote with deep engagement if not — for engagements that typically run six to 18 months. During the engagement, the FDE learns the customer's workflows, identifies the highest-value AI use cases, ships custom integrations into existing production systems, trains internal teams on the deployed software and stays on as a long-term technical relationship owner.

The economics differ structurally from traditional consulting. Where McKinsey, Bain and BCG sell PowerPoints at $500 to $5,000 per hour with no software deliverable, the FDE model sells engineering hours at similar or higher rates with custom software shipped in production. The recurring revenue layer comes from the underlying platform licenses — Claude API for Anthropic, GPT-class API for OpenAI Deployment Company, Foundry for Palantir — and from ongoing maintenance retainers.

Why this is now the dominant enterprise AI delivery shape:

- Production deployment is the customer's actual pain. The hardest part of enterprise AI is not the model — it is the data plumbing, security review, evaluation harness, change management and ongoing maintenance. FDEs handle all of that. Strategy decks do not.

- Speed beats sophistication. A working production AI system shipped in 90 days creates measurable ROI faster than a 12-month strategy engagement that leaves an IT team to figure out implementation.

- Stickiness compounds. Once an FDE has shipped three custom integrations into a customer's production stack, the switching cost to a different AI vendor is enormous. The FDE relationship is the moat.

- Margins are higher than pure consulting. Software licenses compound on top of engineering revenue, lifting blended gross margins from the 60% consulting baseline to 75%+ on mature accounts.

This is what OpenAI Deployment Company is buying with Tomoro: a 150-engineer FDE machine plus the operating playbook to scale it to 500 or 1,000 FDEs over the next 24 months. The capital base supports that scaling. The Big Four consulting partnerships provide the demand pipeline. The math works as long as enterprise AI deployment continues to be a large and growing budget line for Fortune 1000 buyers.

What this means for McKinsey, BCG, Bain and the consulting industry

Bain & Company has solved its AI-deployment problem by buying equity in OpenAI Deployment Company and locking in priority access. McKinsey and Capgemini have solved it via partnership without (publicly disclosed) equity. BCG is now the obvious gap on the consulting map. Whatever BCG announces in the next six months — an Anthropic partnership, a Google Vertex AI tie-up, an open-source LLM bet, an in-house FDE practice — will be a direct response to the May 11 OpenAI move.

The wider consulting industry faces a more uncomfortable question. If the three largest strategy firms have decided that enterprise AI deployment requires partnership with the AI labs themselves, the implicit message is that pure advisory work is no longer sufficient to win enterprise AI engagements. Tier-two strategy firms, regional consultancies and boutique IT integrators without lab partnerships now have a structural disadvantage on AI deals.

One specific operational shift to watch: pricing. McKinsey's day rates are calibrated to the value of strategic advice. OpenAI Deployment Company's day rates will be calibrated to the value of shipped software plus services. If the deployment company prices below McKinsey on net while shipping more measurable output, the consulting industry's pricing model breaks down at the mid-market end first and works its way upmarket from there.

None of this kills consulting. The CEO-to-CEO advisory layer, board-level strategic engagements, M&A advisory and restructuring work all remain insulated. What is exposed is the broad “digital and AI transformation” layer that drove consulting industry growth from 2019 through 2024. That layer now has a structurally better-funded and better-aligned competitor with three of the biggest strategy firms on its cap table.

What we still do not know

Several material details remain undisclosed in the public announcements. We will not speculate on them.

- Equity split. OpenAI Deployment Company is majority-owned by OpenAI per the announcement, but the exact percentage and the dilution profile across the 19 investors are not public.

- The 15 unnamed investors. Only TPG (lead), Brookfield, Advent and Bain Capital have been named. The remaining 15 investors include “global investment firms, consultancies and system integrators” per PYMNTS, but specific names are not disclosed.

- Equity stakes for McKinsey and Capgemini. Bain & Company has explicitly taken a stake. Whether McKinsey and Capgemini are equity holders, contractual preferred partners or something in between is not public.

- Tomoro acquisition price. The amount paid for Tomoro is not disclosed.

- CEO of OpenAI Deployment Company. No CEO has been publicly named. Denise Dresser, OpenAI's CRO, is the only OpenAI executive quoted in launch coverage. Brad Lightcap appears in the Bain & Company press release.

- Year-one revenue or FDE headcount targets. The announcement does not disclose what OpenAI Deployment Company is targeting for its first 12 months.

- Geographic scope of operations. Tomoro is UK-based; how much of OpenAI Deployment Company will operate outside North America is not stated.

What to watch in the next 90 days

Four threads will determine whether the May 11 announcement is a structural turning point or a financing footnote.

First, named customer wins. Tomoro brings Mattel, Supercell, Red Bull, Virgin Atlantic, Fidelity, Tesco and DPD as inherited reference customers. The credibility test is whether OpenAI Deployment Company can convert at least three new named Fortune 500 customers in the next two quarters — ideally with named deployment scope and named revenue.

Second, BCG's counter-move. Boston Consulting Group is the visible gap in the AI lab partnership map. Whichever lab BCG aligns with — Anthropic looks most likely — the move will reshape the consulting-AI competitive landscape. A BCG-Anthropic partnership in the next 60 days would be the cleanest signal.

Third, the cloud distribution detail. OpenAI's cloud commercial relationships run primarily through Microsoft Azure. Whether OpenAI Deployment Company is Azure-exclusive, multi-cloud or builds direct infrastructure relationships outside Microsoft will tell us how independent the new entity is from its parent.

Fourth, the 15 unnamed investors. PYMNTS noted that the 19 backers include consultancies and system integrators alongside investment firms. If additional Big Four names (Deloitte, EY, KPMG, PwC), additional systems integrators (Accenture, IBM, TCS, Infosys) or additional alternative asset managers emerge in subsequent disclosures, each name will rebalance the competitive map.

Our take

OpenAI Deployment Company is the most significant strategic move OpenAI has made in 2026 outside of the GPT-5.5 launch. The $4 billion figure is large but is not the headline. The headline is that OpenAI has decided to own the consulting and integration layer of enterprise AI deployment rather than rent it through partners — and has assembled the capital, the Big Four endorsements and the operational engine (Tomoro's 150 FDEs) to make the bet structural rather than aspirational.

The strategic contrast with Anthropic is now sharper than at any point in either lab's history. Anthropic is betting on distribution leverage through Microsoft, AWS, Akamai, EPAM, NEC and Goldman/Blackstone-backed services JVs. OpenAI is betting on vertical integration through one majority-owned services entity with the Big Four strategy firms on the cap table. Both bets are defensible. They are also incompatible — one of these models will compound faster than the other over the next 24 months, and the answer will define which lab dominates enterprise AI by 2028.

For enterprise buyers, the practical implication of May 11, 2026 is that the AI vendor selection conversation now has a procurement and deployment-shape dimension layered on top of the model-quality dimension. Standardizing on OpenAI means buying into a vertically integrated services stack with consulting partnerships built in. Standardizing on Anthropic means buying into a model layer with a partner ecosystem doing the integration work. Standardizing on Google means buying into a platform-direct deployment running through Google Cloud. None of these is wrong. They are different operating models with different cost, speed, lock-in and risk profiles.

For the consulting industry, the May 11 move is not the end. It is the moment where the AI threat becomes structural rather than theoretical. Bain & Company has bought a seat at the new table. McKinsey and Capgemini have partnered into it. BCG will move next. The firms that do not adapt fast will lose mid-market AI implementation work first, then enterprise digital transformation work, and finally the upper end of the consulting profit pool over a horizon longer than three years but shorter than ten.

For Wall Street, the takeaway is more direct. TPG, Brookfield, Advent and Bain Capital have just placed a multibillion-dollar bet on the proposition that enterprise AI deployment is a structurally large and durable services market — one large enough that a single $10 billion JV inside one AI lab can be a venture-grade outcome. Whether the bet pays off depends entirely on execution from here.

Frequently asked questions

What is OpenAI Deployment Company?

OpenAI Deployment Company is a new majority OpenAI-owned joint venture launched on May 11, 2026 to deploy enterprise AI services to large customers. The entity raised more than $4 billion from 19 global investors at a reported $10 billion post-money valuation. TPG is the lead investor, with Brookfield Asset Management, Advent International and Bain Capital named as co-investors. The simultaneous acquisition of Tomoro brings roughly 150 Forward Deployed Engineers and deployment specialists in-house on day one.

Who are the lead investors in OpenAI Deployment Company?

TPG was named as lead investor. Brookfield Asset Management, Advent International and Bain Capital were named as co-investors. The total investor count is 19 firms across “global investment firms, consultancies and system integrators” per PYMNTS reporting. The remaining 15 investors have not been publicly named as of the May 11, 2026 announcement.

What is the valuation of OpenAI Deployment Company?

OpenAI Deployment Company was valued at $10 billion post-money on the $4 billion round, according to Bloomberg reporting cited by PYMNTS. This represents a 2.5x multiple on capital raised. OpenAI retains majority ownership and operating control of the joint venture per the company's official announcement.

Which consulting firms are integration partners?

Bain & Company, Capgemini and McKinsey signed on as integration partners. Bain & Company has explicitly taken an equity stake in the joint venture per the firm's press release. Whether McKinsey and Capgemini hold equity or operate on a contractual preferred-partner basis has not been disclosed. Boston Consulting Group (BCG) — the third member of the “MBB” strategy consulting trio — is conspicuously absent from the partner list.

What is Tomoro and why did OpenAI acquire it?

Tomoro is an applied AI consulting and engineering firm founded in 2023 in partnership with OpenAI. The company has approximately 150 Forward Deployed Engineers and deployment specialists, with named clients including Mattel, Supercell, Red Bull, Virgin Atlantic, Fidelity, Tesco and DPD across entertainment, finance, logistics and retail. OpenAI acquired Tomoro on May 11, 2026 to give OpenAI Deployment Company an operational FDE engineering layer on day one rather than building it from scratch over 18 to 24 months. The acquisition price has not been disclosed.

How does this compare to Anthropic's enterprise strategy?

Anthropic and OpenAI have made structurally opposite bets on enterprise AI deployment. OpenAI is internalizing the consulting and integration layer via OpenAI Deployment Company (one majority-owned vehicle, 150 in-house FDEs, Big Four consulting partnerships on the cap table). Anthropic is leveraging external distribution through Microsoft Azure, AWS, Akamai ($1.8B seven-year deal), EPAM (10,000 certified architects), NEC Japan and a separate $1.5B services JV with Goldman Sachs, Blackstone and six other Wall Street firms. The two approaches are incompatible — one will compound faster over the next 24 months.

What is a Forward Deployed Engineer?

A Forward Deployed Engineer (FDE) is a hybrid sales engineer, implementation consultant and customer success role pioneered at Palantir. FDEs physically or virtually embed inside customer organizations for engagements typically running six to 18 months, learn customer workflows, identify high-value AI use cases, ship custom integrations into production systems, train internal teams and stay on as long-term technical relationship owners. The model has been adopted by Palantir, ServiceNow + Accenture, Anthropic and now OpenAI Deployment Company in the span of 12 months — making FDE the dominant enterprise AI delivery shape of 2026.

Why is BCG not a partner?

Boston Consulting Group is the visible gap in the AI lab partnership map. Bain & Company has aligned with OpenAI Deployment Company with an equity stake. McKinsey has signed on as an integration partner with OpenAI as well. BCG has not announced a comparable partnership with any major AI lab as of May 11, 2026. The most likely counter-move is a BCG alignment with Anthropic, Google or a smaller AI lab in the next 60 to 90 days. Whichever direction BCG moves will reshape the consulting-AI competitive landscape.

Is McKinsey or Capgemini taking an equity stake?

This has not been publicly disclosed as of the May 11, 2026 announcement. Bain & Company explicitly took an equity stake in OpenAI Deployment Company per the firm's press release. McKinsey and Capgemini have been confirmed as integration partners, but the structure of their participation — equity holder, contractual preferred partner or something in between — remains undisclosed.

What is the strategic significance for enterprise buyers?

The AI vendor selection conversation in 2026 now has a procurement and deployment-shape dimension layered on top of model quality. Standardizing on OpenAI Deployment Company means buying into a vertically integrated services stack with Big Four consulting partnerships built in. Standardizing on Anthropic means buying into a model layer with a partner ecosystem (Akamai, EPAM, NEC, Goldman/Blackstone JV) doing the integration work. Standardizing on Google Vertex AI means buying into a platform-direct deployment running through Google Cloud. The three approaches have different cost, speed, lock-in and risk profiles that buyers need to evaluate alongside model performance.

Who is the CEO of OpenAI Deployment Company?

No CEO has been publicly named as of the May 11, 2026 launch. Denise Dresser, OpenAI's Chief Revenue Officer, is quoted in PYMNTS coverage framing the strategic rationale. Brad Lightcap, OpenAI's COO, appears in the Bain & Company press release on the partnership structure. Operating leadership, brand identity and governance details for OpenAI Deployment Company have not been disclosed, suggesting these are still being negotiated or staged for a later announcement.

When will OpenAI Deployment Company start shipping customer engagements?

OpenAI Deployment Company is operational on day one thanks to the Tomoro acquisition. Tomoro's existing client roster — Mattel, Supercell, Red Bull, Virgin Atlantic, Fidelity, Tesco and DPD — transfers to the new entity, and Tomoro's 150 Forward Deployed Engineers continue their active engagements under OpenAI Deployment Company branding. New named customer wins beyond the Tomoro inheritance are expected in Q3 and Q4 2026 earnings cycles from clients of Bain & Company, Capgemini and McKinsey portfolios.