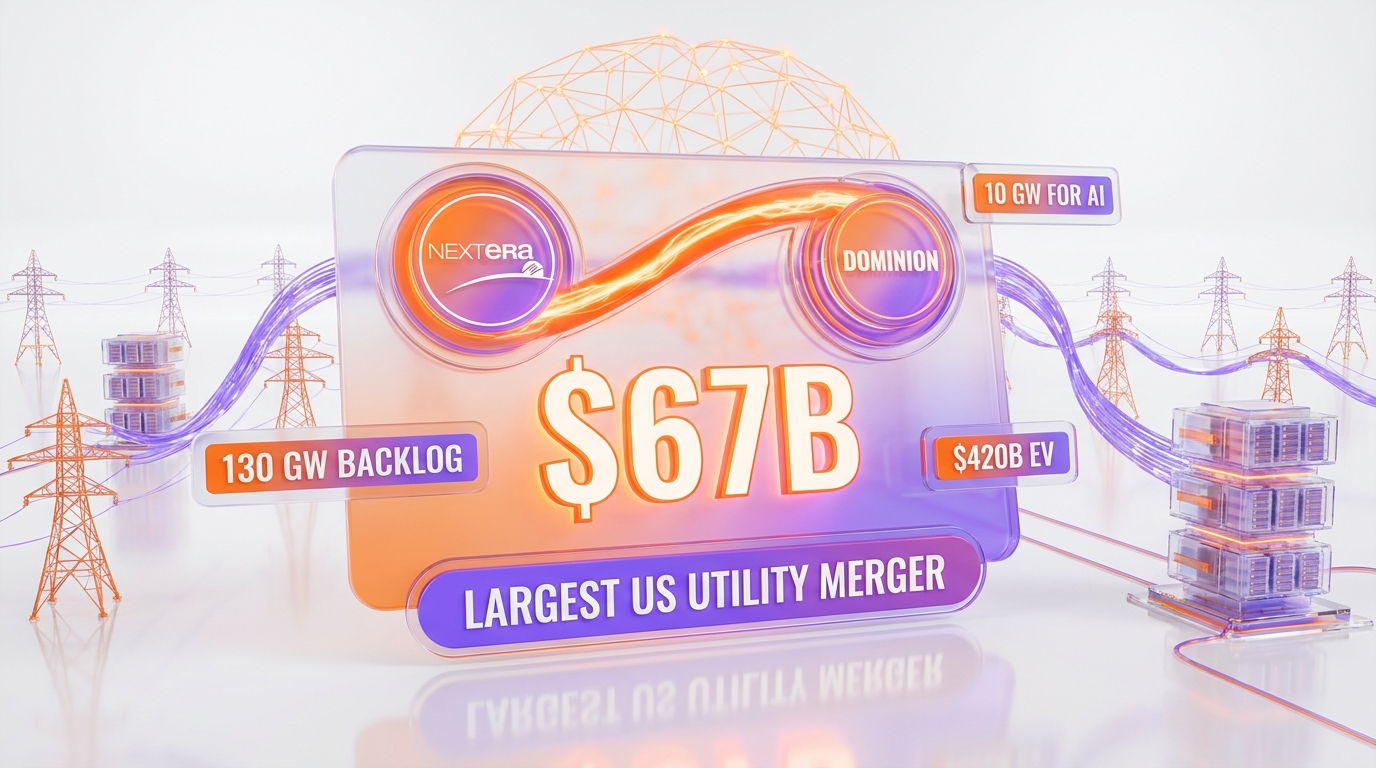

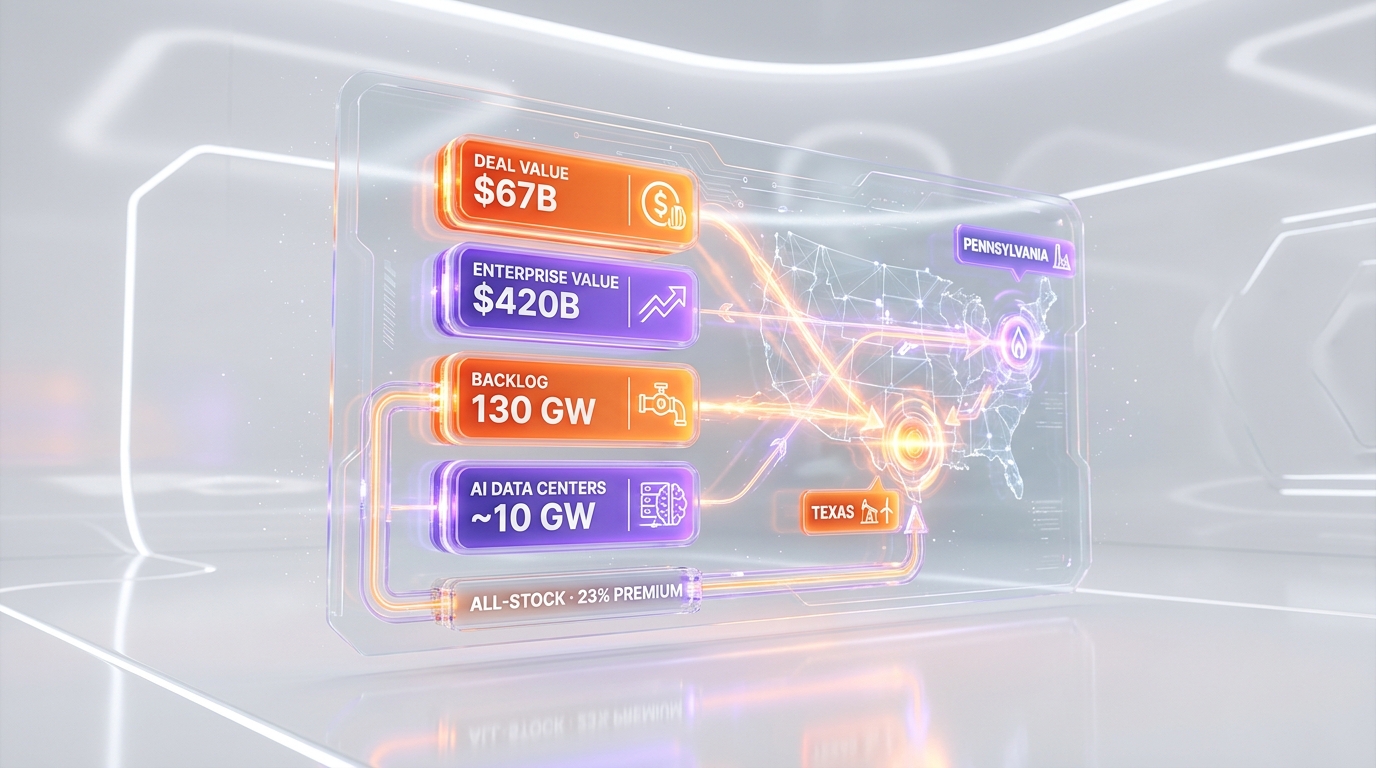

Why did NextEra buy Dominion for $67 billion? To meet AI data-center electricity demand — the largest utility merger in US history and the biggest energy deal since ExxonMobil bought Mobil in 1998. Announced May 18, 2026, the all-stock transaction creates a combined company with roughly $420 billion in enterprise value, a ~130 GW construction backlog, and nearly 10 GW committed to AI data-center hubs in Texas and Pennsylvania. The strategic thesis is blunt: the AI race is no longer won on GPUs — it is won on electrons.

What Happened

On May 18, 2026, NextEra Energy announced it will acquire Dominion Energy in an all-stock deal valued at nearly $67 billion. The transaction is the largest utility merger ever recorded in the United States and, by deal value, the biggest energy acquisition since ExxonMobil absorbed Mobil in 1998. NextEra shareholders will own approximately 74.5% of the combined entity; the offer represents a roughly 23% premium over Dominion's $54.3 billion market capitalization as of May 15, 2026.

The combined company carries an enterprise value of around $420 billion, making it the third-largest US energy company by enterprise value behind ExxonMobil and Chevron, and — per the merger communications — the world's largest regulated electric utility by market capitalization. It will operate from dual headquarters in Juno Beach, Florida and Richmond, Virginia, serving roughly 10 million customer accounts, with an annual capital spending budget reported at about $59 billion.

The number that matters most is the build pipeline. The merged company holds a combined construction backlog of roughly 130 gigawatts, with nearly 10 GW explicitly committed to AI data-center hubs across Texas and Pennsylvania — capacity reportedly structured alongside US and Japanese government participation. Dominion already powers the world's largest data-center market in northern Virginia, the physical heart of US cloud infrastructure.

"Our country is at an inflection point. The demand for electricity is increasing unlike anything we've seen in generations," said NextEra CEO John Ketchum. "We are the only ones out there really building across the United States. We are a builder at our heart."

Subject to shareholder and regulatory approval — federal sign-off plus state public utility commissions — the companies expect the transaction to close within roughly 12 to 18 months, targeting 2027. Reported figures cross-checked across Fortune, CNBC, and the official SEC Form 425 filings; where figures diverged, the more conservative reported value was used.

Why It Matters: The AI Race Moved to the Power Plant

For three years, the AI competitive story was told in chips. Who had the most NVIDIA GPUs. Who locked the most TSMC wafer capacity. Who shipped the highest benchmark scores. The NextEra-Dominion deal reframes that story in a single move: the binding constraint on frontier AI is no longer silicon — it is the electron supply that silicon consumes.

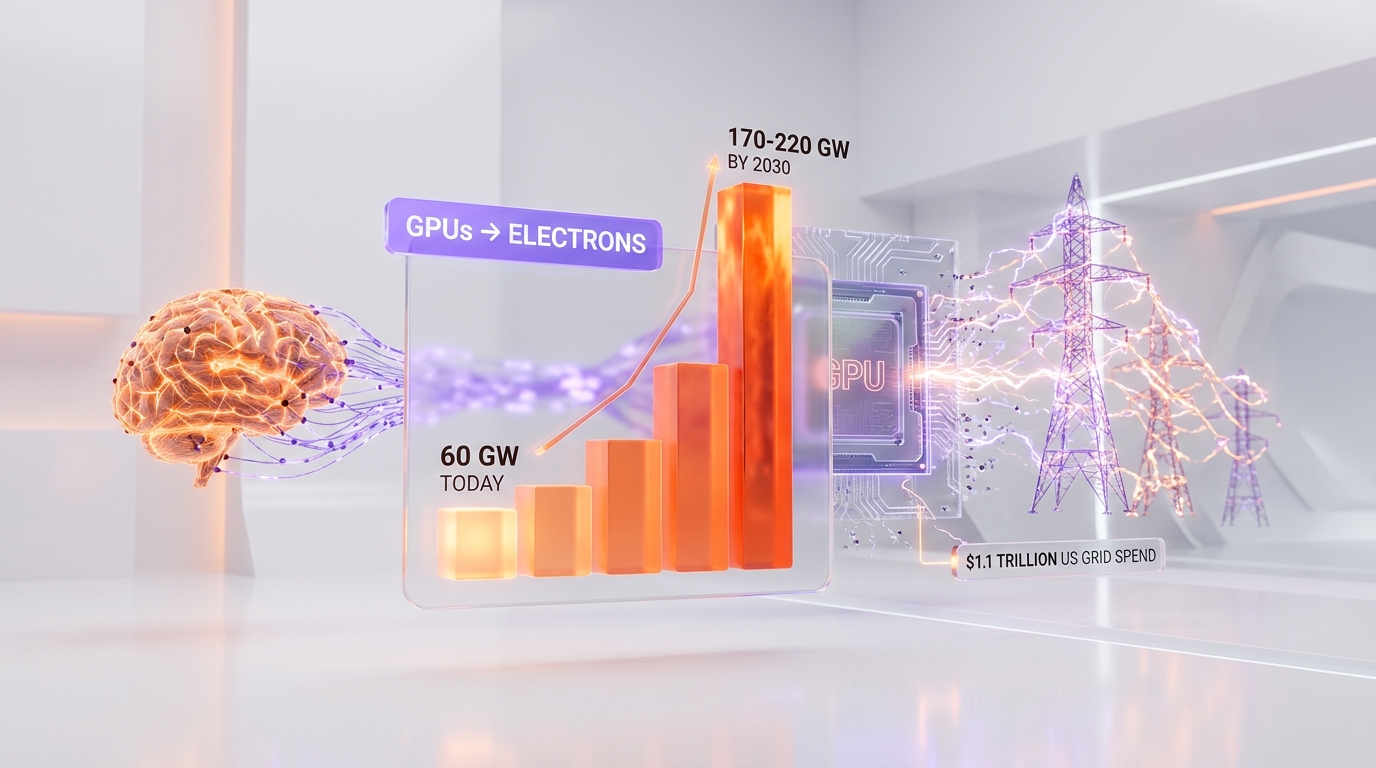

The macro backdrop makes the point. According to the Edison Electric Institute, US electric companies will spend more than $1.1 trillion on the grid over the next five years — roughly $208 billion in 2025 alone — to absorb demand from data centers, AI, and economy-wide electrification. That is a step-change: investor-owned utilities spent about $765 billion across the prior five-year period through 2024. Data-center electricity demand is projected to grow roughly 20% per year through 2030, climbing from about 60 GW today toward 170–220 GW, with aggressive scenarios reaching 300 GW.

This is the same structural pressure we documented when GridCARE raised $64 million to unlock latent grid capacity for AI, and when Anthropic committed to a 10-gigawatt compute empire. The pattern is consistent across the entire sector: AI labs and hyperscalers are now competing for interconnection queue positions and firm power contracts with the same intensity they once reserved for accelerator allocation. NextEra and Dominion just consolidated the supply side of that market into a single counterparty.

Why does a utility merger answer an AI question? Because power is the one input in the AI stack that cannot be conjured on a quarterly roadmap. A GPU cluster can be installed in months. A new high-voltage transmission corridor or a firmed gigawatt of generation takes years and survives multiple regulatory cycles. Whoever controls the build pipeline — the 130 GW backlog — controls the pace at which AI capacity can physically come online. That is the asset NextEra paid $67 billion to assemble.

The Bottleneck Has a Name: Interconnection, Not Inference

Inside hyperscaler and frontier-lab planning, the practical chokepoint is rarely "can we buy chips." It is "can we get a multi-gigawatt site energized on a timeline that matches the model roadmap." Grid interconnection queues in key US markets stretch years deep. Transformer lead times have blown out. Firm capacity — power available on demand, not just when the wind blows — has become the scarce, priced commodity.

NextEra brings the largest US renewables and battery-storage fleet and a deep development machine. Dominion brings the regulated utility footprint that physically serves northern Virginia — Data Center Alley — plus a nuclear base and gas generation. The combined entity is positioned, per the merger materials, as the world leader in renewables and storage, the US leader in natural gas generation, and the number-two player in nuclear. That portfolio is precisely the mix an AI buildout needs: cheap energy from renewables, firmness from gas and nuclear, and dispatch flexibility from storage.

This is also why the ~10 GW data-center commitment in Texas and Pennsylvania reads as the real headline rather than a footnote. Texas (ERCOT) and the PJM footprint that includes Pennsylvania are the two regions where AI load growth is colliding hardest with grid limits. Pre-committing nearly 10 GW into those exact corridors is a statement that the merged company intends to be the default power counterparty for the next wave of AI campuses — the way Anthropic locked SpaceX's Colossus 1 for compute, but one layer down the stack, at the substation.

How It Compares: Consolidation Over Construction

There are two strategic responses to a power-constrained AI economy. The first is organic build — finance, permit, and construct generation and transmission yourself, the path GridCARE accelerates by surfacing hidden grid headroom and the path hyperscalers attempt with behind-the-meter gas and small modular reactors. The second is consolidation — buy the company that already holds the backlog, the interconnection positions, and the regulatory relationships. NextEra chose the second, decisively.

The logic is timing arbitrage. Organic generation build is slow and queue-bound. By acquiring Dominion, NextEra absorbs a ready-made 130 GW pipeline and an incumbent's regulatory standing in Virginia and beyond in one transaction, rather than waiting out a decade of permitting. For AI buyers, fewer, larger power counterparties means simpler — though more concentrated — procurement. For regulators, it raises the obvious question of how much of the US power build pipeline should sit inside a single balance sheet.

Set against the broader efficiency narrative — research like MIT's waste-heat analog computing work aiming to cut the energy AI consumes per computation — the deal underlines a hard near-term truth: efficiency gains are real but gradual, while AI demand is compounding now. Utilities are not betting the bottleneck disappears. They are betting it widens, and pricing assets accordingly. A $67 billion all-stock bid is not a hedge — it is a conviction trade on sustained, structural power scarcity.

The Strategic Read

Three things stand out about how this deal is positioned. First, the framing is explicit rather than implied: this is marketed as an AI-power deal, not a generic utility roll-up. Management is anchoring the entire narrative — and a 23% premium — on data-center electricity demand. That is a deliberate bet that the AI-power thesis is durable enough to underwrite the largest utility merger in US history.

Second, the structure concentrates the supply side. One company would hold roughly 130 GW of backlog, the dominant renewables-and-storage fleet, a top nuclear and gas position, and the utility that serves the world's densest data-center market. For AI builders, that is both a feature — a single, capable counterparty able to commit 10 GW — and a risk: power procurement leverage shifts toward the supplier exactly as demand goes vertical.

Third, the timeline is the soft spot. A 12-to-18-month close targeting 2027, gated by federal regulators and multiple state utility commissions, runs straight into an active policy debate about whether data-center load should socialize grid costs onto ordinary ratepayers. The strategic logic is sound; the regulatory path is the variable that determines whether the thesis converts into delivered gigawatts on the timeline AI roadmaps assume.

What's Next

Watch four signals. One: regulatory posture — how state commissions in Virginia and Florida, plus federal authorities, treat a deal that concentrates this much of the national power build pipeline. Two: the AI customer slate — which hyperscalers and frontier labs sign firm contracts against the ~10 GW Texas and Pennsylvania commitments, and at what price. Three: competitive response — whether other large utilities pursue their own consolidation, accelerating an AI-driven wave of power-sector M&A. Four: the ratepayer question — whether AI load growth is funded by the data-center operators driving it or quietly spread across consumer bills.

The clearest takeaway needs no forecast. The center of gravity in the AI race has moved from the data-center floor to the power plant. The companies that win the next phase will not necessarily be the ones with the best models or the most GPUs — they will be the ones that secured the electrons first. A $67 billion all-stock merger is the loudest possible confirmation that the smart money already believes it.

Frequently Asked Questions

Why did NextEra acquire Dominion Energy for $67 billion?

To position for surging AI data-center electricity demand. Announced May 18, 2026, the all-stock deal creates the largest US electric utility, combining a ~130 GW construction backlog with Dominion's grip on the northern Virginia data-center market. It is the largest utility merger in US history and the biggest energy acquisition since ExxonMobil bought Mobil in 1998.

How big is the combined NextEra-Dominion company?

The combined entity carries roughly $420 billion in enterprise value — the third-largest US energy company behind ExxonMobil and Chevron, and the world's largest regulated electric utility by market capitalization. It serves about 10 million customer accounts with an annual capital spending budget near $59 billion.

How much power is committed to AI data centers?

Nearly 10 gigawatts is explicitly committed to AI data-center hubs in Texas and Pennsylvania, reportedly structured with US and Japanese government participation. That sits within a combined construction backlog of roughly 130 GW across the merged company.

Why is power the real bottleneck for AI, not GPUs?

GPU clusters can be installed in months; multi-gigawatt power and transmission take years and clear multiple regulatory cycles. US electric companies will spend over $1.1 trillion on the grid in five years (Edison Electric Institute) as data-center demand grows ~20% per year toward 170–220 GW by 2030. Whoever controls the build pipeline controls how fast AI capacity comes online.

Is this related to the GridCARE and Anthropic power stories?

Yes — it is the same structural force at a larger scale. GridCARE raised $64 million to unlock latent grid capacity for AI, and Anthropic committed to a 10-gigawatt compute empire. NextEra-Dominion consolidates the supply side of that same power-for-AI market into a single counterparty.

What premium did NextEra pay for Dominion?

The all-stock offer represents roughly a 23% premium over Dominion's $54.3 billion market capitalization as of May 15, 2026. NextEra shareholders will own approximately 74.5% of the combined company.

When will the NextEra-Dominion deal close?

Subject to shareholder approval and regulatory clearance — federal authorities plus state public utility commissions in Virginia and Florida — the companies expect the transaction to close within roughly 12 to 18 months, targeting 2027.

Which regions get the AI power commitments?

Texas (ERCOT) and Pennsylvania (within the PJM footprint) — the two US regions where AI load growth is colliding hardest with grid limits. Dominion separately powers northern Virginia, the world's largest existing data-center market.

What does the combined company lead in?

Per the merger materials, the combined company is positioned as the world leader in renewables and battery storage, the US leader in natural gas generation, and the number-two player in nuclear power — the exact energy mix an AI buildout needs for cheap, firm, and dispatchable supply.

What is the biggest risk to the deal's thesis?

The regulatory path. A 12-to-18-month close gated by federal and multiple state commissions runs into an active debate over whether data-center load should socialize grid costs onto ordinary ratepayers. The AI-power logic is sound; whether it converts to delivered gigawatts on AI's timeline depends on regulatory approval and the ratepayer cost question.

What should AI companies like OpenAI and Anthropic watch?

Power-counterparty concentration. With one company holding ~130 GW of backlog and the dominant renewables, gas, and nuclear positions, frontier labs and hyperscalers gain a single capable supplier able to commit 10 GW — but lose procurement leverage exactly as demand goes vertical. The firms that secure firm power contracts earliest gain a durable AI capacity advantage.