GridCARE raised a $64 million oversubscribed Series A on May 14 2026, led by Sutter Hill Ventures with John Doerr and National Grid Partners participating. Its Energize platform uses physics-based AI to find unused capacity inside existing power grids and convert it into deliverable power for AI factories — compressing interconnection timelines from years to months. The company calls the category "Power Acceleration," and it sits exactly where the two hottest constraints in AI infrastructure now collide: compute is abundant, power is the bottleneck.

The Big Picture: Power Became the Real AI Bottleneck

For most of the AI buildout, the scarce resource was silicon. The story of the last 18 months — Nvidia allocation, Cerebras wafers, custom inference chips — was a story about chips. That story is changing. The constraint has moved upstream, from the rack to the substation. GridCARE's $64 million Series A is one of the cleanest market signals yet that capital now believes power delivery, not compute availability, is the gating factor on AI expansion.

The thesis is blunt: there is more usable capacity already sitting inside the grid than anyone is scheduling, and the bottleneck is not generation — it is the multi-year queue between when a data center needs power and when a utility can formally deliver it. GridCARE's pitch is that this gap is a software problem disguised as an infrastructure problem.

We have been tracking the compute-financing arms race closely — from Nvidia's $40B equity bets and circular financing to Anthropic's Colossus 1 compute deal with SpaceX. GridCARE is the same arms race viewed from the other end of the cable: not who owns the chips, but who can energize the building they sit in.

What "Power Acceleration" Actually Means

GridCARE is explicitly trying to name a new category — "Power Acceleration for AI" — the way "observability" or "FinOps" got named into existence. The framing matters because it reframes the grid from a fixed pipe into a schedulable resource. The claim is not "build more power plants." It is "the watts already exist; the scheduling, congestion modeling, and interconnection logic is what's broken."

What Happened: The $64M Round in Detail

GridCARE announced on May 14 2026 that it closed a $64 million Series A, described as oversubscribed. The round was led by Sutter Hill Ventures, with venture capitalist John Doerr participating directly. Strategic and institutional backers include National Grid Partners (the corporate venture arm of utility National Grid), Future Energy Ventures, Emerson Collective, and Stanford University. Existing investors Xora, Aina Ventures, Overture, Acclimate Ventures, and Clearvision Ventures also returned.

The investor list is the most revealing part of the round. A utility venture arm (National Grid Partners) co-investing alongside a classic Silicon Valley firm (Sutter Hill) and a marquee venture name (Doerr) tells you the bet spans both sides of the power-meter — the people who own the grid and the people who want to draw from it are funding the same intermediary.

Read the syndicate more carefully and the strategic logic sharpens. Future Energy Ventures and Clearvision Ventures are energy-transition specialists; they underwrite the grid-physics credibility. Emerson Collective and John Doerr bring climate-and-scale capital that has historically chased structural infrastructure shifts. Sutter Hill is a deep-technology lead with a long enterprise-software track record. The mix is not a generic growth round — it is a deliberate pairing of energy-domain validators with software-scaling investors, which is exactly the cap table you assemble when the company has to be credible to a utility engineer and a hyperscaler procurement team in the same meeting.

The oversubscription detail matters too. An oversubscribed Series A inside twelve months of a prior raise signals demand exceeded the round size at the price the company set — investors competed in, the company did not have to chase capital. In a category the founders are still actively naming, that is an unusually strong demand signal.

Who Is Behind GridCARE

GridCARE is led by co-founder and CEO Amit Narayan, with co-founder and CTO Ram Rajagopal, a Stanford professor currently on leave to build the company. The Stanford lineage is not cosmetic — the core of the product is a physics-based grid model, the kind of work that comes out of power-systems research labs rather than a generic data startup. Stanford University itself appears on the cap table, which is unusual and reinforces the research-origin signal.

The Valuation Step-Up Signal

The round is reported as a significant step-up in valuation versus the company's prior financing, which closed less than a year earlier. We are deliberately scoping the exact multiple as "reported" rather than stating a precise figure — the lead source (HPCwire) returned a 403 on direct retrieval, and the official Business Wire release confirms the $64M, the oversubscription, and the investor syndicate but does not publish a hard valuation number. What is confirmable: an oversubscribed Series A with a step-up inside 12 months, in a category the company is actively trying to define. That pattern, on its own, is the signal.

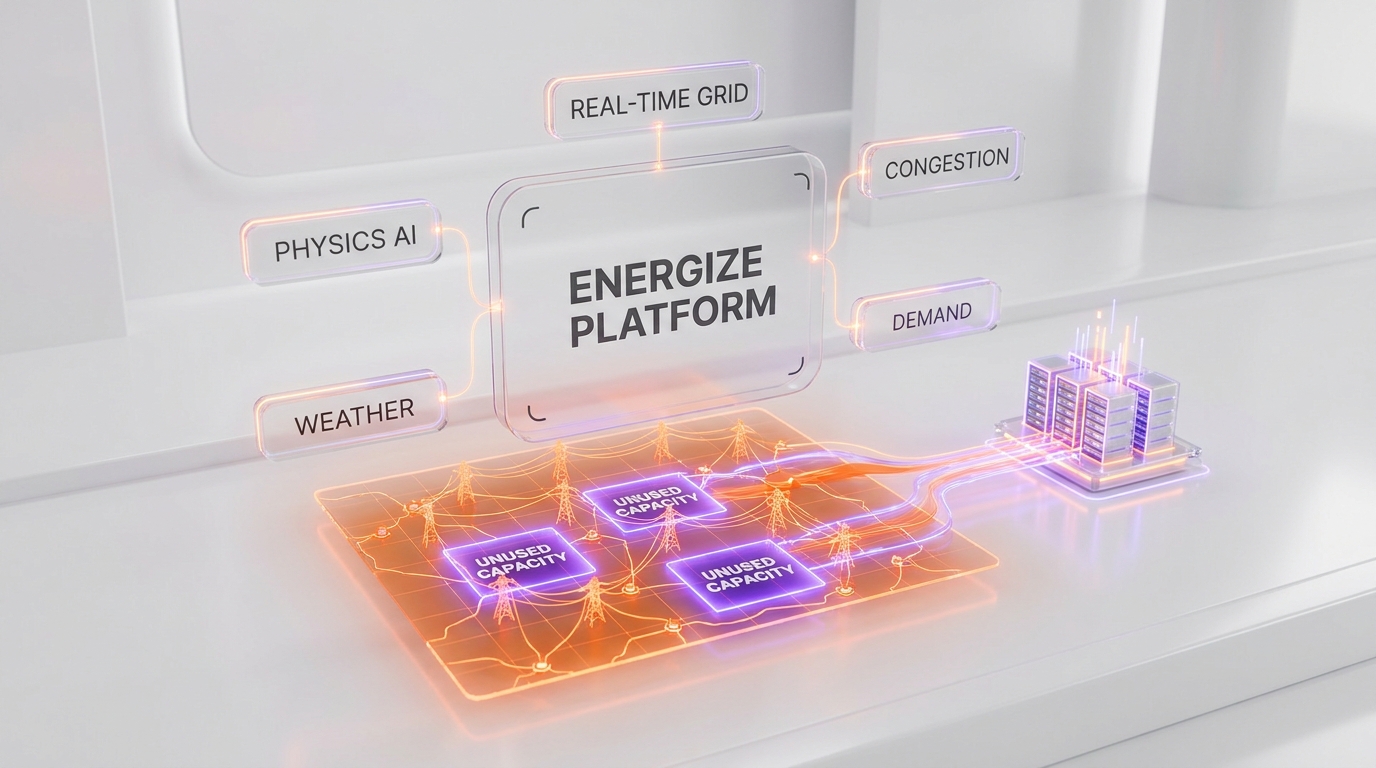

The Energize Platform: How It Works

Energize is the product. It is a physics-based AI system that evaluates grid conditions in real time — congestion, outages, weather conditions, and fluctuations in demand — and then identifies where unused or underutilized capacity already exists in the existing transmission and distribution infrastructure. The output is actionable: where a utility can safely route additional load without triggering a multi-year upgrade.

The key word is physics-based. This is not a demand-forecasting dashboard. The model represents the electrical behavior of the grid — power flow, thermal limits, contingency constraints — so its capacity findings can survive a utility engineer's review rather than just being a statistical guess. That distinction is what lets a utility act on it.

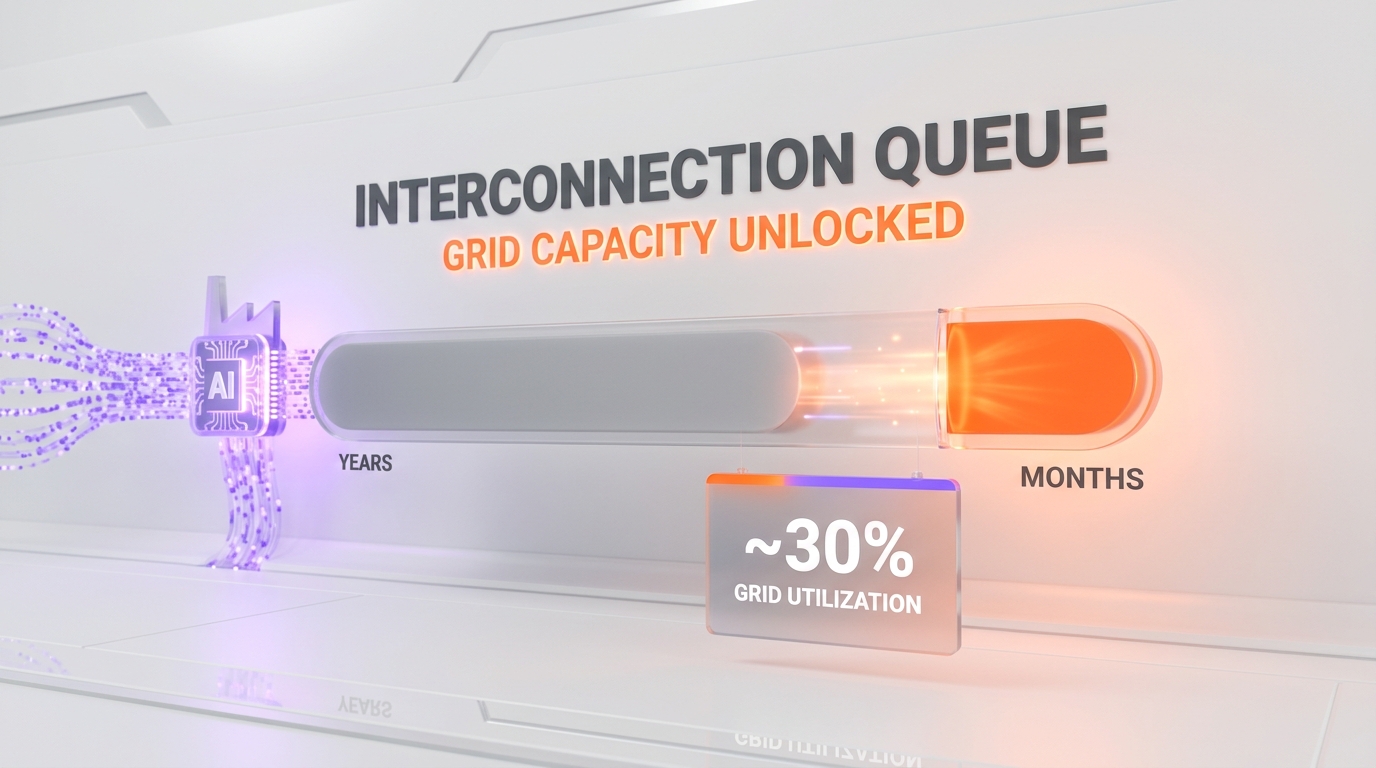

Why "Underutilized Capacity" Is Real, Not Marketing

Grids are engineered for peak conditions that occur a few hours a year. The average utilization across most transmission infrastructure sits around 30 percent. The gap between average load and engineered capacity is enormous — and most of it is invisible to the interconnection process, which is conservative by design. GridCARE's argument is that a physics-aware model can locate the safely-usable slack that static planning processes leave on the table.

From Years to Months

The headline operational claim is timeline compression. Conventional interconnection for a large data center load runs multiple years — queue position, system impact studies, network upgrades. GridCARE positions Energize as a way to find capacity that does not require those upgrades, shrinking the path to energization from years to months. That is the entire commercial value proposition: time-to-power is the scarcest currency in AI infrastructure right now.

The Portland General Electric Proof Point

The round comes with a concrete deployment, not just a thesis. GridCARE is working with Portland General Electric in Hillsboro, Oregon, on a plan to unlock as much as 400 megawatts of excess grid capacity, with an initial tranche on the order of 80 megawatts expected to come online in 2026 and the full envelope targeted by 2029. Hillsboro is a meaningful location: it is one of the densest data center corridors on the US West Coast.

A 400 MW unlock in a single metro is not incremental. For scale: that is roughly the power envelope of a large frontier-scale training cluster. The fact that a regulated utility is willing to co-design this with a startup — and that National Grid's venture arm is on the cap table — is the strongest validation in the round. Utilities do not move fast or take reputational risk lightly.

The Broader Pipeline

Beyond Portland General Electric, GridCARE reports a pipeline on the order of 2+ gigawatts across more than a dozen markets. We treat the pipeline figure as company-reported forward guidance rather than contracted capacity — pipeline is not signed megawatts. But even discounted heavily, a multi-gigawatt funnel across many utilities indicates the demand side of this market is not the constraint. The constraint is execution and regulatory trust, which is exactly what the utility-heavy investor syndicate is designed to de-risk.

Why It Matters: Power for AI Is Now a Market

The strategic read here is that "time-to-power" has become a tradeable, fundable category. Two years ago, the AI infrastructure conversation was almost entirely about GPUs. Today the binding constraint for a new AI factory is the substation, the interconnection queue, and the transmission upgrade — not the order book at Nvidia.

This is the same structural story we have written about from the compute angle. Anthropic's stated 10-gigawatt compute empire is, restated honestly, a 10-gigawatt power commitment. Every gigawatt of frontier compute is a gigawatt that has to be interconnected, energized, and cooled. GridCARE is monetizing the gap between "we ordered the chips" and "the building has power."

The Convergence Thesis

Two themes that were separate are now the same theme. Theme one: the AI compute buildout — chips, clusters, capex. Theme two: the power and grid constraint — interconnection queues, transmission, generation. GridCARE sits precisely on the seam. Its entire value is that it converts an energy-sector problem into an AI-infrastructure deliverable. The $64M Series A is the market pricing that seam.

How It Compares: The Power-for-AI Landscape

GridCARE is not alone in noticing that power gates AI, but its angle is distinct. Most approaches attack the supply side: behind-the-meter generation, on-site gas, nuclear SMRs, dedicated solar-plus-storage. Those add new electrons. GridCARE attacks the scheduling and discovery side: it does not add electrons, it finds the ones the grid already has and is not using. That is a software margin profile layered on top of physical infrastructure — structurally more attractive than building power plants.

The closest conceptual neighbors are interconnection-acceleration and grid-intelligence startups, plus the utility planning incumbents. GridCARE's differentiation is the physics-based model paired with utility co-investment, which is what gives its findings regulatory credibility. The competitor it most has to beat is not another startup — it is the status quo interconnection process and the utilities' own internal planning teams.

Where Compute Infrastructure Connects

For builders renting AI compute today, the practical relevance is indirect but real: capacity-constrained regions mean higher prices and longer waits for GPU access. Inference providers like Cerebras Inference and GPU clouds like RunPod are downstream of exactly the constraint GridCARE targets — every datacenter they run in had to be energized first. We covered the public-market read on this constraint in our piece on Cerebras pricing its IPO above range; the same scarcity logic that supports inference-chip valuations supports power-acceleration valuations.

The deeper point is that the entire AI compute stack now has an implicit power dependency priced into it. When a frontier lab signs a multi-gigawatt compute commitment, the unstated assumption is that the matching power gets interconnected on a compatible timeline. Historically that assumption has been the weak link — clusters have been built and then sat partially dark waiting on grid upgrades. A company that can credibly shorten the energization path is, in effect, de-risking the timeline of every large AI infrastructure commitment downstream of it. That is why a power-discovery layer can command a venture valuation that looks rich for an energy-sector company but reasonable for an AI-infrastructure enabler.

The Risks We See

This is a strategic analysis, so the honest counter-case matters. First: regulatory dependency. GridCARE's value only materializes when a regulated utility acts on its findings. That is a slow, jurisdiction-by-jurisdiction sales motion, and utilities are structurally cautious. The Portland General Electric relationship is strong validation, but one lighthouse customer is not a repeatable enterprise motion yet.

Second: the capacity it finds is real but finite. Physics-based slack discovery has a ceiling — once the underused headroom in a region is allocated, the model has converted a one-time inventory, not created a renewable stream. The durable business has to be the recurring optimization layer, not the initial unlock.

Third: incumbents can copy the method. Nothing stops a large utility or a grid-software incumbent from building a competing physics model. GridCARE's moat is speed, the utility relationships, and the category-naming lead — defensible but not impregnable.

What Would Prove the Thesis Right

The cleanest validation milestone is the Portland General Electric 80 MW tranche actually coming online in 2026 as described. If that capacity energizes on the stated timeline, the "years to months" claim moves from pitch to track record, and the multi-gigawatt pipeline becomes credible. The GridCARE Power Acceleration Summit, scheduled for September 2026, is the company's own forcing function to show that progress publicly.

Our Take

We read this round as one of the most strategically well-positioned bets in AI infrastructure right now, and the reason is the seam. The hardest place to build a durable company is at the intersection of two industries that do not speak the same language — and that is exactly where GridCARE sits, between the AI buildout and the regulated power grid. The investor syndicate is the tell: when a utility venture arm, a classic Sand Hill firm, and John Doerr are all in the same oversubscribed Series A, the market is pricing a structural shift, not a feature.

The honest caveat: software-margin framing on top of regulated infrastructure is always slower in practice than in the pitch. Utilities move on utility time. But the directional call is right. Time-to-power is the scarcest currency in AI for the next several years, and naming the category early — "Power Acceleration" — is itself a strategic move that compounds.

What's Next

Three things to watch. First, the Portland General Electric 80 MW tranche in 2026 — that is the proof point that converts the thesis into a reference. Second, the GridCARE Power Acceleration Summit in September 2026, which will indicate how many utilities and AI operators are actually moving from interest to deployment. Third, the next round: an oversubscribed Series A with a sub-12-month step-up usually means a fast Series B follows if the deployment data lands. We will track all three.

For everyone building on AI infrastructure, the takeaway is simpler than the cap table: the question is no longer only "can I get the chips." It is increasingly "can the building get the power, and how fast." GridCARE just raised $64 million on the bet that the answer is a software answer.

Frequently Asked Questions

How much did GridCARE raise in its Series A?

GridCARE raised a $64 million oversubscribed Series A, announced May 14 2026. The round was led by Sutter Hill Ventures with venture capitalist John Doerr participating, alongside National Grid Partners, Future Energy Ventures, Emerson Collective, and Stanford University, plus returning investors Xora, Aina Ventures, Overture, Acclimate Ventures, and Clearvision Ventures.

What is the GridCARE Energize platform?

Energize is GridCARE's product: a physics-based AI system that evaluates grid conditions in real time — congestion, outages, weather, and demand fluctuations — to identify unused or underutilized capacity already present in existing transmission and distribution infrastructure. The output tells utilities and data center developers where additional load can be safely added without triggering a multi-year grid upgrade.

Who founded GridCARE and who runs it?

GridCARE is led by co-founder and CEO Amit Narayan, with co-founder and CTO Ram Rajagopal, a Stanford professor on leave to build the company. Stanford University also appears on the cap table, reinforcing the company's power-systems research origin.

What is the Portland General Electric project?

GridCARE is working with Portland General Electric in Hillsboro, Oregon, to unlock as much as 400 megawatts of excess grid capacity. An initial tranche of roughly 80 megawatts is expected to come online in 2026, with the full envelope targeted by 2029. Hillsboro is one of the densest data center corridors on the US West Coast.

Why is power the bottleneck for AI instead of compute?

The scarce resource has moved upstream from the chip to the substation. New AI factories and hyperscale data centers can wait multiple years for grid interconnection — queue position, system impact studies, and network upgrades — even when chips are available. GridCARE's bet is that more usable capacity already exists in the grid than is being scheduled, and the bottleneck is interconnection logic, not generation.

What does "Power Acceleration" mean?

"Power Acceleration for AI" is the category GridCARE is explicitly trying to name. It reframes the grid from a fixed pipe into a schedulable resource: rather than building new generation, the approach locates the safely-usable slack the grid already has and routes AI load to it, compressing time-to-power from years to months.

How is GridCARE different from building new power generation?

Most power-for-AI approaches attack the supply side — behind-the-meter gas, nuclear SMRs, dedicated solar-plus-storage — which adds new electrons. GridCARE attacks the scheduling and discovery side: it does not add electrons, it finds the ones the grid already has and is not using. That gives it a software-margin profile layered on physical infrastructure rather than a power-plant cost structure.

What is the GridCARE pipeline beyond Portland General Electric?

GridCARE reports a pipeline on the order of 2+ gigawatts across more than a dozen markets. This is company-reported forward guidance rather than contracted capacity, so it should be treated as funnel rather than signed megawatts — but it indicates the demand side of the market is not the constraint.

What are the risks to GridCARE's thesis?

Three main risks: regulatory dependency, since value only materializes when a cautious regulated utility acts on the findings; finite slack, since discovered headroom is a one-time inventory in any region until the recurring optimization layer proves durable; and copyability, since large utilities or grid-software incumbents could build competing physics models. GridCARE's moat is speed, utility relationships, and the category-naming lead.

Why does GridCARE matter for AI developers and builders?

It is indirect but real. Capacity-constrained regions mean higher prices and longer waits for GPU access from inference providers and GPU clouds, because every datacenter they run in had to be energized first. If GridCARE compresses time-to-power, it loosens the upstream constraint that ultimately prices AI compute access.

What is the GridCARE Power Acceleration Summit?

GridCARE announced plans to host its inaugural GridCARE Power Acceleration Summit in September 2026, convening leaders from the AI and energy sectors around accelerating grid capacity and AI infrastructure deployment. It functions as the company's own public forcing function to demonstrate deployment progress.

What would prove GridCARE's thesis right?

The cleanest validation is the Portland General Electric 80 megawatt tranche actually coming online in 2026 as described. If that capacity energizes on the stated timeline, the "years to months" claim moves from pitch to track record, and the multi-gigawatt pipeline becomes materially more credible.

Sources: GridCARE official announcement (Business Wire, May 14 2026) · HPCwire. Funding amount, oversubscription, investor syndicate, Energize platform description, Portland General Electric figures and the September 2026 summit are confirmed via the official release; the precise valuation step-up multiple is reported and scoped accordingly.