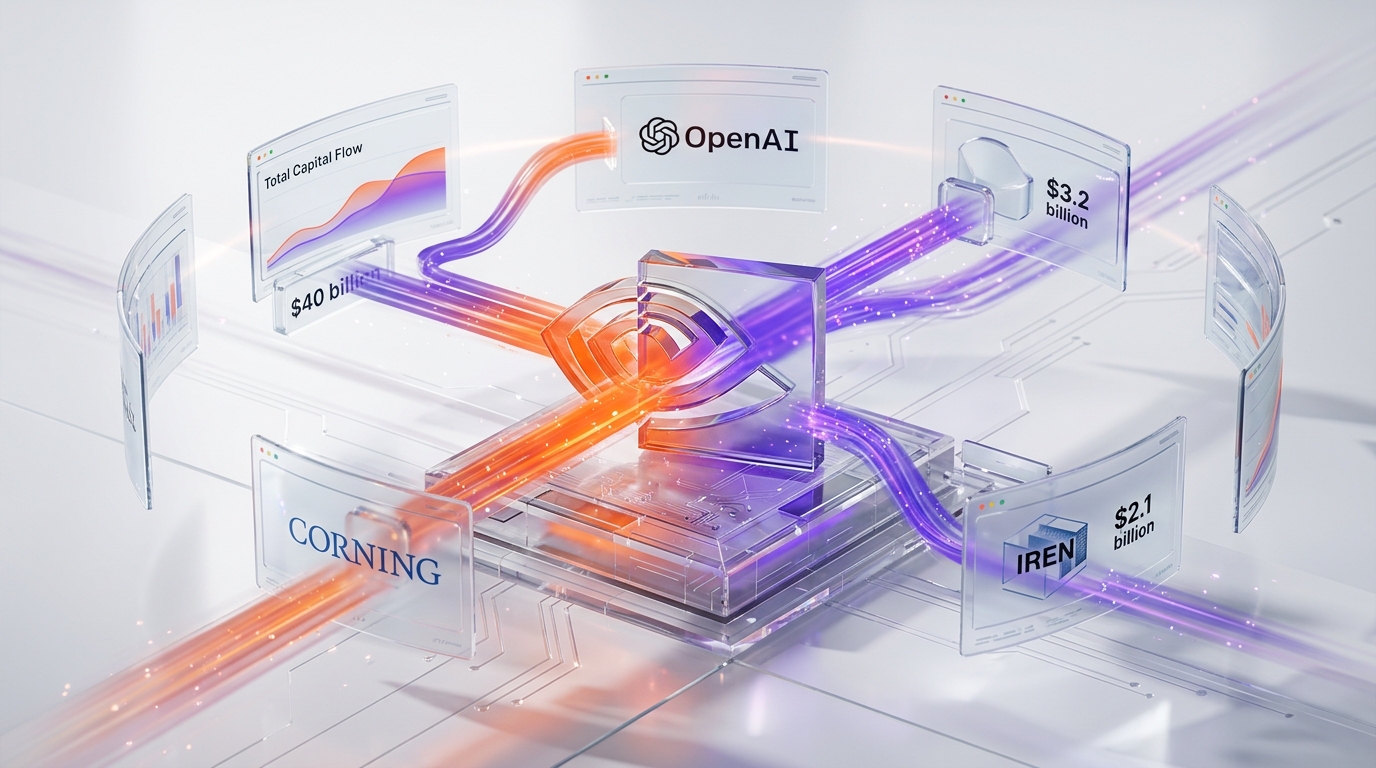

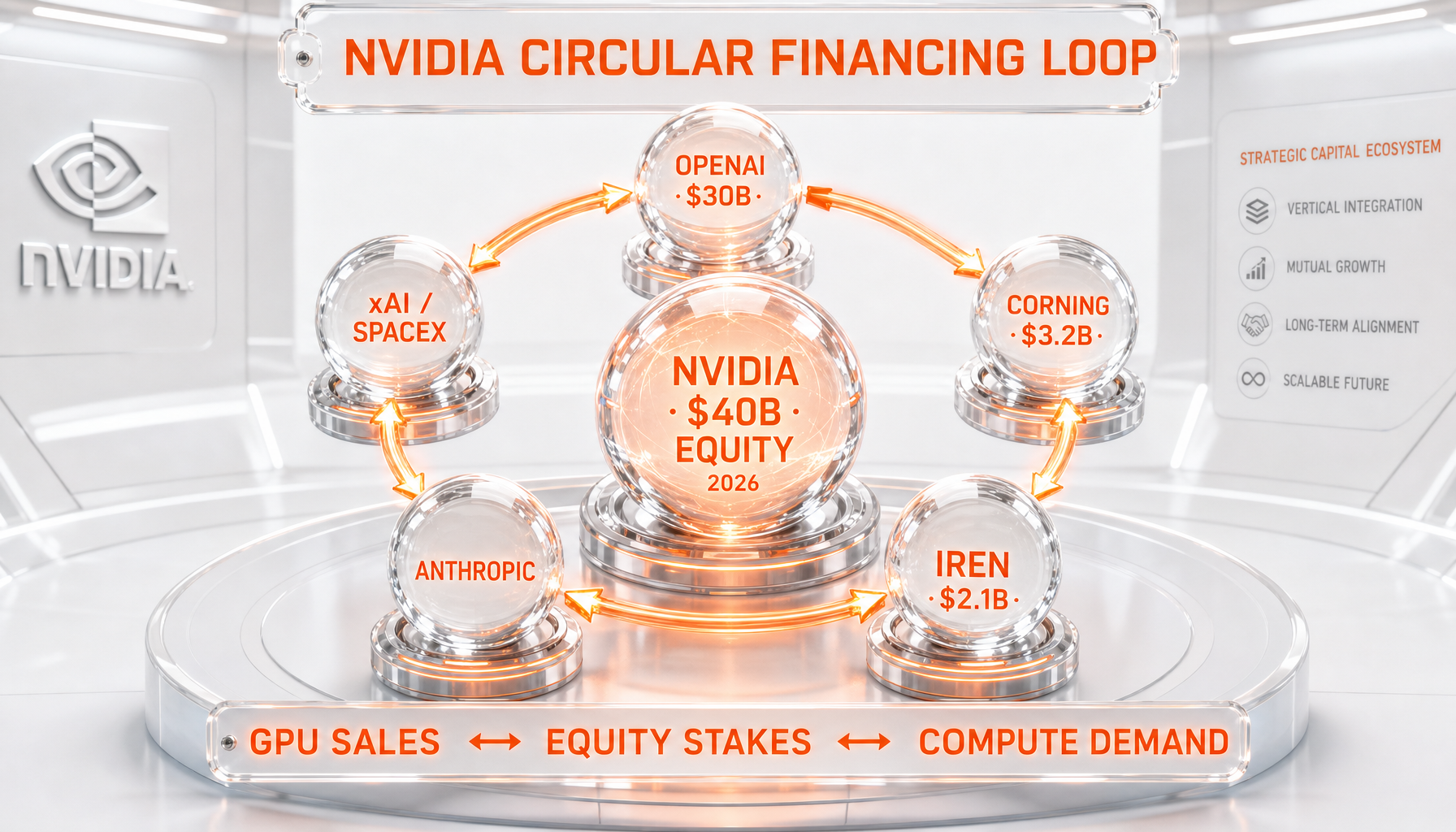

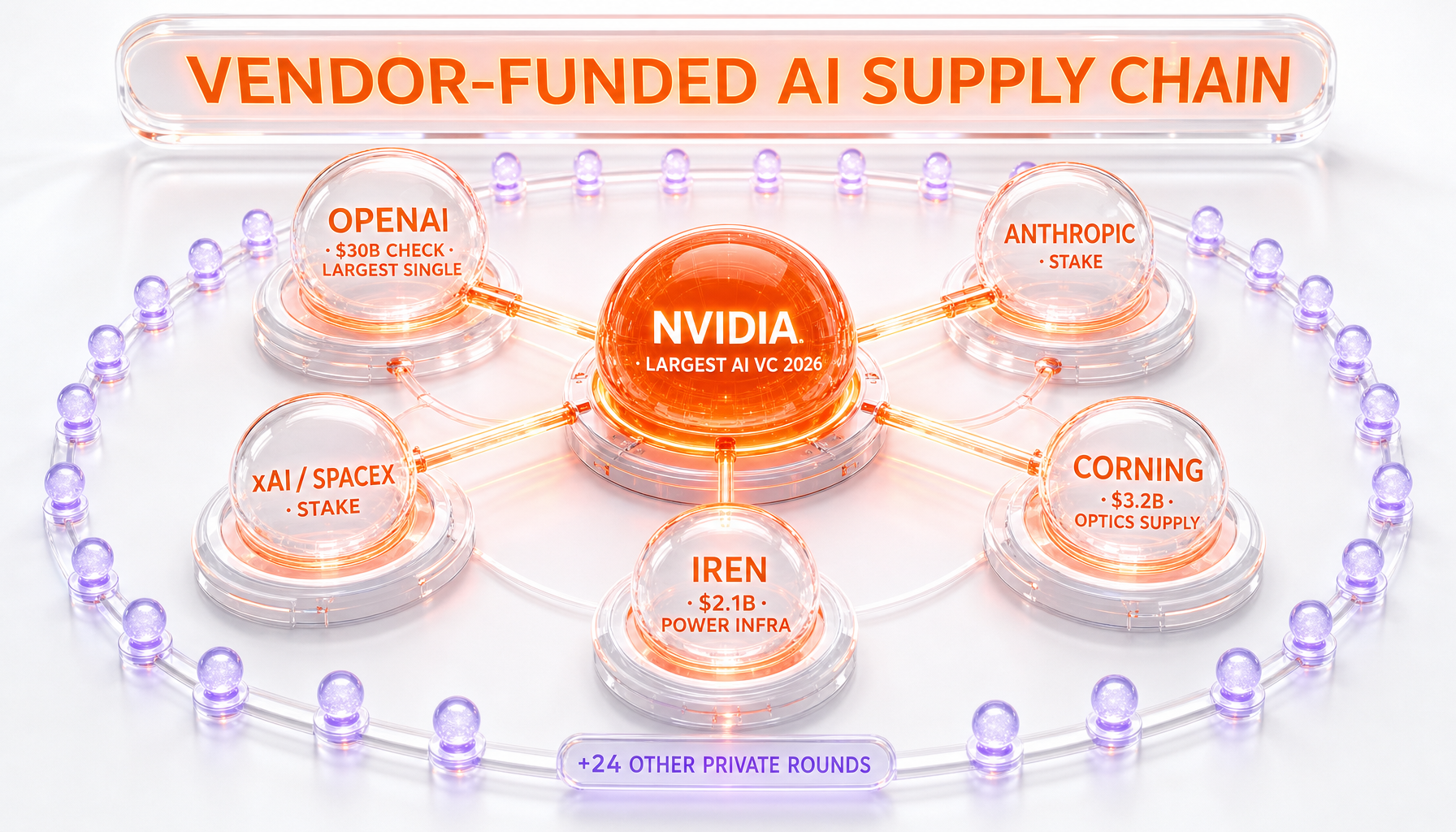

NVIDIA committed more than $40 billion in equity deals year-to-date 2026 — a total that dwarfs every dollar it deployed in 2025, and one that quietly makes Jensen Huang the largest AI venture investor on Earth. The single largest check, reported by CNBC and TechCrunch on May 9 2026, was $30 billion into OpenAI. Then $3.2 billion into glassmaker Corning, $2.1 billion into data center operator IREN, plus roughly two dozen private rounds and previously disclosed stakes in Anthropic and the xAI-SpaceX orbit. NVIDIA does not just sell GPUs anymore. It funds the companies buying them.

We have been tracking NVIDIA's investment pace since the Vera Rubin trillion-dollar order book leaked at GTC in March, and the slope of capital flow is unprecedented. Wedbush Securities analyst Matthew Bryson put it bluntly in the TechCrunch piece: these deals sit "squarely into the circular investment theme." Bryson hedged that the strategy could build "a competitive moat" if it works. Critics frame it differently — they argue Jensen is financing his own demand curve.

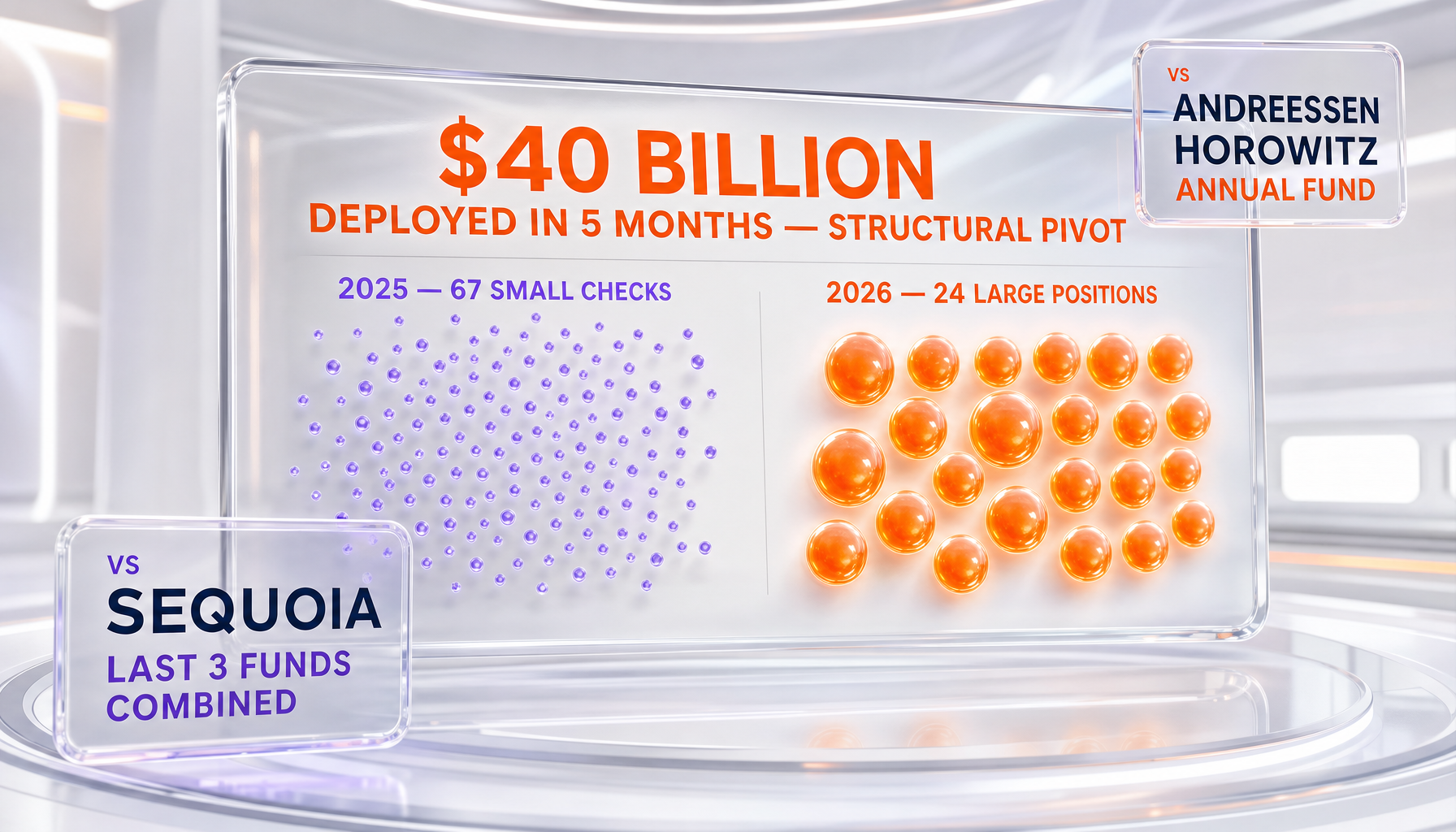

The $40 billion number in context

Forty billion dollars deployed in roughly five months is not a normal venture pace. It is bigger than the entire annual fund of Andreessen Horowitz. It is larger than Sequoia's last three funds combined. It is more equity capital than Microsoft's M12, Google Ventures, and Salesforce Ventures will deploy in 2026 stacked together.

And it represents a structural pivot. In 2025, NVIDIA participated in 67 venture deals — most of them smaller checks alongside traditional VCs. In the first five months of 2026, the company has roughly halved the number of private rounds (about 24 according to TechCrunch) while multiplying the average check size by orders of magnitude. The shape changed: fewer bets, much larger positions, much closer to NVIDIA's own commercial surface area.

This is not a corporate venture arm anymore. It is a sovereign-scale capital allocator inside a publicly traded chip company.

Where the money went

The disclosed allocation breaks down across four clear layers.

- $30 billion to OpenAI — the headline deal. The single largest equity commitment NVIDIA has ever made, and roughly three quarters of the total YTD figure.

- $3.2 billion to Corning — the New York glassmaker that supplies optical components for hyperscale data center networking. NVIDIA needs Corning to scale rack-level fiber faster than the market currently produces it.

- $2.1 billion to IREN — the Australian-listed data center operator that has been retrofitting former bitcoin mining sites into GPU-dense AI compute campuses.

- ~24 private rounds and existing stakes — including disclosed positions in Anthropic and the xAI-SpaceX compute pipeline that we covered in our Anthropic-SpaceX Colossus 1 analysis.

What we read in this pattern: NVIDIA is no longer betting on AI as a category. It is buying control over the specific bottleneck inputs — frontier model training capacity, optical interconnect supply, and physical data center floor space — that determine whether Jensen's GPU shipments actually translate into deployed revenue or sit on factory loading docks.

The OpenAI $30 billion anchor

The OpenAI position is the keystone. CNBC reported the structure as an equity commitment tied to compute infrastructure buildout, not a simple cash injection. The mechanism reportedly involves NVIDIA taking equity in exchange for guaranteed GPU allocation at scale — a structure that turns Jensen into both vendor and stakeholder simultaneously.

Compare this to the Microsoft–OpenAI relationship. Microsoft invested roughly $13 billion in OpenAI over multiple tranches, and in exchange got exclusive Azure compute hosting rights plus deep IP integration. Microsoft was buying a partnership. NVIDIA is buying something different: protection against the day OpenAI tries to build its own chip stack.

OpenAI has telegraphed for months that it wants to reduce dependence on NVIDIA silicon — through internal chip projects, Broadcom partnerships, and now its Stargate compute build. A $30 billion equity check is the strongest possible structural hedge against that. It does not stop OpenAI from designing custom silicon. It just makes sure that if OpenAI succeeds at it, NVIDIA still wins on the upside.

Circular financing — the narrative

The phrase "circular financing" started appearing in analyst notes during Q1 2026 and accelerated after the Corning and IREN announcements. The critique runs like this:

- NVIDIA invests equity in OpenAI.

- OpenAI uses that capital (and adjacent fundraising) to buy NVIDIA GPUs.

- The GPU revenue flows back to NVIDIA's top line.

- Wall Street rewards NVIDIA's top-line growth with a higher multiple.

- Higher market cap funds the next round of equity bets.

In its softest form, this is just vertical integration — every supply chain has flywheels, and Jensen is building one in plain sight. In its sharpest form, the critique is that NVIDIA is artificially inflating end-customer demand because the end customers are partially funded by NVIDIA itself.

Wedbush's Bryson did not endorse the harsh framing. He called it "circular investment theme" — a structural description — and added that if executed well it builds "a competitive moat." We read his framing as the consensus sell-side view: structurally interesting, not yet structurally alarming.

Historical parallels — what does this actually rhyme with?

Three historical comparisons keep surfacing in the analyst chatter.

Microsoft funding OpenAI (2019–present). Microsoft invested billions in OpenAI partly through Azure compute credits — capital that flowed right back to Microsoft as cloud revenue. The structure has been criticized for the same circular logic. The defense: Microsoft genuinely needed OpenAI's models to ship Copilot products, so the "circular" loop produced real downstream revenue outside the loop itself. NVIDIA's bet on OpenAI is structurally similar but larger by a factor of two-plus.

AOL–Time Warner (2000). The doom-side comparison. AOL used inflated equity to absorb Time Warner at the peak of the dot-com bubble. The deal made sense only if AOL's market cap reflected real future cash flows. It did not. We do not think this parallel actually applies to NVIDIA's situation — Jensen's GPU revenue is cash, not promise — but it is the analogy critics reach for when they want to argue valuation reflexivity.

Vendor financing during the 1999 telecom bubble. Lucent, Nortel, and Cisco extended billions in vendor financing to telecom carriers buying their equipment. When the carriers went bankrupt, the vendor financiers swallowed enormous write-downs. This is the parallel that actually keeps us awake. If any of NVIDIA's anchor equity positions impair, the writedown would dent earnings precisely when the GPU cycle is most expected to keep growing.

We covered the AI capital markets dynamics in our Q1 2026 VC funding analysis — that piece showed $300 billion of frontier AI concentration is sitting on top of an extremely narrow set of customer counterparties.

The supply chain bottleneck strategy

Read narrowly, the Corning and IREN positions are not financial bets. They are physical bets on whether NVIDIA can actually ship the GPUs already on order.

Corning's $3.2 billion equity stake makes sense only if you understand the optical interconnect bottleneck. NVIDIA's NVLink and InfiniBand fabrics depend on specialized fiber and connector products that Corning produces. The lead times in 2025 were already stretching into multi-quarter territory. Equity ownership accelerates Corning's capex prioritization toward NVIDIA's roadmap, not Cisco's or Broadcom's.

IREN's $2.1 billion check buys something even more physical: floor space and power capacity. Hyperscalers (Microsoft, Google, Amazon) are buying every megawatt of available GPU-ready data center power on the planet. Anthropic locked in 10 gigawatts of multi-cloud capacity — we broke that down in our Anthropic 10 GW empire analysis. The Akamai 7-year deal we covered in our Akamai compute analysis reinforces the same pattern: the constraint is no longer chips, it is power and floor.

NVIDIA buying IREN equity is Jensen ensuring that when the Vera Rubin orders we covered in our Vera Rubin GTC analysis actually ship, the customers have somewhere to plug them in.

Comparison to other AI mega-deals in 2026

NVIDIA's $40 billion does not exist in isolation. The first half of 2026 has been a parade of structurally massive AI infrastructure bets.

- Google's $40 billion Anthropic investment at a $350 billion pre-IPO valuation — covered in our Google Anthropic analysis. Same order of magnitude as NVIDIA's total YTD, but concentrated in a single model lab.

- Bezos's $10 billion Project Prometheus physical-world AI lab — covered in our Prometheus analysis. Different vector (world models, not LLMs), same scale of personal capital deployment.

- Vera Rubin order book at GTC March 2026 — over a trillion dollars of forward GPU demand — covered in our Vera Rubin analysis.

Stacked together, the picture is unambiguous: the AI capital stack is concentrating into the hands of fewer than ten counterparties, and NVIDIA sits at the geometric center of all of them. Jensen is not just one of the players. He is the clearinghouse.

What this means for developers and builders

If you are building on top of frontier AI — whether using Claude, GPT-5, Gemini, or running open-weight models on rented GPUs — NVIDIA's position changes your risk profile in three ways.

Compute pricing power is consolidating. When NVIDIA controls equity stakes in both the model labs (OpenAI, Anthropic) and the physical infrastructure (IREN), the negotiation leverage of independent compute buyers shrinks. Expect rental GPU prices to remain firm.

Stack lock-in deepens silently. Every dollar of equity NVIDIA puts into a customer is a dollar of soft pressure against that customer building CUDA-alternative stacks. AMD, Cerebras, Groq, and the custom silicon programs at OpenAI and Anthropic still ship — but the equity gravity tilts the playing field.

The bottleneck moves up the stack. If you are picking tools today, the question is no longer "which AI lab has the best model" — it is "which AI lab has the best compute access through 2027." We have been writing more about agentic coding stacks like Claude Code for this reason. The lab with the cleanest compute pipeline produces the most reliable developer tooling.

What would prove the circular financing thesis wrong

We try to be intellectually honest about hot narratives. The "circular financing" framing is rhetorically powerful, but it could also be wrong. Here is what would falsify it.

Falsifier 1: OpenAI, Anthropic, and xAI generate enterprise revenue that comfortably services their compute spend without follow-on equity rounds. If the AI labs ship $100 billion of run-rate ARR by year-end 2027, the loop stops being circular — it becomes vertical with real terminal demand at the end.

Falsifier 2: NVIDIA's equity positions appreciate independently of GPU shipment growth. If OpenAI IPOs at a $1 trillion-plus valuation and NVIDIA's stake holds value through a GPU cycle slowdown, that proves the equity bets are genuine financial alpha, not just demand-pull cosmetics.

Falsifier 3: Customers outside NVIDIA's equity orbit also buy at the same scale. Meta, Apple, and Tencent are not (yet) NVIDIA equity beneficiaries. If their GPU buying matches the scale of NVIDIA-funded customers, the circular critique loses force.

We are watching all three signals through year-end 2026. If they hold, Jensen's strategy looks structurally clever. If they break, the writedown risk is bigger than anything currently priced into NVIDIA's multiple.

Regulatory and antitrust questions

The deals also raise antitrust questions. We read this as a watch item, not yet a clear and present danger.

The FTC and EU competition authorities have already been auditing AI compute concentration. A chip vendor taking large equity positions in its largest customers is not, on its own, illegal — corporate venture investment is a normal market practice. But the combination of (a) dominant market share in training silicon, (b) anchor equity positions in the largest training customers, and (c) growing influence over data center buildouts and optical supply, starts to look like vertical foreclosure logic.

The 2026 antitrust environment is more permissive than 2024 was, which gives Jensen room to operate. But the structural concentration is real, and policy is reactive — typically by three to five years.

Our strategic read

We read Jensen's $40 billion deployment as three things stacked.

First, it is real demand insurance. The Vera Rubin order book only matters if customers exist to take delivery. Equity in OpenAI, Corning, and IREN underwrites the demand side of that order book directly.

Second, it is a structural moat against the day OpenAI, Google, and Anthropic finish their custom silicon programs. NVIDIA cannot prevent the transition. It can profit from it on the way down.

Third, it is a Wall Street narrative play. As long as NVIDIA's reported revenue keeps printing, the equity bets feed the loop. The day the loop breaks, the bets become liabilities. We do not know when that day arrives — but it is closer than the consensus assumes.

Jensen is not the AI bubble. He is the load-bearing wall of it. That is a different position. It carries different risks, and it concentrates different rewards. The circular financing critique is gaining traction because it captures a structural truth — the AI capital stack runs through NVIDIA's balance sheet now — even if the worst-case framing is not yet supported by the data.

What to watch through end of 2026

Five signals worth tracking on this story.

- OpenAI's path to IPO or strategic transaction. A $1 trillion-plus exit validates NVIDIA's $30 billion check. Anything less puts pressure on the mark.

- Anthropic's IPO timing. We covered the indicators in our Google Anthropic analysis — an October 2026 IPO at $350 billion pre-money would set the market for the entire frontier lab cohort.

- Vera Rubin shipment cadence. If H2 2026 cadence matches the order book, the equity bets validate. If it slips, capital cycling becomes visible.

- Corning and IREN earnings. These are the two public companies NVIDIA's equity touches. Watch their NVIDIA-attributed revenue line in 10-Qs.

- FTC and EU statements on AI compute concentration. First formal inquiry would mark the regulatory turn.

We will keep tracking this. If you want our daily AI capital markets read, we publish breaking analysis on the ThePlanetTools blog.

Sources

This analysis draws on tier-1 reporting from the following outlets. We cite their work directly so readers can verify every figure independently:

- CNBC — NVIDIA embraces AI investor, topping $40 billion in equity bets (May 9, 2026)

- Bloomberg — NVIDIA's $40B AI Equity Deals (May 9, 2026)

- The Boston Globe — Akamai-Anthropic compute deal context

- Yahoo Finance — Anthropic compute deals context

Frequently asked questions

How much has NVIDIA committed to equity deals in 2026?

NVIDIA has committed more than $40 billion in equity AI deals year-to-date 2026, according to CNBC and TechCrunch reporting on May 9 2026. That total dwarfs the company's full-year 2025 equity deployment.

What is the single largest NVIDIA equity investment?

The single largest disclosed check is $30 billion into OpenAI, structured as an equity commitment tied to compute infrastructure buildout rather than a pure cash injection.

What does "circular financing" mean in the NVIDIA context?

"Circular financing" refers to the critique that NVIDIA is investing equity into customers who then use that capital to buy NVIDIA GPUs — creating a loop where NVIDIA effectively funds its own revenue. Wedbush analyst Matthew Bryson called the pattern "squarely into the circular investment theme" while noting it could build "a competitive moat" if it works.

Why did NVIDIA invest $3.2 billion in Corning?

Corning produces the optical interconnect fiber and connectors that NVIDIA's NVLink and InfiniBand fabrics require at hyperscale. The $3.2 billion equity stake accelerates Corning's capex prioritization toward NVIDIA's product roadmap and helps unblock the optical bottleneck in GPU rack deployments.

Why did NVIDIA invest $2.1 billion in IREN?

IREN operates data center capacity — including former bitcoin mining sites being retrofitted for AI compute. The $2.1 billion stake gives NVIDIA influence over GPU-ready floor space and power allocation at a moment when megawatts are the binding constraint in AI deployment.

How many private startup rounds has NVIDIA participated in during 2026?

Approximately 24 private rounds in the first five months of 2026, compared to 67 venture deals during all of 2025. The number of deals dropped but the average check size grew by orders of magnitude.

Has NVIDIA invested in Anthropic and xAI?

NVIDIA has disclosed stakes in Anthropic and is part of the xAI compute orbit through the SpaceX-Colossus 1 buildout. The CNBC and TechCrunch May 9 2026 pieces did not specify dollar amounts for those positions.

Is NVIDIA's equity strategy similar to Microsoft's OpenAI investment?

Structurally similar but larger. Microsoft invested roughly $13 billion in OpenAI over multiple tranches in exchange for Azure compute exclusivity. NVIDIA's $30 billion commitment is more than twice the size and is structured as a hedge against OpenAI moving away from NVIDIA silicon.

What historical parallels apply to NVIDIA's circular financing pattern?

Three are commonly cited: Microsoft funding OpenAI through Azure credits, the AOL-Time Warner merger at the dot-com peak in 2000, and vendor financing during the 1999 telecom buildout when Lucent, Nortel and Cisco extended capital to carriers buying their equipment. The telecom parallel is the most operationally relevant — if any anchor equity position impairs, the writedown hits at the worst possible moment in the GPU cycle.

What would prove the circular financing thesis wrong?

Three falsifiers: AI labs generating real enterprise revenue that services compute spend without follow-on rounds, NVIDIA's equity positions appreciating independently of GPU shipment growth, and customers outside the equity orbit (Meta, Apple, Tencent) buying GPUs at the same scale as NVIDIA-funded customers. If all three hold through 2027, the loop becomes vertical integration rather than circular cosmetics.

Are there antitrust concerns with NVIDIA's investment pattern?

Regulatory attention is rising but no formal action has been announced. The combination of dominant GPU market share, equity in the largest training customers, and influence over data center and optical supply could attract scrutiny from the FTC and EU competition authorities. The 2026 antitrust environment is more permissive than 2024, but structural concentration is real and policy responses typically lag by three to five years.

What should developers and AI builders watch?

Five signals through end of 2026: OpenAI's path to IPO or strategic exit, Anthropic's IPO timing (potentially October 2026 at $350 billion pre-money), Vera Rubin shipment cadence in H2 2026, Corning and IREN earnings disclosures, and first formal statements from FTC or EU on AI compute concentration. Any one of these moving materially changes the strategic read.