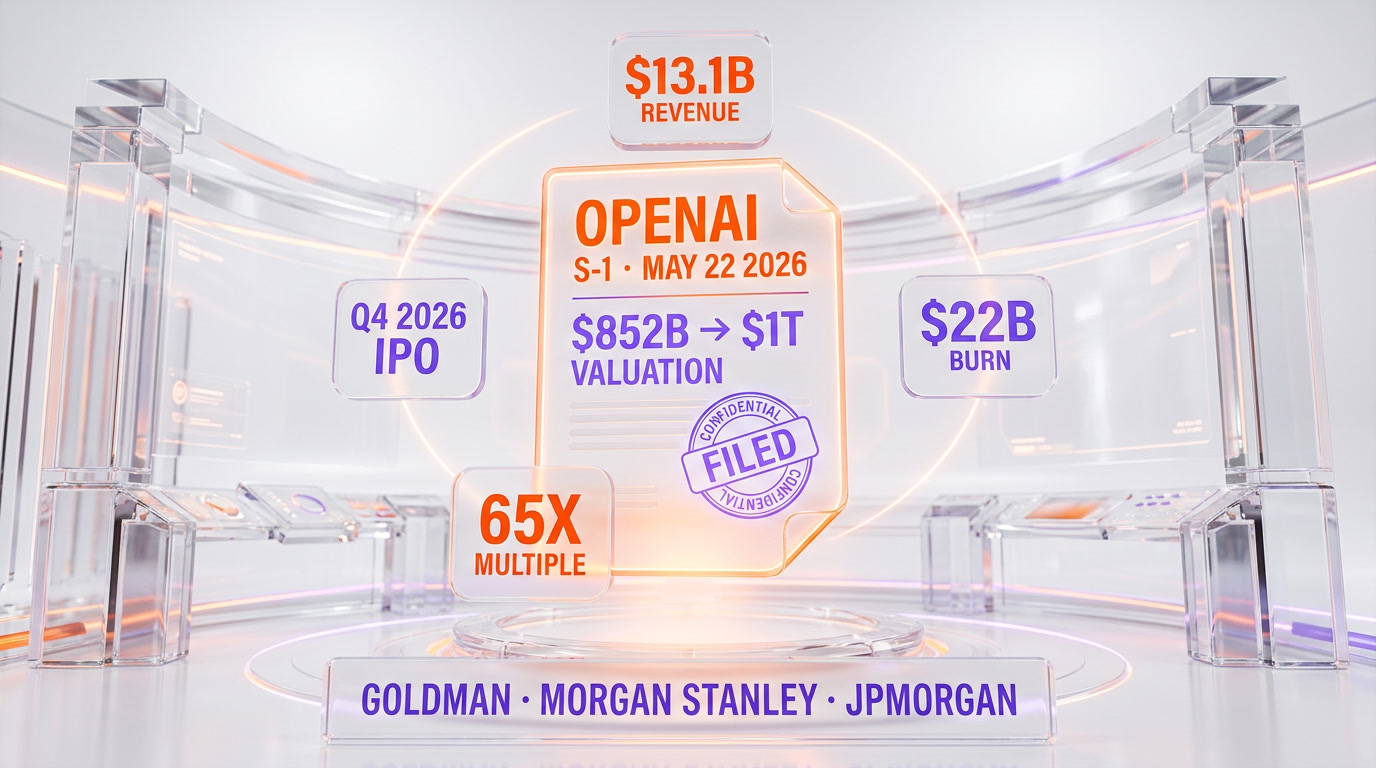

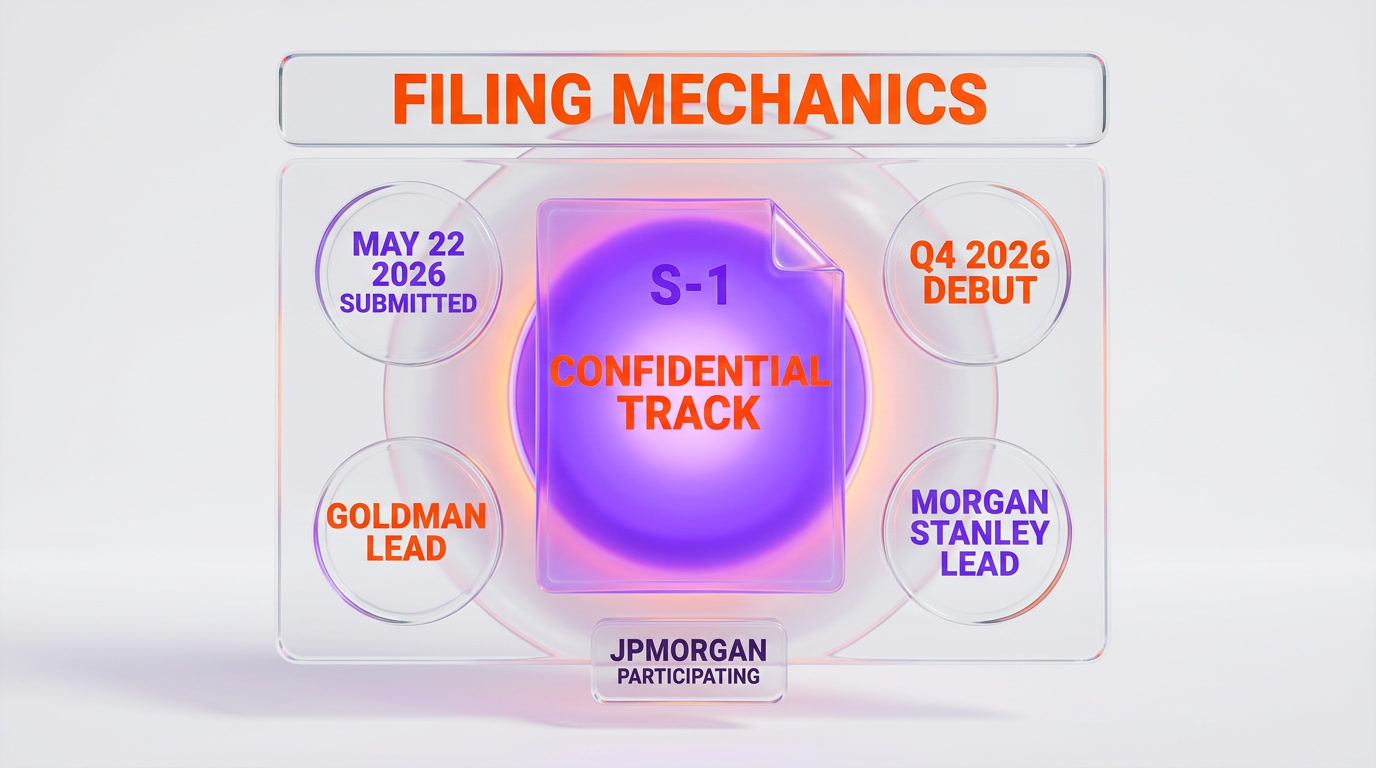

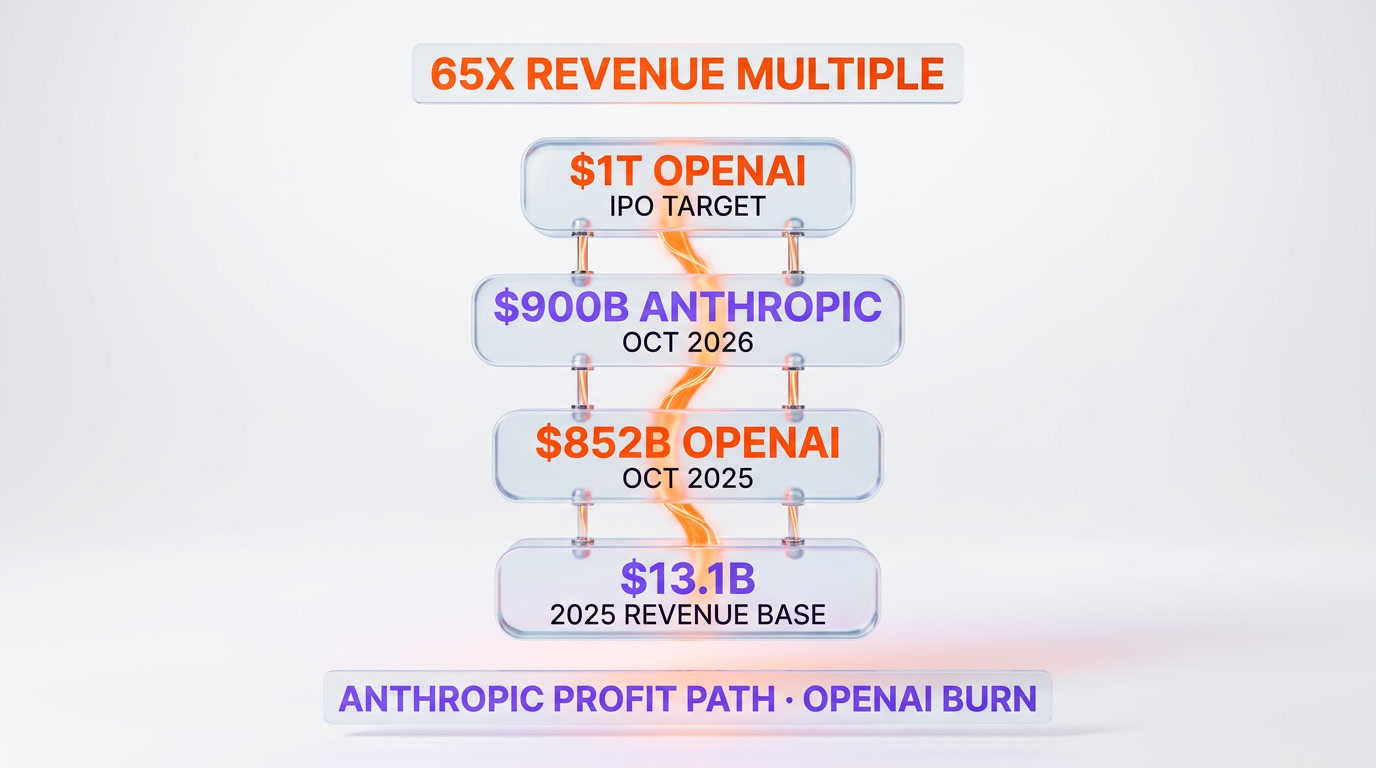

OpenAI confidentially filed its S-1 with the SEC on May 22, 2026, targeting a public debut at $852 billion to $1 trillion valuation in Q4 2026, led by Goldman Sachs and Morgan Stanley with JPMorgan participating. Per reporting from Fortune and Axios, the listing could come as early as September 2026, against a 2025 revenue base of roughly $13.1 billion and a 2025 cash burn estimated at $22 billion. In my reading, the filing answers nothing yet — confidential S-1s stay private until roughly 15 days before the public roadshow — but it forces four numbers into the open that have been buried in fundraising disclosures for two years.

I want to be careful here. As of today, no public S-1 exists. Every financial figure cited in press coverage flows from CNBC's May 20 scoop, banker-led briefings, and analyst estimates rather than from audited disclosures. The numbers I work with in this analysis — $13.1B 2025 revenue, $22B 2025 burn, $14B 2026 projected operating loss, $25B Q1 2026 annualized run rate, $1.22 lost per $1 of Q1 2026 revenue — are reported figures, not filed figures. I flag that distinction throughout. When the public S-1 lands, expect material revisions in both directions.

This is an editorial-opinion piece. I have no affiliate relationship with OpenAI, Microsoft, Goldman Sachs, Morgan Stanley, or any party involved in the listing. ThePlanetTools.ai does not hold OpenAI equity or any pre-IPO secondary position. The analysis below reflects what I see in the public reporting and what I think the S-1 must disclose to clear public-market diligence. It is not investment advice.

The four numbers the S-1 must answer

Confidential filings let issuers test the waters with the SEC and adjust before public exposure. That privilege ends when the company prices the deal. Between now and the September or Q4 2026 listing window, OpenAI will need to expose specific numbers to public-market scrutiny. In my reading of the reporting and the comparable disclosures from Cerebras's $4.8B Nasdaq debut earlier this month, four numbers will decide whether the deal prices at $852 billion or at $1 trillion.

First, unit economics on the inference layer — the cost-per-token of serving frontier model traffic at the current scale. Roborhythms cites a Q1 2026 operating margin of "negative 122% non-GAAP," meaning OpenAI lost an additional $1.22 for every $1 of revenue, producing roughly $6.95 billion in Q1 losses alone. That margin profile is what a unit economics disclosure has to defend, and the defense has to explain how inference cost trends from here. Second, the compute commitments stack — Roborhythms reports "$600 billion in compute commitments over the next five years" and HSBC analysts estimate a "$207 billion capital gap through 2030." Those are the contractual obligations that bind OpenAI to a specific revenue trajectory regardless of how the model market evolves.

Third, the Microsoft revenue-share mechanics through 2030 and the IP license expiration in 2032. As we covered in the OpenAI × Microsoft amendment analysis, Microsoft holds roughly 27 percent of the public benefit corporation entity — worth approximately $270 billion at the $1 trillion valuation. The revshare cap structure, the IP license terms, and the 2030-2032 transition timeline are now mandatory disclosures in the S-1. Investors will price them. Fourth, the cash-flow breakeven timeline. Investing.com cites that breakeven is "not expected before 2029." That date, if confirmed in the filing, defines the dilution risk for IPO buyers — every quarter of negative free cash flow between September 2026 and 2029 is potential follow-on equity or convertible debt that dilutes the IPO investor's position.

The revenue base and the 65x question

Reported 2025 revenue lands at $13.1 billion. The Q1 2026 annualized run rate, per Investing.com and Roborhythms, is $25 billion, roughly $2 billion per month. The user base, as reported across multiple sources, includes 50 million paid consumer subscribers and 9 million business users, with weekly active users approaching 900 million and inference processing 15 billion tokens per minute. The growth trajectory is the strongest in software history at this revenue scale — and that is the bull case. The bear case is the multiple.

At $1 trillion against $13.1 billion in 2025 revenue, the multiple is 76x trailing twelve months. Against the $25 billion Q1 run rate, the multiple is 40x annualized. Against a hypothetical 2026 revenue of $30 billion that bankers may be modeling, the multiple is 33x forward. None of these multiples are absurd by software-IPO standards — Snowflake debuted at a forward multiple of around 100x, and Cerebras priced this month at a comparable triple-digit multiple — but they require accepting that the growth rate sustains for multiple years against a $22 billion annual cash burn that the unit economics disclosure must address.

The forward-revenue debate is the central diligence question. If 2026 revenue lands at $30 billion (annualizing the Q1 run rate flat), the forward multiple is 33x and the deal is priced for high growth but not for the absolute frontier. If 2026 revenue compounds to $40 billion (reflecting product expansion across ChatGPT enterprise, the API, Codex, and the deployment company JV), the forward multiple drops to 25x — which is where the bull case becomes defensible against software comparables. The S-1 must include 2026 guidance or at minimum a discussion of run-rate trajectory that lets public-market investors model that range.

The burn, the profitability path, and the Anthropic comparison

This is where the strategic comparison gets interesting. Anthropic targeted an $800 billion IPO earlier this year and, per Enterprise DNA reporting, is now targeting "above $900 billion" with an October 2026 listing window. The two listings will price within weeks of each other, on competing investment banks, against directly comparable enterprise AI businesses. The valuation gap — $100 billion at the midpoint between Anthropic and OpenAI — encodes a specific market judgment about scale, growth, and profitability path.

In my reading, the $100 billion gap is the public-market premium on OpenAI's user scale (900 million weekly users, 50 million paid consumer subscribers, 9 million business users) over Anthropic's enterprise-heavy distribution. The premium is real, but it is also vulnerable. Anthropic has been advancing a profitability narrative that OpenAI cannot match at the current burn trajectory. Anthropic just overtook OpenAI in US business adoption on Ramp data — 34.4% versus 32.3%, the first historic flip on the metric, and the strategic implication is that Anthropic's revenue base is shifting toward higher-margin enterprise contracts at the exact moment OpenAI is filing against a higher-burn growth trajectory.

The S-1 narrative therefore has to do two things simultaneously: justify the scale premium that gets OpenAI to $1 trillion, and outline a credible path to operating leverage that closes the $22 billion burn-versus-Anthropic-profitability gap. Those are reconcilable in theory — scale should produce inference cost amortization, and the $25 billion run rate against a flat or growing user base should compound — but the reconciliation has to appear in the financial section of the filing. Hand-waving the burn-to-profitability path will price the deal at $852 billion. Documenting the path with specific operating leverage assumptions will price it at $1 trillion.

The Microsoft cap table and the PBC structure

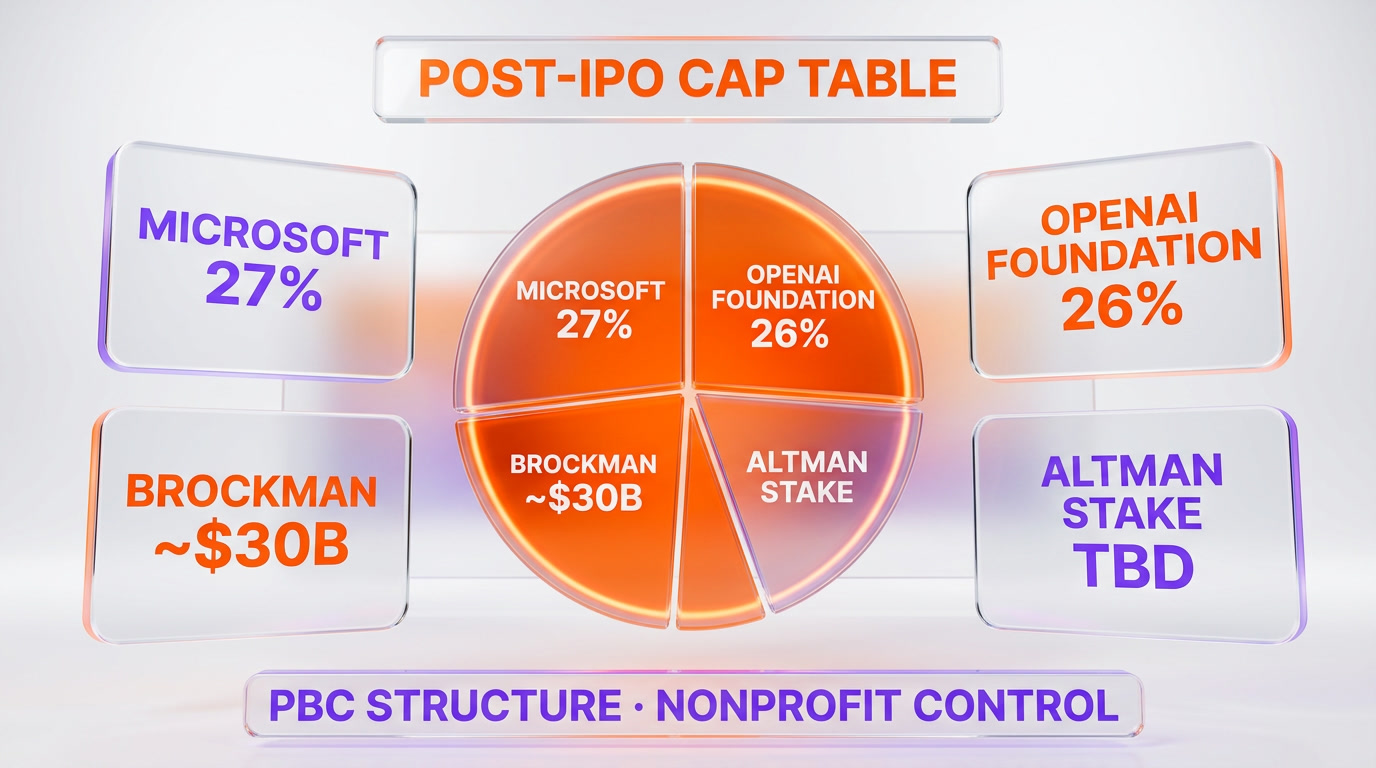

Fortune's reporting on the post-IPO ownership distribution is the most concrete piece of new information the May 22 filing has unlocked. At a $1 trillion valuation, Microsoft holds roughly 27 percent of OpenAI's new public benefit corporation structure — a stake worth approximately $270 billion, comparable to the entire current market capitalization of several Fortune 100 companies. The OpenAI Foundation, the nonprofit parent, retains 26 percent — a stake worth approximately $260 billion that anchors the mission governance structure post-listing.

Greg Brockman's stake is reported at "nearly $30 billion, a figure that could rise to roughly $35 billion" at the $1 trillion valuation. The Brockman number connects directly to the May 18 pre-IPO org reshuffle that placed Brockman over product strategy. Read in sequence — May 18 reshuffle, May 22 filing — the timing tells you the IPO calendar drove the org chart, not the other way around. Brockman moves into a product-leadership position four days before the filing because the S-1 narrative needs a stable product-strategy lead with the largest individual equity stake on the executive team.

Sam Altman's personal stake is one of the four most consequential unknowns the public S-1 has to disclose. Altman has publicly stated he holds no direct OpenAI equity through his founder role at the original capped-profit subsidiary, but the December 2024-2025 conversion to a Delaware public benefit corporation reset the cap table. Whether Altman received equity in the converted structure, whether that equity is performance-vested, and how it compares to Brockman's $30 billion position will be the most-read disclosure in the entire filing. In my reading, public-market sensitivity to founder-CEO equity governance is high after the 2023 board crisis and the 2024 governance turbulence, and the Altman compensation disclosure is the single most likely source of post-filing controversy.

The PBC structure itself is a meaningful disclosure. Public benefit corporations have a fiduciary obligation to consider stakeholder interests beyond shareholder returns. The S-1 must explain how that obligation interacts with the existing OpenAI Foundation governance, how it constrains operating decisions, and how the Microsoft commercial relationship is structured around it. Fortune notes that the OpenAI Foundation retains 26 percent of the new PBC. The Foundation, as the original mission-bound parent, retains specific governance rights that the S-1 must spell out. Public-market investors will price the governance overhang based on how those rights are documented.

The Microsoft amendment, read as pre-IPO cleanup

In the context of the IPO filing, the April 27 Microsoft amendment looks different than it did at announcement. We covered the amendment as a procurement event, and that reading remains correct, but the IPO filing forces a second reading. The amendment cleaned up three issues that would have been disclosure problems in the S-1: the exclusivity question that public-market investors would have priced as a concentration risk, the open-ended revshare obligation that auditors would have struggled to quantify, and the IP license expiration uncertainty that would have appeared as a "going concern" framing risk in any prospectus.

By converting exclusivity to first-launch rights, capping the revshare through 2030, and locking the IP license through 2032, the amendment converted three S-1 disclosure problems into three S-1 narrative strengths. The deal can now be described as a structured, capped, and time-bounded commercial relationship rather than as an open-ended dependency. The amendment was timed to land 25 days before the filing for exactly this reason. Microsoft's stake — 27 percent of the new PBC — is the economic continuity that anchors the relationship through 2030, and the amendment converted the relationship's character from "structural lock-in" to "scheduled transition" in time for the S-1 narrative to read clean.

That reading also explains the May 11 OpenAI Deployment Company $4 billion announcement with Bain, McKinsey, Capgemini, and the Tomoro acquisition. The DeployCo JV documents an enterprise-services revenue stream that scales beyond pure API consumption, which the S-1 needs to support the diversification narrative. Public-market investors prefer revenue mix over revenue concentration. The DeployCo announcement, 11 days before the filing, populated the diversification column of the revenue disclosure. The Brockman reshuffle on May 18 populated the leadership-stability column. The amendment on April 27 populated the partnership-structure column. Read together, the four announcements between April 27 and May 22 are pre-IPO cleanup, sequenced to make the S-1 readable.

The trillion-dollar test — SpaceX and OpenAI together

The Axios reporting frames the OpenAI filing as strategically timed against SpaceX's "imminent IPO unveiling." Investing.com calls the back-to-back listings a "Trillion-Dollar Test" of whether public investors are willing to underwrite trillion-dollar AI infrastructure narratives. In my reading, the OpenAI filing being announced when it was — the same week SpaceX's IPO plans surfaced — is not coincidence. Both deals work the same three banks (Goldman Sachs, Morgan Stanley, JPMorgan). Both deals target Q4 2026 timing. Both deals require public-market investors to accept that conventional earnings analysis does not apply.

The SpaceX listing has a different mechanical profile. Starlink revenue is recurring at scale, and the business is profitable or near-profit-positive depending on the disclosure quarter. The OpenAI listing is not. Pricing the two deals against each other will be the first cross-comparison public markets make. If SpaceX prices well and OpenAI prices in the $852 billion to $900 billion lower range, the market read is that profitability matters and burn is being penalized. If both deals price at the top of their respective ranges, the market read is that AI-infrastructure narrative pricing is intact and the burn-to-profitability path is being underwritten on growth alone.

The September window matters because it lands before US fiscal-year-end and gives institutional investors the budget cycle to allocate to AI listings before Q4 marketing windows close. If the SEC review process pushes either filing into November or December, the deal calendar compresses and pricing dynamics get tougher. The September-to-October window is therefore the optimal timing, and the May 22 confidential filing date is calibrated to the SEC review timeline that hits that window. If the public S-1 surfaces in mid-August, the September window is in reach. If it surfaces in October, the deal slides to November-December and prices against a different macro backdrop.

What the S-1 must not disclose

The disclosure choices are where this gets strategically interesting. OpenAI has flexibility within SEC reporting standards on how much it segments the revenue base (consumer ChatGPT versus API versus enterprise versus Codex versus DeployCo), how much it discloses about model training costs versus inference serving costs, and how much it details about the geographic distribution of users and revenue. Each choice trades transparency for competitive sensitivity.

The competitive sensitivity is real. Anthropic, Google DeepMind, xAI, and emerging frontier players will read every disclosed number against their own internal benchmarks. Model training cost disclosure is the single most competitively sensitive number in the filing — if OpenAI discloses that training the next frontier generation costs $X billion, every competing lab will price their own compute commitments against that benchmark and the structural moats of frontier-model investment shift. In my reading, expect the S-1 to disclose aggregate "research and development" without separating training versus inference, and expect the SEC review process to push back on that aggregation. The eventual disclosure will be more granular than OpenAI prefers and less granular than investors want.

Geographic revenue disclosure is the second sensitivity. If a meaningful percentage of OpenAI's $25 billion run rate comes from outside the United States — China, EU, India, or specific high-growth markets — the public S-1 must disclose the geographic split. That disclosure has implications for trade policy, export-control compliance, and competitive pricing in those markets. Microsoft has the same disclosure obligation, but Microsoft's geographic revenue is diversified across hundreds of products. OpenAI's is concentrated across a small number of products with limited geographic obfuscation. The geographic disclosure will be more transparent than competitive strategists at OpenAI would prefer.

The four questions the S-1 must answer

Stepping back, the S-1's job between confidential filing and pricing is to answer four questions to the satisfaction of three buyer pools: institutional asset managers, retail buyers via the eventual public listing, and the sovereign wealth funds that will participate in the cornerstone investor tranche. Each pool will read the disclosures differently, but the four questions are common across all three.

Question one: what is the unit economics trajectory on the inference layer? The Q1 2026 operating margin of negative 122 percent — losing $1.22 for every $1 of revenue per Roborhythms — must show a clear improvement path. The improvement levers are well understood (cheaper inference hardware, model distillation, batch optimization, custom silicon) but the S-1 must quantify their contribution and timeline. A disclosure that shows unit economics turning positive by 2028 prices the deal favorably. A disclosure that stretches that timeline to 2030 or later prices it lower.

Question two: how is the $600 billion compute commitment funded? The HSBC analyst estimate of a $207 billion capital gap through 2030 implies that OpenAI's current revenue trajectory does not fund the compute obligations. The S-1 must outline how that gap is closed — through follow-on equity, convertible debt, structured financing against compute infrastructure, or a combination. The funding mechanism affects dilution risk for IPO buyers materially. Equity-heavy funding dilutes pro rata. Debt-heavy funding adds interest expense and credit risk. Structured financing transfers the asset risk to lenders but adds operational constraints.

Question three: what are the Microsoft cap mechanics through 2030 and the IP license through 2032? The amendment clarified the structure but did not disclose the specific dollar cap on the revshare. The S-1 must specify the dollar value and the calculation method. That number — call it the "Microsoft cap" — is the single most important commercial disclosure in the filing for the period between 2026 and 2030. It defines OpenAI's net revenue capture across enterprise distribution channels and bounds Microsoft's economic upside outside the equity stake.

Question four: when does cash-flow breakeven arrive? Investing.com cites that breakeven is "not expected before 2029." If the S-1 confirms 2029 or earlier with credible operating leverage assumptions, the deal prices toward $1 trillion. If the S-1 pushes breakeven to 2030 or later, the deal prices toward $852 billion. The cash-flow breakeven timeline is the disclosure that anchors every other diligence question because it converts the abstract burn-to-profit narrative into a specific dilution-risk timeline.

What would prove me wrong

I want to be explicit about the failure modes for this analysis. Several specific developments would invalidate the read above and force a different framing.

First, the SEC review process delays the deal past Q4 2026. The confidential filing is the start of a multi-week review that surfaces specific disclosure questions, and historical comparable filings have taken anywhere from 90 to 240 days from confidential submission to public S-1. If the SEC review surfaces material questions on the PBC governance structure, the OpenAI Foundation control rights, the Microsoft revshare cap accounting, or the model training cost disclosures, the timeline slips. A Q1 2027 listing prices against a different macro environment and likely a different valuation range.

Second, the Microsoft amendment unwinds. The amendment is documented in the joint OpenAI-Microsoft April 27 announcement, but its operational implementation across AWS Bedrock, Google Cloud, and Oracle remains in progress. If a material dispute surfaces between Microsoft and OpenAI on the cap calculation method, the first-launch interpretation, or the IP license scope, the amendment becomes a disclosure liability rather than a strength. The S-1's narrative about "structured commercial relationship" weakens, and the deal prices lower.

Third, governance turbulence resurfaces. The 2023 board crisis remains the most-referenced precedent for OpenAI governance risk. If the period between filing and pricing surfaces new board, foundation, or executive disputes — particularly around the Altman compensation disclosure or the PBC obligation interpretation — the deal prices at a governance discount. The 2024-2025 conversion to PBC was meant to resolve governance, but the S-1 disclosures will test whether the resolution holds under public-market scrutiny.

Fourth, macro conditions deteriorate. The September-October 2026 window assumes Federal Reserve policy is supportive of equity issuance, the AI-infrastructure narrative remains the dominant market theme, and competing IPO supply does not absorb available institutional capital. If any of those conditions weaken — rate path tightens, AI narrative cools, or the SpaceX listing absorbs disproportionate institutional allocation — the deal prices lower or slips. In my reading, the macro window is currently supportive but materially fragile.

Fifth, an audit finding emerges. Confidential S-1 review surfaces audit questions that often do not become public until the eventual public filing. If the SEC review surfaces material revenue recognition questions on the consumer subscription base, the enterprise contract structure, or the API consumption accounting, the disclosed revenue figures revise materially. Either direction — upward or downward — affects the multiple math. A downward revision of 10 to 15 percent prices the deal at $750 billion to $850 billion. An upward revision is possible but historically less common at this scale.

What the listing tells us about the AI cycle

Beyond the deal-specific reading, the OpenAI filing is a signal about where the AI investment cycle sits. The 2022-2025 phase was private-market funding at increasing valuations. The 2026 phase — marked by Cerebras's $48.8 billion Nasdaq debut, OpenAI's confidential filing, Anthropic's October target, and SpaceX's parallel listing — is the public-market transition phase. Each successful listing changes the institutional cost of capital for AI infrastructure and unlocks new private-to-public flow.

The structural read is that the 2026-2028 window will see five to ten trillion-dollar or near-trillion-dollar AI listings, with OpenAI and Anthropic as the lead names and a tail of infrastructure plays (custom silicon, agent platforms, vertical AI applications) following. Each listing absorbs institutional capital that would otherwise flow to private markets, which compresses private-market valuations for late-stage rounds and accelerates the IPO path for the next tier of private companies. The flywheel was visible at small scale with the Cerebras listing this month and will run at full scale with OpenAI in September.

The risk to the flywheel is concentrated in two failure modes: a deal prices materially below expectations (the OpenAI deal pricing at $700 billion would be the canonical case), or a deal trades poorly post-listing for the first six to twelve months. Either outcome would tighten institutional appetite for the subsequent tail of AI listings and could delay the broader public-market transition by 12 to 24 months. The deal-specific stakes for OpenAI are therefore higher than the immediate dilution math suggests — the listing's reception will price the entire 2026-2028 AI listing pipeline.

What I am watching between now and pricing

The signals I will be tracking between the May 22 confidential filing and the eventual September pricing:

The SEC comment letter timeline. Material questions on the PBC structure, the Microsoft revshare cap, the model training cost segmentation, or the geographic revenue disclosure will show up as comment-letter exchanges. The frequency and depth of those exchanges signal how much disclosure friction sits between OpenAI and the public S-1.

The cornerstone investor tranche. Confidential filings are typically paired with private cornerstone-investor conversations that lock in roughly 20 to 40 percent of the deal at pricing. The identity of those cornerstone investors — sovereign wealth funds, large institutional asset managers, strategic corporate buyers — and the size of their commitments shape the pricing dynamic. Expect rumors and selective disclosures across June and July.

The competitive announcement pace. Anthropic, Google DeepMind, xAI, and Meta AI all face the strategic question of how to position against the OpenAI listing. Expect competing announcements on model capability, enterprise deals, and infrastructure investment timed to the OpenAI filing window. Anthropic's own IPO timeline — currently October 2026 per Enterprise DNA reporting — will need to maintain relative positioning, which constrains the disclosure choices Anthropic can make.

The Microsoft and Foundation disclosures. Microsoft, as a 27 percent holder, has its own disclosure obligations to its public shareholders about the OpenAI stake's value and accounting treatment. The OpenAI Foundation has its own nonprofit disclosure obligations as well. Both sets of disclosures will surface incremental information about the OpenAI structure ahead of the public S-1.

The macro market read. Federal Reserve policy, broader equity market conditions, and competing IPO supply across June, July, and August will set the pricing environment. The market open in September with OpenAI as the lead AI listing will price not just the company but the entire AI-infrastructure narrative for the subsequent listing pipeline.

Frequently asked questions

When did OpenAI file its S-1 for IPO?

OpenAI confidentially submitted its S-1 to the SEC on May 22, 2026, per reporting from CNBC, Fortune, and Axios. Confidential filings remain private until roughly 15 days before the public roadshow, so the public version of the S-1 is expected to surface in mid to late August 2026 if the September listing window holds.

What is OpenAI's target IPO valuation?

The reported valuation range is $852 billion to $1 trillion. The $852 billion floor reflects OpenAI's last private funding round in October 2025. The $1 trillion ceiling reflects the bull case that bankers Goldman Sachs and Morgan Stanley are reportedly working toward. Final pricing will depend on the disclosures in the public S-1 and the macro market conditions in September.

Which banks are leading the OpenAI IPO?

Goldman Sachs and Morgan Stanley lead the deal as bookrunners, with JPMorgan participating per Axios reporting. The same three banks are reportedly working on the parallel SpaceX listing, which is one of the strategic reasons the OpenAI filing was timed to land before SpaceX's own unveiling.

When will OpenAI go public?

The targeted public debut window is Q4 2026, potentially as early as September 2026 per Fortune and Enterprise DNA reporting. The actual listing date depends on the SEC review timeline, the market conditions in the September-October window, and whether competing IPO supply (notably SpaceX) shifts the deal calendar.

What was OpenAI's 2025 revenue?

Reported 2025 revenue is approximately $13.1 billion per Investing.com and Roborhythms, with a Q1 2026 annualized run rate of $25 billion (roughly $2 billion per month). These are reported figures from banker-led briefings and analyst estimates, not yet audited disclosures. The public S-1 will confirm the audited number.

How much is OpenAI losing each year?

OpenAI's 2025 cash burn is estimated at $22 billion with a net loss around $9 billion per Roborhythms. The 2026 projected operating loss is approximately $14 billion. Q1 2026 alone reportedly produced roughly $6.95 billion in losses against $6 billion in revenue — a negative 122 percent non-GAAP margin meaning OpenAI lost $1.22 for every $1 of revenue.

What is Microsoft's stake in OpenAI after the amendment?

Microsoft holds approximately 27 percent of OpenAI's new public benefit corporation structure per Fortune reporting, worth approximately $270 billion at the $1 trillion valuation. The April 27, 2026 amendment converted Azure exclusivity to first-launch rights, capped the revenue share through 2030, and extended the IP license through 2032 — cleanup that mechanically prepared the deal structure for the S-1 disclosures.

What is the OpenAI Foundation's stake?

The OpenAI Foundation, the nonprofit parent that retains mission governance control, holds 26 percent of the public benefit corporation per Fortune reporting — a stake worth approximately $260 billion at the $1 trillion valuation. The Foundation's governance rights over the PBC are a mandatory S-1 disclosure that public-market investors will scrutinize for their effect on operating decisions.

How does the OpenAI IPO compare to the Anthropic IPO?

Anthropic is targeting an October 2026 listing at a valuation above $900 billion per Enterprise DNA reporting, roughly four weeks after OpenAI's targeted September window. The $100 billion midpoint gap encodes the market's premium on OpenAI's user scale (900 million weekly users) over Anthropic's enterprise-heavy distribution. Anthropic is advancing a profitability narrative that OpenAI cannot currently match given the $22 billion annual burn.

What is Greg Brockman's stake at the $1 trillion valuation?

Greg Brockman's equity stake is reported by Fortune at "nearly $30 billion, a figure that could rise to roughly $35 billion" at the $1 trillion valuation. The May 18, 2026 pre-IPO org reshuffle that placed Brockman over product strategy connected directly to the May 22 filing — the timing tells us the IPO calendar drove the org chart, not the other way around.

What is Sam Altman's stake in OpenAI?

Sam Altman's personal equity stake is one of the most consequential unknowns the public S-1 must disclose. Altman has publicly stated he held no direct equity in the original capped-profit subsidiary, but the December 2024-2025 conversion to a Delaware public benefit corporation reset the cap table. Whether Altman received equity in the converted structure and how it compares to Brockman's approximately $30 billion position will be the most-read disclosure in the filing.

What are the four numbers the S-1 must answer?

Per my reading: unit economics on the inference layer (current Q1 2026 margin is negative 122 percent), the $600 billion compute commitments stack against the HSBC-estimated $207 billion capital gap through 2030, the Microsoft revshare cap mechanics through 2030 and the IP license through 2032, and the cash-flow breakeven timeline (Investing.com cites "not expected before 2029"). These four disclosures will decide whether the deal prices at $852 billion or at $1 trillion.

Bottom line

OpenAI's May 22 confidential S-1 filing is the largest pre-IPO event in tech history and will price the entire AI-infrastructure narrative for the September-October 2026 listing window. The reported numbers — $852 billion to $1 trillion valuation, $13.1 billion 2025 revenue, $22 billion 2025 burn, $14 billion 2026 projected operating loss, $25 billion Q1 2026 run rate, $207 billion capital gap through 2030 — are not yet audited disclosures. They flow from banker-led briefings and analyst estimates. The public S-1 will revise them. In my reading, the deal prices in the $900 billion to $1 trillion range if the four S-1 questions on unit economics, compute commitment funding, Microsoft cap mechanics, and breakeven timeline get credible answers. It prices in the $750 billion to $850 billion range if those disclosures surface meaningful diligence pushback. Either outcome rewires institutional appetite for the subsequent AI-listing pipeline.

Editorial disclosure: this analysis is editorial opinion based on public reporting from Fortune, CNBC, Axios, Investing.com, Roborhythms, Enterprise DNA, and AI Weekly. ThePlanetTools.ai has no affiliate relationship with OpenAI, Microsoft, Goldman Sachs, Morgan Stanley, or any party involved in the listing. The site does not hold OpenAI equity or any pre-IPO secondary position. This is not investment advice and should not be relied on for any allocation decision. — Anthony Martinez, May 24, 2026.