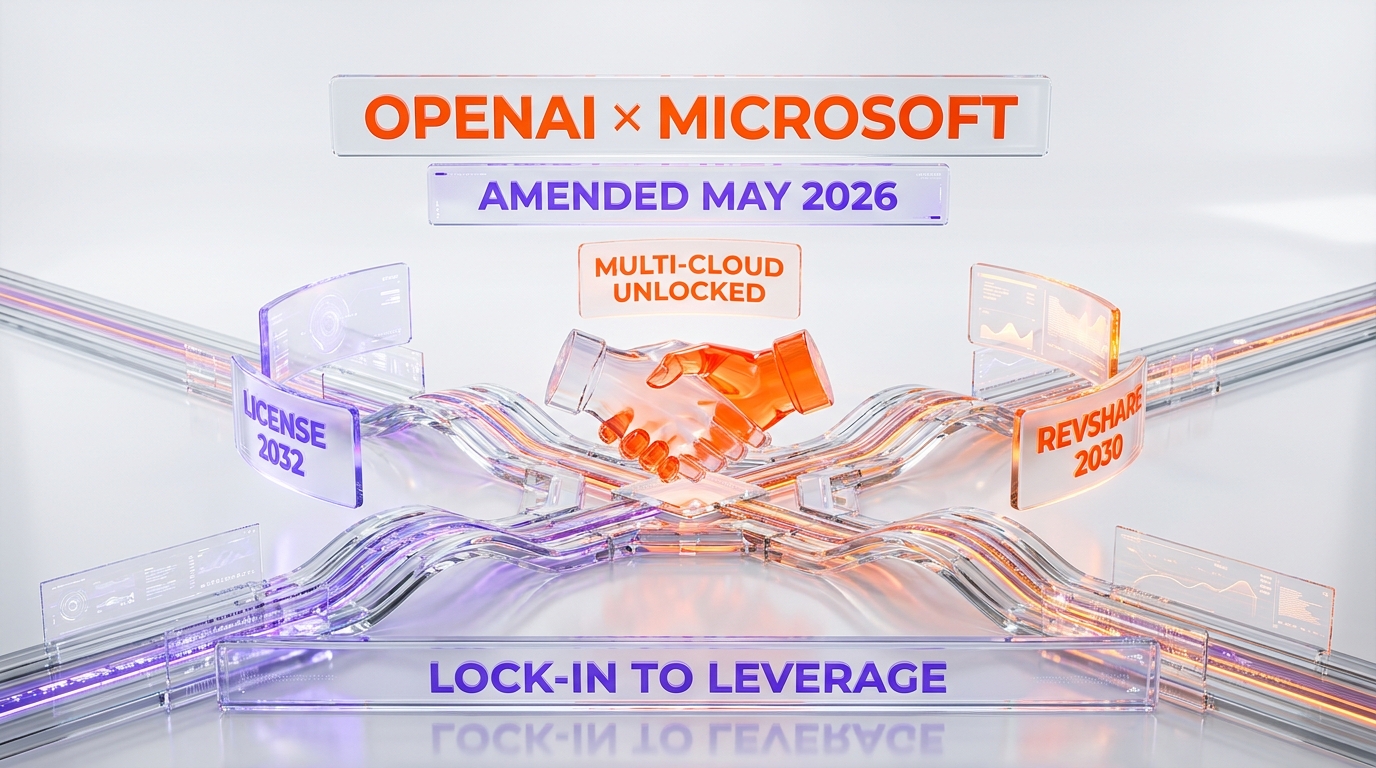

OpenAI and Microsoft amended their partnership on April 27, 2026, ending Azure's structural exclusivity on OpenAI model deployment. Under the amended terms, OpenAI can now serve all its products across any cloud provider, Microsoft retains a non-exclusive IP license through 2032, and OpenAI's revenue-share payments to Microsoft continue through 2030 under a total cap. Two weeks later, on May 13, 2026, CNBC reported on internal Microsoft strategy testimony revealing that Satya Nadella had feared as early as April 2022 that Microsoft was on track to become "the next IBM" through its OpenAI dependency. The amendment, read against that backdrop, is not a friendly evolution. It is the formal exit from a structural risk that Microsoft's CEO had internally diagnosed four years earlier.

We have been tracking the Microsoft-OpenAI partnership architecture since the original 2023 multi-billion-dollar investment, and the April 27 amendment is the single most consequential procurement event in enterprise AI since that initial deal. The shift from exclusive to non-exclusive licensing rewrites every assumption that IT buyers, cloud strategy teams, and AI vendor management functions have operated on for the past three years. The Fifthrow strategic analysis frames the change as a move from lock-in to leverage, and the framing holds because it accurately captures what the amendment unlocks: procurement leverage that was contractually impossible 30 days ago.

What the amendment actually changes

The headline is multi-cloud, but the mechanics matter. The amended agreement, as published jointly by OpenAI and Microsoft on April 27, 2026, makes four structural changes to the previous deal. Microsoft's license to OpenAI intellectual property — covering frontier models and product implementations — extends through 2032 and is no longer exclusive. OpenAI is now permitted to serve all of its commercial products to customers across any cloud provider, breaking Azure's prior right of refusal. Microsoft remains OpenAI's primary cloud partner, and OpenAI products will continue to ship first on Azure unless Microsoft "cannot and chooses not to support the necessary capabilities." Revenue-share payments from OpenAI to Microsoft continue through 2030, but the payments are now subject to a total cap rather than open-ended.

The "total cap" language is the most technically dense clause in the amendment. Microsoft and OpenAI have not disclosed the dollar value of the cap, but every analyst we have read converges on the inference that the cap is bounded by Microsoft's existing equity position rather than by an arbitrary financial milestone. Microsoft holds approximately 27 percent of OpenAI's commercial entity, a stake valued in the most recent public reporting at around $135 billion. The revenue-share cap is structured to ensure that Microsoft's economic upside continues to flow through equity appreciation rather than through ongoing revenue-share royalties — a cleaner accounting structure that simplifies the eventual OpenAI public-market exit and reduces the surface area for future disputes about what constitutes "revenue" under the agreement.

The "first launch" provision is the second most consequential clause. OpenAI products will still ship first on Azure — that is the explicit language. The carve-out is narrow but real: if Microsoft "cannot and chooses not to support the necessary capabilities," OpenAI can ship elsewhere first. In practice, the carve-out becomes operative when Azure lacks the compute footprint, the regulatory posture, or the geographic presence to support a given model release. For most major launches between now and 2032, Azure will retain the first-mover advantage. For specialized launches — sovereign-cloud deployments, regulated-industry pilots, hardware-specific optimizations — the carve-out becomes the trapdoor that lets OpenAI partner directly with AWS, Google Cloud, or Oracle on day one.

The multi-cloud impact on enterprise procurement

The amendment's biggest procurement implication has nothing to do with Microsoft and everything to do with AWS. Within weeks of the announcement, Amazon CEO Andy Jassy confirmed that AWS Bedrock would offer access to OpenAI's frontier models, including GPT-5.5 and Codex, on the standard Bedrock pricing and governance model. Named early adopters in AWS communications included Ericsson, Thomson Reuters, Cox Automotive, and Fox Sports — a roster heavy on regulated industries and global enterprises with existing AWS commitments. The implication is that AWS is now positioned as the direct alternative deployment surface for OpenAI workloads, with the operational integration that AWS-native customers have spent years building (IAM, PrivateLink, CloudTrail) immediately usable for OpenAI model access.

Google Cloud and Oracle have not yet announced general availability of OpenAI models on their platforms, but the Fifthrow analysis and Constellation Research reporting both treat their inclusion as a near-term certainty. The structural read is that the amendment created the legal possibility of multi-cloud, AWS moved first to make it commercially real, and the remaining hyperscalers will follow on a timeline driven primarily by their own engineering capacity to support OpenAI's API surface and their commercial willingness to pay OpenAI for the privilege. For procurement teams, this means the realistic comparison set for OpenAI workloads in mid-2026 is Azure versus AWS, with GCP and Oracle entering the comparison frame by Q4 2026 at the latest.

The 2032 and 2030 timeline that creates leverage

The dates matter more than they look. The IP license to Microsoft runs through 2032 — six years from the amendment date. The capped revenue share runs through 2030 — four years. The asymmetric runway tells you exactly how the parties expect the relationship to evolve. Through 2030, Microsoft retains both economic flow (capped revshare) and IP access (license). Between 2030 and 2032, Microsoft retains IP access but loses ongoing revenue-share economics. After 2032, the structural relationship is open for renegotiation in a market that will look nothing like 2026.

That asymmetric structure creates a specific kind of leverage window for enterprise buyers. For deals signed before 2030, the buyer benefits from a Microsoft incentive to retain the OpenAI workload on Azure (because Microsoft is still collecting revenue share on consumption). For deals signed between 2030 and 2032, the Microsoft incentive shifts toward retaining the IP license as a competitive moat rather than as a revenue stream. For deals signed after 2032, the buyer is operating in a market where Microsoft's structural Azure-OpenAI advantage may or may not still exist, depending on whether the partnership is renewed. The strategic implication: long-term enterprise commitments to OpenAI workloads should be sized to the 2030-2032 transition rather than to the 2032 license expiration.

The Musk v. Altman trial context that frames the amendment

The amendment was announced on April 27, four days before the Musk v. Altman trial opened in the Northern District of California on May 1. The timing was not accidental. The trial discovery process, as we have been analyzing across our Musk v. Altman trial coverage, surfaced an April 2022 internal Microsoft strategy memo in which Satya Nadella documented his concern that Microsoft was at risk of becoming "the next IBM" — a reference to IBM's 1980s positioning as the hardware partner of a software ecosystem that captured all the strategic upside while IBM captured the commodity hardware role. The memo was disclosed during trial discovery and reported publicly by CNBC on May 13.

Read in sequence, the amendment becomes the public-facing resolution of a private concern that Nadella had internally diagnosed four years earlier. Microsoft committed billions to OpenAI in 2023 with the "next IBM" risk fully understood at the CEO level. The amendment is the formal mechanism by which Microsoft restructured the relationship to escape that risk: by giving OpenAI multi-cloud rights, Microsoft eliminated the strategic dependency that the 2022 memo identified. Microsoft trades exclusive control for capped economic continuity and a multi-year IP license window — a trade that protects Microsoft's downside while removing the structural risk of being the locked-in commodity partner.

The trial verdict, expected within five to ten business days of the May 14 closing arguments, will determine the legal status of the 2024-2025 OpenAI conversion from capped-profit subsidiary to Delaware public benefit corporation. The amendment is structurally independent of that verdict — both parties have agreed to the new terms regardless of how the conversion question is resolved. But the trial record makes the amendment readable as a strategic act with a precise CEO-level rationale, not as a negotiation outcome arrived at in good faith between equals. Microsoft restructured because Microsoft had to. OpenAI agreed because OpenAI gained the multi-cloud distribution surface it needed to grow past Azure's capacity limits.

"Lock-in to leverage": the procurement framework shift

The Fifthrow strategic framework is the most precise public articulation of what the amendment changes for IT buyers. The shift is from a market in which OpenAI workloads were available only on one cloud — making procurement leverage limited to volume discounts within that cloud — to a market in which the same workloads are available across multiple clouds, making procurement leverage available across competitive RFPs, cross-cloud benchmarking, and migration-clause negotiation. The framework identifies four specific leverage points that were previously unavailable.

First, capped revenue-share terms. Enterprise buyers can now negotiate consumption caps on OpenAI workloads across clouds, because the cloud providers themselves are now competing for the OpenAI workload share. Second, transparent cross-cloud model licensing. Buyers can request and receive disclosure of how OpenAI's first-launch rights affect model parity across Azure and AWS, with formal disclosures becoming part of the contract evidence rather than vendor-supplied marketing. Third, explicit audit rights and migration clauses. Procurement teams can now write contract language that gives them the right to migrate OpenAI workloads from one cloud to another with defined SLAs and data-portability obligations on the cloud provider. Fourth, performance parity guarantees. Buyers can demand that cloud providers guarantee latency, throughput, and feature parity across deployment surfaces — guarantees that were structurally impossible when Azure had exclusivity.

The documented savings on early implementations support the framework. Redress Compliance, cited in the Fifthrow analysis, achieved over $5.2 million in cost avoidance on a single multi-cloud OpenAI procurement structured in the weeks after the amendment. The savings came from leveraging cross-cloud pricing competition during the contract negotiation, not from operational efficiency gains post-deployment. That distinction matters: the savings exist because the leverage exists, and the leverage exists because the amendment created the competitive market structure that procurement teams can now negotiate against.

The "soft lock-in" that replaces hard exclusivity

The amendment does not eliminate all lock-in dynamics. It eliminates the contractual exclusivity that defined the previous deal, and replaces it with operational integration depth that creates new switching costs. Azure retains entrenched advantages that the amendment does not touch: deep managed service integrations including Cognitive Services, Microsoft Fabric, and Sentinel; exclusive early access to new model generations under the first-launch provision through 2032; feature and version lag on competing platforms during the rollout window of each new model; and cloud-specific agent and orchestration toolchains that enterprises have spent two years building against the Azure-OpenAI integration surface.

Feature parity on AWS Bedrock — and later on Google Cloud and Oracle — remains a work in progress, with early reports of lag in specific agent and security functionalities relative to the Azure deployment. The Fifthrow analysis notes that integration depth differs across providers: Azure leads in enterprise-oriented orchestration maturity, AWS Bedrock offers regulatory flexibility and existing customer relationships, and other providers remain nascent. The structural read for procurement is that the amendment unlocks the legal possibility of multi-cloud OpenAI workloads, but the operational reality is that Azure will retain feature leadership for the next 18 to 24 months on most enterprise-grade integrations.

The implication for IT decision-makers: the leverage is real, but exercising it requires accepting a feature-parity gap during the transition. Enterprises that need the latest OpenAI capabilities the day they ship will stay on Azure. Enterprises that prioritize cost, governance flexibility, and existing-vendor consolidation will move workloads to AWS as Bedrock catches up. The bifurcation is rational, not contradictory: the amendment created the option, and procurement teams now choose which side of the option to exercise based on their specific tradeoff between feature recency and cost-governance leverage.

What the amendment means for AWS, Google, and Oracle

AWS moved first and aggressively. Andy Jassy's confirmation that OpenAI models would ship on Bedrock within weeks of the amendment was paired with rollout announcements for Trainium-optimized OpenAI inference, named-customer commitments from Ericsson and Thomson Reuters, and explicit integration with AWS's existing IAM and PrivateLink governance surface. The strategic posture is clear: AWS treats OpenAI access as a marquee Bedrock capability and is investing in the engineering and customer-success motion to make multi-cloud OpenAI adoption operationally seamless for existing AWS customers.

Google Cloud's posture has been more measured. The expected GCP rollout of OpenAI models on Vertex AI sits in a more competitively complex position because Google operates Gemini as a directly competing frontier model line. The Constellation Research analysis notes that Google Cloud is signaling near-term availability but has not committed to a specific timeline. The strategic read is that GCP wants OpenAI workload share for customer-acquisition reasons but is cautious about positioning OpenAI as the default frontier model on its own platform, given the Gemini competitive overlap. Expect GCP availability by Q4 2026, with positioning that treats OpenAI as one option in a broader frontier-model catalog rather than as the default.

Oracle's posture is the wildcard. Oracle has been pursuing OpenAI integration through the OpenAI Stargate compute partnership and has a strong incentive to add OpenAI model access to OCI as a sovereign-cloud and regulated-industry differentiator. Oracle's smaller frontier-AI footprint relative to AWS and GCP means that OpenAI on OCI faces less internal competition, and Oracle's traditional strength in regulated-industry enterprise deployments aligns well with the OpenAI customer base in financial services, healthcare, and government. We expect Oracle to announce OpenAI on OCI by Q3 2026, with specific positioning around sovereign-cloud and air-gapped deployment scenarios that AWS and GCP do not prioritize.

How enterprise IT teams should respond

The amendment changes the procurement playbook in five concrete ways. First, audit current state. Inventory all existing OpenAI-dependent workloads, their Azure integration depth, and their actual cloud-specific feature dependencies. Most enterprises will discover that 60 to 80 percent of their OpenAI workloads have shallow Azure integration that is portable to AWS Bedrock with minimal engineering work, while 20 to 40 percent have deep integration with Azure-specific tooling that would require meaningful migration effort.

Second, benchmark independently. The Fifthrow analysis is explicit that as of May 2026 no independent enterprise-ready dashboard exists to benchmark end-to-end OpenAI performance across clouds. The implication is that procurement teams should build internal benchmarking capacity — measuring latency, throughput, token-level cost, and SLA adherence on actual production workloads on each candidate cloud — rather than relying on vendor-supplied performance comparisons.

Third, deploy real-time governance. The procurement intelligence requirement has shifted from static annual reviews to continuous SLA, cost, and feature-parity tracking. Tools like Ivalua and Suplari are positioned for this category, but the operational requirement is procurement-team capacity to actually exercise the leverage that the contracts now enable. Without continuous benchmarking, the contractual rights granted by the amendment become unused leverage.

Fourth, establish cross-functional teams. The amendment makes AI procurement a cross-domain function: procurement for commercial terms, legal for contract structure, IT for technical integration, compliance for regulatory posture. The previous Azure-exclusive structure allowed single-function ownership; the multi-cloud structure forces functional integration. Enterprises that organize for cross-functional AI procurement will exercise leverage faster than those that retain siloed structures.

Fifth, plan for the 2030 transition. The capped revenue share ends in 2030. The IP license continues to 2032. Enterprise commitments to OpenAI workloads should be sized with that timeline in mind, particularly for multi-year contracts signed in 2026 and 2027 that will straddle the 2030 cap expiration. The contracting recommendation is to build explicit renegotiation triggers at the 2030 milestone, with the right to re-bid the workload across clouds at that point.

The Azure OpenAI Service tactical implications

For enterprises currently on Azure OpenAI Service, the amendment does not require immediate action. The first-launch provision means that new OpenAI models will continue to arrive on Azure before they reach other clouds, and the Azure-OpenAI integration surface remains the most mature for at least the next 18 months. The recommended posture is to retain Azure as the primary deployment surface for production workloads requiring the latest models, while building parallel capability on AWS Bedrock for workloads where cost, governance, or vendor diversification carry more weight than feature recency.

The tactical procurement move is to use the amendment as the basis for renegotiating existing Azure OpenAI Service contracts. Microsoft account teams are now operating with the knowledge that the customer has a credible alternative deployment surface, which changes the bargaining dynamic on consumption discounts, volume commitments, and contract length. Enterprises with significant existing Azure OpenAI spend should expect to extract 5 to 15 percent pricing concessions on renewal, based on the leverage the amendment creates — comparable to the savings documented in the Redress Compliance case study.

The developer and tooling ecosystem response

The amendment also reshapes the developer-tooling ecosystem around OpenAI. Tools like Claude Code and the broader Anthropic developer surface gain competitive positioning, because the multi-cloud OpenAI distribution surface increases the credibility of frontier-model multi-vendor strategies at the developer level as well as the enterprise level. ChatGPT as a product surface is unchanged by the amendment, but the underlying GPT-5.5 model line gains distribution surface that strengthens the long-term ChatGPT competitive position by ensuring that OpenAI's API revenue base is not capped by Azure's deployment capacity.

GPT-5.5, the current frontier OpenAI model, becomes the first major model release to land on multiple clouds simultaneously. The strategic implication is that GPT-5.5's commercial trajectory will not be capped by Azure deployment throughput — a real constraint that has affected the rollout pace of previous frontier OpenAI models. For developer adoption, this means GPT-5.5 capacity availability should be substantially better in mid-2026 than the rollout pace of previous frontier releases, which should accelerate the model's penetration in production deployments.

The Claude competitive surface gains a different kind of advantage. Anthropic's existing multi-cloud distribution — Claude is available on AWS Bedrock, Google Cloud, and through Anthropic's direct API — has been a real differentiator against the Azure-exclusive OpenAI model. The amendment narrows that differentiation. Anthropic will respond by deepening cloud-specific integrations and by accelerating its public-market trajectory, which our coverage of the Anthropic business adoption trajectory has tracked across the past 90 days.

The Microsoft Copilot enterprise context

The amendment lands in the context of Microsoft Copilot's continued enterprise growth. Microsoft Copilot crossed 20 million paying users with $37 billion ARR in May 2026, and the Copilot Cowork frontier preview launched in the same month with agentic task execution capabilities. Microsoft's Copilot business is structurally insulated from the amendment because Copilot operates on Azure regardless of the underlying frontier-model relationship — the integration surface, the enterprise distribution motion, and the M365 attach value remain Microsoft's regardless of whether OpenAI models also ship on AWS.

The strategic read is that Microsoft is comfortable giving up OpenAI's exclusive deployment surface because Microsoft has already extracted the strategic value it needed: market-leading enterprise AI distribution through Copilot, deep integration of OpenAI capabilities into the M365 surface, and continued IP access through 2032 to keep that integration alive. The amendment removes a structural risk (the "next IBM" dependency) while preserving the commercial value (Copilot's enterprise growth) and the strategic optionality (IP license through 2032). For Microsoft, the trade is favorable. For OpenAI, the trade is also favorable, because OpenAI gains the distribution surface to grow past Azure's capacity constraints. The amendment is the rare deal in which both parties improve their position.

What could still go wrong

The amendment is structurally sound but operationally untested. Three failure modes are visible in the early implementation reporting. First, feature-parity gaps on non-Azure clouds may persist longer than the 18-24 month estimate. If AWS Bedrock and Google Cloud cannot close the integration depth gap with Azure on OpenAI-specific tooling, the legal multi-cloud right becomes a practical single-cloud reality, and the procurement leverage the amendment creates becomes notional rather than real.

Second, the OpenAI Deployment Company structure, covered in our $4 billion JV analysis with Bain, McKinsey, Capgemini, and the Tomoro acquisition, creates a parallel channel through which OpenAI services large enterprises directly rather than through cloud-provider intermediation. The structural question is whether OpenAI Deployment Company's direct-engagement model will pull large enterprise workloads off cloud providers entirely, or whether the deployment company will operate as a layer that sits on top of multi-cloud infrastructure. The answer matters because it determines whether the amendment's cloud-procurement implications scale to the largest enterprise deals or are limited to mid-market deployments.

Third, the trial verdict in Musk v. Altman, if it lands against OpenAI on the PBC conversion question, could introduce structural uncertainty about OpenAI's long-term corporate form that affects the amendment's enforceability. The amendment was signed by OpenAI's current commercial entity. If the trial verdict requires unwinding aspects of that entity's structure, the amendment terms could require renegotiation. Both parties have signaled confidence that this risk is contained, but the trial record makes it impossible to rule out completely until the verdict lands.

The strategic bottom line

The amendment is the most consequential enterprise AI procurement event of 2026. It ends Azure's structural exclusivity on OpenAI deployment. It creates a real multi-cloud market for frontier OpenAI workloads. It shifts procurement leverage from cloud providers to enterprise buyers in a way that was contractually impossible 30 days before the announcement. And it does all of that while preserving Microsoft's economic position through capped revenue share to 2030 and IP license to 2032, giving Microsoft a runway long enough to absorb the strategic shift without operational disruption.

The framework shift — from lock-in to leverage — is the right way to read the amendment. The structural question for the next 24 months is whether enterprise IT teams build the procurement capacity to exercise the leverage that the amendment grants. Those that do will extract documented savings on the scale of Redress Compliance's $5.2 million. Those that do not will retain the same procurement posture they had under Azure exclusivity and will leave the leverage unused on the table. The amendment created the option. The exercise is now on the buyer.

Frequently Asked Questions

When was the OpenAI-Microsoft partnership amendment announced?

The amendment was announced jointly by OpenAI and Microsoft on April 27, 2026. The internal Microsoft strategy testimony revealing Satya Nadella's April 2022 "next IBM" memo was reported publicly by CNBC on May 13, 2026, two weeks after the amendment, providing strategic context for why Microsoft restructured the relationship.

Can OpenAI now serve its products on AWS, Google Cloud, and Oracle?

Yes. Under the amended agreement, OpenAI can serve all of its commercial products to customers across any cloud provider. AWS Bedrock launched OpenAI model access within weeks of the announcement, with Amazon CEO Andy Jassy confirming named early adopters including Ericsson, Thomson Reuters, Cox Automotive, and Fox Sports. Google Cloud and Oracle availability is expected by Q4 2026.

How long does Microsoft's IP license to OpenAI technology last?

Microsoft retains a non-exclusive license to OpenAI intellectual property — covering frontier models and product implementations — through 2032. The license was previously exclusive; the amendment converts it to non-exclusive while extending the duration.

How long does the revenue share between OpenAI and Microsoft continue?

OpenAI's revenue-share payments to Microsoft continue through 2030 under a total cap. The cap dollar value has not been publicly disclosed, but analysts converge on the inference that the cap is bounded by Microsoft's existing equity position in OpenAI rather than by an open-ended financial milestone. Microsoft no longer pays revenue share back to OpenAI as it had under the previous structure.

Does Azure still get OpenAI products first?

Yes. The amendment preserves Microsoft's "first launch" rights on Azure. OpenAI products will ship first on Azure unless Microsoft "cannot and chooses not to support the necessary capabilities." The carve-out is narrow but real, allowing OpenAI to launch first on other clouds for specialized scenarios where Azure lacks the required compute footprint, regulatory posture, or geographic presence.

What is the "lock-in to leverage" framework that defines the amendment?

The framework, articulated in the Fifthrow strategic analysis, describes the shift from a market in which OpenAI workloads were exclusive to Azure (lock-in) to a market in which the same workloads are available across multiple clouds (leverage). The leverage is exercised through multi-cloud RFPs, cross-cloud benchmarking, migration clauses, and SLA audit rights — procurement tools that were structurally impossible under the previous exclusive arrangement.

What is Microsoft's equity position in OpenAI after the amendment?

Microsoft continues to participate as a major shareholder. Public reporting places Microsoft's stake at approximately 27 percent, valued at around $135 billion at the most recent disclosure. The equity position is the primary mechanism by which Microsoft retains economic upside in OpenAI's growth after the capped revenue share ends in 2030.

How does the amendment relate to the Musk v. Altman trial?

The amendment was announced on April 27, 2026, four days before the Musk v. Altman trial opened on May 1. Trial discovery surfaced an April 2022 internal Microsoft strategy memo in which Satya Nadella documented his concern that Microsoft was at risk of becoming "the next IBM" through its OpenAI dependency. The amendment is structurally independent of the trial verdict, but the trial record makes the amendment readable as Microsoft's formal exit from a structural risk that Nadella had internally diagnosed four years earlier.

What documented enterprise savings have emerged from the amendment?

The most-cited early case is Redress Compliance, which achieved over $5.2 million in cost avoidance on a single multi-cloud OpenAI procurement structured in the weeks after the amendment. The savings came from leveraging cross-cloud pricing competition during contract negotiation, not from operational efficiency gains post-deployment. The savings are documented in the Fifthrow strategic analysis.

What should enterprise IT teams do in response to the amendment?

Five concrete actions: audit current OpenAI workload inventory and Azure integration depth; benchmark independently across candidate clouds since no enterprise-ready cross-cloud dashboard exists yet; deploy real-time governance tooling for continuous SLA and cost tracking; establish cross-functional procurement teams spanning IT, legal, compliance, and procurement; and plan for the 2030 revenue-share cap expiration with explicit renegotiation triggers in multi-year contracts.

What "soft lock-ins" persist despite the structural multi-cloud unlock?

Azure retains advantages that the amendment does not touch: deep managed service integrations (Cognitive Services, Microsoft Fabric, Sentinel), exclusive early access to new model generations through the first-launch provision until 2032, feature and version lag on competing platforms during rollout windows, and cloud-specific agent and orchestration toolchains. Enterprises that need the latest OpenAI capabilities the day they ship will stay on Azure; enterprises prioritizing cost, governance flexibility, and vendor consolidation will move workloads to AWS as Bedrock catches up on feature parity.

Does the amendment affect the Microsoft Copilot business?

No, directly. Microsoft Copilot operates on Azure regardless of OpenAI's deployment surface elsewhere. Copilot crossed 20 million paying users with $37 billion ARR in May 2026, with the Copilot Cowork frontier preview adding agentic task execution capabilities. Microsoft's Copilot integration surface, enterprise distribution motion, and M365 attach value remain Microsoft's regardless of whether OpenAI models also ship on AWS, Google Cloud, or Oracle. The amendment preserves Microsoft's strategic value extraction from the OpenAI relationship while removing the structural exclusivity risk.