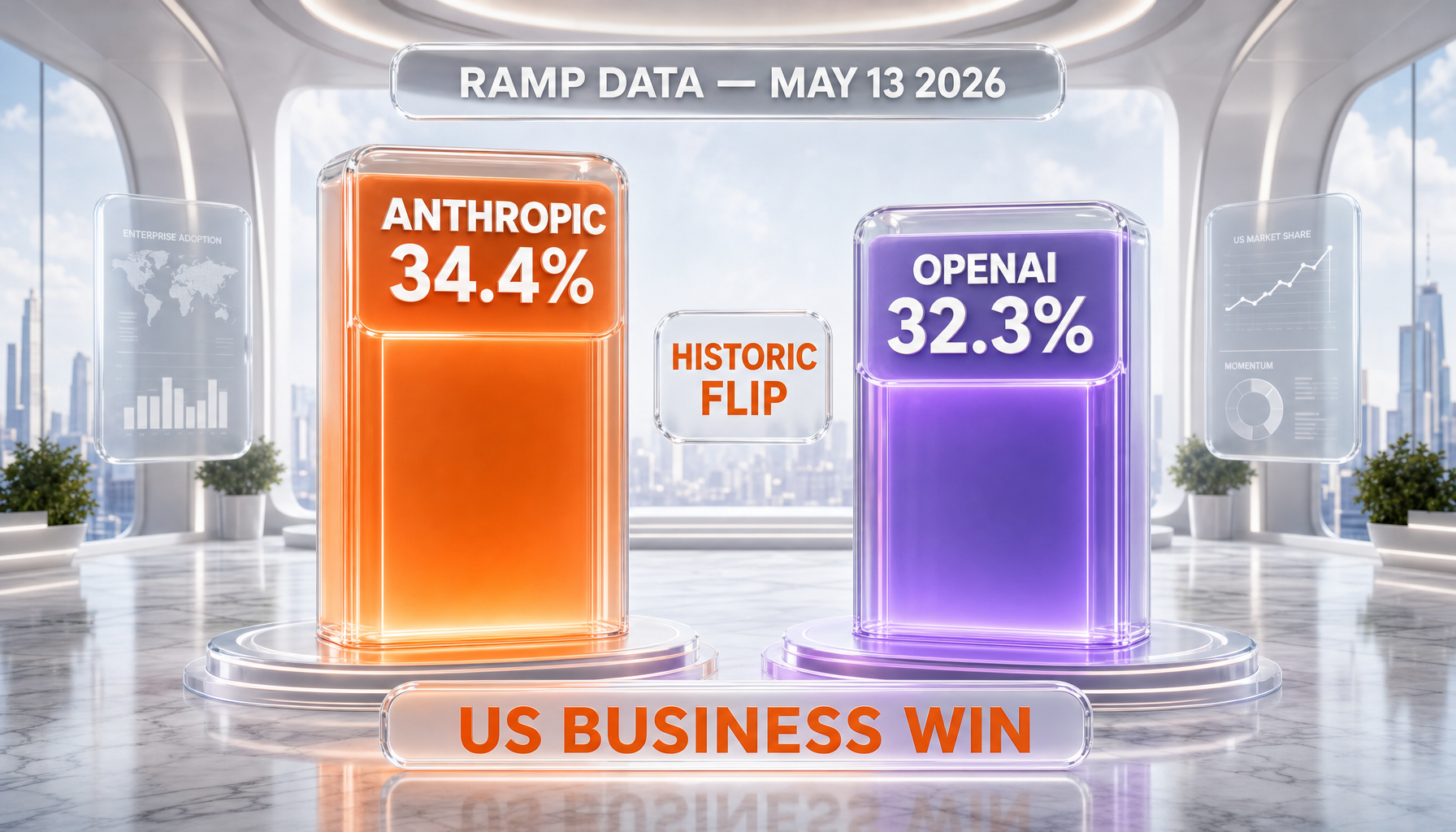

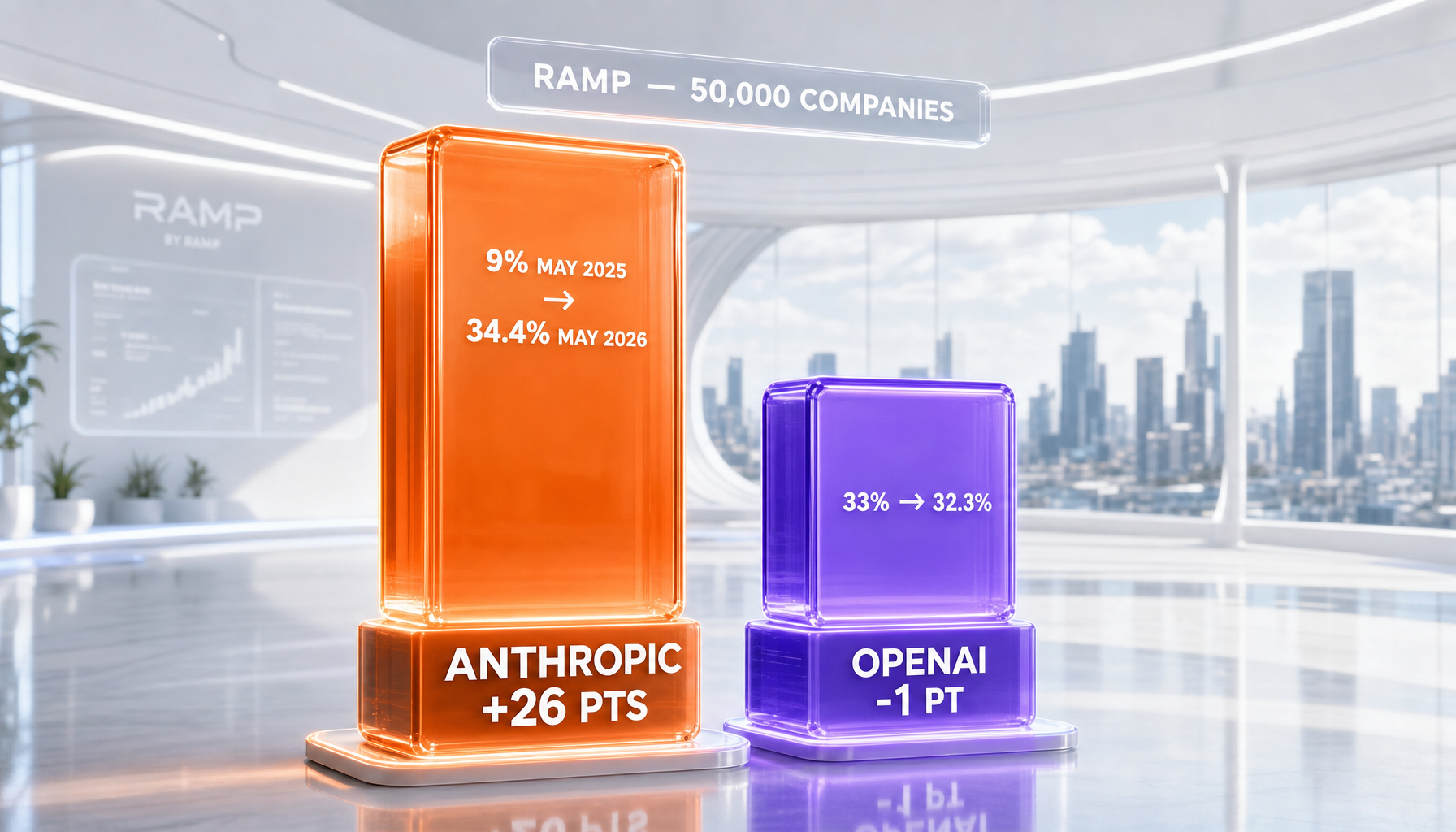

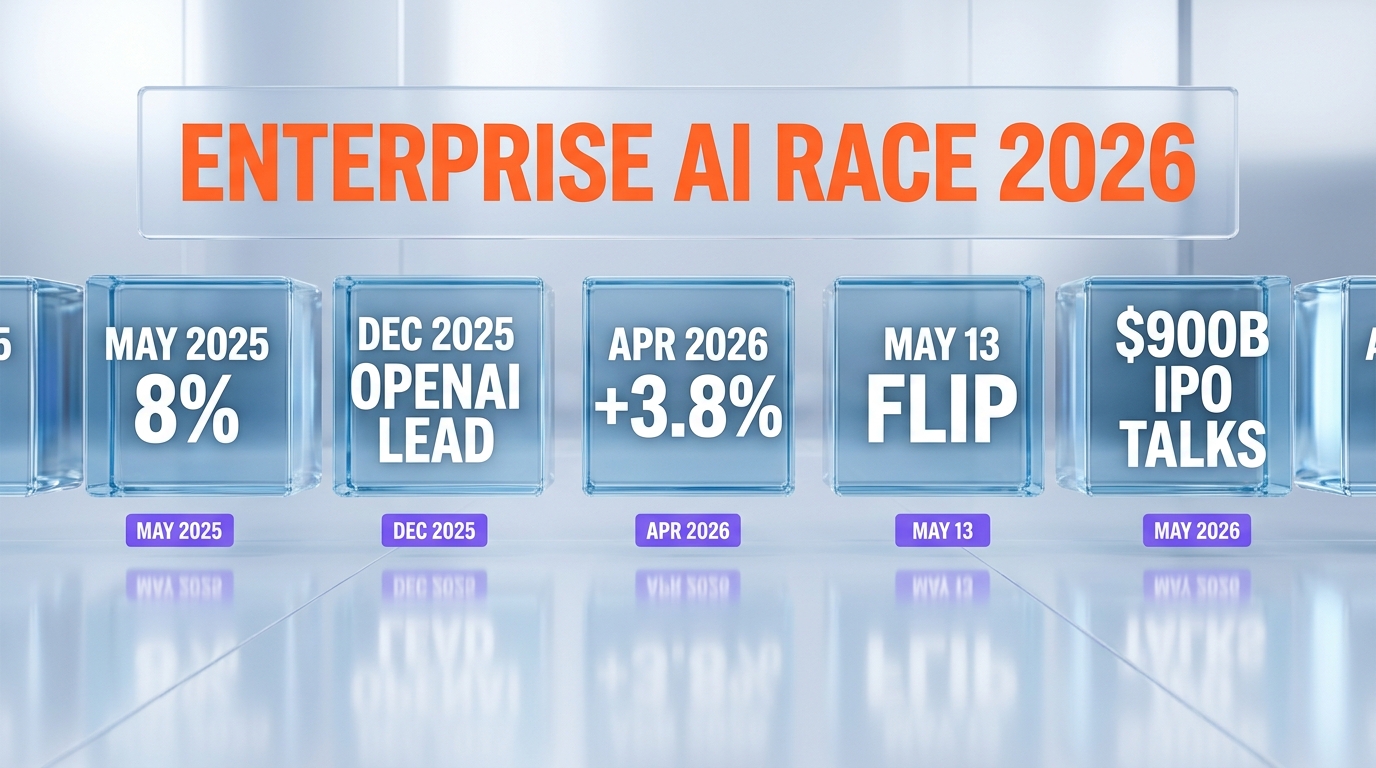

On May 13, 2026, Ramp — the corporate spend platform tracking expense data across roughly 50,000 US companies — published its monthly AI Index showing Anthropic at 34.4 percent of paying business customers versus OpenAI at 32.3 percent. This is the first time Anthropic has crossed OpenAI in US business adoption since the AI race began. In April 2025, Anthropic was under 8 percent. OpenAI sat near 33 percent. Over twelve months, Anthropic added 26 percentage points; OpenAI dropped 1. Ramp economist Ara Kharazian credits Anthropic's strength in finance, technology, and professional services first — then expansion through tools like Cowork. The underlying growth engine, in our reading, is Claude Code: CEO Dario Amodei told staff Anthropic saw 80 times growth per year in revenue and usage in Q1 2026 against a plan of 10 times. The flip is real. But VentureBeat's same-day analysis identified three threats — compute costs, cheap open-source inference, and OpenAI's Codex-plus-Deployment-Company counter-punch — that could erase the lead. This is the strategic anatomy of the May 13 flip and what we think happens next.

What Ramp Actually Published on May 13

Ramp's AI Index tracks expense-line items across the company's 50,000-plus customers — a sample heavily skewed toward US startups, growth-stage tech, professional services, and finance, but broad enough to be a useful proxy for the early-to-mid-adopter segment of US business AI spend. The May 2026 release moved the headline numbers as follows:

- Anthropic. 34.4 percent of participating businesses paying for the service in April 2026, up 3.8 percentage points month-over-month.

- OpenAI. 32.3 percent of participating businesses paying for the service in April 2026, down 2.9 percentage points month-over-month.

- Twelve-month delta. Anthropic moved from roughly 8 to 9 percent in April 2025 to 34.4 percent in April 2026 — a 26-percentage-point gain. OpenAI moved from roughly 33 percent to 32.3 percent over the same window.

- Overall AI category. Up 9 percent across all AI products in the period, so the flip is not a zero-sum reshuffle — the AI category is expanding while OpenAI's share specifically is compressing.

Three caveats matter before reading too much into the headline. First, Ramp's sample over-indexes on US startups and tech-forward mid-market companies; Fortune 500 procurement does not flow through Ramp the same way and shows different vendor distributions. Second, the metric is paying business customers — not revenue, not seats, not workloads. A 50-seat startup paying $20 per user counts the same in this index as a 50-seat startup paying $200 per user. Third, the underlying number is share of businesses, not share of inference. OpenAI may still be processing more total tokens; the question is who the buyer at the corporate card thinks of as the AI vendor of record.

The Kharazian quote that anchors the strategic story

Ramp economist Ara Kharazian framed Anthropic's gain as concentrated execution rather than broad demand expansion. The cohort breakdown he highlighted: Anthropic's adoption was strongest first in finance, then technology, then professional services. The expansion lever was Cowork — Anthropic's enterprise team-collaboration product for non-developer use cases — which carried Anthropic out of the developer ghetto and into the spreadsheet seats. Kharazian's published skepticism: he is not convinced the lead is durable, even while crediting the strategy execution over the past twelve months. That asymmetry — credit on execution, doubt on durability — is the analyst frame the entire VentureBeat threat piece picks up on.

The Anatomy of the Flip — How Anthropic Closed 26 Points in Twelve Months

A 26-point gain in twelve months is not normal in enterprise software. SaaS categories typically reshuffle by 3 to 5 points of market share per year at the leader level once a category matures past the early-adopter stage. The mechanic behind the Anthropic surge has three identifiable components.

Component one — Claude Code as the developer pull

Claude Code, Anthropic's command-line coding agent, did the work that historically takes a paid sales motion. Developer-led adoption created a bottom-up pull inside engineering teams that procurement could not block. By the time the procurement team noticed the Anthropic invoice line, the engineering team had already standardized on Claude for code review, refactoring, and CI failure triage. The same pattern that built GitHub inside Fortune 500 IT — quiet developer adoption, then a procurement conversation — is what Claude Code repeated across roughly fifty thousand Ramp-tracked companies in twelve months. We covered the strategic compute side of this in Anthropic's 10-Gigawatt Empire and the Coding Supremacy Bet.

Component two — Cowork as the non-developer expansion lever

Cowork is Anthropic's collaboration surface for non-developer team work — what most enterprise buyers think of when they think "ChatGPT for the office." Cowork shipped in late 2025 and reached enterprise general availability in Q1 2026. Kharazian credits Cowork as the lever that carried Anthropic out of the engineering-team beachhead and into finance, ops, and professional services seats. The structural read: developer adoption opens the door; Cowork takes the building.

Component three — Claude Opus 4 and 4.5 closing the model-quality gap

The model side mattered too, but only as a permission slip for the procurement story. Claude Opus 4 in mid-2025, then Claude 4.5 Sonnet and Opus 4.7 through Q1 2026, closed the perception gap that had previously let OpenAI win head-to-head bake-offs on raw benchmark scores. Once Claude was credibly inside the same quality tier — and ahead on long-context coding work — the procurement team had no model-quality reason to block the developer team's preference. The bake-off stopped being the bottleneck.

Component four — OpenAI's self-inflicted enterprise friction

OpenAI did not lose this on model quality. OpenAI lost it on enterprise posture. The 2025 board chaos, the consumer-product priority signaling, the late entry on Codex versus Anthropic's eighteen-month head start on Claude Code, the recent token-cost increase on image-bearing prompts that triples per-request economics — each of these gave the buyer side a reason to slow-walk OpenAI seat expansion while Anthropic line items climbed. None of these are fatal individually. Stacked over twelve months, they describe the 1-point share decline in the Ramp data.

Claude Code Is the Growth Engine — Eighty Times Revenue and Usage Growth

The fact that did the most damage to OpenAI's enterprise narrative in 2026 came from inside Anthropic. Per The Information's reporting on a leaked Anthropic all-hands, CEO Dario Amodei told staff that Q1 2026 saw 80 times growth per year in revenue and usage — when the operating plan had projected 10 times. An 80-times annualized growth rate inside a sub-$10 billion revenue company is the kind of number that flips fundraising rounds, pulls forward the IPO timeline, and — crucially for the Ramp data — pulls forward enterprise procurement decisions.

Why Claude Code monetizes better than chat

Claude Code's per-developer economics run higher than chat economics by roughly an order of magnitude. A developer running Claude Code on a real engineering workload burns through compute on long-context refactors, multi-file edits, and CI-loop triage. The pricing surface is built on token volume, the workloads are token-heavy, and the buyer — the engineering director with a $50,000 dev-tools budget — does not blink at $200 to $500 per developer per month if the agent ships measurable PR throughput.

For ChatGPT's enterprise plan, the comparable seat tops out around $25 to $60 per user per month. The arithmetic favors Anthropic at the unit-economic level: fewer seats, much higher revenue per seat, much lower churn because the developer is operationally dependent on the workflow. That is the structural reason a 26-point gain in business count over twelve months also translated into the 80-times revenue and usage growth Amodei cited. The seats are different seats.

The $900 billion valuation talk is downstream of this

Anthropic's reported $900 billion valuation conversations — which we covered in Anthropic Eyes $900B Valuation: 48-Hour Sprint Could Eclipse OpenAI — are not a vibe round. They are a math problem solved against an 80-times annualized growth rate on revenue that crossed into double-digit-billion territory in the first half of 2026. The Ramp data is one downstream signal of that growth rate. The valuation conversation is another. The two reinforce each other because the same enterprise procurement decisions that produce the Ramp share data also produce the contract revenue that supports the valuation math.

The Three Threats VentureBeat Flagged That Could Erase the Lead

VentureBeat's May 13 analysis was the most disciplined piece of skepticism published the same day as the flip. The piece names three threats. They are not equally weighted, but each one is structurally credible enough to belong in any honest write-up of the moment.

Threat one — compute cost and the image-token tripling

Anthropic shipped a model update that triples per-token cost on any prompt that includes an image. This is a small policy change with a large downstream effect: Cowork is image-heavy by design (screenshots, document images, dashboard exports), and the new pricing surface inflates the cost-per-task on exactly the workflows that drove Cowork's procurement-side traction in finance and operations seats. Coupled with Amodei's own framing of compute as the gating constraint on Anthropic's growth, the image-token increase reads as a forced trade-off — protecting margin on the inference layer at the cost of friction on the buyer side. A buyer that just signed a Cowork annual contract in Q4 2025 is now repricing the workload in Q2 2026.

The mitigation is structural, not tactical. Anthropic needs more compute, faster — which is what the 10-gigawatt compute build-out we covered is supposed to deliver over 24 to 36 months. In the meantime, the buyer has reasons to look at cheaper alternatives for image-heavy work.

Threat two — cheap open-source inference platforms taking the long tail

The fastest-growing AI vendors on Ramp's April 2026 data were not Anthropic and OpenAI. They were inference platforms — companies that host open-source models like Llama 4, Qwen 3, Mistral Large 3, and DeepSeek R3 on commodity infrastructure and undercut frontier-lab pricing by 60 to 80 percent on equivalent workloads. For the long tail of enterprise tasks — bulk classification, summarization, routine extraction — "good enough" beats "frontier" on the procurement math. The Anthropic-OpenAI duopoly captures the high-value reasoning surface; the open-source inference layer captures the volume.

The strategic risk to Anthropic is not that open-source replaces Claude on the reasoning workload. The risk is that procurement teams use the open-source inference line item as a wedge to renegotiate the Anthropic contract at renewal — "we have a workable second source on most of our workloads, so the Anthropic premium needs to compress." Switching costs on the reasoning workload are sunk, but contract-renewal pricing is not.

Threat three — OpenAI Codex plus the $4 billion Deployment Company JV

OpenAI's enterprise response shipped May 11, two days before the Ramp data flipped. We covered the structure in OpenAI Deployment Company: $4B JV, Big 4 Consulting and Tomoro Acquired. The structure: OpenAI plus Bain plus McKinsey plus Capgemini plus Tomoro (acquired) ships a services-led enterprise deployment motion designed to put GPT-5.5 and Codex inside Fortune 500 IT through trusted consulting channels.

Codex itself is the more direct threat. Codex is OpenAI's coding agent — late to market versus Claude Code by roughly eighteen months, but shipping inside a vendor with deeper enterprise distribution and the Deployment Company services arm behind it. If Codex closes the developer-experience gap with Claude Code in Q3 or Q4 2026, the bottom-up developer pull that drove the Ramp gains compresses. The compounding effect: developer mindshare flows back to OpenAI, procurement loses the reason to expand Anthropic seats, the Ramp index reverses by Q2 2027.

The Anthropic counter-counter is the SAP × Anthropic deal we covered in SAP Just Made Claude the Reasoning Brain of the Fortune 500 — putting Claude inside the F500 ERP application surface so the procurement decision is already made by the time Codex closes its gap. Speed matters here. Whoever locks in the application-surface position wins the next 24 months regardless of which coding agent ships better in Q4.

The Enterprise AI Race Map After May 13

The May 13 Ramp flip is not a standalone signal. It sits inside a sequence of enterprise wins that compound into Anthropic's strategic position for the rest of 2026. Reading the sequence chronologically clarifies the trajectory.

March 2026 — Anthropic for Legal launches

Anthropic shipped Claude for Legal — a verticalized configuration of Claude with workflows for contract review, deposition prep, and regulatory research — in March 2026. The launch put Anthropic on the buying menu inside law firms and corporate legal departments, two segments where AI vendor selection is unusually sticky because of confidentiality and privilege concerns.

April 2026 — Goldman, Blackstone, and the finance agents JV

The $1.5 billion Goldman plus Blackstone services JV wrapped Claude in a financial-services delivery vehicle aimed at the largest banks and asset managers. The structural read: Anthropic gets revenue without distribution cost, the JV gets product without R&D cost, and the F500 financial customer gets a managed-services wrapper that solves the procurement and compliance objections that previously slowed direct Anthropic adoption.

May 11, 2026 — Claude Platform on AWS GA

The same week the Ramp data flipped, Anthropic shipped Claude Platform on AWS to general availability. The platform bundles the Messages API, Managed Agents in beta, Skills, MCP connector, Files API, code execution, and prompt caching behind AWS IAM authentication and AWS Marketplace billing. For an AWS-anchored enterprise — which describes a meaningful slice of the Ramp sample — Claude is now buyable through the existing AWS contract without standing up a separate Anthropic relationship.

May 12, 2026 — SAP × Anthropic at Sapphire

The day before the Ramp flip published, SAP and Anthropic announced Claude as the primary reasoning layer across the SAP Business AI Platform — locking Claude into the application surface of roughly 440,000 enterprise customers globally, including most of the Fortune 500. Joule, SAP's AI assistant, and the 200-plus specialized Joule agents now run their reasoning loop on Claude. The competitive read: the F500 ERP floor is now Anthropic territory by default.

May 13, 2026 — Ramp flips the leaderboard

Ramp publishes the AI Index. Anthropic 34.4 percent. OpenAI 32.3 percent. First flip since the race began. The data captures activity through April, so the SAP and AWS announcements landed too late to drive the April numbers — meaning the flip is the leading indicator, and SAP plus AWS plus the $900 billion valuation conversation are the lagging compounders that should accelerate the trajectory in the May and June Ramp releases.

How to Read This If You Are a Buyer

For enterprise buyers running an AI vendor selection or renewal in Q2 to Q3 2026, the May 13 flip changes the negotiating frame. Here is the practical read.

If you are already on OpenAI

The Ramp data is not a reason to migrate. It is a reason to negotiate. OpenAI's enterprise team is fully aware of the share-loss narrative and has unusual pricing flexibility this quarter as a result. If your contract renewal lands between June and December 2026, the leverage is materially better than it was six months ago. The line to use: "we are evaluating Claude Code for our engineering org and Cowork for cross-functional teams — what makes the OpenAI footprint defensible at renewal?"

If you are evaluating fresh

The default starting position for new AI procurement in mid-2026 should be a side-by-side Claude versus ChatGPT evaluation, not a single-vendor RFP. The Ramp flip means both vendors will compete hard on price and contract terms. The bake-off matters less for model quality (the gap has compressed) and more for vendor posture, integration depth, and the renewal-cycle pricing track record. Build the second-source clause into the first contract.

If you are already Anthropic-anchored

Build the contingency plan now. The three threats VentureBeat flagged are real, and the renewal-cycle pricing risk on a Claude-anchored architecture is the same concentration-risk pattern Forrester warned about for the SAP customers. Document the second-source path for your top three workloads — one open-source inference candidate, one OpenAI candidate, one Cohere or Mistral candidate. You probably will not use it. But the existence of the documented second-source path is what gives you pricing leverage at the 2027 renewal.

What We Think Happens Next

Three predictions, weighted by confidence, on what the next six months produce.

Prediction one — the flip holds through summer 2026

High confidence. The May 13 Ramp data reflects April activity. SAP × Anthropic and Claude Platform on AWS land in the May and June indices. The compounding effect of those two announcements alone should add another 2 to 4 percentage points to Anthropic's Ramp share by August 2026. OpenAI's Codex catch-up and the Deployment Company JV mature on a slower timeline — Q3 to Q4 2026 — so the share gap likely widens before it narrows.

Prediction two — Codex applies real pressure starting Q4 2026

Medium confidence. OpenAI's Codex has the developer-experience gap to close, but the company has the engineering bench to close it. By Q4 2026 we expect Codex to be credibly within striking distance of Claude Code on the workflows that matter — long-context refactors, CI failure triage, multi-file edits. The first market signal will be on GitHub Copilot's renewal cycle inside Fortune 500 IT shops. If Copilot retention holds in Q4, the Anthropic narrative has a structural counter to manage.

Prediction three — Anthropic's IPO timeline pulls forward to 2027

Medium-to-high confidence. The combination of 80-times revenue and usage growth, the SAP application-surface lock-in, the AWS distribution surface, and the May 13 Ramp data flip together fix the IPO narrative. Anthropic does not need a 2028 timeline; the financial profile supports a 2027 listing. The $900 billion valuation conversation is the marker. The IPO would be the largest tech listing in history if priced inside the rumored range. The Ramp data is part of the storyboard the investment bankers will show in the roadshow deck.

Bottom Line

The May 13 Ramp flip is the cleanest single signal we have seen in 2026 that the enterprise AI race has structurally inverted. Anthropic 34.4 percent versus OpenAI 32.3 percent is the headline; the 80-times revenue and usage growth on the operational side is the math underneath; the SAP plus AWS plus $900 billion valuation conversation set is the compounding flywheel. The three VentureBeat threats are real and worth taking seriously, but each of them has a defensible counter — and the Ramp data captures only the leading edge of a story whose compounders are still ramping.

If you are building, buying, or financing AI infrastructure today, the May 13 print is the moment to reprice the enterprise vendor question from "OpenAI by default" to "Anthropic by default, OpenAI on the second source." Whether that frame holds at the 2027 renewal cycle depends on Codex, on compute economics, and on whether Anthropic can keep the operational discipline that produced the past twelve months of execution. The strategic burden of proof, for the first time, sits on OpenAI to take the lead back.

Frequently Asked Questions

What exactly did Ramp report on May 13, 2026?

Ramp's May 2026 AI Index reported that 34.4 percent of paying business customers on its platform were buying from Anthropic in April 2026, versus 32.3 percent buying from OpenAI. This is the first time Anthropic has been ahead of OpenAI in US business adoption since the AI race began. The data set covers roughly 50,000 US companies on Ramp's corporate spend platform, weighted toward startups, growth-stage tech, finance, and professional services. Anthropic rose 3.8 percentage points month-over-month while OpenAI fell 2.9 points.

How big a deal is the Ramp flip in twelve-month context?

In April 2025, Anthropic sat below 9 percent of paying businesses on the Ramp index. OpenAI sat near 33 percent. Over the twelve months to April 2026, Anthropic added 26 percentage points; OpenAI dropped 1. A 26-point share gain in twelve months is unusual at the leader level of any mature SaaS category. The structural read is that Anthropic compounded developer adoption via Claude Code into procurement decisions via Cowork at a faster rate than OpenAI compounded ChatGPT consumer momentum into enterprise seat expansion.

Is Ramp data a reliable proxy for the broader US business AI market?

Partially. Ramp's customer base over-indexes on US startups, growth-stage tech companies, finance, and professional services. Fortune 500 procurement does not flow through Ramp the same way and shows different vendor distributions; large enterprises still buy meaningful OpenAI capacity through Microsoft Azure that does not appear on Ramp at all. The Ramp index is best read as the early-to-mid-adopter leading indicator, not the entire market. The fact that the leading indicator just flipped is the strategic news.

What role does Claude Code play in the Anthropic surge?

Claude Code is the bottom-up developer pull that drove the Anthropic line item onto procurement spreadsheets without requiring a top-down sales motion. Developer-led adoption inside engineering teams created seat expansion and budget normalization that procurement could not easily reverse. CEO Dario Amodei told Anthropic staff that Q1 2026 saw 80 times growth per year in revenue and usage against a 10-times plan — a growth rate that maps cleanly onto the Ramp share trajectory, since Claude Code's per-seat economics run roughly an order of magnitude above ChatGPT enterprise pricing.

What are the three threats VentureBeat identified to Anthropic's lead?

First, compute cost and the recent model update that triples per-token cost on prompts containing images — a friction point on Cowork's image-heavy workflows. Second, cheap open-source inference platforms hosting Llama, Qwen, Mistral, and DeepSeek that capture the long-tail enterprise workloads at 60 to 80 percent below frontier pricing and become a renewal-cycle pricing wedge. Third, OpenAI's Codex catching up to Claude Code's developer experience plus the $4 billion Deployment Company JV with Bain, McKinsey, Capgemini, and the acquired Tomoro shipping a services-led enterprise counter-attack.

How does the flip connect to Anthropic's reported $900 billion valuation talk?

The Ramp share data and the valuation conversation are different lenses on the same underlying growth. The Ramp index measures share of paying businesses; the valuation conversation prices the revenue compounding from those businesses. Anthropic's 80-times annualized revenue and usage growth in Q1 2026 supports a math case for a $900 billion valuation that did not exist twelve months earlier. The May 13 Ramp flip is one of the public signals investment bankers will use in the IPO roadshow deck if Anthropic pulls the listing forward into 2027.

What does the SAP × Anthropic deal mean for the Ramp trajectory?

The SAP × Anthropic Sapphire announcement on May 12 puts Claude inside the application surface of roughly 440,000 enterprise customers globally, including most of the Fortune 500. The Ramp data only captured activity through April, so SAP's footprint had not yet landed in the May 13 print. The compounding effect should appear in the June and July Ramp releases — adding 2 to 4 percentage points to Anthropic's share over the summer if our model holds. The strategic read: SAP plus AWS plus Cowork plus Claude Code form a four-surface enterprise capture that did not exist a year ago.

What is OpenAI doing to respond to the flip?

OpenAI shipped the Deployment Company joint venture with Bain, McKinsey, Capgemini, and the acquired Tomoro on May 11 — two days before the Ramp data flipped. The structure is services-led: Big Four consulting firms package GPT-5.5 and Codex into Fortune 500 IT deployments through trusted consulting channels. The Codex coding agent is the more direct competitive response to Claude Code, but Codex remains roughly eighteen months behind Claude Code on developer experience. The catch-up timeline is Q3 to Q4 2026 in our reading.

How should enterprise buyers read the May 13 flip?

If you are already on OpenAI, use the Ramp data as renewal-cycle leverage rather than as a migration trigger — OpenAI's enterprise team has unusual pricing flexibility this quarter. If you are evaluating fresh, run a side-by-side Claude versus ChatGPT bake-off and build a second-source clause into the first contract. If you are already Anthropic-anchored, document a second-source path for your top three workloads now, before the 2027 renewal cycle when concentration-risk leverage shifts back toward the vendor.

What is Cowork and why does it matter for the flip?

Cowork is Anthropic's collaboration product for non-developer team work — finance, operations, professional services seats that previously sat outside Anthropic's developer-led footprint. Cowork reached enterprise general availability in Q1 2026 and is the lever Ramp economist Ara Kharazian credited for Anthropic's expansion beyond the engineering beachhead. Without Cowork, Claude Code would have anchored a developer-only revenue base. With Cowork, the same Anthropic relationship expands into the seats that historically defined ChatGPT enterprise growth.

Is the Ramp flip durable or a one-month anomaly?

Our reading is that the flip holds through summer 2026 with high confidence, widens through Q3 as SAP and AWS compounders land in the index, and becomes contested again in Q4 2026 as Codex closes its developer-experience gap. Ramp economist Kharazian was openly skeptical about durability on the day of publication — that skepticism is honest analyst caution given the threat triangle. Our base case is that the May 13 print is the leading edge of a multi-quarter trend rather than a one-month anomaly, but the durability question reopens at the next renewal cycle in 2027.

Sources

- TechCrunch — Anthropic now has more business customers than OpenAI, according to Ramp data (May 13, 2026)

- VentureBeat — Anthropic finally beat OpenAI in business AI adoption — but 3 big threats could erase its lead (May 13, 2026)

- Ramp AI Index — May 2026 release

- SAP News Center — SAP and Anthropic Plan to Bring Claude to SAP Business AI Platform (May 12, 2026)

- AWS Machine Learning Blog — Introducing Claude Platform on AWS (May 12, 2026)