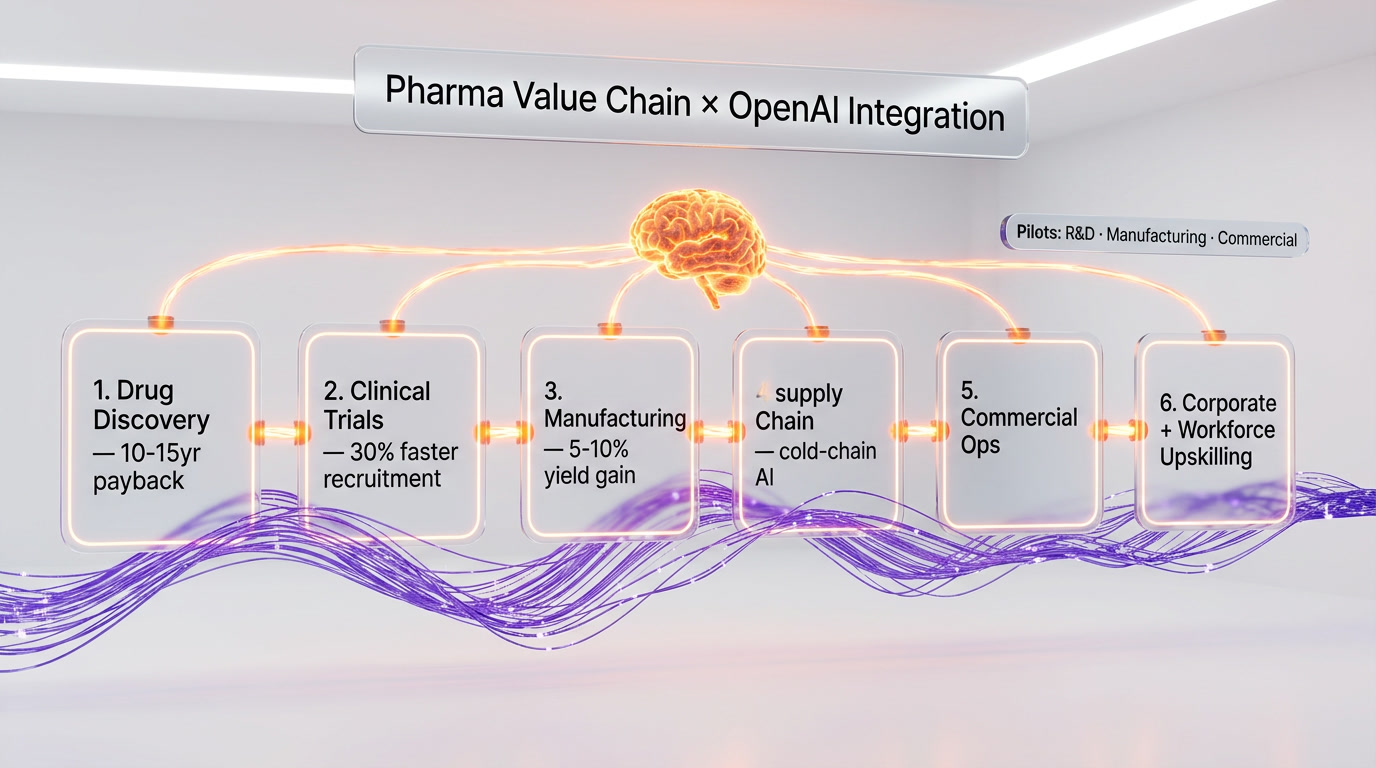

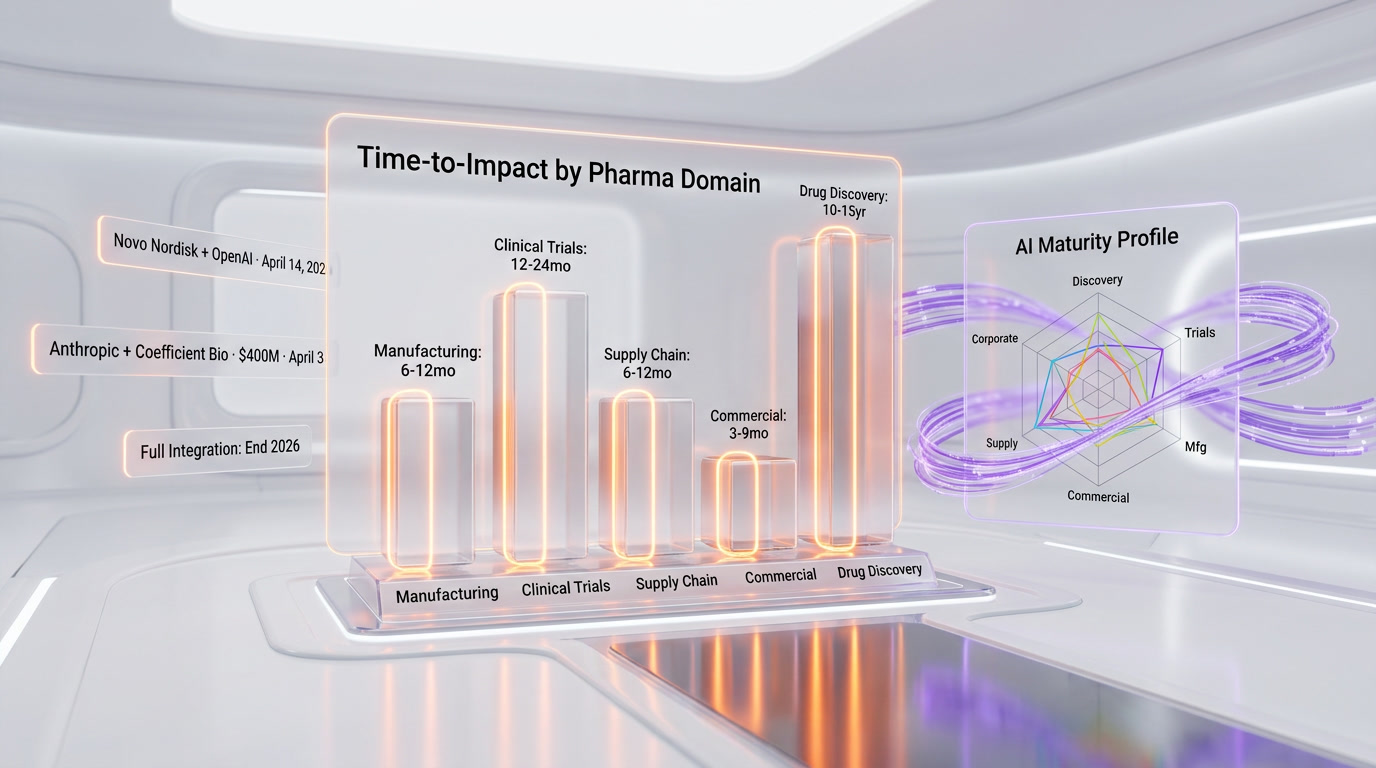

On April 14, 2026, Novo Nordisk — the world's largest pharmaceutical company by market capitalization and the maker of Ozempic and Wegovy — announced a strategic partnership with OpenAI to integrate AI across every layer of its pharmaceutical business: drug discovery, clinical trials, manufacturing, supply chain, commercial operations, and corporate functions. Pilot programs are launching across R&D, manufacturing, and commercial divisions, with full integration targeted for end of 2026. OpenAI will also lead workforce upskilling and AI literacy programs across Novo Nordisk's global organization. Eleven days earlier, on April 3, 2026, Anthropic acquired Coefficient Bio for $400 million. Two frontier labs. Two pharma bets. One defining month for AI inside drug discovery.

This is a catch-up analysis on a story we did not cover when it broke. We are publishing it now because the strategic shape of 2026 has clarified — and the Novo Nordisk move is a structural data point inside our 3-track market thesis on OpenAI's enterprise super-app expansion. The partnership is not just another pharma + AI press release. It is the largest pharma company on the planet handing OpenAI the entire value chain, from molecule identification to corporate operations, with a workforce-wide AI literacy mandate attached.

What Novo Nordisk Just Handed OpenAI

The announcement on April 14, 2026 is not framed as a procurement deal. It is framed as a strategic partnership covering six operational domains: drug discovery and candidate identification, clinical trials and research operations, manufacturing and supply chain efficiency, distribution and corporate operations, commercial operations, and global workforce upskilling. Pilot programs are commencing across R&D, manufacturing, and commercial divisions. Full integration is targeted for end of 2026 — roughly an eight-month runway from announcement to enterprise-wide deployment.

Novo Nordisk CEO Mike Doustdar framed the rationale in the joint announcement: "Integrating AI in our everyday work gives us the ability to analyse datasets at a scale that was previously impossible." OpenAI CEO Sam Altman framed the partnership outcome: "This collaboration with Novo Nordisk will help them accelerate scientific discovery, run smarter global operations." The capability stack OpenAI is bringing in is the standard frontier model surface — large-scale dataset analysis, pattern recognition across heterogeneous data, hypothesis acceleration, and operational copilot integration — wired into Novo Nordisk's existing data infrastructure under what the announcement describes as "strict data protection, governance and human oversight."

The market context matters here. Novo Nordisk is not a typical pharma customer. It is the largest pharmaceutical company in the world by market capitalization, the maker of the GLP-1 obesity and diabetes franchise that has redefined chronic disease economics, and a Danish public company with deep European institutional credibility. When OpenAI signs Novo Nordisk for a six-domain integration, the signal to the rest of the pharma industry is not "OpenAI is exploring healthcare." It is "OpenAI just became a default pharma AI substrate, and your board will ask why you have not signed."

Pharma Value Chain: Where AI Sits In Six Stages

The default narrative on AI in pharma focuses on drug discovery — molecule generation, target identification, lead optimization. That is the photogenic part of the value chain. It is also the part with the longest payback horizon, because pharma R&D cycles run 10 to 15 years from candidate identification to approved drug. The Novo Nordisk deal is structurally interesting because it covers six stages, not one. Each stage has a different AI maturity profile and a different time-to-impact curve.

Stage 1 — Drug Discovery

The high-visibility, long-payback stage. AI here is supposed to accelerate target identification, generate candidate molecules, predict binding affinity, and triage compound libraries. The honest read is that no AI-discovered drug has yet completed a full Phase 3 to approval — every announcement to date is a candidate at some earlier stage. The Novo Nordisk + OpenAI work here will likely produce qualitative wins on early-stage triage and hypothesis generation, not a 2027 approved drug.

Stage 2 — Clinical Trials

This is where AI has shorter-horizon, measurable wins. Trial design optimization, patient recruitment matching, real-time safety signal detection, and protocol amendment modeling are tractable today. A trial that recruits 30 percent faster or detects a safety signal six months earlier is worth substantial money on Novo Nordisk's R&D budget. The OpenAI partnership lists clinical trials inside scope, but the announcement language does not commit to a specific use case here. Expect this to be one of the first domains where pilots show measurable throughput gains.

Stage 3 — Manufacturing

Pharma manufacturing is process-heavy, regulated, and unforgiving. Novo Nordisk's GLP-1 manufacturing capacity has been a public bottleneck on global Wegovy and Ozempic supply since 2024. AI applied to manufacturing means predictive maintenance, yield optimization, batch deviation prediction, and supply-side simulation. The announcement explicitly names manufacturing as a pilot domain. The strategic stake is that Novo Nordisk has spent billions of dollars on fill-finish capacity expansion. Squeezing five to ten percent additional yield out of existing capacity through AI is direct revenue.

Stage 4 — Supply Chain

Cold-chain logistics, demand forecasting, distribution routing, and inventory placement. This is the operational AI playbook the Microsoft 365 Copilot generation already understands. Plugging OpenAI capabilities into Novo Nordisk's supply chain means demand-sensing models that adjust faster to regional uptake, distribution-routing models that optimize across pharmacy networks, and inventory-placement models that reduce stockouts in high-demand geographies. Lower-glamour than drug discovery. Higher near-term cash impact.

Stage 5 — Commercial Operations

Sales enablement, medical-affairs content, market access submissions, payer negotiation modeling, healthcare-professional (HCP) engagement personalization. This is the domain where general-purpose frontier LLMs are most directly substitutable for traditional pharma-tech vendors. Veeva and IQVIA build deep verticalized stacks here; OpenAI is bringing a horizontal substrate that Novo Nordisk's internal teams can build on. Pilot programs are explicitly running in commercial — expect measurable wins on content velocity and HCP-engagement personalization within the eight-month window.

Stage 6 — Corporate Functions

Finance, HR, legal, procurement, internal IT. The lowest-hanging fruit and the part where workforce upskilling matters most. The announcement explicitly states that OpenAI will assist with global workforce upskilling and AI literacy. This is the Microsoft 365 Copilot rollout pattern applied to a 64,000-person pharma organization. The wins here are unglamorous but compound — meeting summarization, drafting assistance, document search, expense workflow automation. They also give the C-suite the politically necessary headline of "AI deployed across the company" without needing a Phase 3 readout to justify the investment.

Anthropic Coefficient Bio vs OpenAI Novo Nordisk: Two Pharma Bets, Two Strategies

The clearest way to read the Novo Nordisk + OpenAI deal is against the Anthropic + Coefficient Bio acquisition that landed eleven days earlier on April 3, 2026. Same month. Same vertical. Two completely different strategies.

Anthropic acquired Coefficient Bio for $400 million: fewer than 10 researchers, zero revenue, an 8-month-old company. The bet is upstream — Anthropic is buying a small, deeply-credentialed scientific research team and integrating them into Claude development. The thesis is that frontier AI for biology needs in-house biological expertise to advance the model itself. The acquisition is about model capability, not market access.

OpenAI partnered with Novo Nordisk: 64,000 employees, $40+ billion in revenue, the world's largest pharma company by market capitalization. The bet is downstream — OpenAI is selling the existing frontier capability stack into the largest possible pharma deployment surface. The thesis is that frontier AI for pharma needs the largest possible distribution footprint to lock in vertical incumbency. The partnership is about market access, not model capability.

Both bets can be right. They are not zero-sum. But they tell you something durable about how the two labs are thinking about the pharma vertical:

- Anthropic plays for model depth. Acquire scientific expertise, fold it into Claude development, build defensible AI-for-biology capability. The Coefficient team is now inside Anthropic — they ship into Claude, not into the open market. The customer in this model is, ultimately, every Anthropic API caller working in biology.

- OpenAI plays for market distribution. Sign the largest enterprise integration, scale the capability surface across six operational domains, use Novo Nordisk as the gravitational center that pulls other pharma customers into the same architecture. The customer is Novo Nordisk specifically, but the reference deal is for every other top-20 pharma board.

Strategically, this is the same pattern we have seen across other verticals. Anthropic's Wall Street deployment with Citadel, BNY, and Carlyle is depth — agentic capabilities tuned to financial workflows. OpenAI tends to scale horizontally — generic frontier capability deployed broadly. Pharma in April 2026 is the cleanest side-by-side instance of these two strategies meeting in the same month, in the same vertical.

One observation that matters for our editorial read: Novo Nordisk did not pick Anthropic. The world's largest pharma had every option on the table and signed with OpenAI. That choice is data. It suggests that for an enterprise of Novo Nordisk's scale, the operational breadth of OpenAI's capability stack — and the workforce-upskilling component — was more compelling than the depth-first capability story Anthropic is building. We will be watching closely whether Roche, Pfizer, Merck, AstraZeneca, and the rest of the top 20 follow Novo Nordisk's signal or hedge with both labs.

OpenAI's Enterprise Vertical Map: Becoming A Horizontal Platform

Zoom out from pharma. The Novo Nordisk deal is the latest data point in a sequence of OpenAI enterprise vertical announcements across 2026:

- Microsoft 365 Copilot — the foundational horizontal deployment surface across the existing enterprise productivity base.

- Sierra and the finance enablement layer — agentic deployment into customer support and customer operations, scaling laterally toward financial services.

- Novo Nordisk and pharma vertical — April 14, 2026, the six-domain pharma integration analyzed in this article.

- EU Cyber Action Plan and GPT-5.5-Cyber — May 11, 2026, sovereign-grade defensive AI access for European cybersecurity teams, governments, and EU institutions.

- ServiceNow integration — agentic deployment inside the enterprise workflow stack.

- GPT-5.5 super-app strategy — April 23, 2026 launch, the consumer-facing super-app that gives OpenAI a direct consumer surface to anchor the enterprise stack.

The shape of this map is not a single vertical specialist. It is a horizontal enterprise platform play. OpenAI is building the substrate that sits under pharma operations, finance operations, government cyber, EU sovereign workflows, and the consumer super-app — all on the same model family. The Novo Nordisk deal is the most operationally aggressive version of this pattern we have seen in 2026, because the six-domain scope means OpenAI is not just an API vendor inside one team. It is a workforce-wide capability layer with explicit upskilling commitments.

If you are building the mental model of where OpenAI sits in 2026 enterprise software, the right metaphor is not "the AI lab that ships ChatGPT." The right metaphor is "the AI lab that is becoming SAP, with consumer ChatGPT as the front door." The Novo Nordisk integration is, in that frame, a $40+ billion revenue customer signing onto the SAP-like substrate for the entire pharma operational stack.

Workforce Upskilling: The Quiet Part Of The Deal

The announcement language is precise on one detail that most coverage skipped over. OpenAI is not just deploying capabilities. OpenAI is "assisting with global workforce upskilling and AI literacy." Translated: OpenAI is the default AI competency standard inside Novo Nordisk, taught by OpenAI-led programs, anchored on OpenAI tooling.

This is the same playbook Anthropic ran with EPAM. In May 2026, EPAM committed to training 10,000 architects as Claude-certified, which we analyzed as Anthropic locking in the consulting industry's reference architecture. The OpenAI + Novo Nordisk version is structurally the same move on the customer side rather than the consulting side. When 64,000 Novo Nordisk employees learn AI on OpenAI tooling, OpenAI becomes the muscle memory of the largest pharma workforce on Earth. Replacing OpenAI two years from now is not a procurement decision. It is a retraining decision.

The same dynamic is playing out at Anthropic + NEC in Japan, where Anthropic is wiring Claude into the engineering practices of 30,000 NEC employees as the first global AI-native engineering partnership. The frontier labs are not just selling models — they are competing for the right to be the default AI literacy standard inside the largest enterprise workforces. Novo Nordisk's 64,000-person workforce is, on that scoreboard, one of the biggest individual prizes available in the pharma vertical.

What Would Prove This Overhyped

The case for this deal being structurally important is the case I have made above. The honest counter-case is worth sitting with, because pharma is the industry where AI hype meets the hardest empirical reality on Earth — clinical trials.

Three failure modes would suggest the Novo Nordisk + OpenAI deal is more press release than pipeline transformation:

- Pilot programs produce only marginal gains. If the R&D, manufacturing, and commercial pilots end the year reporting single-digit percentage improvements on standard KPIs, this becomes a workforce-productivity story rather than a pharma-transformation story. That outcome is the base-rate expectation for first-year enterprise AI deployments and would not be a scandal — but it would deflate the "AI changes drug discovery" framing.

- Drug discovery wins do not materialize in the 2026-2028 window. Pharma R&D cycles are structurally 10 to 15 years from molecule to approved drug. No AI-discovered drug has yet completed Phase 3 to approval. If the partnership cannot point to an AI-accelerated candidate moving through Phase 2 by end of 2027, the discovery thesis remains unproven.

- Manufacturing and supply chain gains are smaller than capacity expansion. Novo Nordisk has been pouring billions of dollars into fill-finish manufacturing capacity. If brute-force capacity expansion delivers more incremental output than AI-driven yield optimization, the AI manufacturing thesis becomes a footnote rather than a centerpiece.

What would prove the bullish case? An AI-accelerated GLP-1 follow-on candidate entering trials by mid-2027, a documented manufacturing yield improvement above five percent in the existing fill-finish footprint, or a measurable shift in Novo Nordisk's R&D cost-per-candidate-progressed metric. Any one of those would convert the deal from "horizontal enterprise platform expansion" to "AI structurally changed pharma economics."

Why Novo Nordisk Picked OpenAI, Not Anthropic

This is the question worth sitting with longest, because it has implications across the entire 2026 frontier lab competitive map. Novo Nordisk could have signed with either lab. The world's largest pharma has buyer power, regulatory sophistication, and zero need to take the first available offer. The choice landing on OpenAI is informative.

The most likely reasons, in plausibility order:

- Operational breadth fits OpenAI's deployment shape better than Anthropic's. The six-domain integration spans drug discovery (capability-heavy) through corporate functions (productivity-heavy). OpenAI's stack — including the Microsoft 365 Copilot integration footprint — is built for that horizontal sweep. Anthropic — the lab behind Claude — is still narrower in horizontal enterprise tooling in 2026.

- Workforce upskilling at 64,000-employee scale needs the consumer surface. ChatGPT is the AI tool most of Novo Nordisk's workforce already uses informally. Building the official AI literacy curriculum on the tool employees already know is structurally easier than rolling out a Claude-first program. Anthropic's consumer footprint, as we have analyzed, lags OpenAI's by a meaningful margin in 2026.

- Sam Altman's enterprise sales motion is the most aggressive in the industry. The frequency, scale, and political-grade quality of OpenAI's 2026 enterprise deal flow — Novo Nordisk, Microsoft 365, Sierra, EU Cyber Action Plan, ServiceNow — suggests OpenAI's enterprise organization is operating at higher cadence than Anthropic's. For a deal of this scope, sales execution likely mattered.

- Safety positioning was not the deciding factor. Anthropic's safety-first brand positioning is real and is a competitive moat in some buyer conversations. For a six-domain pharma deal where the workforce upskilling component is central, the buyer wanted breadth and deployment velocity more than safety theater. Both labs ship governance frameworks — Novo Nordisk's announcement specifically references "strict data protection, governance and human oversight" — so safety became a tie-stake, not a differentiator.

The competitive question for Anthropic out of this deal is whether the depth-first capability strategy is enough to win the next top-20 pharma deal, or whether OpenAI's six-domain breadth becomes the default reference architecture that compresses Anthropic's pharma TAM. The Coefficient Bio acquisition is the right move for the depth strategy. It is not, by itself, the answer to the breadth question.

Three-Track Market Thesis Update

For readers tracking our running 2026 market thesis, the Novo Nordisk + OpenAI deal sits on all three tracks simultaneously:

- Track 1 — OpenAI enterprise super-app expansion. Pharma is now an explicit vertical in the OpenAI enterprise map alongside finance (Sierra), government (EU Cyber Action Plan), and horizontal productivity (Microsoft 365). The shape is a horizontal enterprise platform, not a vertical specialist.

- Track 2 — Anthropic depth-versus-breadth positioning. Coefficient Bio is a depth bet. Novo Nordisk is the largest pharma signing with the competitor. The depth strategy will be tested directly by whether Anthropic wins any top-20 pharma deal of comparable scope in the next six quarters.

- Track 3 — Workforce upskilling as the structural moat. OpenAI is now the default AI literacy standard inside Microsoft 365 customers and inside Novo Nordisk's 64,000 employees. Anthropic is doing the same with EPAM consultants and NEC engineers. The "default AI competency standard" is becoming a measurable competitive metric.

If we get one prediction on the record for this analysis, it is this: by end of 2027, the strongest predictor of frontier-lab enterprise market share will not be model benchmark scores. It will be cumulative workforce-upskilled headcount inside Fortune 500 customers. On that scoreboard, the Novo Nordisk deal moves OpenAI's footprint forward by roughly 64,000 employees in a single signature.

What To Watch Next

Three signals will tell us whether the strategic shape implied by this deal holds:

- Which top-20 pharma signs next. Roche, Pfizer, Merck, AstraZeneca, Johnson & Johnson, AbbVie. If three of those six sign with OpenAI by end of 2026, the breadth strategy is the dominant pharma reference architecture. If three of those six split between OpenAI and Anthropic, the vertical remains contested.

- Whether Novo Nordisk publishes early pilot results. Pharma is press-release-shy on internal pilots. If we get a documented manufacturing yield or commercial productivity number from a Novo Nordisk + OpenAI pilot by end of Q3 2026, the deployment is real. If we get only end-of-year aggregate "AI is transformational" language, the deployment is more marketing than measurement.

- Whether Anthropic counters with its own large pharma signing. The Coefficient Bio acquisition is upstream of any enterprise pharma sale. A direct enterprise counter from Anthropic — analogous to Novo Nordisk in scope, even if smaller in revenue footprint — would prove the depth strategy can also win at distribution. No counter, or a smaller-than-Novo signing, suggests the breadth strategy is structurally winning the pharma vertical.

We will be tracking each of these signals through the rest of 2026. The Novo Nordisk + OpenAI deal is the largest pharma + frontier AI integration announced in the modern AI era. Whether it becomes the defining pharma deployment of the decade, or a well-marketed productivity rollout that delivers single-digit operational wins, will define how much of the rest of the industry follows the same template.

Frequently Asked Questions

What did Novo Nordisk and OpenAI announce on April 14, 2026?

Novo Nordisk and OpenAI announced a strategic partnership to integrate AI across the entire pharmaceutical value chain: drug discovery, clinical trials, manufacturing, supply chain, commercial operations, and corporate functions. Pilot programs are launching across R&D, manufacturing, and commercial divisions, with full integration targeted for end of 2026. OpenAI is also assisting with global workforce upskilling and AI literacy across Novo Nordisk's 64,000-employee organization.

Why is the Novo Nordisk + OpenAI deal strategically important?

Novo Nordisk is the world's largest pharmaceutical company by market capitalization and the maker of the GLP-1 obesity and diabetes franchise (Ozempic and Wegovy). When the largest pharma on Earth signs a six-domain integration with OpenAI, the deal sets a reference architecture other top-20 pharma companies will be asked to match. It also positions OpenAI as a horizontal enterprise platform across pharma, finance, government, and productivity verticals rather than a single-vertical specialist.

How does this compare to Anthropic's Coefficient Bio acquisition?

Anthropic acquired Coefficient Bio for $400 million on April 3, 2026 — a 9-person biotech research lab, zero revenue, 8 months old. The bet is upstream and depth-focused: acquire scientific expertise to advance Claude's biology capabilities. OpenAI's Novo Nordisk partnership is downstream and breadth-focused: deploy existing frontier capabilities into the largest possible pharma enterprise footprint. Different strategies, same vertical, same month.

What does OpenAI's workforce upskilling commitment mean?

OpenAI committed to leading AI literacy programs across Novo Nordisk's global workforce of approximately 64,000 employees. This makes OpenAI the default AI competency standard inside one of the world's largest pharma organizations, taught by OpenAI-led programs and anchored on OpenAI tooling. Replacing OpenAI two years from now becomes a retraining decision rather than a procurement decision — a structural moat similar to Anthropic's 10,000 Claude-certified architects program at EPAM.

When will the Novo Nordisk + OpenAI integration go live?

Pilot programs are launching in 2026 across research and development, manufacturing, and commercial divisions. Full integration is targeted for end of 2026, giving the partnership roughly an eight-month runway from the April 14 announcement to enterprise-wide deployment across drug discovery, clinical trials, manufacturing, supply chain, commercial operations, and corporate functions.

Will this partnership accelerate drug discovery in 2026?

Likely not in 2026, and probably not in 2027 either. Pharma R&D cycles run 10 to 15 years from candidate identification to approved drug, and no AI-discovered drug has yet completed Phase 3 to approval. Realistic 2026 wins from this partnership will appear first in clinical trial design, manufacturing yield optimization, supply chain efficiency, commercial content velocity, and corporate productivity. Drug discovery acceleration is a real long-term thesis, but it is not a 2026 deliverable.

Which pharma operational domains are likely to show wins first?

Manufacturing and supply chain optimization should show measurable wins first because Novo Nordisk has documented GLP-1 production bottlenecks where five-to-ten-percent yield improvements translate directly to revenue. Commercial operations and corporate-function productivity will likely follow because those domains have shorter feedback cycles and clearer KPIs. Clinical trial design optimization is plausible by mid-2027. Drug discovery wins materialize on a much longer horizon.

Why did Novo Nordisk choose OpenAI over Anthropic?

The most likely factors, in plausibility order: OpenAI's operational breadth across six domains fit Novo Nordisk's integration scope better than Anthropic's deeper-but-narrower stack; ChatGPT's existing consumer footprint made workforce upskilling at 64,000-person scale structurally easier; OpenAI's enterprise sales motion has been more aggressive in 2026; and safety positioning was a tie-stake rather than a differentiator since both labs ship governance frameworks. The decision is informative for the broader pharma vertical map.

What governance and safety controls are in place?

The joint announcement explicitly references "strict data protection, governance and human oversight to ensure ethical and compliant use." Specific governance documents have not been published publicly. Pharma operates under heavy regulatory frameworks including GxP, GDPR, HIPAA-equivalent regimes, and pharmacovigilance reporting requirements — any AI deployment in this scope inherits all of those obligations regardless of the AI vendor.

What is OpenAI's broader 2026 enterprise vertical strategy?

The pattern across 2026 is a horizontal enterprise platform play across pharma (Novo Nordisk), finance (Sierra), government (EU Cyber Action Plan and GPT-5.5-Cyber), workflow (ServiceNow), productivity (Microsoft 365 Copilot), and consumer (GPT-5.5 super-app). The Novo Nordisk deal is the most operationally aggressive single signing in the sequence because the six-domain scope means OpenAI is not just an API vendor — it is a workforce-wide capability layer with explicit upskilling commitments.

What signals would prove this deal is overhyped?

Three signals to watch: pilot programs reporting only single-digit percentage productivity improvements; no AI-accelerated candidate entering Phase 2 trials by end of 2027; and manufacturing yield gains smaller than the wins from Novo Nordisk's ongoing brute-force fill-finish capacity expansion. Any of those outcomes would convert the deal from "AI changes pharma economics" to "another workforce productivity rollout." None would necessarily mean the deal failed — but they would deflate the more ambitious framing.

Which top-20 pharma signs next will define the vertical map?

Watch Roche, Pfizer, Merck, AstraZeneca, Johnson & Johnson, and AbbVie. If three of those six sign with OpenAI by end of 2026, the breadth strategy is the dominant pharma reference architecture and Anthropic's depth bet faces a TAM compression risk in pharma. If three of those six split between OpenAI and Anthropic, the vertical remains contested and the Coefficient Bio acquisition starts paying off via downstream enterprise wins. The next two quarters of pharma + AI announcements will tell us which way the market resolves.

Sources

- Novo Nordisk press release — "Novo Nordisk and OpenAI partner to transform how medicines are discovered and delivered" (April 14, 2026)

- CNBC — "Novo Nordisk teams up with OpenAI for AI-driven drug discovery" (April 14, 2026)

- BioSpace — Novo Nordisk + OpenAI partnership coverage

- Fierce Pharma — "Novo taps OpenAI to deploy AI across R&D, manufacturing and corporate functions"

- BioPharm International — Novo Nordisk + OpenAI drug discovery partnership