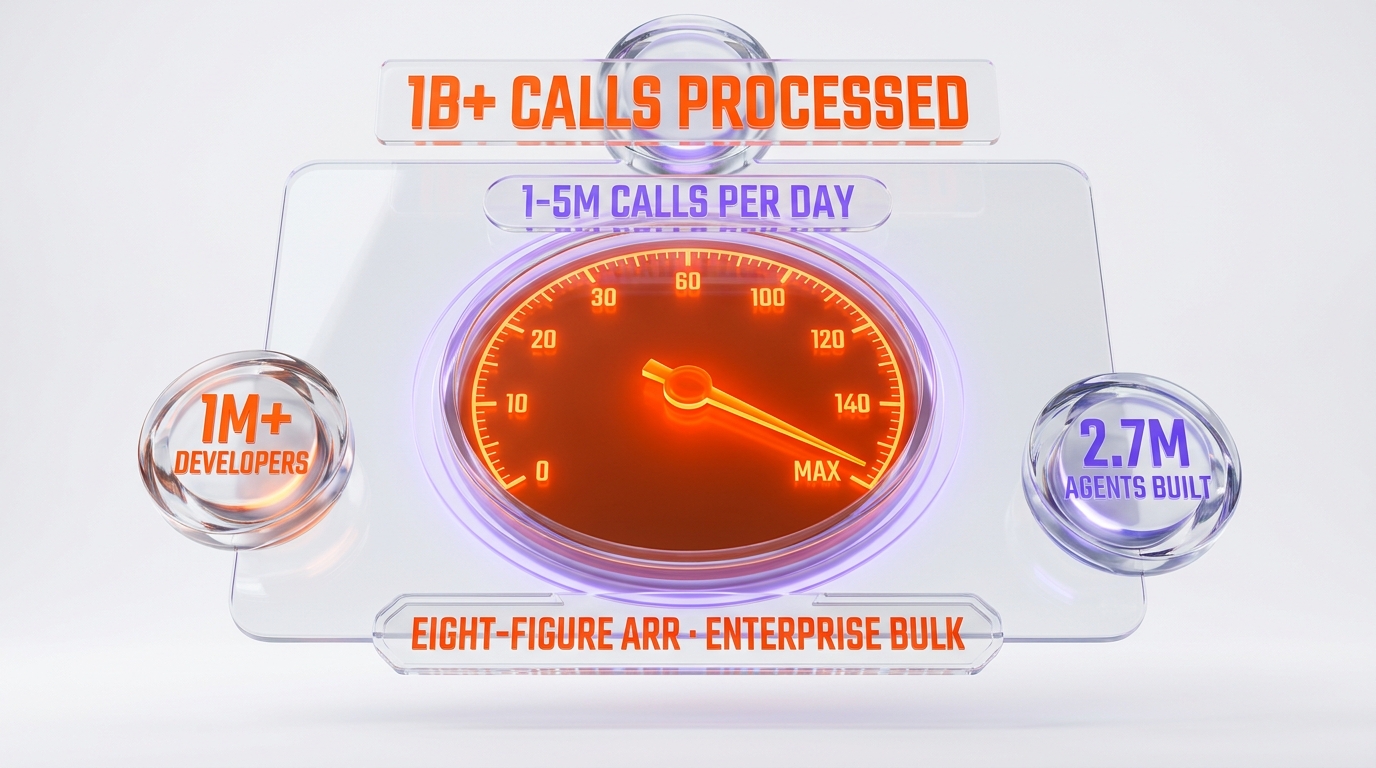

Vapi closed a $50 million Series B at a $500 million valuation on May 12, 2026, with Peak XV leading and Microsoft's M12, Kleiner Perkins, and Bessemer participating. The round is the clearest signal yet that enterprise voice AI has moved from experimental to operationally critical, and the headline customer proof point is unusually concrete: Amazon Ring routes 100% of its inbound calls through Vapi's platform after evaluating more than 40 voice AI vendors in late 2025. According to TechCrunch's reporting and Vapi's official press release, the platform has processed over one billion calls to date, with current daily volume sitting between one and five million calls. Vapi's customer roster also names Kavak, ServiceTitan, New York Life, and Intuit — a procurement mix that lines up with the company's positioning as the developer stack for production-grade enterprise voice agents.

We have been tracking the voice AI category across every meaningful release since the ElevenLabs v3 cycle and the Cartesia Sonic-2 launch, and the Vapi round is the cleanest enterprise-validation event the category has seen so far. Most voice AI funding to date has been justified by demo quality, frontier model capability, or generative breadth. The Vapi narrative inverts that — the funding thesis is anchored to a specific Fortune 500 deployment with a documented selection process, a documented call-volume share (100%), and a documented competitive field (more than 40 vendors evaluated). For procurement teams comparing Vapi against ElevenLabs, Cartesia, GPT-Realtime, Murf AI, and Play.ht, the case study just compressed the evaluation cycle. The platform that wins 100% of Amazon Ring's inbound volume is now the implicit reference deployment for the entire category.

What the round delivered on May 12, 2026

The Series B announcement carries five facts that procurement teams and competitive analysts should anchor against. First, $50 million in new capital at a $500 million post-money valuation, bringing total funding to date to $72 million. Second, Peak XV leading with three named co-investors — Microsoft's M12 venture arm, Kleiner Perkins, and Bessemer Venture Partners — plus participation from earlier-stage backers. Third, more than one billion calls processed cumulatively, with daily volume in the one-to-five-million range. Fourth, an enterprise customer roster that includes Amazon Ring, Kavak, ServiceTitan, New York Life, and Intuit. Fifth, the headline qualitative claim: Ring chose Vapi over more than 40 evaluated vendors and now routes 100% of inbound call volume through the platform.

Each of those five facts deserves separate examination, because the combination is what makes this round structurally different from earlier voice AI raises. The valuation level — $500 million on $72 million raised — implies the round priced the company at roughly seven times invested capital, which is the kind of multiple typically associated with companies that have already demonstrated enterprise lock-in rather than companies that are still working on product-market fit. The call volume metric — over one billion processed — is the largest publicly disclosed figure in the voice AI builder-platform category to date. The daily volume range — one to five million calls per day — implies an annualized run-rate between 365 million and 1.8 billion calls, which is a meaningfully higher operating tempo than any voice AI provider has previously substantiated with a single number.

The customer roster is the most underrated of the five facts. Amazon Ring is the headline because of the 100% number, but the inclusion of New York Life signals regulated-industry adoption (insurance compliance is the highest bar in the voice AI category), Intuit signals fintech adoption (TurboTax and QuickBooks customer service workflows), ServiceTitan signals vertical SaaS adoption (home services dispatch and quoting), and Kavak signals international enterprise adoption (LATAM used-car marketplace operations). The four named accounts cover four distinct verticals, four distinct compliance postures, and four distinct geographies. That spread is what justifies the $500 million valuation more than any single deployment.

The Amazon Ring deployment is the central case study

The Ring deployment is the load-bearing element of the Series B narrative, so it deserves a careful read. According to Vapi's own press release and TechCrunch's interview reporting, Ring approached the voice AI category in late 2025 with a binary question: expand the human call-center capacity to meet inbound demand, or replace inbound handling with AI agents. The Ring team ran an evaluation process across more than 40 voice AI vendors, narrowed the field to a shortlist, and ultimately selected Vapi based on what Vapi CEO Jordan Dearsley described as "granular control over how the AI agents behaved in live customer interactions." The deployment timeline from contract to 100% production routing was two weeks, per Jason Mitura, Amazon Ring's VP of software development, who is quoted as saying "we went from zero to production in two weeks, and 100% of our inbound volume now runs through Vapi."

Three operational details from the deployment matter to procurement teams. First, the "granular control" framing is the specific architectural primitive that distinguishes Vapi from the pure model-API approach offered by general-purpose voice providers. Vapi exposes the agent behavior surface — turn-taking thresholds, barge-in handling, interruption recovery, voicemail detection, hold-music recognition, conversational state management — as developer-controllable parameters rather than as opinionated defaults. For an enterprise where every percentage point of customer-satisfaction-score impact is material, that level of control is the difference between a usable deployment and a stalled pilot. Second, the two-week timeline from zero to 100% production is unusually fast for a Fortune 500 voice deployment, which typically takes three-to-six months in regulated industries. The speed implies the platform is mature enough that integration friction with existing IVR, CRM, and contact-center routing infrastructure is low. Third, the CSAT-maintained-or-improved outcome is the procurement signal that closes the deal in most enterprise evaluations — the question is never whether AI can match human-agent quality, it is whether it can match it without dropping customer satisfaction.

The competitive field deserves attention as well. Forty-plus voice AI vendors evaluated is a large competitive set, and the named runners-up are not publicly disclosed in either the TechCrunch piece or the Vapi press release. Industry observers will reasonably assume the shortlist included ElevenLabs, Cartesia, and the major hyperscaler voice services (Amazon Connect's own Lex-based stack, Google Dialogflow CX, Microsoft's Azure Communication Services), but the specific shortlist remains an open question. What is unambiguous is that the selection was conducted by a team that had the technical depth to evaluate 40+ vendors against production criteria — which means the decision is harder to dismiss as a vendor relationship play. For comparable enterprises evaluating voice AI, the Ring evaluation methodology is now the implicit reference.

One billion calls processed: the scale economics

The cumulative call-volume metric — over one billion calls processed on the platform — is the largest disclosed figure in the voice AI builder-platform category to date, and the operating implications are worth examining. A platform that has processed one billion calls has surfaced edge cases at a scale most competitors have not. Latency spikes during regional carrier congestion, transcription failures on heavily accented speech, barge-in misfires during background noise events, voicemail detection failures across regional voicemail tones, hold-music false-positive handling — each of those failure modes is a separate engineering problem, and each one is only discoverable at scale. Platforms with smaller call-volume bases will inevitably surface these issues later, with the corresponding deployment friction at the customer side.

The daily volume range — one to five million calls per day — implies sustained infrastructure tempo. At the upper bound of five million calls per day, the platform is handling approximately 58 calls per second on a 24-hour average, with peak loads almost certainly an order of magnitude higher during business-hours concentration. That throughput requires production-grade infrastructure across speech-to-text streaming, large language model inference, text-to-speech synthesis, voice activity detection, network telephony routing (SIP, PSTN interconnect), and the application-level orchestration that glues those layers together. Building that stack in 2024-2025 was a meaningful engineering achievement; sustaining it at one-to-five-million calls per day in 2026 is an operational achievement that distinguishes Vapi from earlier-stage voice AI platforms still working on infrastructure scaling.

The developer-density metric — one million developers and 2.7 million agents created on the platform — is the leading indicator of platform stickiness. Each developer-built agent represents a configuration sunk cost: prompt engineering, conversational state design, integration with backend CRM or order-management systems, voice selection, latency tuning, evaluation harness setup. Once an agent is in production, the migration cost to a competing platform is typically measured in weeks of engineering work, which creates the kind of platform-level moat that justifies premium valuation multiples. A platform with 2.7 million agents built is structurally harder to displace than a platform with 27,000 agents built, even if the per-call quality is otherwise comparable.

The eight-figure ARR disclosure, paired with the customer roster and the call-volume metrics, implies a per-call gross revenue that is broadly consistent with developer-platform unit economics in adjacent categories. The valuation multiple — roughly $500 million on eight-figure ARR — is in the range of 10-to-50x ARR depending on where in the eight-figure band the actual number sits, which is a multiple consistent with infrastructure-software comparables in mid-2026 rather than an outlier. The round is priced for growth continuation, not for a re-rate.

The voice AI enterprise landscape in mid-2026

The Vapi round arrives at a moment when the voice AI category is bifurcating into two distinct sub-segments. On one side, the model-and-voice providers — companies whose primary product is the underlying speech model, the voice library, or the text-to-speech engine. ElevenLabs sits at the top of this segment with its v3 model and consumer-facing voice library, joined by Cartesia with the Sonic family, Murf AI for studio-grade narration, and Play.ht in the legacy synthesis tier. On the other side, the builder-platform providers — companies whose primary product is the developer stack that turns underlying models into production-grade conversational agents. Vapi sits at the top of this segment, with GPT-Realtime from OpenAI competing on the model-and-builder axis simultaneously.

The bifurcation matters because the procurement question differs between the two segments. For model-and-voice providers, the buyer is typically a media production team, a content creator, or a marketing department, and the evaluation criteria center on voice quality, voice library breadth, and pronunciation accuracy. For builder-platforms, the buyer is typically a developer organization or a contact-center engineering team, and the evaluation criteria center on conversational state management, telephony integration, latency budgets, observability tooling, and the agent-behavior control surface that the Ring deployment specifically highlighted.

Vapi's positioning as a builder-platform — rather than as a model-and-voice provider — is the strategic choice that explains both the Ring case study and the $500 million valuation. The company does not own the underlying speech model; it composes models from third-party providers (including ElevenLabs and Cartesia voices) into a managed agent runtime. That architectural choice means Vapi can ride the frontier model improvements from every provider rather than being tied to its own model roadmap. It also means Vapi competes on the orchestration layer rather than on the model layer — a thinner competitive surface but a stickier one once enterprise deployments have configured against the platform's primitives.

Readers evaluating the segment structure should also see our ElevenLabs vs Cartesia comparison for the head-to-head between the two leading model-and-voice providers, our ElevenLabs vs Murf comparison for the studio-grade narration vector, and our ElevenLabs vs Play.ht comparison for the legacy-versus-frontier model contrast. The Eleven Music vs Suno AI comparison covers the adjacent music-generation segment that sits one layer above pure voice in the audio-AI category map. Each of those four comparisons is a different vector on which the Vapi positioning will be tested over the next two to four quarters.

The cap table and the investor thesis

The investor mix on the round is structurally informative. Peak XV — the rebranded Sequoia India and Southeast Asia franchise — leads, which is a non-trivial choice for a US-headquartered enterprise infrastructure company. Peak XV's involvement at lead position implies the firm believes the voice AI builder-platform category will have material global expansion outside the US-and-EU enterprise base, which is a defensible thesis given Kavak's presence on the customer roster and the structural opportunity in LATAM and Southeast Asian contact-center markets where labor-cost arbitrage from voice AI is most material.

Microsoft's M12 participation is the strategic signal that gets the least attention in the announcement coverage. M12 invests with a mandate to identify Microsoft-relevant infrastructure layers, and voice AI integrated with Azure Communication Services, Microsoft Teams, and the broader Microsoft 365 contact-center suite is a clear strategic fit. M12's involvement does not preclude Microsoft building a competing internal capability, but it does signal that Microsoft's strategic investment arm sees the builder-platform layer as a separate value capture from the underlying model layer. That is consistent with Microsoft's broader pattern of investing across the AI infrastructure stack — funding the model layer through OpenAI while also funding the application-orchestration layer through partners.

Kleiner Perkins and Bessemer Venture Partners are the enterprise-software specialists on the round, and their participation underwrites the thesis that Vapi's category structure is enterprise-infrastructure rather than consumer or developer-tools. Both firms have track records in voice and contact-center adjacent investments, and both have the operating expertise to support an enterprise sales motion as the company scales beyond its current customer base. The presence of both firms on the round, alongside Peak XV's global thesis and M12's Microsoft strategic angle, gives the cap table four distinct strategic vectors: global expansion, Microsoft ecosystem integration, US enterprise SaaS scaling, and enterprise contact-center vertical depth. That is an unusually well-balanced investor mix for a Series B.

CEO Jordan Dearsley's profile completes the founder-and-financing picture. Dearsley is a University of Waterloo alum and Y Combinator graduate, and the company maintains a roughly 100-person headcount at Series B. The headcount-to-revenue ratio implied by an eight-figure ARR run-rate at 100 people is consistent with software-infrastructure efficiency benchmarks rather than with the higher headcount profile typical of services-heavy enterprise vendors. That efficiency profile is part of what justifies the valuation multiple at the round.

Why this round matters for procurement teams evaluating voice AI

For procurement teams in active evaluation of voice AI platforms, the Vapi round changes the evaluation rubric in three concrete ways. First, Amazon Ring is now the reference deployment for the category. Any procurement conversation that includes Vapi will reference the Ring deployment, the 100% inbound volume figure, the two-week deployment timeline, and the "selected over 40 rivals" framing. Competing vendors will need to address the Ring reference directly — either by acknowledging it and positioning around a different deployment archetype, or by surfacing their own comparable reference deployment. The procurement conversation now starts with the Ring comparison rather than ending with it.

Second, the builder-platform versus model-and-voice distinction now sits at the top of the evaluation taxonomy. Procurement teams evaluating voice AI will be asked upfront whether they are evaluating a builder-platform (where Vapi is the reference) or a model-and-voice provider (where ElevenLabs and Cartesia are the references). That bifurcation reduces the chance of category-mismatched evaluations, which has historically been a source of stalled procurement cycles in voice AI. The category map is now legible enough that procurement teams can run two parallel evaluations rather than one confused evaluation.

Third, the agent-behavior control surface — turn-taking, barge-in, voicemail handling, conversational state management — is now an explicit procurement criterion rather than an implicit one. The Ring deployment's selection narrative specifically called out "granular control over how the AI agents behaved in live customer interactions," and that language will propagate into RFPs and evaluation rubrics across the category. Vendors whose control surface is less granular — typically because the underlying architecture is model-API-as-product rather than builder-platform — will need to address that gap explicitly. Vendors with comparable or superior control surfaces will use the Ring narrative as proof that the control surface is the production-deployment differentiator.

Why the timing of this round signals broader voice AI category maturity

The May 12, 2026 announcement timing is itself a category-level signal worth reading. Voice AI funding through 2024 and 2025 was characterized by frequent rounds at consumer-tech valuation multiples — strong founding teams, frontier-model partnerships, and demo-driven narratives. The Vapi round breaks that pattern in three ways. First, the funding-to-customer-validation ratio inverts: the Ring deployment is named in the announcement materials with specific volume share, specific deployment timeline, and specific evaluation depth. Most prior voice AI rounds named customers as a marketing list rather than as a validation thesis. Second, the round arrives after the model layer has already commoditized to the point where multiple frontier voice models are competitively available — which means the value-capture conversation has shifted from "who has the best model" to "who has the best agent runtime." Third, the lead investor is not a voice-AI-specialist firm but a generalist global growth-equity firm (Peak XV), which signals the category is now legible to non-specialist capital allocators.

The category-maturity reading has implications for adjacent categories. The video AI category — where ElevenLabs' adjacent music model and the broader generative-media space sit — is roughly 12 to 18 months behind the voice category on the same maturity curve. The same pattern that just played out in voice (model commoditization → builder-platform consolidation → enterprise validation event → generalist-capital lead at $500M+ valuation) is the pattern that will play out in video and music over the next four to eight quarters. Investors and procurement teams tracking generative AI infrastructure should treat the Vapi round as a leading indicator for the structural evolution of every generative media sub-category.

The other category signal is the cumulative-call-volume metric. One billion calls processed is a number that voice AI category observers have been waiting to see disclosed by a builder-platform, and the disclosure now anchors the floor for what serious enterprise voice operations look like in 2026. Competing builder-platforms will face pressure to disclose comparable cumulative volume figures, which will reshape the public-disclosure norms in the category over the next two quarters. Procurement teams will increasingly demand cumulative-call-volume figures during evaluation cycles, and vendors without comparable numbers will face the asymmetric burden of explaining the absence.

What could go wrong for Vapi from here

The round is structurally strong but the post-round execution has three identifiable risk vectors. First, the model-provider dependency. Vapi's positioning as a builder-platform rather than a model owner means the platform's quality is bounded by the quality of the underlying speech and language models the customer composes into agents. If ElevenLabs or Cartesia chooses to vertically integrate into builder-platform capabilities, Vapi's value proposition shifts from "best-in-class orchestration on best-in-class models" to "orchestration layer on models that increasingly include their own orchestration." The model providers are not currently moving aggressively into builder-platform territory, but the strategic risk is real and worth monitoring across the next two to four model release cycles.

Second, the hyperscaler competitive vector. Amazon Connect, Google Dialogflow CX, and Microsoft's Azure Communication Services are all positioned to compete in the builder-platform segment, with the natural advantage of integrated cloud billing, integrated identity, and integrated CRM. The Vapi-Ring case study demonstrates that an independent builder-platform can win against the hyperscaler-native voice stacks at Fortune 500 scale, but the win is one deployment rather than a category-wide pattern. Hyperscaler builder-platform capability will improve, and Vapi's independent positioning will need to continue out-executing the hyperscaler product cycles to sustain the lead the Ring deployment establishes.

Third, the deployment-concentration question. The Ring case study is the load-bearing reference deployment in the Series B narrative, and the procurement signal is strong precisely because the deployment is at 100% inbound volume. The downside of leaning on a single reference deployment is that any operational incident at Ring becomes a category-wide event for Vapi. A multi-hour outage, a regulatory inquiry, or a customer-satisfaction regression that hits public reporting at Ring would propagate through every active Vapi procurement conversation. The mitigation is the breadth of the rest of the customer roster — Kavak, ServiceTitan, New York Life, Intuit — and the company will likely emphasize that breadth in upcoming customer-success messaging.

Strategic bottom line

The Vapi $50 million Series B at a $500 million valuation is the cleanest enterprise-validation event the voice AI category has produced. The round is anchored to a specific Fortune 500 deployment with a documented selection process across more than 40 vendors, a documented call-volume share at 100% of inbound, and a documented operational outcome with customer satisfaction maintained or improved. That combination of facts is what the voice AI category has been missing across two years of demo-driven funding cycles. Vapi now occupies the implicit reference position in the builder-platform segment, and the procurement conversation across the category shifts accordingly.

The cap table — Peak XV leading with Microsoft M12, Kleiner Perkins, and Bessemer participating — covers four distinct strategic vectors: global expansion, Microsoft ecosystem integration, US enterprise SaaS scaling, and enterprise contact-center vertical depth. That balance is the structural signal that the investor consensus has formed around the builder-platform segment as a distinct value-capture layer in the voice AI stack, separate from the model-and-voice layer where ElevenLabs and Cartesia compete. The two segments will continue to evolve in parallel, and procurement teams will increasingly run separate evaluations against each segment rather than confusing the category map.

For builders, the immediate implication is that the agent-behavior control surface — turn-taking, barge-in, voicemail handling, conversational state — is now the production-deployment differentiator rather than the voice library or the model choice. For procurement teams, the immediate implication is that the Ring reference deployment is the comparison anchor for every voice AI evaluation through the rest of 2026. For competitors in the builder-platform segment, the immediate implication is that the platform-completeness bar has moved up, and the next round of competitive responses will need to address the operational scale (one billion calls processed) and the reference deployment (Amazon Ring at 100% volume) directly. The category just compressed around a clear leader, and the next three quarters will determine whether the lead consolidates or whether the model providers and hyperscalers close the gap.

Frequently Asked Questions

How much did Vapi raise in its Series B and at what valuation?

Vapi raised $50 million in Series B funding at a $500 million post-money valuation, announced on May 12, 2026. The round brings total capital raised to approximately $72 million across seed, Series A, and Series B. Peak XV led the round, with Microsoft's M12 venture arm, Kleiner Perkins, and Bessemer Venture Partners participating alongside earlier-stage investors. The valuation puts Vapi among the top-tier voice AI builder-platform companies in mid-2026.

Why is the Amazon Ring deployment so important for Vapi's story?

Amazon Ring routes 100% of its inbound customer calls through Vapi's platform after evaluating more than 40 voice AI vendors in late 2025. The deployment went from contract to 100% production routing in two weeks, per Amazon Ring VP of software development Jason Mitura, with customer satisfaction scores maintained or improved through the cutover. The combination of competitive evaluation depth (40+ vendors), volume share (100% of inbound), deployment speed (two weeks), and CSAT outcome makes Ring the clearest enterprise validation event the voice AI category has produced to date.

How many calls has Vapi processed and what is the daily volume?

Vapi has processed over one billion calls cumulatively on the platform, with current daily volume between one and five million calls. At the upper bound of five million calls per day, the platform handles approximately 58 calls per second on a 24-hour average, with peak loads almost certainly an order of magnitude higher during business-hours concentration. The cumulative one-billion-calls figure is the largest publicly disclosed number in the voice AI builder-platform category as of May 2026.

Who are Vapi's named enterprise customers besides Amazon Ring?

Vapi's press release names Kavak (LATAM used-car marketplace), ServiceTitan (vertical SaaS for home services), New York Life (insurance, the highest compliance bar in voice AI), and Intuit (fintech, covering TurboTax and QuickBooks customer service workflows) alongside Amazon Ring. The four named accounts cover four distinct verticals, four distinct compliance postures, and four distinct geographies, which is part of what justifies the $500 million valuation beyond the headline Ring deployment.

How does Vapi differ from ElevenLabs and Cartesia?

Vapi is a builder-platform — a developer stack that composes underlying speech models, voices, and language models into production-grade conversational agents. ElevenLabs and Cartesia are model-and-voice providers — companies whose primary product is the underlying speech model and the voice library. The two segments serve different procurement teams: builder-platforms typically sell to developer organizations and contact-center engineering teams, while model-and-voice providers typically sell to media production, content creation, or marketing teams. Vapi can compose ElevenLabs and Cartesia voices into its agents, which is one reason the platform competes on orchestration rather than on model quality.

Who leads Vapi and what is the team profile?

Jordan Dearsley is CEO and co-founder. Nikhil Gupta is the other co-founder. Both are alumni of the University of Waterloo and graduates of Y Combinator. The company maintains a roughly 100-person headcount at Series B, with an eight-figure ARR run-rate. The headcount-to-revenue ratio implied by those numbers is consistent with software-infrastructure efficiency benchmarks rather than with the higher headcount profile typical of services-heavy enterprise vendors.

Why did Peak XV lead instead of a US-headquartered firm?

Peak XV — the rebranded Sequoia India and Southeast Asia franchise — leading at a US-headquartered enterprise infrastructure round implies the firm sees material global expansion opportunity in the voice AI builder-platform category. The Kavak account on Vapi's customer roster is one anchor point for the LATAM thesis, and the broader structural opportunity in Southeast Asian contact-center markets — where labor-cost arbitrage from voice AI is most material — is the second. Peak XV's involvement at lead position signals the global expansion thesis is central to the round narrative, not adjacent to it.

What role does Microsoft M12 play on the cap table?

Microsoft's M12 venture arm invests with a mandate to identify Microsoft-relevant infrastructure layers. Voice AI integrated with Azure Communication Services, Microsoft Teams, and the broader Microsoft 365 contact-center suite is a clear strategic fit. M12's participation does not preclude Microsoft building competing internal capability, but it does signal that Microsoft's strategic investment arm sees the builder-platform layer as a separate value-capture from the underlying model layer — consistent with Microsoft's broader pattern of investing across the AI infrastructure stack.

What is the agent-behavior control surface that Ring referenced?

The agent-behavior control surface refers to the developer-controllable parameters that determine how a voice AI agent behaves in live customer interactions — turn-taking thresholds, barge-in handling, interruption recovery, voicemail detection, hold-music recognition, conversational state management, and similar primitives. Amazon Ring's selection narrative specifically called out Vapi's "granular control over how the AI agents behaved in live customer interactions" as the deciding factor. Builder-platforms expose this control surface as configurable parameters, while model-API-as-product approaches typically ship opinionated defaults that are harder to tune at the enterprise level.

How does this round affect procurement teams currently evaluating voice AI?

The round changes the procurement rubric in three ways. First, Amazon Ring becomes the reference deployment that every voice AI evaluation will compare against. Second, the builder-platform versus model-and-voice distinction now sits at the top of the evaluation taxonomy, reducing category-mismatched evaluations. Third, the agent-behavior control surface — turn-taking, barge-in, voicemail handling, conversational state — moves from implicit to explicit procurement criterion. Vendors without comparable control surfaces will need to address the gap directly in upcoming RFP responses.

What are the biggest risks to Vapi's competitive position from here?

Three risks worth tracking. First, the model-provider dependency — if ElevenLabs or Cartesia chooses to vertically integrate into builder-platform capabilities, Vapi's orchestration-layer value proposition shifts. Second, the hyperscaler competitive vector — Amazon Connect, Google Dialogflow CX, and Microsoft Azure Communication Services all compete in the builder-platform segment with integrated cloud billing and identity advantages. Third, the deployment-concentration question — Ring is the load-bearing reference, and any operational incident at Ring would propagate through every active Vapi procurement conversation. The mitigation is the breadth of the rest of the customer roster across Kavak, ServiceTitan, New York Life, and Intuit.

How should builders and developers respond to the Vapi round?

For builders evaluating where to invest agent-development effort, the round is a signal that the builder-platform segment has reached enterprise-validation maturity and that production-grade voice agents are now a documented procurement category rather than a speculative one. Developer teams already on Vapi should treat the round as validation that the platform's roadmap will be funded through the next two to three product cycles. Developer teams on alternative builder-platforms should evaluate their platform's competitive response to the Ring case study and the agent-behavior control-surface positioning over the next two to four quarters. Developer teams still on model-API-as-product approaches should evaluate whether the builder-platform segment is the right architectural choice for their production agent use cases.