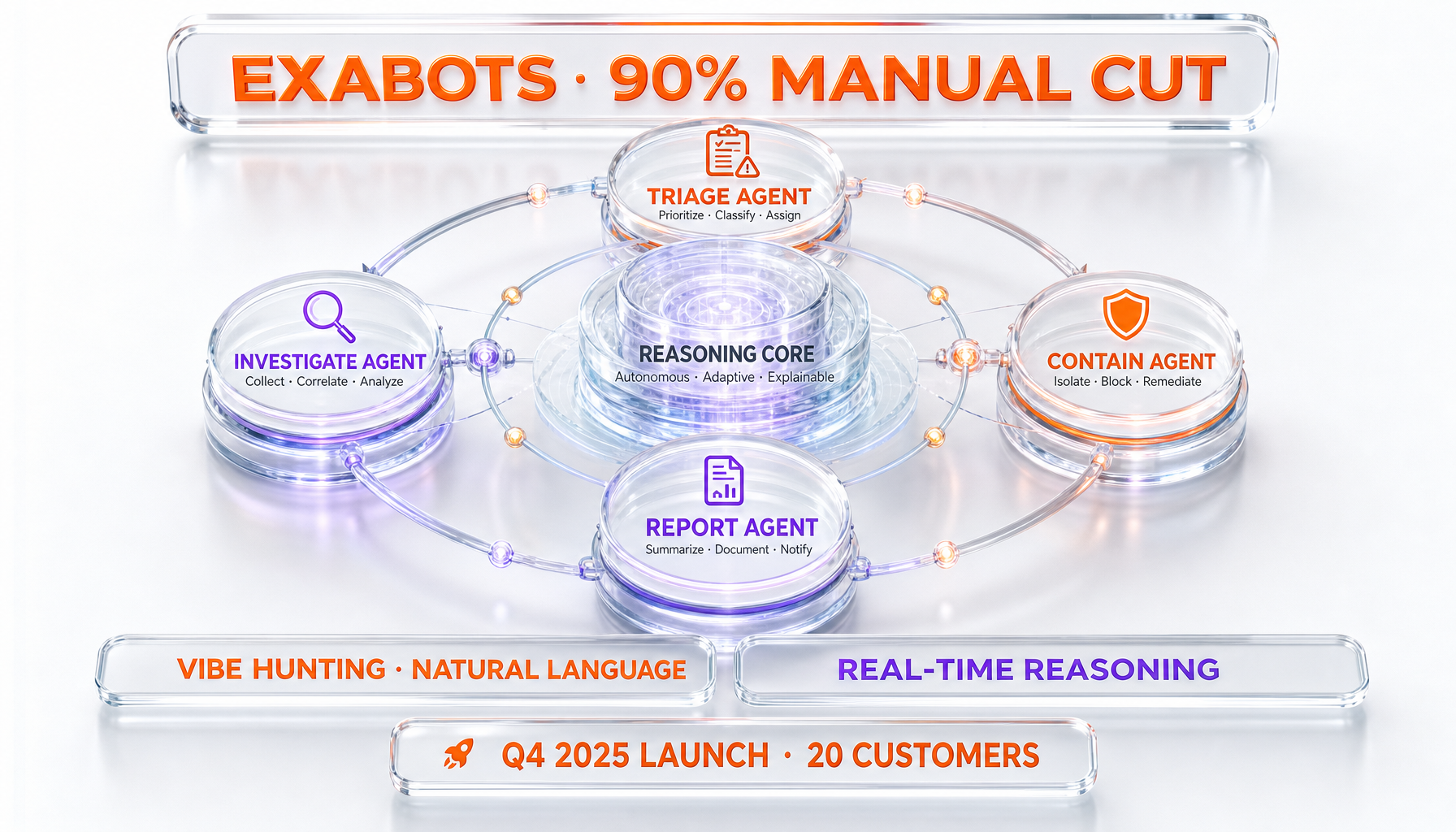

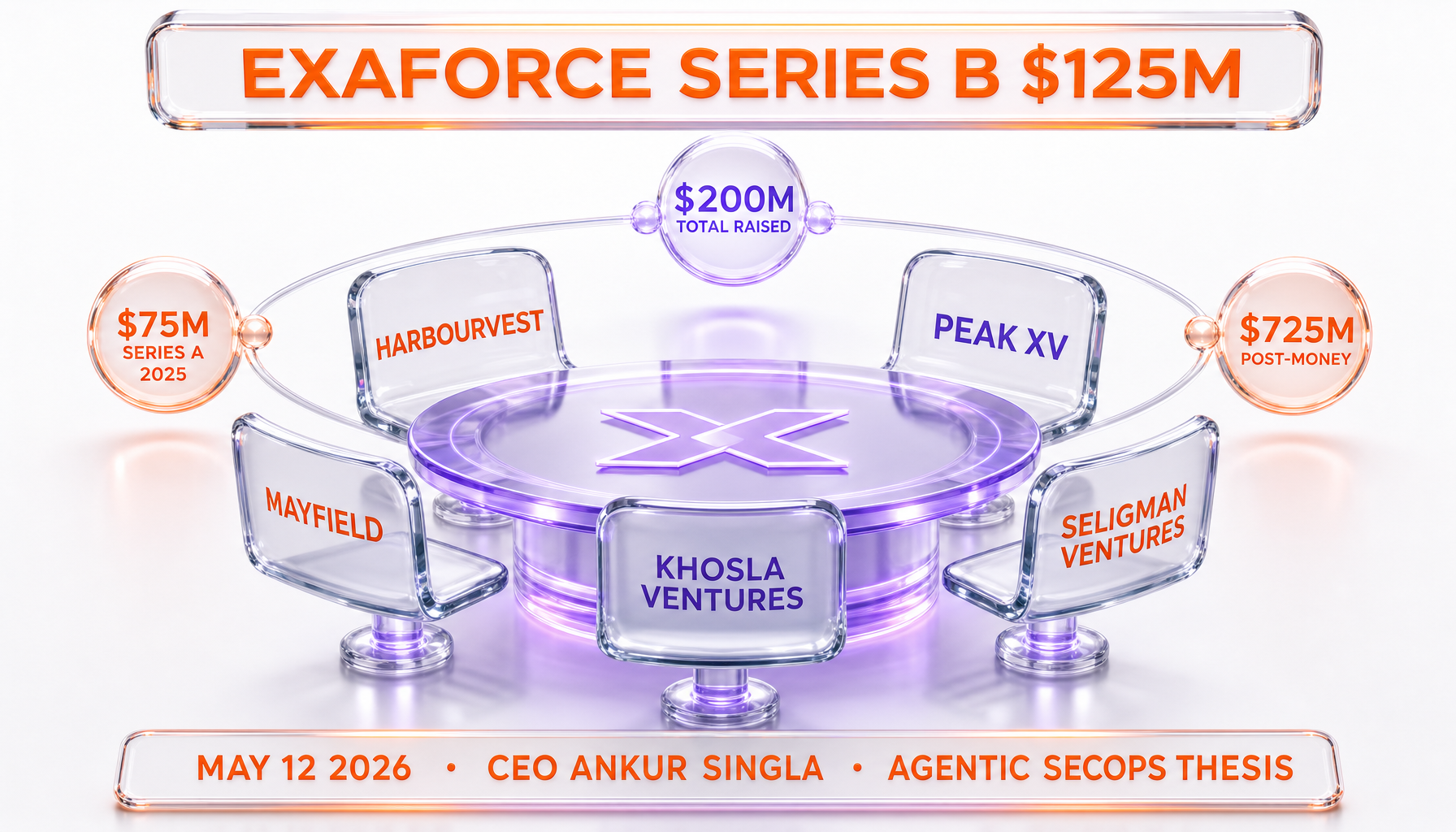

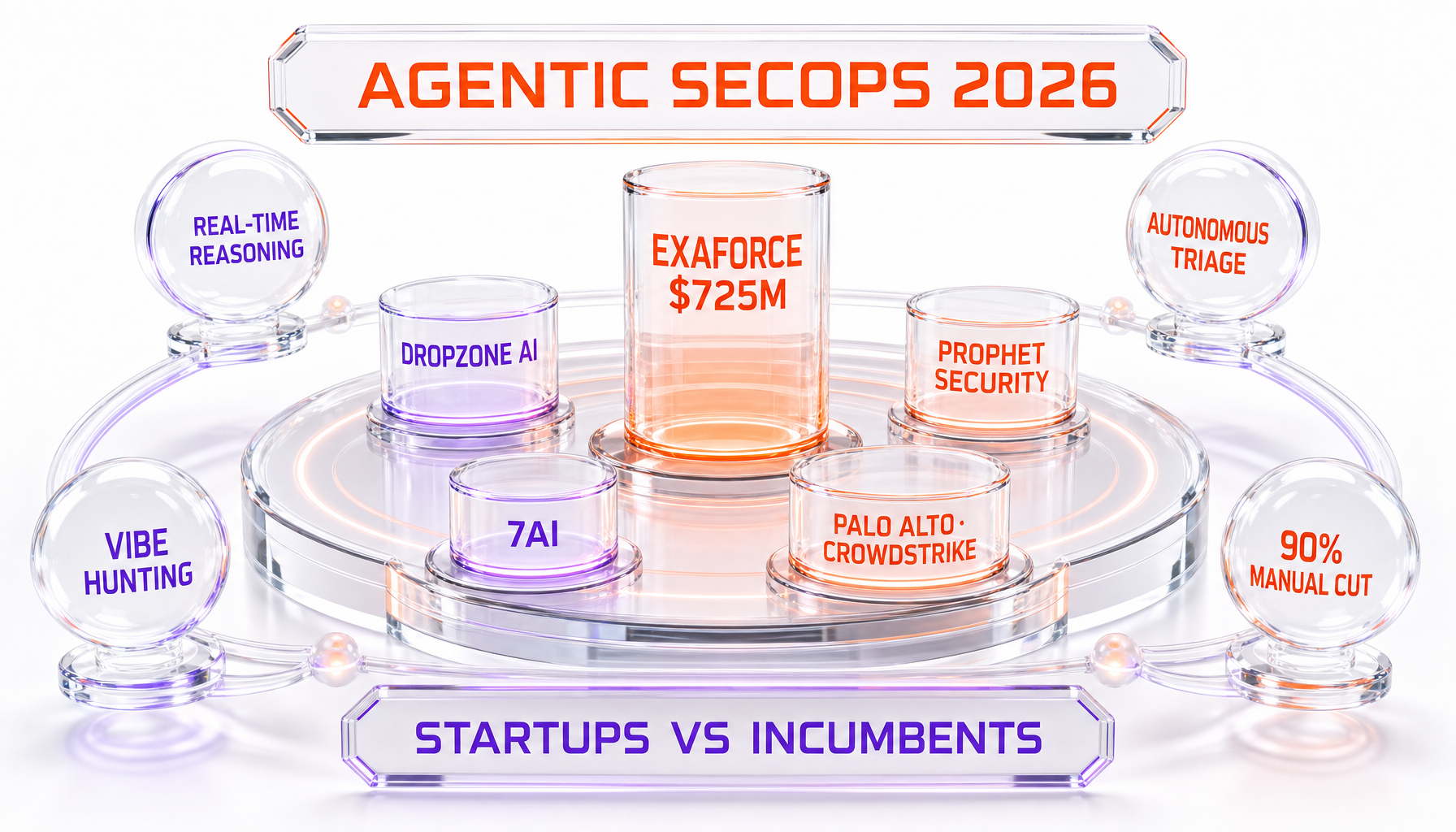

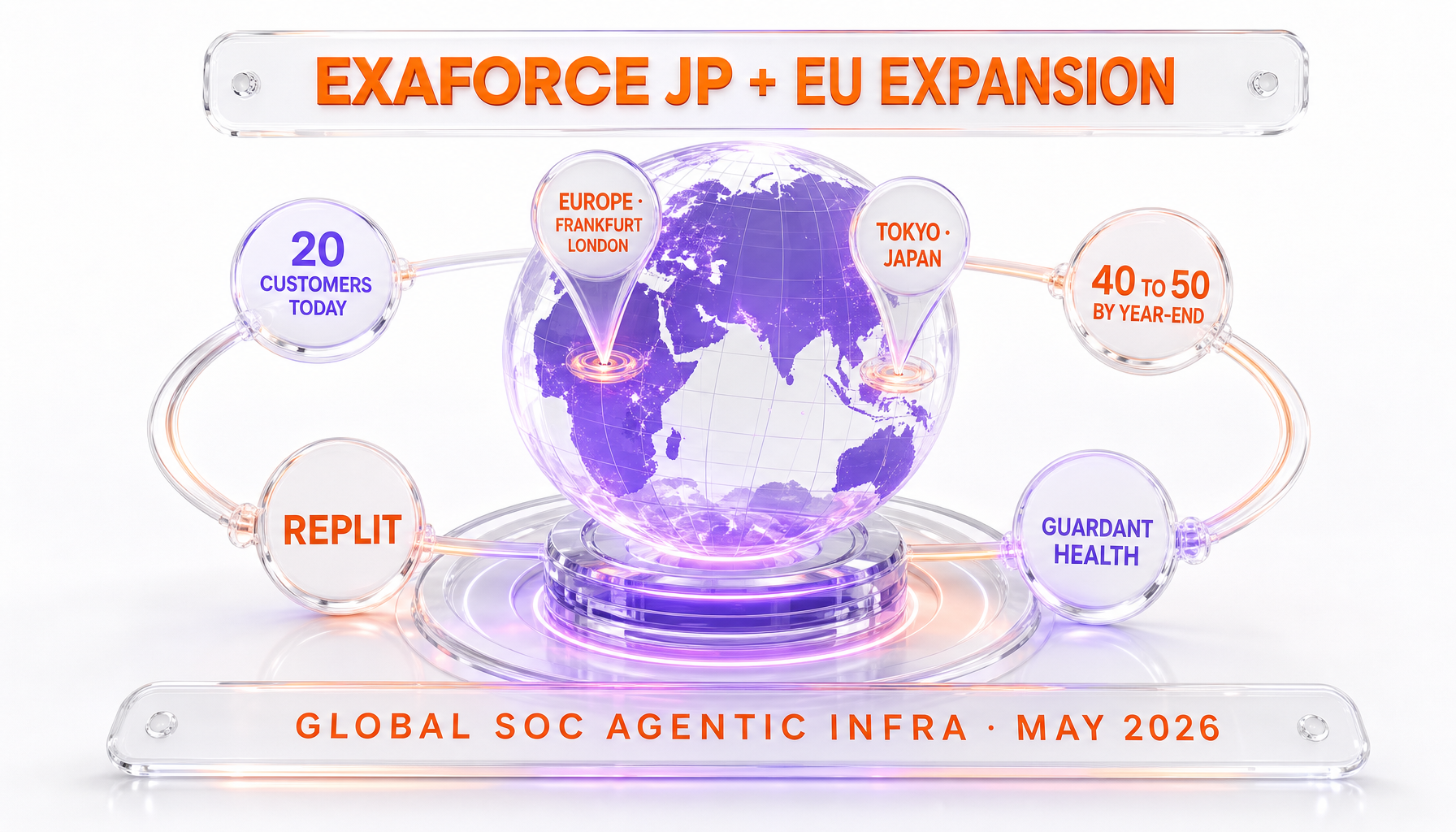

Exaforce closed a $125 million Series B at a $725 million post-money valuation on May 12, 2026, with HarbourVest leading and Peak XV, Mayfield, Khosla Ventures, and Seligman Ventures participating. The round brings total funding to $200 million across a Series A and Series B sequence completed in roughly one year, and arrives nine months after the platform's Q4 2025 commercial launch. According to TechCrunch's reporting, the company has signed 20 customers since launch — including Replit and Guardant Health — and is projecting 40 to 50 customers by year-end alongside a coordinated expansion into Japan and Europe. CEO Ankur Singla describes the platform as agentic SecOps with real-time AI cyber reasoning: autonomous agents the company calls "Exabots" that triage, investigate, and contain incidents at machine speed, with natural-language query primitives ("vibe hunting") that let analysts interrogate the threat surface without writing SIEM queries.

We have been tracking the agentic SecOps category since the Anthropic Claude Security public beta reframed vulnerability scanning as an agent-runnable workload, and the Exaforce round is the cleanest valuation signal the segment has produced in 2026. Most cyber AI funding to date has been priced on point-product narratives — detection, triage, response, or threat intelligence treated as separate buyer journeys. The Exaforce thesis collapses those journeys into a single agentic runtime, and the $725 million valuation prices the company at roughly 3.6x total invested capital, which is the kind of multiple typically associated with infrastructure platforms that have crossed enterprise-validation thresholds rather than with point-product startups still proving land-and-expand motion. For security buyers comparing Exaforce against CrowdStrike's Charlotte AI workflows, Palo Alto Networks' Cortex XSIAM agentic features, and the wave of agentic SecOps startups including Dropzone AI, Prophet Security, and 7AI, the round just compressed the procurement window for evaluating whether a dedicated agentic runtime beats the incumbent EDR-and-SIEM workflow attachment.

What the Exaforce round delivered on May 12, 2026

The Series B announcement carries six facts that procurement teams and competitive analysts should anchor against. First, $125 million in new primary capital at a $725 million post-money valuation, bringing total funding raised to $200 million across the seed, Series A, and Series B sequence. Second, HarbourVest leading the round, with Peak XV, Mayfield, Khosla Ventures, and Seligman Ventures participating — a four-firm strategic cap table with each name representing a different thesis vector. Third, a Q4 2025 commercial launch followed by 20 signed customers in roughly two quarters, with public references including Replit (developer infrastructure) and Guardant Health (regulated healthcare). Fourth, a projected customer count of 40 to 50 by the end of 2026, implying a customer-add tempo that is approximately doubling the current base. Fifth, an architecture built around autonomous "Exabot" agents that the company claims reduce manual SOC analyst tasks by up to 90%. Sixth, a coordinated international expansion into Japan and Europe immediately following the round close.

Each of those six facts deserves separate examination, because the combination is what makes this round structurally different from prior SecOps AI raises. The funding tempo — $75 million Series A in 2025, $125 million Series B in May 2026, both within roughly twelve months — is the kind of cadence reserved for companies whose early-customer signal compresses the time the next round would normally need to season. The valuation jump from Series A to Series B is the implicit signal of how investor consensus has formed. The customer-count detail — 20 signed in two quarters, projected 40 to 50 by year-end — is one of the cleanest disclosed traction metrics the agentic SecOps category has produced. The "90% manual task reduction" claim is the headline operational metric that the platform asks security operations leaders to evaluate against their current Tier-1 and Tier-2 analyst workload.

The international expansion announcement is the most strategically informative of the six facts. Japan and Europe are the two regions where cyber regulation, data-residency requirements, and SOC staffing economics differ most from the US baseline that early-stage cyber startups typically optimize for. A startup announcing a Japan and Europe expansion within nine months of commercial launch is making an early bet that the agentic SecOps thesis travels across regulatory boundaries — which is structurally different from the typical SaaS GTM pattern that defers international expansion to Series C or later.

The Exabot architecture and real-time cyber reasoning

The Exabot architecture is the load-bearing technical claim of the Series B narrative, so it deserves a careful read. Exaforce positions Exabots as autonomous SecOps agents that handle the workflow stages traditionally consumed by Tier-1 and Tier-2 analyst time — alert triage, false-positive suppression, evidence collection, threat hypothesis generation, lateral-movement investigation, and initial containment recommendations. Each Exabot operates within a constrained decision surface defined by the customer's SOC policy: what data sources to query, what containment actions to recommend versus execute, what escalation thresholds to apply for human review. The "real-time cyber reasoning" framing references the architectural difference between batch SIEM analytics (where queries return historical aggregates) and continuous-streaming agent reasoning (where the platform makes triage decisions as alerts arrive).

The "vibe hunting" terminology — Exaforce's framing for natural-language threat investigation — is the procurement-friendly shorthand for what the platform actually does at the analyst interface. Instead of writing a structured SIEM query in a vendor-specific query language, an analyst describes the investigation in plain English ("show me lateral movement from finance-team accounts in the last 24 hours that touched the customer database"), and the platform translates that intent into the underlying data-source queries, correlates the results, and returns a structured investigation timeline. The framing is consumer-friendly enough to land in vendor marketing materials, and the underlying capability — natural-language-to-detection translation — is one of the cleanest agentic primitives in the current SecOps category.

Three operational details from the platform architecture matter to procurement teams. First, the 90% manual task reduction claim is a category-leading number and will be the metric that incumbent EDR and SIEM vendors are forced to benchmark against in upcoming RFPs. Vendors whose AI features ship as workflow enhancements rather than as autonomous agents will face the asymmetric burden of explaining why their assist-mode automation cannot match the autonomous-mode numbers Exaforce is publishing. Second, the real-time reasoning architecture changes the latency budget that downstream SOC workflows operate against. Batch SIEM analytics typically run on a minutes-to-hours latency budget; streaming agentic reasoning operates on a seconds-to-tens-of-seconds latency budget, which is the difference between catching an attack in progress and reconstructing one after the fact. Third, the natural-language query primitive collapses the analyst training overhead that vendor-specific SIEM query languages impose, which is a meaningful talent-acquisition lever in a SOC labor market where senior detection-engineering capacity remains scarce.

Replit and Guardant Health: what the customer base signals

The 20-customer count after roughly two quarters of commercial availability is the cleanest disclosed traction metric the agentic SecOps category has produced in 2026. More important than the absolute number is the composition of the public references. Replit anchors the developer-infrastructure vertical — a company whose security posture has to balance the openness developers expect with the threat surface that AI-assisted code generation introduces. Guardant Health anchors the regulated healthcare vertical — a company whose data-residency, HIPAA, and clinical-genomics compliance posture is among the strictest in the SecOps category. Two named accounts covering two of the highest-trust verticals in mid-2026 is a stronger procurement signal than ten named accounts in lower-trust verticals.

The projected customer count — 40 to 50 by year-end — implies a customer-add tempo of approximately 20 to 30 net new accounts in the second half of 2026. That tempo is consistent with infrastructure-software early-scaling benchmarks rather than with point-product land-and-expand motions, and reflects the cap-table-implied thesis that the platform can pull procurement budget directly rather than waiting for security teams to displace existing SIEM or SOAR contracts. The bookings implication, if the company hits the 40-to-50 customer target, is an annualized run-rate trajectory that supports the $725 million valuation under reasonable per-customer ACV assumptions.

The cap table and the investor thesis

The investor mix on the round is structurally informative. HarbourVest leading is the signal that institutional growth-equity capital — the kind that prices rounds based on cash-flow-discountable infrastructure metrics rather than on category-momentum narratives — has formed conviction on the agentic SecOps segment. HarbourVest's pattern of participation in cybersecurity infrastructure rounds tracks closely with companies that have crossed the early-enterprise-validation threshold, and the firm leading at Series B rather than waiting for a later round signals confidence that the next 12 to 24 months of platform execution will price in higher than the current $725 million mark.

Peak XV — the rebranded Sequoia India and Southeast Asia franchise — joining the round adds the global-expansion vector that the announced Japan and Europe expansion plan needs to support. Peak XV's involvement at a US-headquartered cyber infrastructure round is a relatively rare pattern, and signals the firm sees material expansion opportunity in the agentic SecOps category across Asia-Pacific markets where SOC staffing costs and regulatory complexity create natural pull for automation. The Japan expansion piece of the announcement reads as a partial expression of Peak XV's thesis rather than as a US-firm decision made independently of the cap table.

Mayfield brings enterprise-infrastructure depth that the round needs to support the platform-versus-point-product positioning. Mayfield's track record in cybersecurity infrastructure investing — including category-defining outcomes in earlier eras of the SIEM and EDR markets — gives the round an operator-investor signal that is hard to fake. Khosla Ventures brings the frontier-AI thesis credibility that anchors the "agentic" framing of the platform. Vinod Khosla's broader portfolio bet on AI-native infrastructure plays continues at Exaforce, and the firm's participation gives the round a clean read on the AI-native architecture thesis rather than reading as a generalist enterprise-software investment. Seligman Ventures continuing from earlier rounds rounds out the cap table with strategic continuity.

CEO Ankur Singla's profile completes the founder-and-financing picture. Singla co-founded the company roughly three years ago, took it from concept through a $75 million Series A in early 2025, launched commercially in Q4 2025, and has now closed the Series B nine months post-launch. That sequencing is unusual in cyber — typical SecOps startups season for two to three years post-launch before raising a Series B of this size — and reflects the cap-table consensus that the early customer signal warrants accelerated capital deployment rather than measured patience.

Exaforce versus Dropzone, Prophet Security, and 7AI

The agentic SecOps startup category has three other named competitors in mid-2026: Dropzone AI, Prophet Security, and 7AI. Each company is positioned slightly differently along the autonomy spectrum and the workflow coverage spectrum, and procurement teams running a multi-vendor evaluation should understand the structural differences before running RFPs. Dropzone AI has been the longest-tenured of the three competitors and emphasizes the "AI SOC analyst" framing — an autonomous agent that operates inside the customer's existing SIEM-and-SOAR workflow rather than replacing the underlying detection stack. Prophet Security positions closer to Exaforce on the autonomous-investigation axis, with a similar emphasis on agent-driven triage and natural-language hunting. 7AI is the newer entrant and has been emphasizing the AI-native runtime claim more aggressively than the workflow-attachment claim.

The Exaforce $725 million valuation now sets the implicit ceiling for the segment. Competitors will face procurement comparison questions that anchor against the Exaforce funding, valuation, customer count, and architecture claims, and the answer to "why are you not at Exaforce's valuation" will be the first question every Series B prospect in the segment fields for the next four quarters. Dropzone, Prophet, and 7AI will need to address the comparison directly — either by surfacing a comparable enterprise-validation metric (named regulated-industry customers, named developer-infrastructure customers, comparable autonomous-task-reduction claims), or by positioning around a different architectural archetype that the Exaforce round did not anchor.

The incumbent vector is where the most consequential competitive analysis sits. CrowdStrike's Charlotte AI agentic features, Palo Alto Networks' Cortex XSIAM agentic capabilities, and the broader EDR-plus-AI category attach AI workflows to platforms with established customer bases, mature compliance certifications, and integrated identity into existing enterprise security stacks. The structural question is whether the agentic runtime is better delivered as a feature attached to a mature EDR or SIEM, or as a dedicated platform that pulls procurement budget on its own. The Exaforce round is the cleanest argument to date that the dedicated-platform answer has investor consensus, but the next 12 to 24 months of customer wins versus losses against the incumbents will determine whether the consensus holds.

Readers evaluating the comparison should also see our coverage of the OpenAI EU Cyber Action Plan and the GPT-5.5 Cyber versus Anthropic Mythos positioning, our coverage of the OpenAI Daybreak cybersecurity platform and Glasswing response, and the supply-chain attack postmortem in PyTorch Lightning Shai Hulud malware. The frontier-model cyber posture and the supply-chain-attack threat-model both shape what an agentic SecOps platform needs to handle to be procurement-credible in mid-2026.

The Japan and Europe expansion and the global SOC TAM

The Japan and Europe expansion announcement is the clearest signal that the agentic SecOps thesis is being priced as a global infrastructure play rather than as a US-market product. Japan in particular is structurally interesting for cyber automation: the country has a documented SOC staffing shortage, a high proportion of enterprise IT budget allocated to security compared to global benchmarks, and a regulatory environment (METI guidelines, financial-services cyber rules, and the broader cybersecurity strategy refresh under the Kishida and Ishiba governments) that has been pushing enterprises toward documented incident-response capability. A platform that automates Tier-1 and Tier-2 SOC analyst workflows has unusually high pull in the Japan market for those structural reasons.

Europe is the second leg of the expansion, and the regulatory complexity is the gating factor that determines how fast the platform can scale across EU member states. GDPR data-handling rules, the NIS2 directive's incident-reporting requirements, the EU AI Act's high-risk-system categorization questions for autonomous cyber agents, and the Digital Operational Resilience Act (DORA) for financial-services customers all create a non-trivial compliance overhead that early-stage US cyber startups typically underestimate. The Exaforce expansion plan reads as an early bet that the agentic SecOps architecture is regulator-defensible — autonomous agents whose decisions are auditable, whose data flows are scoped to customer-controlled tenants, and whose containment actions can be configured to require human-in-the-loop approval where regulation demands it.

The TAM read on the Japan-plus-Europe expansion is structurally meaningful. The global enterprise cybersecurity market is approximately $250 billion in 2026 annualized run-rate, with the SOC-and-detection sub-segment estimated in the $40 to $60 billion range. If agentic SecOps captures 5 to 10% of that sub-segment over the next five years — a range consistent with the historical pattern of AI-native categories pulling share from incumbent workflows — the addressable revenue pool for Exaforce-and-comparable platforms is in the $2 to $6 billion range. The $725 million valuation prices the company at roughly 12 to 36% of the platform-leader share of that range, depending on the bullish-or-bearish read of the segment trajectory.

Why this round matters for security procurement teams

For security procurement teams in active evaluation of agentic SecOps platforms, the Exaforce round changes the evaluation rubric in three concrete ways. First, the $725 million valuation sets the implicit funding tier that competing startups will need to either match or explain. Dropzone, Prophet, and 7AI will face procurement questions that reference the Exaforce valuation as the segment anchor, and the procurement conversation now starts with the Exaforce comparison rather than ending with it. Vendors below the funding tier will need to surface comparable customer-validation or architecture-differentiation evidence to remain in evaluation shortlists.

Second, the autonomous-versus-assisted distinction now sits at the top of the evaluation taxonomy. Procurement teams evaluating agentic SecOps will be asked upfront whether they are evaluating fully autonomous agents (where Exaforce is the segment reference) or analyst-assist AI workflows (where the EDR and SIEM incumbents' agentic features cluster). The bifurcation reduces the chance of category-mismatched evaluations, which has historically been a source of stalled procurement cycles in cyber AI. Procurement teams can now run two parallel evaluations rather than one confused evaluation that conflates feature attachment with platform replacement.

Third, the manual-task-reduction percentage is now an explicit procurement criterion rather than an implicit one. Exaforce's "up to 90%" claim will propagate into RFPs and evaluation rubrics across the segment, and vendors whose comparable number is materially lower will need to address that gap explicitly. Vendors with comparable or superior numbers will use the Exaforce claim as the procurement anchor that turns RFP responses into head-to-head architecture comparisons. The procurement language has just become more concrete.

Why the timing of this round signals broader cyber AI category maturity

The May 12, 2026 announcement timing is itself a category-level signal worth reading. Cyber AI funding through 2024 and 2025 was characterized by frequent rounds at category-momentum valuation multiples — strong founding teams, frontier-model partnerships, and demo-driven narratives. The Exaforce round breaks that pattern in three ways. First, the funding-to-customer-validation ratio inverts: the round is anchored to a 20-customer base with two named regulated-vertical references (Replit, Guardant Health) and a projected 40-to-50 customer count by year-end. Most prior cyber AI rounds named customers as a marketing list rather than as a validation thesis. Second, the round arrives after the broader frontier-model cyber posture has consolidated to the point where the major frontier models (OpenAI's GPT-5.5 Cyber restricted access, Anthropic's Claude Security beta, the Glasswing-and-Mythos positioning conversation) have created a baseline of cyber-aware model capability that platform startups can compose into agentic runtimes rather than build from scratch. Third, the lead investor is an institutional growth-equity firm (HarbourVest) rather than a cyber-specialist firm, which signals the category is now legible to non-specialist capital allocators.

The category-maturity reading has implications for adjacent categories. The application-security agentic category — where AI-driven vulnerability scanning, application-security testing, and software-supply-chain monitoring sit — is roughly 12 to 18 months behind the SecOps agentic category on the same maturity curve. The same pattern that just played out in SecOps (frontier-model commoditization to platform layer to autonomous-runtime emergence to enterprise-validation event to generalist-capital lead at $700M+ valuation) is the pattern that will play out in application security over the next four to eight quarters. Investors and procurement teams tracking the broader cyber AI infrastructure stack should treat the Exaforce round as a leading indicator for the structural evolution of every cyber AI sub-category, including the supply-chain monitoring vector that the PyTorch Lightning Shai Hulud incident brought into sharp procurement focus.

The other category signal is the international-expansion timing. A nine-months-post-launch expansion into Japan and Europe is unusually aggressive for a US-headquartered cyber startup, and the willingness of the cap table to underwrite that expansion at Series B implies investor consensus that agentic SecOps is structurally less geographically constrained than incumbent EDR or SIEM categories. Competing startups will need to make analogous international decisions earlier in their funding trajectories, which will reshape the GTM playbook the category executes against over the next two to four quarters.

What could go wrong for Exaforce from here

The round is structurally strong but the post-round execution has three identifiable risk vectors worth tracking. First, the autonomous-action liability question. Agentic SecOps platforms that take autonomous containment actions — quarantining accounts, isolating endpoints, blocking traffic — operate against a regulatory and contractual surface where false-positive containment can create material customer-business impact. The architectural answer is policy-controlled autonomy with human-in-the-loop gates for high-impact actions, but the operational answer requires production-grade evidence that the policy controls work under adversarial conditions. The next 12 to 24 months of customer deployments will surface whether the Exabot architecture's autonomy boundaries hold up against the specific failure modes the segment will encounter at scale.

Second, the incumbent-attachment vector. CrowdStrike Charlotte AI, Palo Alto Networks Cortex XSIAM, and Microsoft Sentinel's Security Copilot all attach agentic features to platforms with established customer bases and integrated identity-and-billing into existing enterprise stacks. The structural question is whether procurement teams will displace incumbent platform contracts to bring in a dedicated agentic runtime, or whether they will prefer the agentic features the incumbent platforms ship as workflow attachments. Exaforce's 20-customer base in two quarters is the early evidence that the displacement path is viable, but the question is open at the broader segment level and the incumbents' product cycles will continue compressing the feature gap.

Third, the model-provider dependency. Exaforce's autonomous-agent architecture is built on top of frontier large language models that the company does not own — the same dependency structure that Claude-and-GPT-powered agentic platforms across the broader category face. If the frontier model providers materially shift their cyber-use-case pricing, restrict access to specific cyber capabilities, or vertically integrate into agentic runtimes themselves, the platform-layer economics for Exaforce shift. The risk is structurally manageable — model-provider switching at the agent-orchestration layer is non-trivial but tractable — but the strategic risk is real and worth monitoring across the next two to four model release cycles. The current dynamic, captured in our coverage of the GPT-5.5 Cyber restricted access announcement and the Q1 2026 frontier-AI funding concentration, sets the backdrop the platform layer has to navigate.

Strategic bottom line

The Exaforce $125 million Series B at a $725 million valuation is the cleanest enterprise-validation signal the agentic SecOps category has produced. The round is anchored to a 20-customer base built in roughly two quarters, two named regulated-vertical references (Replit and Guardant Health), a projected 40-to-50 customer count by year-end, an autonomous-agent architecture with a 90% manual-task-reduction headline claim, and a coordinated international expansion into Japan and Europe. That combination of facts is what the agentic SecOps segment has been missing across the prior funding cycles. Exaforce now occupies the implicit reference position in the segment, and the procurement conversation across the category shifts accordingly.

The cap table — HarbourVest leading with Peak XV, Mayfield, Khosla Ventures, and Seligman Ventures participating — covers four distinct strategic vectors: institutional growth-equity validation, global-expansion thesis, enterprise-infrastructure depth, and frontier-AI architecture conviction. That balance is the structural signal that the investor consensus has formed around agentic SecOps as a distinct value-capture layer in the cyber stack, separate from the EDR-and-SIEM workflow attachment layer where CrowdStrike and the incumbents continue to compete. The two segments will continue to evolve in parallel, and procurement teams will increasingly run separate evaluations against each segment rather than confusing the category map.

For SOC engineering teams, the immediate implication is that the autonomous-agent architecture — Exabot triage, investigation, and containment with natural-language hunting primitives — is now the production-deployment reference rather than an experimental architecture. For security procurement teams, the immediate implication is that the Exaforce $725 million valuation is the comparison anchor for every agentic SecOps evaluation through the rest of 2026. For competitors in the agentic SecOps segment, the immediate implication is that the platform-completeness bar has moved up, and the next round of competitive responses will need to address the operational scale (20 customers in two quarters), the architecture claims (90% manual-task reduction), and the international expansion footprint (Japan and Europe within nine months of launch) directly. The category just compressed around a clear leader, and the next three quarters will determine whether the lead consolidates or whether the incumbents close the gap.

Frequently Asked Questions

How much did Exaforce raise in its Series B and at what valuation?

Exaforce raised $125 million in Series B funding at a $725 million post-money valuation, announced on May 12, 2026. The round brings total capital raised to approximately $200 million across the seed, Series A, and Series B sequence completed in roughly one year. HarbourVest led the round, with Peak XV, Mayfield, Khosla Ventures, and Seligman Ventures participating alongside earlier-stage backers. The valuation puts Exaforce at the top of the agentic SecOps startup segment in mid-2026 and prices the company at roughly 3.6x total invested capital.

What does Exaforce actually do, and what is agentic SecOps?

Exaforce builds an agentic security operations platform: autonomous agents the company calls "Exabots" that handle Tier-1 and Tier-2 SOC analyst workflows including alert triage, investigation, containment recommendations, and incident reporting. The platform applies what the company describes as real-time AI cyber reasoning — continuous-streaming agent decisions that operate in seconds-to-tens-of-seconds latency budgets rather than the minutes-to-hours latency of traditional batch SIEM analytics. Natural-language query primitives — the company's "vibe hunting" framing — let analysts interrogate the threat surface without writing structured SIEM queries. Exaforce claims the platform reduces manual SOC analyst tasks by up to 90%.

Who are Exaforce's named customers and what verticals do they represent?

The public references in Exaforce's announcement coverage are Replit (developer infrastructure) and Guardant Health (regulated healthcare and clinical genomics). The two named accounts cover two of the highest-trust verticals in mid-2026 — Replit's security posture has to address the threat surface that AI-assisted code generation introduces, and Guardant Health's compliance posture covers HIPAA and clinical-genomics data-residency requirements among the strictest in cyber. The total signed customer count is 20 after roughly two quarters of commercial availability, with a projected 40 to 50 customers by year-end 2026.

Who leads Exaforce and what is the team profile?

Ankur Singla is CEO and co-founder. Singla took the company from concept through a $75 million Series A in early 2025, launched commercially in Q4 2025, and has now closed the $125 million Series B nine months post-launch. The funding-to-launch sequencing is unusual in cyber — typical SecOps startups season for two to three years post-launch before raising a Series B of this size — and reflects investor consensus that the early customer signal warrants accelerated capital deployment rather than measured patience. The company was founded approximately three years before the May 2026 Series B announcement.

How does Exaforce compare to Dropzone, Prophet Security, and 7AI?

Dropzone AI is the longest-tenured of the agentic SecOps startup competitors and emphasizes an "AI SOC analyst" framing that operates inside the customer's existing SIEM-and-SOAR workflow. Prophet Security positions closest to Exaforce on the autonomous-investigation axis, with similar emphasis on agent-driven triage and natural-language hunting. 7AI is the newer entrant and emphasizes the AI-native runtime claim more aggressively than the workflow-attachment claim. The Exaforce $725 million valuation now sets the implicit ceiling for the startup segment, and the three competitors will face procurement comparison questions anchored to Exaforce's funding, customer count, and architecture claims for the next four quarters.

How does Exaforce compare to CrowdStrike and Palo Alto Networks?

CrowdStrike Charlotte AI and Palo Alto Networks Cortex XSIAM are the leading incumbent platforms attaching AI agentic capabilities to EDR-and-SIEM stacks with established customer bases, mature compliance certifications, and integrated identity into existing enterprise security architectures. The structural question is whether agentic SecOps is better delivered as a feature attached to an incumbent platform or as a dedicated runtime that pulls procurement budget on its own. The Exaforce round is the cleanest argument to date that the dedicated-platform answer has investor consensus, but the procurement question remains open at the broader segment level. CrowdStrike and Palo Alto retain advantages on incumbency, brand trust, and integrated billing; Exaforce competes on autonomy depth and architecture purity.

Why does the cap table feature HarbourVest, Peak XV, Mayfield, and Khosla together?

Each name on the cap table represents a different thesis vector. HarbourVest brings institutional growth-equity validation — the kind of capital that prices rounds on cash-flow-discountable infrastructure metrics rather than category-momentum narratives. Peak XV brings the global expansion vector that the announced Japan and Europe rollout needs to support. Mayfield brings enterprise-infrastructure depth and a track record in earlier eras of SIEM and EDR investing. Khosla Ventures brings frontier-AI architecture credibility that anchors the agentic framing of the platform. Seligman Ventures continues from earlier rounds with strategic continuity. The four-firm strategic mix is structurally well-balanced for a Series B in cyber infrastructure.

Why is Exaforce expanding to Japan and Europe at Series B rather than later?

Japan is structurally pulled toward SOC automation by documented analyst-staffing shortages, a high proportion of enterprise IT budget allocated to security, and a regulatory environment under the Kishida and Ishiba governments pushing enterprises toward documented incident-response capability. Europe is gated on regulatory complexity around autonomous-agent decisions under GDPR, NIS2, the EU AI Act's high-risk-system categorization questions, and DORA for financial-services customers. The Exaforce expansion at Series B reads as an early bet that the agentic SecOps architecture is regulator-defensible and that the structural pull from Japan's staffing economics is strong enough to justify earlier-than-typical international GTM investment.

What is "vibe hunting" and how is it different from a SIEM query?

Vibe hunting is Exaforce's framing for natural-language threat investigation: an analyst describes the investigation in plain English ("show me lateral movement from finance-team accounts in the last 24 hours that touched the customer database"), and the platform translates that intent into the underlying data-source queries, correlates the results, and returns a structured investigation timeline. A traditional SIEM query requires the analyst to write a structured query in a vendor-specific query language (Splunk SPL, Sentinel KQL, Elastic ES|QL, and so on). The natural-language primitive collapses the analyst training overhead that vendor-specific query languages impose and is one of the cleanest agentic primitives in the current SecOps category.

What are the biggest risks to Exaforce's position from here?

Three risks worth tracking. First, the autonomous-action liability question — agentic SecOps platforms that take autonomous containment actions operate against a regulatory and contractual surface where false-positive containment can create material customer-business impact, and the next 12 to 24 months will surface whether the Exabot architecture's autonomy boundaries hold under adversarial conditions. Second, the incumbent-attachment vector — CrowdStrike Charlotte AI, Palo Alto Cortex XSIAM, and Microsoft Sentinel Security Copilot attach agentic features to mature platforms with integrated identity and billing, and procurement teams may prefer feature attachment over platform replacement. Third, the model-provider dependency — Exaforce's agents are built on frontier large language models the company does not own, and frontier-model pricing shifts or vertical-integration moves into agentic runtimes would shift the platform-layer economics.

How does this round affect cyber procurement teams currently evaluating AI platforms?

The round changes the evaluation rubric in three ways. First, the $725 million valuation sets the funding tier that competing agentic SecOps startups will need to either match or explain in procurement conversations. Second, the autonomous-versus-assisted distinction now sits at the top of the evaluation taxonomy, reducing the chance of category-mismatched evaluations between fully autonomous platforms like Exaforce and analyst-assist AI workflows from incumbent EDR and SIEM vendors. Third, the "up to 90% manual-task reduction" claim becomes an explicit procurement criterion that vendors with comparable or lower numbers will need to address directly in RFP responses. Procurement language across the segment becomes more concrete.

What should security teams and SOC engineers do with this information?

For SOC engineering teams evaluating where to invest agentic AI effort, the Exaforce round is a signal that the autonomous-agent runtime segment has reached enterprise-validation maturity and that production-grade Tier-1 and Tier-2 SOC automation is a documented procurement category rather than a speculative one. SOC teams already piloting agentic platforms should treat the round as validation that the platform-layer roadmap will be funded through the next two to three product cycles. SOC teams on alternative startup platforms should evaluate competitive responses to the Exaforce case study and the autonomous-task-reduction positioning over the next two to four quarters. SOC teams still relying on incumbent EDR-plus-AI workflow attachments should evaluate whether the dedicated agentic runtime segment is the right architectural choice for their production-incident-response use cases, with reference to the frontier-model cyber posture captured in the Anthropic Claude Security beta and OpenAI EU cyber action plan coverage.