Q1 2026 just rewrote the venture capital playbook. Global VCs deployed $300 billion across roughly 6,000 startups between January and March 2026, an unprecedented +150% quarter-over-quarter jump versus Q4 2025 and +150% year-over-year versus Q1 2025, according to Crunchbase News. Frontier AI labs absorbed the dominant share, with mega rounds clustering around a handful of names: Anthropic ($40B from Google), Project Prometheus ($10B from Bezos), Cursor ($2B at $50B), AMI Labs ($1.03B seed led by Yann LeCun), Harvey ($200M at $11B), and DeepSeek talks with Tencent and Alibaba above $20B. The Top 10 deals alone account for an outsized portion of the total. We are no longer in normal venture territory.

The numbers: what $300 billion in 90 days actually looks like

Three hundred billion dollars in a single quarter is a number that does not have many real-world analogues. It is roughly equivalent to the entire annual GDP of Finland, or the combined market capitalization of Citigroup and Goldman Sachs as of early 2026. It is more than US venture capital deployed in any single full year before 2021. Crunchbase News, which tracks global venture funding through its proprietary database of investor disclosures and SEC filings, reported the figure on April 2, 2026, and within a week analysts at PitchBook, Bloomberg, and the Financial Times had cross-confirmed the order of magnitude.

The 6,000-startup figure is itself misleading if read superficially. The arithmetic is brutal: $300 billion divided by 6,000 companies yields an average check of $50 million per startup. But the median is far smaller than the mean, because the distribution is severely top-heavy. Our reading of the Crunchbase dataset suggests that the Top 10 deals alone represent somewhere between $90 billion and $110 billion of the total — meaning roughly 30 to 35% of the entire quarter's capital flowed into ten companies. The remaining 5,990 startups split the rest, which still leaves an extraordinary $190B+ for traditional Series A through C, but the headline is unambiguous: this is a barbell market.

For comparison, the prior all-time quarterly record was Q4 2021, during the late stages of the zero-rate-policy bubble, at approximately $180 billion. Q1 2026 beat that by roughly $120 billion, or 67%. Q4 2025 came in at around $120 billion. Q1 2025 was $120 billion. The +150% delta on both axes is not a typo; it reflects the genuine step-change that occurred in the first three months of this year.

QoQ and YoY in historical context

To understand how unusual a 150% QoQ jump is, consider that since 2010, quarterly venture funding has changed by more than 50% in either direction only six times. The 2021 bubble saw QoQ growth of roughly 30% to 60% during peak quarters. The 2022 crash saw QoQ declines of 30% to 45%. A QoQ of +150% on a base that was already historically elevated is, mathematically and behaviorally, an outlier event of the kind we associate with regime change rather than seasonal variation.

Three forces explain the magnitude. First, frontier AI lab valuations have decoupled from traditional venture math; we cover that in the next section. Second, sovereign wealth funds, hyperscalers, and corporate balance-sheet investors (Google, Microsoft, Nvidia, Amazon, Tencent, Alibaba) are deploying capital at velocities that conventional limited partners cannot match. Third, and most importantly, the perceived strategic risk of not investing in frontier compute and frontier models has reached the point where capital allocators are paying ahead of clarity. That last force is the bubble warning sign we will examine below.

Concentration: how the Top 10 absorbed a third of the quarter

The Top 10 picture is the story. Below is our reconstruction of the largest known Q1 2026 venture rounds, based on Crunchbase News, public filings, and reporting from The Information, Bloomberg, the Financial Times, and Reuters.

- Anthropic — approximately $40 billion in primary investment from Google at a roughly $350 billion valuation, ahead of an October 2026 IPO target. Single largest private capital injection of the quarter.

- Project Prometheus — $10 billion led by Jeff Bezos and partners for a stealth physical-world-model AI lab competing with PhysicalIntelligence, Skild, and Figure AI.

- DeepSeek — Tencent and Alibaba in talks for a stake at a $20B+ valuation (initial $10B doubled within 48 hours of investor inbound), final round size pending.

- Cursor — $2 billion led by Andreessen Horowitz at a $50 billion valuation, alongside reported plans to train an in-house frontier model.

- AMI Labs — $1.03 billion seed round led by Yann LeCun, the largest seed round in venture history, dedicated to world-model AI.

- Harvey AI — $200 million at an $11 billion valuation, the highest-valued vertical AI legal application.

- xAI — undisclosed strategic round amid the SpaceX merger discussion at a combined $1.25 trillion theoretical entity valuation.

- Mistral — reported European sovereign-AI raise estimated in the $3 billion to $5 billion range; final figures pending official confirmation.

- Suno — strategic round to fund the v5.5 release and the audio frontier-model expansion; figures undisclosed.

- Starcloud — $170 million Series A for orbital AI data centers, a category that did not exist 18 months ago.

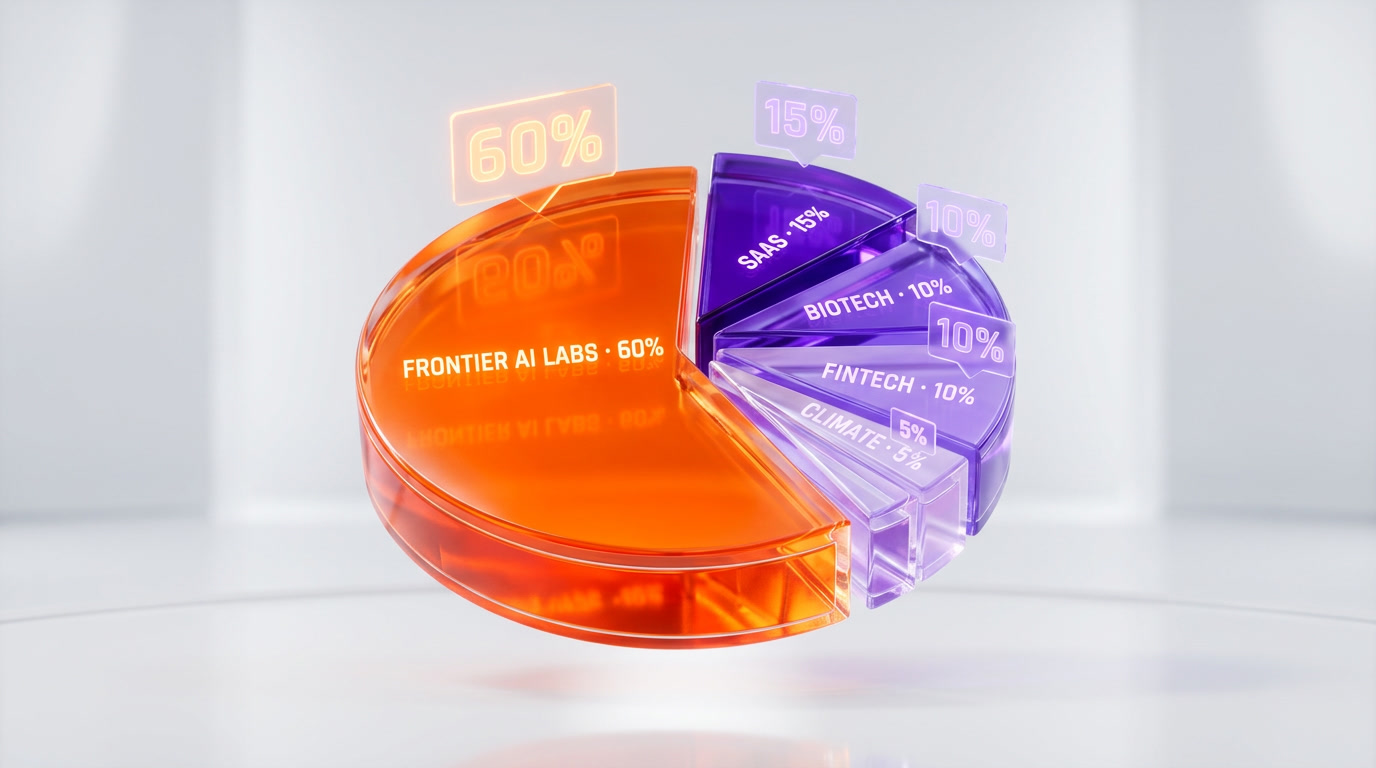

That list is not exhaustive. Mid-quarter rounds at MiniMax ($30B+), Moonshot ($18B), Zhipu ($50B+), and a half-dozen US frontier-model labs round out the picture. But the structural fact is unmistakable: roughly 60% of frontier-AI-tagged capital went to companies that did not exist five years ago, and the other 40% went to organizations that were sub-$10 billion valuations as recently as 2024.

What this means for classic Series A through C

Series A through C founders outside of frontier AI are facing an increasingly bimodal market. On one hand, the absolute dollars available to non-AI rounds is still up year-over-year — that $190 billion residual is no small pool. On the other hand, the bar to clear has risen because investors have visible alternatives offering apparent power-law returns. A pre-revenue SaaS Series B at $80 million now competes for the same partner attention as a $500 million strategic check into an AI infrastructure vertical. The implicit hurdle rate inside venture firms has reset upward.

We are seeing this play out in three patterns. First, traditional SaaS rounds are taking 30 to 50% longer to close than they did in Q1 2024. Second, valuations outside frontier AI are flat to slightly down — there is no spillover bubble. Third, founders who can credibly position their company as "AI infrastructure-adjacent" are commanding a 1.5x to 2x valuation premium, even when the underlying business is unchanged from twelve months ago. That premium is not a bug; it is the rational market response to where capital wants to go.

Mega rounds in detail: Anthropic, Prometheus, Cursor, AMI Labs

The four rounds that anchor the quarter deserve individual treatment because each represents a distinct strategic logic, and together they explain how $300B got deployed in 90 days.

Google's $40B into Anthropic at $350B

The Google investment into Anthropic is the marquee transaction of the quarter and arguably of the decade. The structure, as reported by The Information and confirmed by Bloomberg, involves $40 billion in primary capital at a $350 billion post-money valuation, with the round serving as the de facto pre-IPO bridge ahead of a planned October 2026 listing. The implied IPO target valuation is in the $700 billion to $800 billion range. The IPO context is detailed in our breakdown of why Anthropic's $800B IPO target now beats OpenAI on revenue. For the parallel scale of strategic AI capital concentration, see our analysis of the xAI-SpaceX merger discussion at a $1.25 trillion combined entity valuation.

The strategic read is that Google is buying optionality on a model lab whose research output is increasingly indispensable to its own roadmap, while Anthropic gains the compute commitments and the equity float necessary to support its IPO. Neither side wanted a full acquisition because both regulatory and cultural barriers make that path impassable. The minority strategic round is the cleanest available structure, and at $40 billion it sets the gold standard for what frontier-lab rounds look like in 2026.

Bezos's $10B into Project Prometheus

Project Prometheus is the most enigmatic round of the quarter. Bezos personally led a $10 billion raise into a stealth lab focused on physical-world models — robotics foundation models, embodied reasoning, and what the lab's leaked memo calls "the locomotion layer of artificial intelligence." Our full analysis is in Jeff Bezos's Project Prometheus and the $10 billion physical-world-models bet.

The signal here matters more than the dollars. Bezos has been comparatively absent from the AI capital wave; his decision to deploy $10 billion personally, into a category (physical AI) that is at most twelve months away from contested public attention, suggests a thesis that the next frontier of foundation models is not text or video but physical interaction. If correct, the entire robotics-foundation-model category is about to enter the same hyper-funded loop that text models entered in 2023.

Cursor's $2B at $50B with in-house model

Cursor's $2 billion round is the most aggressive vertical-AI mega round of the quarter. At $50 billion, the company is now valued above every other developer-tools company in history, including the all-time peaks of Atlassian, GitHub at acquisition, and JetBrains. The strategic kicker, as we covered in Cursor at $50B valuation and the in-house model strategy, is the announcement that Cursor will train and ship its own frontier model in 2026, ending the Anthropic-only dependency.

This is the canary for vertical AI. If Cursor at $50B can credibly fund a frontier-model program, every category leader in vertical AI — Harvey for legal, Sierra for support, Glean for enterprise search, Hippocratic for healthcare — has a roadmap to do the same. Capital intensity in vertical AI is about to enter a phase that resembles 2023's frontier model arms race, except it will play out across a dozen specialized verticals simultaneously.

AMI Labs $1.03B seed (LeCun)

AMI Labs's $1.03 billion seed is the largest seed round in the history of venture capital, and it was led by Yann LeCun on a thesis that text-only foundation models have hit a wall and that world models — Joint Embedding Predictive Architectures, V-JEPA, and their successors — are the next architectural primitive. Our deep dive: AMI Labs's $1B seed round and the case for world models.

A $1B seed is, on its face, a financial absurdity. It is also a rational response to a specific market condition: if you believe a researcher of LeCun's caliber genuinely intends to ship a non-LLM frontier paradigm, the cost of not being on the cap table is asymmetric. Investors did not write $1.03B because they have validated the thesis; they wrote it because the option value of the thesis being correct dominates the downside. That is the same logic that Bezos applied to Prometheus, and it is the logic that increasingly explains the entire quarter.

Vertical AI: Harvey, Sierra, and the next layer

While frontier labs absorbed the headlines, vertical AI applications absorbed an enormous secondary layer of capital. Harvey AI's $200 million round at an $11 billion valuation is the canonical example. Harvey is a legal-AI platform with concrete enterprise revenue, real customer deployments at top-tier law firms, and a clean revenue-to-valuation ratio relative to the frontier-lab cohort. At $11B, Harvey is priced at roughly 40 to 60 times forward revenue, which by SaaS standards is rich but by frontier-AI standards is conservative.

The vertical-AI category cleared roughly $40 billion to $50 billion in Q1 2026, by our reckoning. That includes Harvey, Sierra, Glean, Hippocratic, Decagon, Crescendo, and another dozen sector specialists in healthcare, finance, defense, and education. The investor logic is straightforward: frontier models are increasingly commoditized at the API layer; the durable margin lives in the application layer where domain expertise, compliance, and workflow integration create defensibility. We expect this category to absorb a growing share of the quarterly total throughout 2026.

Geopolitical drivers: the US-China AI race accelerates capital

The US-China dynamic is the macro driver that explains why capital deployment has accelerated rather than rationalized. Three vectors matter.

First, the export-controls regime imposed on Nvidia H200 and Blackwell-class GPUs in 2024 and tightened in 2025 has produced a parallel Chinese frontier-AI capital pipeline. Tencent and Alibaba's reported talks with DeepSeek at $20B+, MiniMax at $30B+, Moonshot at $18B, and Zhipu at $50B+ represent the Chinese-side response. Beijing-aligned capital is deploying with urgency precisely because Chinese labs cannot procure top-end Western compute at scale, which paradoxically increases the strategic value of any Chinese frontier lab that can ship competitive results despite the constraint.

Second, the US side is responding with what we have called elsewhere "compute-as-foreign-policy." The $1 trillion Nvidia Vera Rubin order book unveiled at GTC 2026 is functionally a national industrial strategy with private balance sheets bearing the cost. Hyperscalers are pre-buying capacity through 2028 because the strategic risk of capacity shortfall now exceeds the financial risk of overprovisioning.

Third, the orbital and energy-frontier categories have received their first major checks. Starcloud's $170M Series A for orbital AI data centers and the wave of energy-efficiency research, including MIT's waste-heat analog computing breakthroughs, signal that the infrastructure layer below frontier models is itself becoming a fundable category. Compute, energy, and orbit are the new triad.

Bubble warning, or new era? The honest comparison

The question every honest analyst is asking, and that we have to answer here, is whether $300 billion in 90 days is the start of a sustainable infrastructure cycle or the late-2026 echo of a 1999-style bubble. Our verdict is mixed, and we will explain why.

The dot-com parallels worth taking seriously

Three structural similarities to the 1999-2000 era are real and undisputed. One: capital is flowing at velocities that exceed the operational capacity of the funded companies to deploy it productively. AMI Labs raised $1.03B seed; the company will not spend $1B on R&D in its first 24 months under any plausible assumption. Two: public-market enthusiasm is leaking into private markets, with secondary tender offers at frontier labs trading at 1.4x to 1.8x recent primary marks, mirroring the late-1999 secondary frenzy. Three: there is genuine fraud in the system. The Cluely CEO admission of fabricating $7M ARR in front of Andreessen Horowitz is an unambiguous late-cycle signal. When founders feel pressure to fabricate metrics to keep up with peer rounds, the cycle has entered a phase where price discovery has decoupled from fundamentals.

The dot-com cycle peaked in March 2000 and bottomed in October 2002, and the path between those points wiped out roughly 80% of public market AI-adjacent valuations. A 2026 correction of similar amplitude would erase $1.5 trillion to $2 trillion of paper wealth in venture and adjacent public markets. That is the downside scenario, and ignoring it would be irresponsible.

Why this might not be a bubble after all

The counter-argument is structural, and we find it more persuasive than the bubble case for one specific reason: the underlying technology is generating measurable productivity gains in production deployments today. In 1999, the median dot-com had no revenue and no path to revenue; it was an ad-funded category in search of a market. In 2026, the median frontier-AI customer is a Fortune 500 enterprise reporting genuine cost reductions in customer support, software engineering, document review, and content production. Anthropic alone is reportedly tracking $8B+ in annualized revenue. OpenAI is in a similar order of magnitude. Cursor's revenue ramp is verified. Harvey's enterprise traction is contractually disclosed.

The second counter-argument is that the compute infrastructure being built is not speculative — it is being consumed faster than it is being produced. Hyperscaler cap-ex tied to AI workloads is running at $200B+ annually, and utilization rates on frontier-class clusters are at 90%+ according to disclosed metrics from Microsoft Azure and Google Cloud. That is the opposite of the dark-fiber problem of 2001, when the telecom buildout ran 10x ahead of demand.

The third counter-argument is geopolitical. A bubble assumes that capital is irrationally responding to a fad. The US and China are not in a fad; they are in an accelerated industrial-policy race for what both governments believe is the most strategically significant technology of the 21st century. That race does not care about valuations and does not pause for price corrections.

Our verdict: a bifurcated market

We expect Q1 2026 to be remembered as the inflection point where venture capital split into two markets that no longer trade on the same logic. The frontier-AI cohort — labs, vertical applications, infrastructure — will continue to attract record capital through 2026 and likely into 2027, propelled by the geopolitical race and the genuine technological gains. Some of these companies will deliver returns that justify their entry prices; others will not, and the spread between winners and losers will be unusually wide even by venture standards.

Outside that cohort, traditional venture is reverting to discipline. Series A and B rounds in non-AI categories are being priced more conservatively than at any point since 2019. That bifurcation is healthy and rational. The danger is not the broad cycle; the danger is the specific subset of frontier-AI-adjacent rounds where deployment capacity does not match capital intensity. AMI Labs at $1B seed is the canonical case, and the test will be whether LeCun's team can absorb that capital productively over 36 months. If they can, it sets a new standard. If they cannot, it becomes the case study that defines the next correction.

What comes in the next 12 months

We project four major dynamics through Q1 2027.

First, the IPO window opens hard in Q3 and Q4 2026. Anthropic's October target is the marquee event, with an implied $700B-$800B listing. OpenAI is expected to follow within six months. Cursor, Harvey, and Glean are all viable 2027 IPO candidates. The volume of late-stage AI capital backing up behind the IPO window is creating a queue that, once opened, will move enormous amounts of paper into public markets. That public-market liquidity event is the key external risk to private valuations: if early IPOs trade poorly, every private mark inflates accordingly.

Second, consolidation accelerates. The mid-tier of the frontier-lab market — labs at $5B to $30B valuations that cannot self-fund a 2027 frontier compute build — will face acquisition or shutdown decisions. We expect 5 to 10 mid-tier consolidation events through Q1 2027, with hyperscalers, large defense primes, and the top three labs as the most likely buyers. The Manus situation, where China blocked the Meta acquisition, is a preview of the geopolitical complexity these deals will face.

Third, the vertical-AI category fragments and re-aggregates. We expect Harvey, Sierra, Glean, and Hippocratic to remain independent, but the long tail of vertical-AI startups — currently several hundred companies in the $20M to $200M revenue band — will compress into 30 to 50 dominant verticals through M&A. The pattern is the same as the SaaS consolidation of 2015-2018, except faster and at higher valuations.

Fourth, capital intensity in compute infrastructure increases. The Vera Rubin order book, the orbital data-center category, the energy-efficiency research wave, and the announced reactor-on-site programs at Microsoft, Google, and Amazon all converge on a single fact: the AI infrastructure buildout is not slowing in 2026 and will not slow in 2027. The corollary is that the capital absorbed by frontier labs is matched by an equally large capital flow into the picks-and-shovels layer below them. Both flows are real, both are large, and both are pointed in the same direction.

How to read this quarter as an operator

If you are running a startup outside frontier AI, the operational read is to focus relentlessly on capital efficiency. The era when growth-at-any-cost was rewarded by venture markets is over outside the AI cohort. Conserve runway, hit revenue milestones cleanly, and assume your next round will be priced more conservatively than you would like. The good news is that the residual $190B in the quarter still flowed into thousands of non-AI companies; capital is available, but it is more disciplined.

If you are operating in frontier or vertical AI, the read is the opposite. The window to raise large primary capital at growth-stage valuations may not be wider than it is right now. Operators in this cohort should consider raising more than they think they need, on cleaner terms than they would historically accept, because the optionality of having $200M in the bank during a market correction far exceeds the cost of taking modest dilution today. The historical precedent is 1999, when the companies that raised aggressively in the late stages of the bubble survived the crash, and the companies that conserved dilution did not.

For investors, the test of this quarter will not be the entry prices but the discipline at exit. The bifurcation we described above means that the dispersion of returns inside the AI cohort will be unusually wide. Picking the right ten frontier-AI bets will produce 50x to 100x outcomes; picking the wrong ten will produce zeros. Diversification within the cohort matters more than diversification across categories.

The bottom line

Q1 2026 is the largest venture quarter in history. $300 billion across 6,000 startups, +150% on both QoQ and YoY axes, with concentration on frontier AI labs at a level that no single quarter has ever produced. The two competing interpretations — late-cycle bubble or early-cycle infrastructure boom — both contain truth. The honest read is that the cycle has bifurcated into two distinct markets that no longer trade on the same fundamentals, and the next twelve months will determine whether the frontier-AI cohort delivers returns that justify the entry prices or whether the inevitable correction wipes out the marginal late-stage rounds that absorbed capital faster than they can deploy it productively.

We expect both outcomes simultaneously. The top quartile of the frontier-AI cohort will outperform any prior venture vintage. The bottom half will produce zeros at a rate that even seasoned investors find painful. The middle will be a noisy mass of acquihires, recapitalizations, and quiet wind-downs. That is what the largest venture quarter in history actually means: an outsized barbell of outcomes that will make the headlines in 2027 and 2028 either the celebration of a once-in-a-generation infrastructure buildout, or the cautionary tale of late-cycle excess. Possibly both, in adjacent quarters.

For now, the data is what it is. $300 billion. 90 days. 6,000 companies. +150%. Read it carefully. The next move is everyone else's.

Frequently asked questions about the Q1 2026 venture funding record

How much venture capital was deployed in Q1 2026?

Approximately $300 billion was deployed across roughly 6,000 startups in Q1 2026, according to Crunchbase News reporting from April 2, 2026. This figure represents the largest single quarter in the history of venture capital, exceeding the prior record of approximately $180 billion set in Q4 2021 by roughly $120 billion or 67%.

What does +150% QoQ and YoY actually mean for Q1 2026 venture funding?

It means Q1 2026 deployed roughly 2.5x the capital of both Q4 2025 (around $120 billion) and Q1 2025 (around $120 billion). A 150% increase on both quarter-over-quarter and year-over-year axes is statistically rare; since 2010, quarterly venture funding has changed by more than 50% in either direction only about six times.

Which startups received the largest Q1 2026 rounds?

The largest disclosed rounds were Anthropic ($40 billion from Google at a $350 billion valuation), Project Prometheus ($10 billion led by Jeff Bezos), Mistral (estimated $3-5 billion European raise), Cursor ($2 billion at $50 billion led by Andreessen Horowitz), DeepSeek (in talks with Tencent and Alibaba above $20 billion), AMI Labs ($1.03 billion seed led by Yann LeCun), Harvey AI ($200 million at $11 billion), and Starcloud ($170 million Series A for orbital AI data centers).

How concentrated was Q1 2026 venture funding on frontier AI labs?

Our reconstruction suggests the Top 10 deals account for between $90 billion and $110 billion of the quarter's total, meaning roughly 30 to 35% of all capital flowed into ten companies. Roughly 60% of frontier-AI-tagged capital went to companies founded within the last five years, indicating extreme concentration on a small cohort of frontier model labs and vertical AI leaders.

Is the Q1 2026 venture funding record a bubble?

It is genuinely contested. Bubble parallels include capital flowing faster than companies can deploy it productively (AMI Labs raised $1.03 billion seed), public-market enthusiasm leaking into private secondary markets at 1.4-1.8x recent marks, and confirmed fraud cases like Cluely's CEO fabricating $7 million ARR. The counter-argument is that frontier AI is generating measurable productivity gains today, hyperscaler compute utilization is at 90%+, and the geopolitical US-China race is driving real industrial policy rather than speculative excess. Our verdict is bifurcated: bubble dynamics in late-stage marginal rounds, infrastructure-cycle dynamics in the top tier.

What is the largest seed round in venture history?

AMI Labs's $1.03 billion seed round, led by Yann LeCun and announced in Q1 2026, is the largest seed round ever recorded. It is dedicated to building world-model AI systems based on Joint Embedding Predictive Architectures, and represents a thesis that text-only foundation models have hit architectural limits.

How does Q1 2026 compare to the dot-com era of 1999-2000?

The structural parallels are real but partial. Three similarities apply: capital flowing faster than operational deployment capacity, public-market enthusiasm leaking into private secondary markets, and visible founder fraud (Cluely). Three differences apply: the underlying AI technology is generating measurable productivity gains in production today (unlike most 1999 dot-coms), hyperscaler compute is consumed faster than produced (opposite of the 2001 dark-fiber overhang), and the US-China geopolitical race is driving industrial-policy capital rather than retail-investor speculation.

What happens to Series A and B startups outside frontier AI in this market?

They face a bimodal market. Absolute capital available to non-AI rounds is still elevated (around $190 billion residual after frontier deals), but the bar to clear has risen because investors have visible alternatives offering apparent power-law returns. Traditional SaaS rounds are taking 30 to 50% longer to close than in Q1 2024, valuations outside frontier AI are flat to slightly down, and founders who can credibly position as AI-infrastructure-adjacent command a 1.5x to 2x valuation premium even when the underlying business is unchanged.

Why is Google investing $40 billion in Anthropic instead of acquiring it?

Two structural barriers prevent acquisition. First, antitrust regulators in the US and EU would block a Google-Anthropic merger given Google's dominance in AI and search. Second, Anthropic's cultural and research independence is core to its talent retention; an acquisition would trigger key-person departures. The minority strategic investment at $350 billion valuation is the cleanest available structure: Google secures compute commitments and equity exposure, Anthropic gains the capital runway for its October 2026 IPO target without losing operational control.

What are the four major dynamics expected through Q1 2027?

First, the IPO window opens hard with Anthropic's October 2026 listing as the marquee event. Second, consolidation accelerates with 5 to 10 mid-tier frontier-lab consolidation events expected. Third, vertical AI fragments and re-aggregates with Harvey, Sierra, Glean, and Hippocratic likely staying independent while the long tail consolidates into 30 to 50 dominant verticals through M&A. Fourth, capital intensity in compute infrastructure increases, with the Nvidia Vera Rubin trillion-dollar order book, orbital data centers, and on-site reactor programs all expanding.

How much did Project Prometheus raise and what is its strategic focus?

Project Prometheus raised $10 billion led personally by Jeff Bezos in Q1 2026. The lab is focused on physical-world models — robotics foundation models, embodied reasoning, and what its leaked memo calls "the locomotion layer of artificial intelligence." The strategic signal matters more than the dollars: Bezos has been comparatively absent from prior AI capital waves, so a $10 billion personal commitment into physical AI suggests strong conviction that physical interaction is the next frontier of foundation models.

What is the Top 10 deal contribution to Q1 2026's total?

The Top 10 disclosed and reported deals account for an estimated $90 billion to $110 billion of the $300 billion total, roughly 30 to 35%. The remaining 5,990 startups split approximately $190 billion. This concentration ratio is unusually high even by venture-capital standards, where the Top 10 typically accounts for 15 to 25% of quarterly volume in normal cycles.