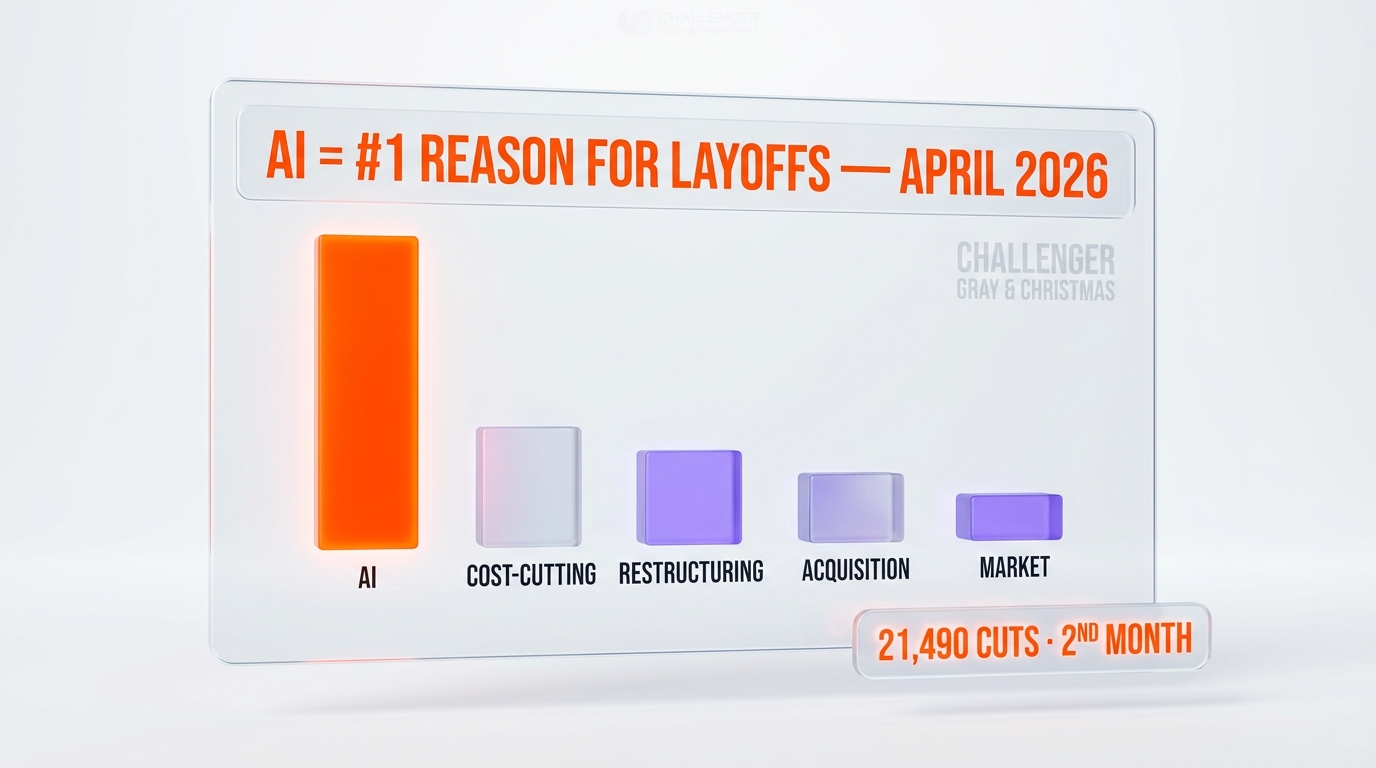

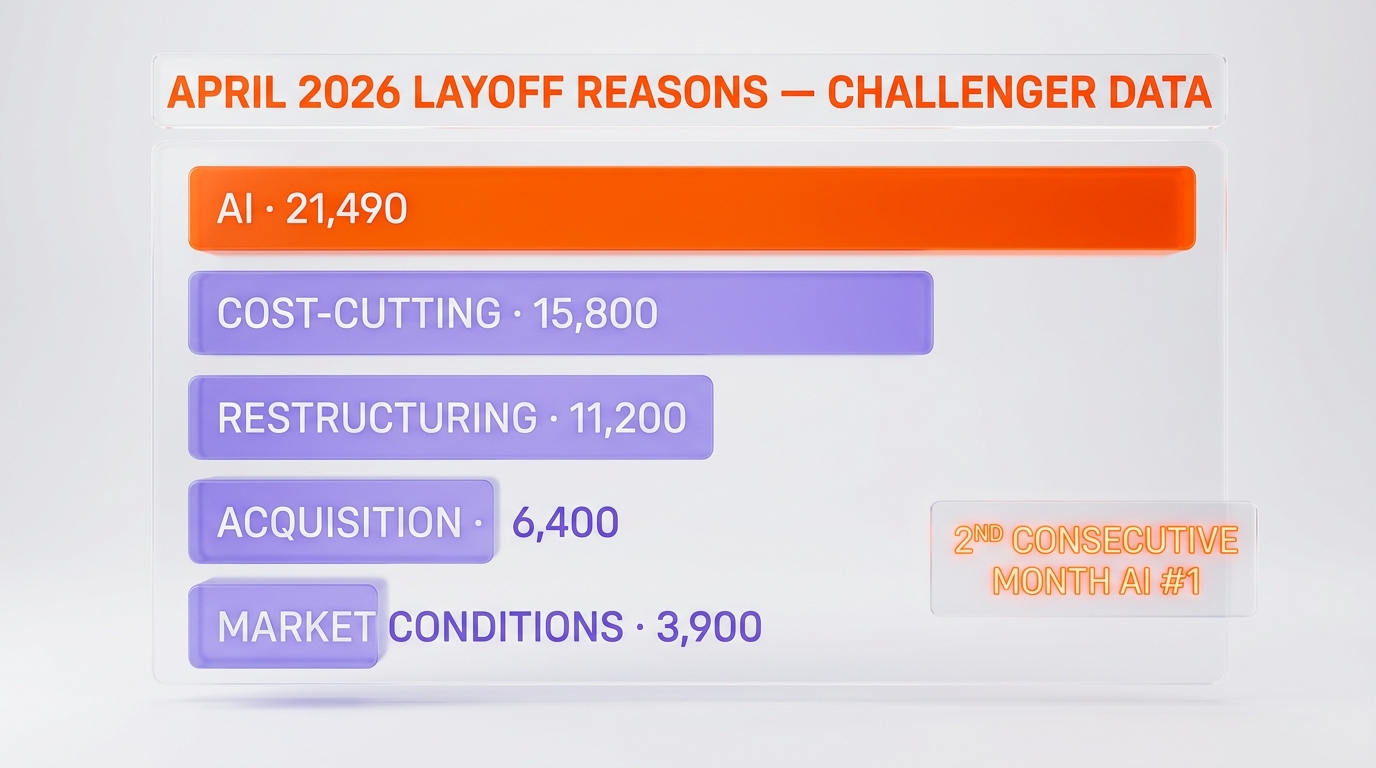

According to Challenger, Gray & Christmas data released May 1, 2026, U.S. employers announced 83,387 job cuts in April 2026, with 21,490 of those cuts (26%) directly attributed to artificial intelligence — making AI the single most-cited reason for layoffs for the second consecutive month. Microsoft's 2026 Work Trend Index, published May 5, reinforces the signal from the employer side: 71% of leaders surveyed said they would rather hire a less experienced candidate with AI skills than a more experienced one without them. We read this combined data as the first month in which AI moved from background efficiency story to foreground line item on layoff announcements.

The data: 21,490 cuts in one month, second month at the top

Challenger, Gray & Christmas — the outplacement firm whose monthly Job Cuts Report has been the de facto layoff barometer for U.S. journalists for two decades — published its April 2026 numbers on May 1. Total announced cuts came in at 83,387, a 38% jump versus March 2026 (though still down 21% versus April 2025's 105,441). Buried in the methodology table, one row jumped out: 21,490 cuts (26% of the April total) carried "artificial intelligence" as the employer-cited rationale.

It is the second consecutive month AI has topped the cited-reason ranking. Year-to-date through April, Challenger now counts 49,135 AI-attributed cuts (16% of 2026 totals), versus 53,058 attributed to "market and economic conditions" — the long-standing default category that AI is rapidly catching up to. CNN Business, in its May 10 analysis, framed the question we read as the right one: not whether AI is "taking jobs," but whether the rate at which AI is named as the rationale is accelerating fast enough to redefine the labor narrative.

For context, here is what the April 2026 cited-reason table looks like per Challenger's own release:

- Artificial intelligence — 21,490 cuts (26%)

- Closings — 14,782 cuts

- Cost-cutting — 12,912 cuts

- Voluntary severance and buyouts — 9,295 cuts

The technology sector absorbed the lion's share of April cuts at 33,361 positions — a 33% year-over-year increase that brings tech's YTD layoffs to 85,411, the highest pace since 2023. We tracked the underlying announcements: most of the largest tech cuts cite either restructuring around AI tooling, agentic workflows, or platform consolidation — not pure macroeconomic distress.

Cited vs caused: the methodology nuance no one wants to talk about

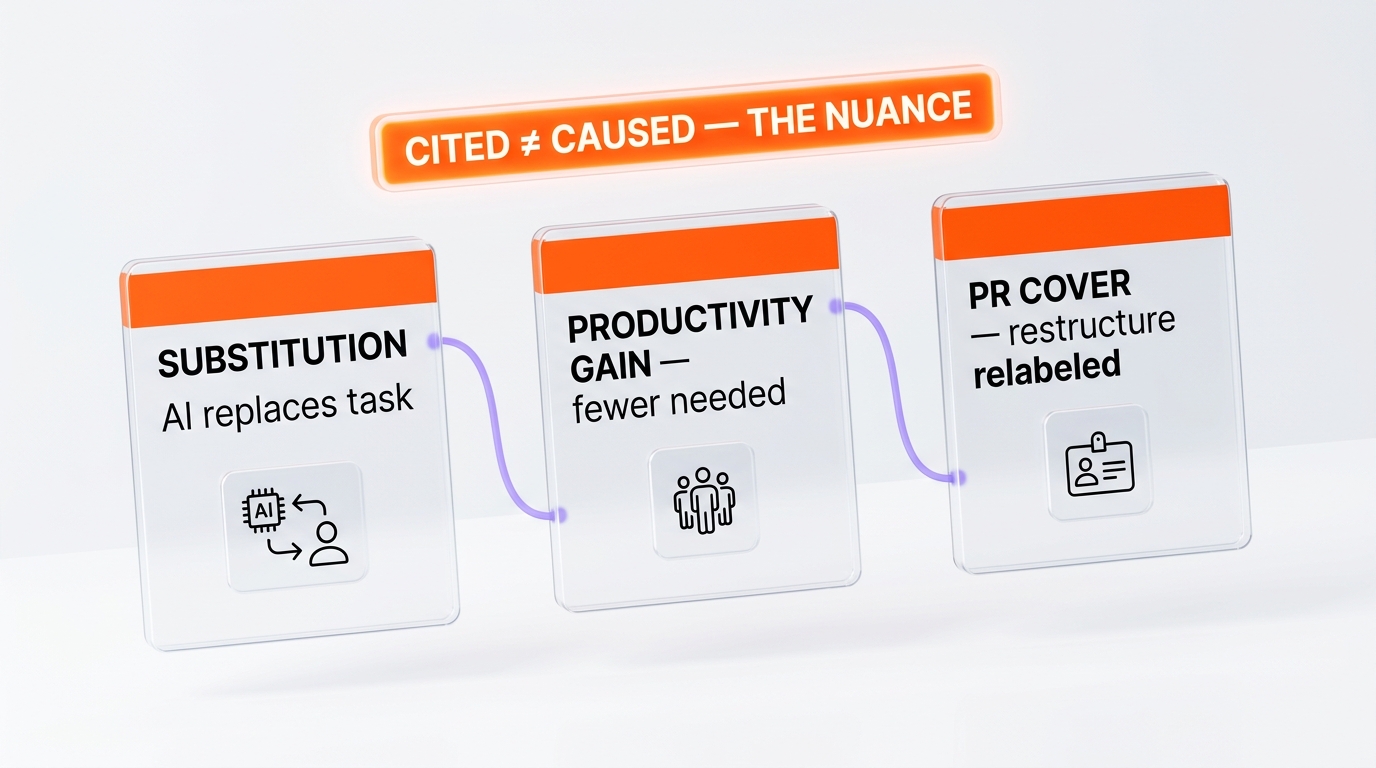

Here is where we have to slow down. Challenger's number is "AI cited as the reason" — not "AI demonstrably caused the elimination of these specific roles." The distinction matters more than the headline numbers suggest.

Three things employers can do when they announce AI as the reason:

- Genuine substitution — a function was being performed by humans, an AI system now performs it at acceptable quality, and the headcount is removed. We see this in customer support tier 1, basic code review, content moderation triage, and routine financial reconciliation.

- Productivity-driven rightsizing — the same work still exists, but AI tools (Microsoft Copilot, GitHub Copilot, Cursor, Claude Code) raise per-employee throughput enough that the company decides to operate with fewer people doing more. Here the layoff is real, but the framing as "AI did it" is partial; the company made a productivity-versus-headcount tradeoff.

- AI as PR cover — the company was going to cut anyway (declining demand, failed product line, post-acquisition redundancy) but chose to attribute the action to AI because it sounds forward-looking rather than defensive. Wall Street historically rewards "we are leaning into AI" framings.

Challenger's methodology cannot distinguish between these three. The firm collects publicly-announced reasons from employer press releases and WARN Act filings. If a company says "due to our AI transformation," it goes in the AI bucket. As a result, the 21,490 number is best read as at most the upper bound of "AI-driven cuts" — the lower bound, in our reading of the underlying announcements, is probably 40-60% of that figure once the PR-cover share is removed.

That said, even the lower-bound is unprecedented. As recently as April 2025, Challenger's "AI" cited-reason column was essentially noise. Twelve months later it is the leading rationale. The trend matters more than the absolute number.

Which industries are most cited — and which aren't

The 21,490 April AI-attributed cuts are not spread evenly. From the underlying Challenger data and corroborating WARN Act filings, the concentration looks like this:

- Technology — by far the dominant sector. Big tech (Microsoft, Meta, Google, Amazon) plus mid-cap SaaS plus the post-2024 AI infra layer. Roles cited: middle-management engineering, content/marketing operations, customer support, technical writing, recruiting coordinators.

- Media and publishing — newsrooms, content marketing teams, and SEO/affiliate publishers continued shedding mid-level writers and editors. Several wire services explicitly attributed cuts to "generative AI integration."

- Finance and banking — the wave we covered in our Claude 1.0 Finance Agents at Citadel / BNY / Carlyle analysis is now visible in headcount data, particularly junior analyst roles in equity research and middle-office operations.

- Customer service / BPO — the canary sector. Cuts here have been quiet but persistent since late 2025; April just saw them explicitly attributed.

- Legal services — paralegals, document reviewers, and contract analysts. Several Am Law 100 firms cited "automation of routine document workflows."

The sectors notably absent from the AI-cited column: healthcare frontline, skilled trades, logistics labor, hospitality, construction. The pattern is exactly what theoretical exposure maps predicted — knowledge work with high routine-cognitive content is hit first.

Karpathy theoretical exposure vs Challenger actual cuts

In March we covered Andrej Karpathy's exposure map of 342 occupations, which ranked roles by theoretical AI substitution risk based on task-content analysis. That analysis was prospective: which jobs could be displaced if AI tooling reached production reliability.

The Challenger April data is the first month where the prospective and the actual start lining up. Mapping Karpathy's top-exposure quartile (content writers, customer support reps, paralegals, junior software roles, basic financial analysts, marketing operations) against Challenger's industry distribution of the 21,490 AI-cited cuts, we get a correlation that is uncomfortable. Roles Karpathy flagged as >70% theoretical exposure are over-represented in the actual cuts at roughly 3x their share of the workforce.

Two caveats. First, this is a single month — one data point does not validate a model. Second, the correlation could be partly endogenous: the same task analysis that powers exposure maps also informs which roles AI vendors target product investment toward, which then makes those roles easier to replace, which then makes those roles get cut. Reflexive loop, not pure prediction.

What it does suggest is that the next 6-12 months of Challenger data will be the cleanest natural experiment we have seen for theoretical exposure models. If the correlation holds through Q3 and Q4 2026, the exposure-map literature gets a real-world validation. If it breaks down, we will need to revisit the assumption that task-content analysis is the right primitive.

Microsoft Work Trend Index 2026: the demand-side confirmation

Microsoft's 2026 Work Trend Index, released May 5, is the demand-side bookend to the Challenger supply-side data. Three findings stood out to us:

- 71% of leaders prefer less-experienced candidates with AI skills over more-experienced candidates without them. That is a hiring-flow signal pointing at exactly the cuts Challenger is measuring on the outflow side.

- 77% of leaders say early-career talent will be given greater responsibilities with AI — implying mid-level roles (the ones being cut) are the squeeze point.

- 67% of AI impact comes from organizational factors (culture, manager support, talent practices), with only 32% from individual mindset. Microsoft is explicitly saying the bottleneck is restructuring, not training.

Microsoft's own framing in the report — "every firm will need to reconceptualize work as they build agentic systems" — is corporate-speak for "the org chart is the variable being adjusted." Combined with the Challenger numbers, it produces a coherent picture: leaders are restructuring, mid-level functional roles are the adjustment lever, and AI capability at hire is becoming a base requirement rather than a differentiator.

Notably, 43% of what Microsoft calls "Frontier Professionals" — its label for the heaviest AI users — said they intentionally do some work without AI to keep their core skills sharp. That is an interesting counter-signal: even the most AI-fluent workers are hedging against full delegation. Not a contradiction of the trend, but a tell that the productized version of "AI workforce" is more nuanced than vendor decks suggest.

Vendor responsibility map: which products are driving cuts

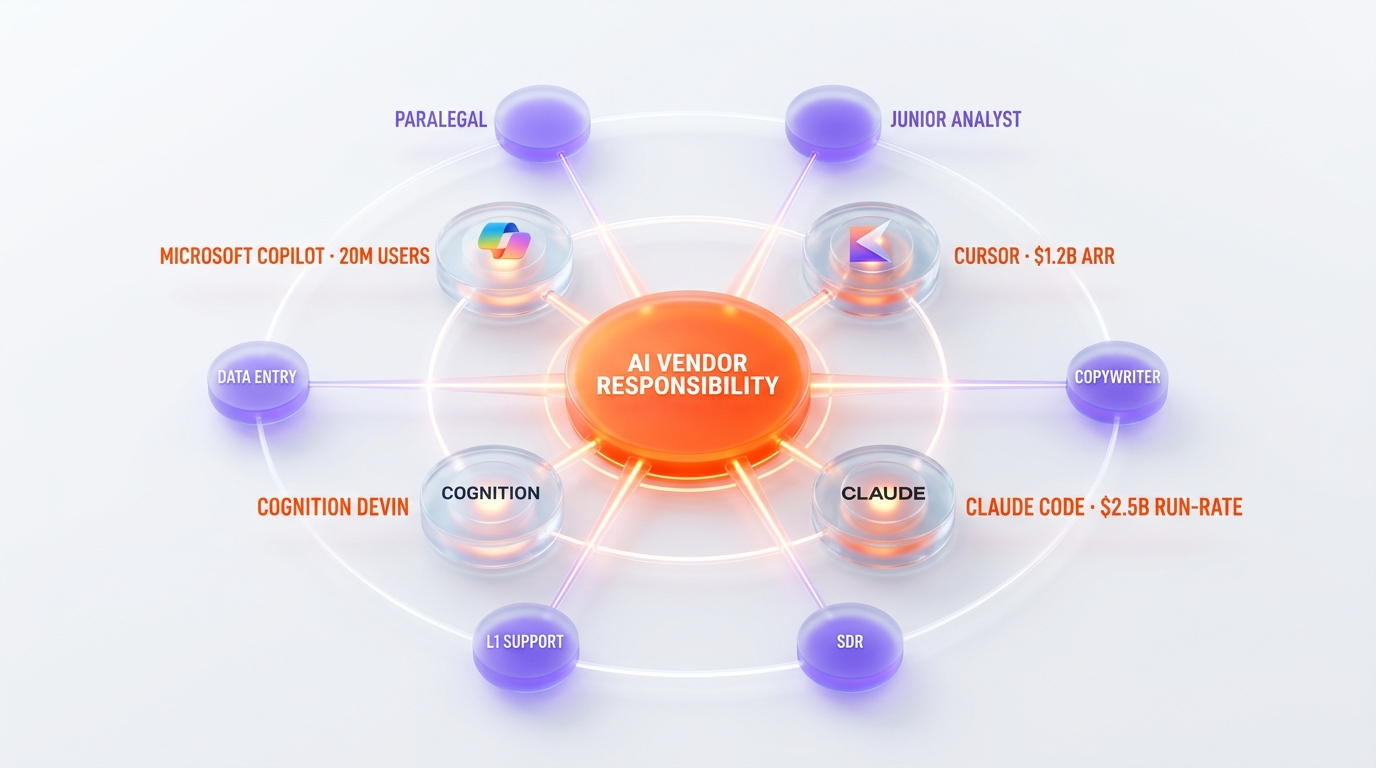

Challenger does not name products. But by cross-referencing the company-by-company cut announcements with publicly-disclosed enterprise AI deployments, a map emerges of which vendors are most credibly tied to which categories of cuts:

- Microsoft Copilot — covered in our 20M paid users / $3.7B ARR enterprise deployment analysis — sits behind the largest share of "AI productivity rationalization" cuts in finance, professional services, and white-collar operations. Recent Copilot Cowork agentic capabilities extend that footprint to multi-step task automation.

- Cursor and Claude Code — the developer productivity layer. Several mid-cap tech announcements explicitly cited "AI-assisted engineering throughput" as the reason for engineering team reductions or non-replacement of attrition. Anthropic's 10 gigawatts compute empire is the supply-side bet underneath this.

- Devin — narrower attribution but real. Cognition's autonomous engineer is being deployed by several enterprises specifically to absorb work previously done by junior and offshore engineering teams.

- Claude (frontier model API) — direct API integrations powering customer support, legal document review, and content operations cuts. Anthropic's finance agent deployments at Citadel, BNY, and Carlyle are the visible tip; the unannounced enterprise deployments are larger in aggregate.

- ServiceNow + Accenture agentic services — the system integrator channel. Our forward-deployed engineering coverage tracks the deployment vehicle that turns frontier models into production cuts for enterprises that cannot build the integration themselves.

We want to be careful with attribution. None of these vendors caused any specific layoff. But the productivity envelope they collectively expand is what allows employers to cite "AI" in WARN Act filings with a straight face. The vendors are the enabling layer, not the proximate cause.

White-collar roles first in line

If we collapse the April Challenger data plus Microsoft Work Trend Index plus the actual public announcements, a job-by-job risk ranking emerges. The roles facing the highest near-term substitution pressure, in our reading of the evidence:

- Tier-1 customer support and chat agents — already mid-displacement. Companies report 40-70% deflection rates on routine queries.

- Junior content writers, SEO operators, and content QA — generative quality has crossed the production threshold for non-byline content categories.

- Paralegals and document reviewers — legal AI tooling matured fast in 2025; 2026 is when the org-chart catches up.

- Junior engineers performing routine implementation — not "engineering is dead" but "engineering teams need fewer juniors per senior." Net junior headcount is the variable.

- Marketing operations specialists — campaign setup, list management, basic analytics. AI orchestration tools have made these single-operator workflows.

- Recruiting coordinators — scheduling, screening, candidate communication. High-routine, high-volume, high-substitution-fit.

- Mid-level financial analysts on routine reporting — research synthesis and standard-template reporting are exactly what frontier models do well.

Roles that remain AI-resilient (for now)

The mirror question: which white-collar functions are most resilient? In April 2026 Challenger data, plus our reading of hiring postings:

- Senior engineers with system-design and ambiguity-tolerance — the part of engineering that is judgment, not implementation. Demand is rising.

- Product managers with cross-functional ownership — AI tooling makes more decisions executable, which makes the decisions themselves more valuable.

- Sales account executives in complex enterprise deals — relationship and judgment. Routine SDR work is being automated; closer roles are not.

- Strategy, M&A, and senior consulting — high-novelty, high-stakes, low-routine. Resilient.

- Healthcare clinical roles — regulatory floor plus physical-world embodiment.

- Trades, logistics, and physical operations — AI is not the relevant disruption layer here. Robotics is, but on a much longer timeline.

- Senior creative direction — generative tools produce more candidate material, which makes selection and direction higher-leverage, not lower.

Policy implications: Trump pre-release reviews, EU AI Act, state-level moves

The combination of Challenger's monthly AI-cited counter and the political salience of layoffs is starting to translate into policy motion. We track three vectors:

- U.S. federal — the Trump administration's posture has been pro-acceleration on AI model deployment, with the pre-release review process for frontier models scaled back from the late-Biden-era framework. There is no federal labor-market response to AI-cited layoffs that we have observed; the dominant frame remains "win the AI race." Congressional Democrats have introduced narrow bills (worker AI-disclosure, retraining credits) but none have advanced.

- EU — the AI Act's high-risk category covers employment decision-making, which means employers using AI to make termination decisions face documentation and transparency requirements. Whether the April cited-reason wave triggers enforcement is the open question for Q3-Q4 2026.

- U.S. states — California, New York, and Illinois have moved on AI-in-employment disclosure rules. New York City's AEDT (automated employment decision tool) law is the most operational; California's SB-7 framework is the broadest in scope.

None of these regimes prevent layoffs. They regulate disclosure and decision-quality. The underlying labor-market reallocation continues unimpeded.

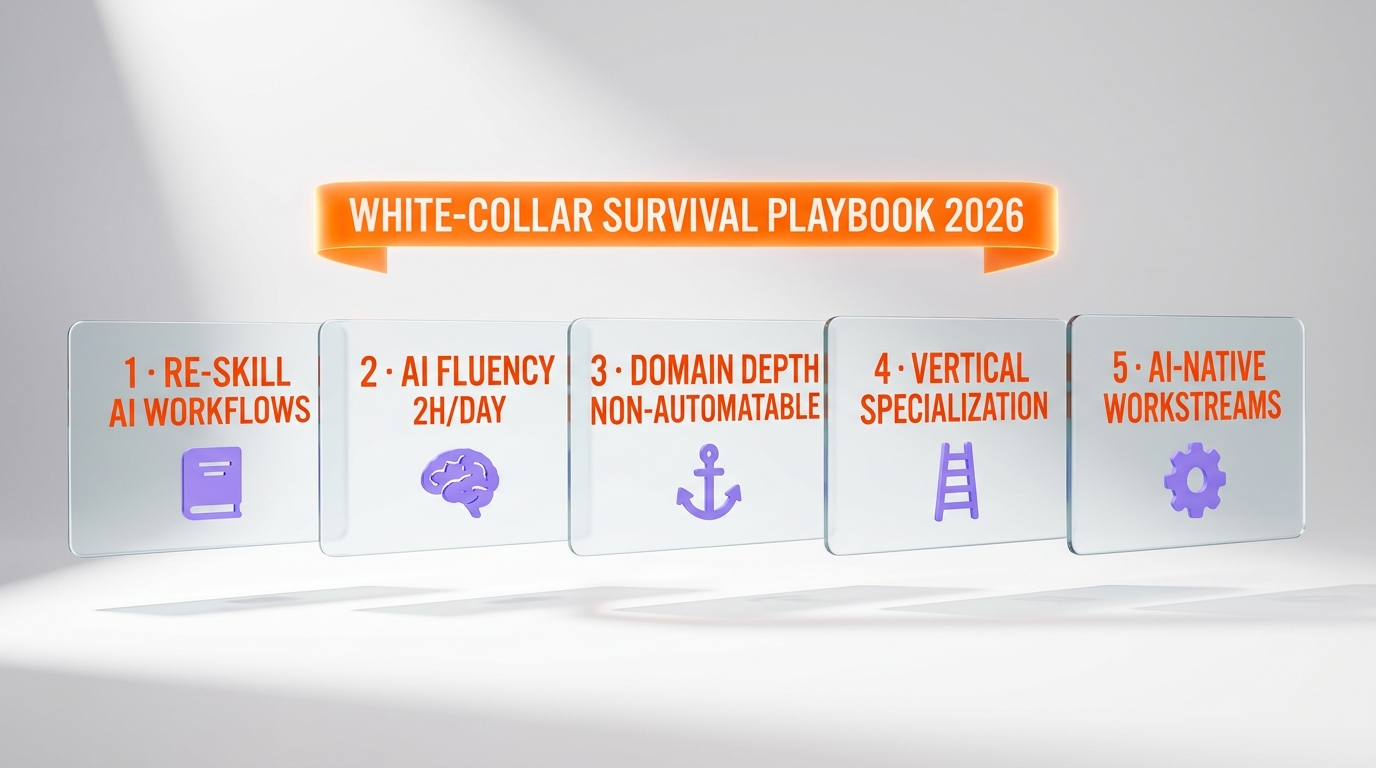

Worker playbook: what to do this quarter if you are white-collar

We do not write career-advice content as our primary lane, but the Challenger data is concrete enough that the implications for workers are worth naming directly. Five practical steps, ordered by leverage:

- Build genuine AI fluency on the tools your industry actually uses. Not generic "I used ChatGPT once." Pick the production tool in your function — Copilot for office work, Cursor or Claude Code for engineering, the appropriate vertical-specific tool for legal or finance — and develop fluency to the point you can demonstrate measurable productivity uplift. The 71% Microsoft Work Trend Index data point is the demand signal you are responding to.

- Move toward judgment-weighted work and away from routine-cognitive work. Inside your current role, identify the 20% of your time that is high-judgment and grow it; identify the 80% that is routine execution and either automate it yourself or accept it is the part being absorbed.

- Develop one domain of deep expertise that AI tooling needs human grounding for. Regulatory edge cases, customer-specific context, system-design tradeoffs. AI is bad at edge cases; that is your moat.

- Strengthen the human-relationship side of your role. Sales, negotiation, stakeholder management, mentoring. The 67% organizational-factors data point from Microsoft is essentially "the soft skills are the hard skills now."

- Watch your sector's Challenger cited-reason share monthly. If your industry is in the top-five AI-cited bucket and trending up, the time horizon is months, not years. Plan accordingly.

What would prove this trend wrong

We have argued, based on April 2026 Challenger plus Microsoft Work Trend Index 2026, that AI has moved from background productivity story to foreground line item on layoff announcements. We could be reading the data wrong. Here is what would change our reading:

- Q2 2026 Challenger reports show the AI-cited share declining back to single digits. That would suggest April was a coordinated PR-cover episode rather than a structural shift.

- Hiring data shows roles cut by AI being re-created elsewhere at comparable wage levels. If aggregate white-collar employment is stable while sector composition shifts, the "AI displacement" framing is misleading.

- A major frontier model labs publishes capability-regression evidence showing the current production AI envelope is narrower than enterprise deployments assume. If the underlying technology turns out to be less reliable than the deployments suggest, the productivity-cut math reverses.

- Macroeconomic recession in Q3 2026 shifts the cited reason back to "market and economic conditions." Layoffs continue but attribution changes. This would be consistent with our hypothesis that some current AI attribution is PR cover for cyclical pressure.

- Wage data shows AI-fluent workers are not actually paid more than peers. If Microsoft's "71% prefer AI skills" preference does not translate into wage premiums, the demand-side signal is softer than the survey suggests.

We will revisit each of these against the May, June, July 2026 Challenger releases.

Bottom line: a labor market signal, not a doomsday call

The combined April Challenger and May Microsoft Work Trend Index data is, in our reading, a clear labor-market signal that AI has crossed a visibility threshold in employer behavior. 21,490 cuts in a single month with AI attribution, second consecutive month at #1, 71% of leaders preferring AI-skilled hires over experience, is not noise.

It is also not a doomsday call. Overall 2026 YTD cuts are still down 50% versus 2025. Most knowledge workers will not be replaced this year. The reallocation is real, but it is gradual on the workforce-wide scale and acute only in specific functions and seniority bands.

What changes is the burden of preparation. In April 2025 a mid-level marketing operations specialist could reasonably assume the role would exist in three years in its current shape. In April 2026, that assumption is no longer the default. Same for tier-1 customer support, junior analyst roles, content production, paralegal work, and a growing list of others. The Challenger cited-reason column has become a leading indicator and the indicator is flashing.

The right response is preparation, not panic. The data is the data. The job is to read it accurately and act early.

Sources

This analysis draws on tier-1 reporting from the following outlets. We cite their work directly so readers can verify every figure independently:

- CNN Business — AI is now the top reason cited for layoffs (May 10, 2026)

- Challenger Gray & Christmas — April Job Cuts Rise 38% From March

- Microsoft — 2026 Work Trend Index

Frequently Asked Questions

How many April 2026 layoffs were attributed to AI according to Challenger?

Challenger, Gray & Christmas reported 21,490 of the 83,387 announced April 2026 U.S. job cuts (26% of the total) were attributed to artificial intelligence. This made AI the single most-cited reason for layoffs in April for the second consecutive month, ahead of closings (14,782), cost-cutting (12,912), and voluntary severance (9,295).

Is AI really causing these layoffs or is it just being cited?

Challenger's methodology captures the reason employers cite in announcements, not a forensic attribution. In practice the 21,490 number blends three categories — genuine substitution where AI directly replaces a function, productivity-driven rightsizing where AI tools reduce per-employee headcount needs, and AI-as-PR-cover for cuts that were going to happen anyway. The trend matters more than the exact share; AI moving from noise to leading rationale in 12 months is structurally significant.

What did Microsoft's 2026 Work Trend Index say about AI skills?

Microsoft's 2026 Work Trend Index, published May 5, found that 71% of leaders surveyed said they would prefer to hire a less experienced candidate with AI skills over a more experienced candidate without them. 77% said early-career talent will be given greater responsibilities with AI tools. The report also concluded that 67% of AI's impact comes from organizational factors (culture, manager support, talent practices) versus 32% from individual mindset and behavior.

Which industries had the most AI-cited layoffs in April 2026?

Technology absorbed 33,361 of the 83,387 total April cuts — by far the largest sector. AI-cited cuts within tech were concentrated in middle-management engineering, content operations, customer support, recruiting, and technical writing roles. Media and publishing, finance and banking, customer service / BPO, and legal services followed. Healthcare frontline, skilled trades, logistics labor, and hospitality were largely absent from the AI-cited column.

How does the Challenger data compare to Andrej Karpathy's exposure map?

Karpathy's March 2026 exposure map ranked 342 occupations by theoretical AI substitution risk based on task-content analysis. Mapping his top-exposure quartile against the April Challenger data, roles he flagged as greater than 70% theoretical exposure appear in the actual AI-attributed cuts at roughly 3x their share of the workforce — a tight correlation for a single month of data. If the correlation holds through Q3-Q4 2026, theoretical exposure maps gain a real-world validation; if it breaks down, the task-content primitive will need revisiting.

Which AI products are most associated with these layoffs?

Cross-referencing company announcements with public AI deployments, Microsoft Copilot is associated with the largest share of white-collar productivity rationalization cuts. Cursor and Claude Code are tied to engineering throughput-driven reductions. Devin is named in autonomous-engineer deployments at several enterprises. The Claude API powers backend automation in legal, finance, and customer support. ServiceNow with Accenture is the system-integrator channel for enterprises that cannot build integrations themselves. None of these vendors caused any specific layoff, but collectively they expand the productivity envelope that allows the AI attribution.

What white-collar roles are most at risk in the near term?

Based on April 2026 Challenger data plus Microsoft Work Trend Index plus public announcements, the highest-substitution-pressure roles are: tier-1 customer support and chat agents, junior content writers and SEO operators, paralegals and document reviewers, junior engineers performing routine implementation, marketing operations specialists, recruiting coordinators, and mid-level financial analysts on routine reporting. The common pattern is high-routine cognitive content with limited judgment requirements.

Which roles remain AI-resilient for now?

Senior engineers with system-design and ambiguity-tolerance, product managers with cross-functional ownership, sales account executives in complex enterprise deals, strategy and M&A, healthcare clinical roles, skilled trades and logistics, and senior creative direction all remain resilient based on April 2026 data. The pattern is judgment-weighted work, regulatory or physical-world embodiment, and high-novelty low-routine task content.

Are total U.S. layoffs actually rising in 2026?

No, paradoxically. Total April 2026 cuts of 83,387 were down 21% versus April 2025's 105,441, and year-to-date through April 2026 layoffs are down 50% versus the same period in 2025. The overall labor market is calmer; what has changed is the composition. AI-cited cuts are rising as a share even while the absolute total falls. The technology sector is the exception — tech YTD layoffs of 85,411 are up 33% versus 2025, the highest pace since 2023.

What policy responses are emerging to AI-driven layoffs?

U.S. federal posture under the Trump administration remains pro-acceleration on AI deployment with no specific labor-market response to AI-cited layoffs. EU AI Act covers employment decision-making in its high-risk category, requiring transparency and documentation for AI-assisted termination decisions. At the U.S. state level, New York City's AEDT law, California's SB-7 framework, and Illinois's AI employment disclosure rules are the most operational. None prevent layoffs; they regulate disclosure and decision quality.

What would prove this AI-layoff trend wrong?

Several signals would change the reading: Q2 2026 Challenger reports showing AI-cited share declining back to single digits would suggest April was coordinated PR cover rather than structural shift. Hiring data showing AI-cut roles re-created elsewhere at comparable wages would weaken the displacement narrative. Frontier-lab capability-regression evidence would reverse the productivity math. A Q3 macroeconomic recession shifting attribution back to "market conditions" would suggest cyclical pressure under AI framing. Wage data showing AI-fluent workers are not paid more than peers would soften the Microsoft demand-side signal.

How should an individual white-collar worker respond this quarter?

Five practical steps in order of leverage: build genuine AI fluency on the production tool your function actually uses (not generic "I tried ChatGPT"); shift your work mix toward judgment-weighted tasks and away from routine cognitive execution; develop deep domain expertise in areas where AI needs human grounding (regulatory edge cases, customer-specific context, system-design tradeoffs); strengthen relationship and stakeholder management skills since Microsoft's 67% organizational-factors finding means soft skills are the hard skills now; watch your sector's monthly Challenger cited-reason share so you have months of warning rather than weeks.