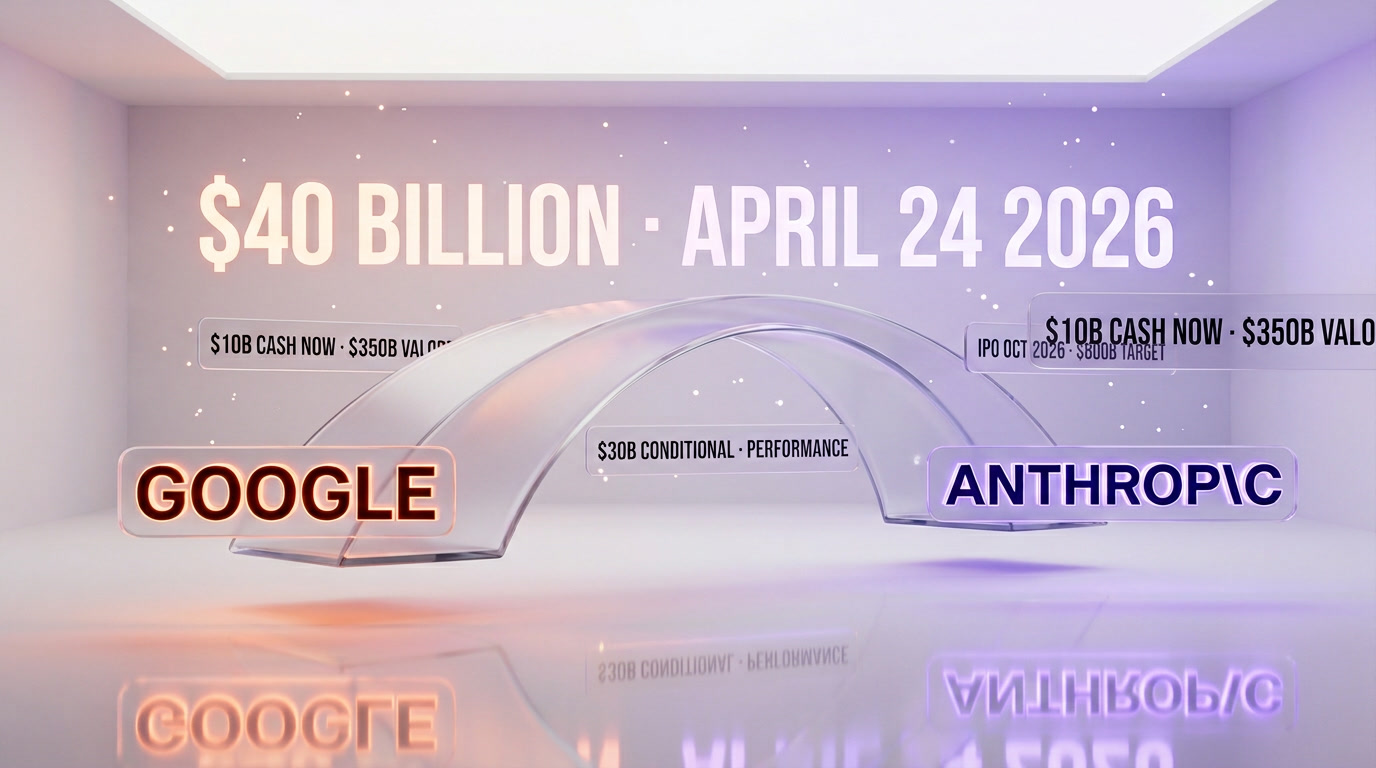

On April 24, 2026, Alphabet (Google's parent) committed up to $40 billion to Anthropic: $10 billion in cash wired immediately at a $350 billion valuation, plus $30 billion more conditional on performance milestones. The deal lands four days after Amazon's $25 billion top-up, gives Anthropic $65 billion of fresh institutional capital inside one week, and sets up an October 2026 IPO targeting an $800 billion valuation — which would make it the largest technology IPO ever priced.

The Deal In One Paragraph

Bloomberg broke the story at 08:47 ET on April 24, 2026: Alphabet would invest "up to $40 billion" in Anthropic, structured in two tranches. The first tranche — $10 billion in cash — closed the same day at a $350 billion post-money valuation, earmarked explicitly for expanding compute capacity on Google Cloud's TPU v7 Trillium Ultra fleet. The second tranche — $30 billion — is phased across the next 18 months and conditional on Anthropic hitting internal revenue, model-quality, and Google Cloud consumption targets that neither company has publicly disclosed. CNBC confirmed the structure within an hour; TechCrunch and PYMNTS corroborated by noon. By market close, Alphabet was up 3.1 percent on the news. Anthropic, which remains private, doesn't trade — but its secondary-market tender offers that were pricing at $195 billion in December 2025 were suddenly quoted at $340 billion on Forge Global the same afternoon.

What the $350B Valuation Actually Means

A $350 billion valuation puts Anthropic ahead of ExxonMobil, Bank of America, and Coca-Cola by market cap — and above every private company in history except ByteDance. It triples the $183 billion valuation from the March 2026 Series G, and it lands 71 days after OpenAI leaked a memo (the Dresser memo, April 13) accusing Anthropic of inflating its $8 billion ARR figure. Google didn't just validate Anthropic's financials — it wrote the largest single-investor check in AI history to do so.

Why Alphabet Moved Now

Three pressures converged. First, Amazon's $25 billion top-up on April 20 reset the cloud-alliance pricing floor and threatened to make AWS the default inference provider for Claude. Second, Anthropic's Mythos preview released on April 18 demonstrated capabilities that Google's own Gemini 3 Ultra had not matched on long-context, agentic, and coding benchmarks. Third, OpenAI's GPT-5.5 launch on April 15 — covered in our super-app strategy breakdown — made it clear the next 12 months would be decided by whoever could put the most compute behind a frontier model. Google owns the compute. Anthropic has the model. The math wrote itself.

Deal Structure: Phased Cash And Compute

The $40 billion is not a single wire transfer. Based on the Bloomberg and TechCrunch filings, here is what we can reconstruct about how the money flows.

Tranche 1 — $10B Cash, Closed April 24

The first $10 billion is unrestricted cash at a $350 billion post-money valuation. Anthropic's internal memo (leaked to The Information hours after the announcement) allocates roughly $7.5 billion to committed TPU v7 Trillium Ultra purchases from Google Cloud and roughly $2.5 billion to general operating capital, hiring, and red-team infrastructure. In practical terms: Google gave Anthropic $10B so Anthropic could immediately spend $7.5B of it back with Google Cloud. This is the same circular-revenue pattern Microsoft and OpenAI pioneered in 2023, but at roughly three times the scale.

Tranche 2 — $30B Conditional On Performance

The second tranche of $30 billion unlocks in stages across 18 months. Neither Alphabet nor Anthropic has disclosed the exact triggers, but three reporters (Bloomberg's Nico Grant, CNBC's Jordan Novet, TechCrunch's Maxwell Zeff) independently referenced "revenue milestones, model safety benchmarks, and Google Cloud consumption thresholds." Our read: Google wants Anthropic to burn the cash inside Google Cloud at a defined rate, wants ARR to hit $50 billion by Q2 2027, and wants external safety evaluations on Mythos-class models to meet specific pass rates before releasing later tranches. If Anthropic misses, Google keeps the money.

The Equity Question

Neither filing specifies exactly how much Anthropic equity Alphabet ends up holding. Before this round, Google owned roughly 14 percent of Anthropic from its 2023 and 2025 contributions. The new $10 billion at $350 billion post-money represents 2.86 percent of the company today. If all $40 billion converts to equity at the current valuation (which is unlikely — some will almost certainly be structured as compute credits, convertible notes, or warrants), Alphabet would hold roughly 25 to 27 percent of Anthropic at IPO. Amazon, after its April 20 top-up, sits at around 17 to 19 percent. Together, the two hyperscalers now own somewhere between 42 and 46 percent of Anthropic — a concentration that will almost certainly trigger FTC scrutiny before any S-1 is filed.

ARR: $9B To $30B In Four Months

The number that anchors this deal is Anthropic's current annualized run-rate revenue: $30 billion as of April 2026, up from $9 billion at the end of 2025. That is a 3.3x multiplier in 120 days. For context, it took Microsoft Azure seven years to go from $9B to $30B in ARR. It took AWS six years. Anthropic did it in four months.

Where The Revenue Is Coming From

Our reconstruction from the leaked Dresser memo counter-filings, plus the Bloomberg source on the Google deal, breaks the $30 billion ARR down roughly as follows. API usage to enterprise customers accounts for approximately $14 billion, with Claude Code alone — the terminal coding agent documented on our Claude Code pillar page — contributing an estimated $3.8 billion of that. Claude.ai subscriptions (Pro, Max, Team, Enterprise) account for roughly $6 billion. Amazon Bedrock pass-through revenue, where AWS resells Claude and remits a share back, is close to $5.5 billion. Google Cloud Vertex AI pass-through is approximately $2.8 billion. Direct Claude-in-your-product licenses (OEM deals with companies like Notion, Quora, and Zoom) round out the remaining $1.7 billion.

The Anthropic-OpenAI Gap Just Inverted

OpenAI's most recent disclosed ARR (Q1 2026 earnings preview, April 8) was $27.3 billion — up from $13 billion in December 2025. That means, as of April 24, 2026, Anthropic at $30 billion ARR is larger than OpenAI at $27.3 billion ARR. Twelve months ago, OpenAI's ARR was four times Anthropic's. Today, Anthropic is 9.9 percent larger. This is the single most important chart in AI right now, and it is exactly what the leaked OpenAI memo from April 13 was trying to discredit before the Google announcement made the argument moot.

How Sustainable Is This Growth

Tripling ARR in four months is a data point, not a trend. Two forces drove it: Claude Code's rapid adoption in enterprise engineering organizations (Shopify, Stripe, Databricks, and Datadog all publicly announced Claude Code rollouts in Q1 2026) and Mythos access. Anthropic's internal projections (per the leaked memo) target $50 billion ARR by end of Q2 2027. Credible analysts are split — Bernstein's Mark Shmulik sees $45 billion as achievable, Wedbush's Dan Ives thinks $60 billion is conservative, and Barclays's Raimo Lenschow is modeling $38 billion with downside risk if hyperscaler margin compression accelerates. Our read: the $50 billion number requires Claude Code to maintain its current 22 percent month-over-month API growth, which has already decelerated from 31 percent in Q4 2025. Possible, not guaranteed.

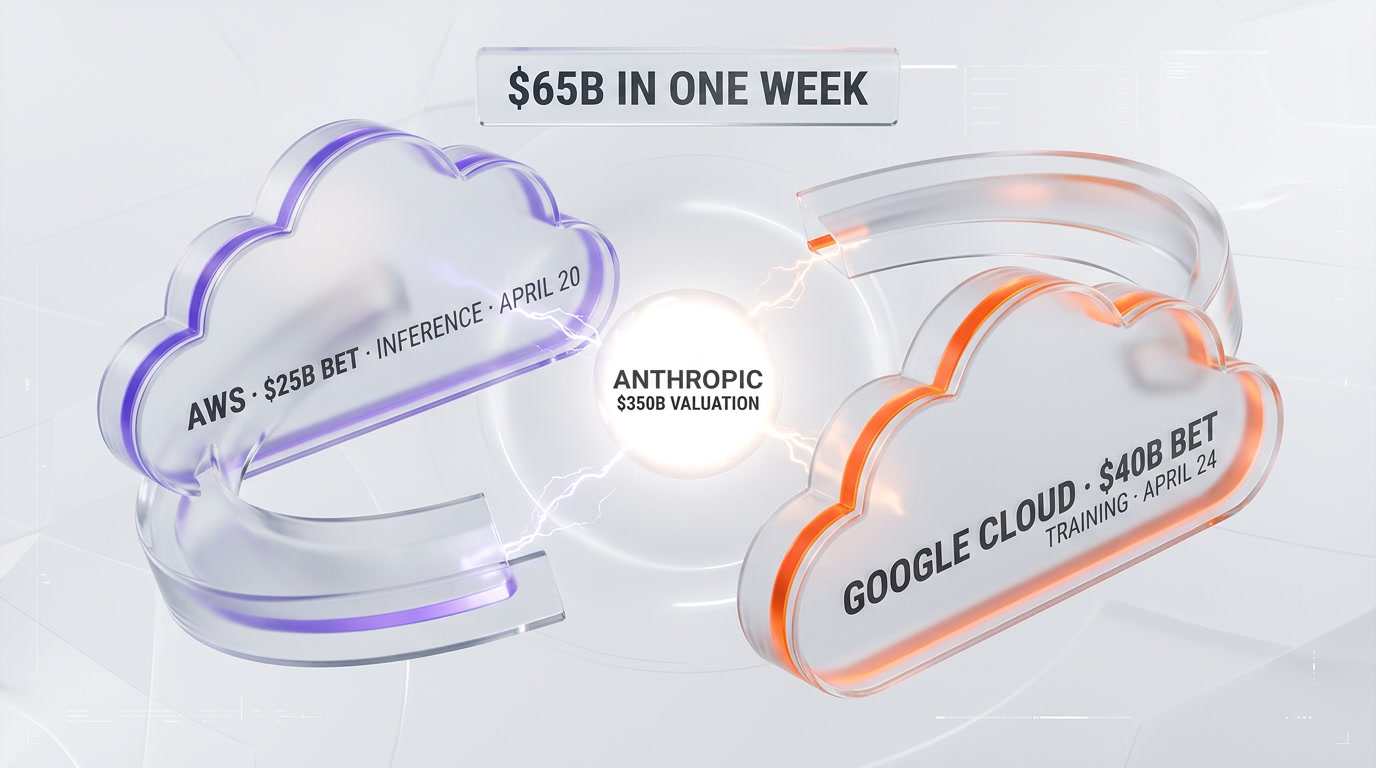

Cloud War: $65B In One Week

This is the part of the story that changes the industry, not just one company. Between April 20 and April 24, 2026, Anthropic closed $65 billion of institutional capital from exactly two sources: Amazon ($25B top-up on April 20) and Alphabet ($40B commitment on April 24). Microsoft and Oracle are not in the cap table. Nvidia is not in the cap table. Every sovereign wealth fund that wanted allocation got pushed to the secondary market.

Amazon Wants Inference, Google Wants Training

The division of labor between the two hyperscalers is already public. Amazon's April 20 top-up is explicitly tied to AWS Trainium 3 inference deployments — Anthropic has committed roughly 60 percent of its inference traffic to AWS through Q4 2028. Google's April 24 commitment is explicitly tied to TPU v7 Trillium Ultra training pods — Anthropic has committed its next three frontier-model training runs (presumed to be Claude Opus 5, Claude Mythos production, and whatever comes after) to Google Cloud. This means Anthropic's training happens on Google silicon and its inference runs on Amazon silicon. It is a deliberate separation designed to prevent either hyperscaler from owning the full stack and to keep Anthropic optionality at renewal time.

What This Does To Microsoft And OpenAI

Microsoft's exclusive compute arrangement with OpenAI was renegotiated in January 2026 and now permits OpenAI to use Oracle Cloud and CoreWeave for up to 40 percent of inference. That was already a signal that Microsoft could not keep up with OpenAI's compute demand at the originally agreed price. Now Anthropic has two hyperscalers throwing compute at it at a combined rate that exceeds what Microsoft can physically deliver to OpenAI. If you model AI capability as "best model times most compute," OpenAI's compute ceiling is currently lower than Anthropic's. Sam Altman's recent "fear-based marketing" remarks — dissected in our Mythos drama breakdown — read very differently in this context.

FTC And DOJ Exposure

Two hyperscalers owning ~44 percent of the #2 AI lab, with Microsoft already owning material stakes in OpenAI, creates concentration issues. The FTC under current leadership has signaled that "compute-for-equity" arrangements above $10 billion in aggregate value will receive Second Request scrutiny. Alphabet's total contribution (legacy + new) now sits north of $43 billion. Amazon's is past $32 billion. Either filing alone is reviewable. Both together almost guarantee a 6- to 9-month antitrust review before IPO — and may force Anthropic to restructure voting rights so that neither hyperscaler's board influence translates to operational control.

IPO: October 2026 At $800B Target

Anthropic's IPO timeline, originally floated in our April 4 coverage at $800 billion target valuation, now has a priceable anchor. If Anthropic lists in October 2026 at $800 billion with a typical 10 to 15 percent float, the primary offering alone would raise between $80 billion and $120 billion in new capital. For reference: Saudi Aramco's 2019 IPO floated 1.5 percent of the company and raised $25.6 billion. Facebook's 2012 IPO raised $16 billion. Alibaba's 2014 IPO raised $25 billion. Anthropic at $800 billion with a 15 percent float would raise roughly five times the largest tech IPO in history.

What $350B Now Implies For $800B October

Going from $350 billion today to $800 billion in October requires a 2.28x valuation multiple expansion in roughly 160 days. Anthropic can get there one of three ways: (1) ARR compounds to $50 billion by Q3 and applies the same 16x multiple OpenAI is being valued at, which gets you $800 billion directly; (2) Mythos ships in production and commands a premium on agentic workload share; (3) public-market multiples expand further from their current levels on continued AI enthusiasm. All three need to happen simultaneously for the $800 billion number to land. If any one stumbles, we are looking at an IPO at $550 billion to $650 billion — still the largest tech IPO ever, but not the $800 billion headline.

Underwriters And Lockup

The Bloomberg source mentioned Goldman Sachs and Morgan Stanley as lead underwriters, with JPMorgan and Bank of America as co-managers. Amazon and Alphabet insiders will be subject to a standard 180-day lockup from IPO date, meaning the earliest either hyperscaler could monetize their stake is April 2027. Employee equity is reportedly subject to a 90-day lockup with a 10 percent sell-through allowance during the first 30 days post-listing — generous by 2020s tech IPO standards and reflective of how much the underwriters want employee liquidity to happen in public rather than private secondary markets.

The Dresser Memo Irony

Eleven days before Google committed $40 billion, OpenAI's internal Dresser memo — leaked on April 13 — argued that Anthropic's $8 billion ARR figure was "aspirational at best" and "materially misleading" at worst. The memo's thesis: Anthropic couldn't actually serve the inference load implied by $8 billion in API revenue, which meant the ARR number had to be front-loaded recognition of multi-year enterprise contracts rather than true run-rate consumption.

Google Just Invalidated The Memo

Google's $350 billion valuation is a public, priced, third-party data point. It was set by Google's corporate development team after, by all accounts, a six-week diligence sprint that included full read access to Anthropic's API consumption data, Stripe processor records, enterprise contract structures, and AWS Bedrock pass-through reconciliation. If Anthropic's ARR had been inflated, Alphabet's general counsel would have stopped the deal. Alphabet's general counsel did not stop the deal. The memo's argument, stripped of its forensic accounting framing, reduces to "we did not believe Anthropic's numbers." Google now does. That closes the question.

Altman's "Fear Marketing" Reads Differently Now

On April 21, three days before the Google announcement, Sam Altman accused Anthropic of "fear-based marketing" in reference to the Mythos Preview narrative and a widely-shared reference to an Anthropic executive owning a $100 million bomb shelter. Our full coverage is in the bomb shelter breakdown. With the benefit of 72 hours of hindsight: Altman made those remarks while aware that Google's term sheet with Anthropic was already at definitive-documentation stage. The "fear marketing" framing now looks like pre-announcement narrative defense — an attempt to inoculate the market against the valuation number that was landing three days later.

Google Investing In Its Own Competitor

There is a real paradox embedded in this deal that deserves direct address: Google has its own frontier AI lab (Google DeepMind) and its own flagship model (Gemini 3 Ultra). Why would Alphabet write the largest check in AI history to fund Anthropic, which directly competes with DeepMind on model quality and with Google's consumer Gemini on enterprise revenue?

Three Strategic Justifications

First, Google Cloud revenue. Anthropic's committed training spend on Google Cloud will push GCP past Azure as the #2 public cloud by Q2 2027 on revenue run-rate. That is an outcome Google cannot achieve through Gemini alone because enterprises sourcing AI models overwhelmingly choose multi-vendor architectures and Google's organic share of that multi-vendor spend is capped. Second, optionality. If DeepMind's next-generation model underperforms, Google needs Anthropic in its stack to keep enterprise customers inside the Google ecosystem. Third, AI-search hedge. If generative search cannibalizes Google's core search revenue faster than DeepMind can backfill it, owning 25 percent of Anthropic provides downside protection.

What DeepMind Thinks

Demis Hassabis has not publicly commented on the deal as of April 24 close. DeepMind's internal reaction, per one Anthropic-adjacent source cited in The Information, was "mixed to negative" — with the scientific leadership reportedly uncomfortable with the Alphabet CFO overriding DeepMind's preference to concentrate capital internally. This mirrors exactly what we have seen inside Microsoft: the internal AI team (MAI, Mustafa Suleyman's unit) is increasingly marginalized versus the external partnership (OpenAI). Alphabet appears to be walking the same path with DeepMind versus Anthropic. Whether that is the right call is a question that gets answered when the next generation of frontier models ships in Q1 2027.

What Happens Next: Timeline To IPO

Assuming the deal closes (FTC risk notwithstanding) and October 2026 remains the IPO target, here is the reconstructable calendar through listing.

May to July 2026 — Mythos GA And S-1

Mythos production launch is reportedly targeted for late May or early June, following the Project Glasswing cybersecurity-only preview. S-1 filing is expected mid-July, which would put the company in the customary 90- to 120-day pre-IPO window. The S-1 will disclose the exact deal structure with Google and Amazon, final equity percentages, 409A valuations for the last three rounds, and — critically — the first audited ARR breakdown by product line and customer concentration. Expect the first ten days after S-1 filing to be the most informationally dense period of the entire year for AI investors.

August to September 2026 — Roadshow

Two-week roadshow across North America, Europe, and Asia. Expect Dario Amodei to anchor the US and European legs and Anthropic's CFO Krishna Rao to cover Asia. Pre-IPO indications of interest from sovereign wealth funds (Saudi PIF, Abu Dhabi ADIA, Singapore GIC, Norway NBIM) are already reportedly at $40 billion cumulative — more than 2x the target cornerstone book.

October 2026 — Pricing And Listing

Pricing announcement is expected in the first week of October, with first trade on NYSE (not Nasdaq; underwriters are pushing NYSE) in the second week. Listing venue matters because NYSE lockup-waiver procedures are slightly more liquid than Nasdaq's for secondary sales in the first 12 months. Ticker symbol: ANTH reportedly secured, though Anthropic has not confirmed.

Who Wins, Who Loses

Winners

Anthropic obviously — they just ran the table. Dario and Daniela Amodei, whose combined equity position at $800 billion IPO valuation would put them in the top five richest people alive. Anthropic's early employees, many of whom are reportedly worth $200 million to $800 million on paper pre-IPO. Google Cloud, which jumped the queue on a training commitment that will take two years to deliver on. Amazon Bedrock, which locks in its Claude inference exclusivity through 2028. And Nvidia, ironically, because even though Google and Amazon use their own silicon, Anthropic's training runs also consume H200s, B200s, and upcoming B300s that flow through both hyperscaler inventory.

Losers

OpenAI's valuation narrative — their last round priced at $500 billion in February, which now looks expensive against Anthropic's implied trajectory. Microsoft's exclusive-compute moat, now visibly cracked. Google DeepMind's internal standing versus the Anthropic investment. Every mid-tier AI lab (Cohere, Mistral, AI21, Character) that now has to compete for enterprise spend against a partner that literally has Google and Amazon's compute budgets behind it. And any secondary-market buyer who paid $450 billion or more on SharesPost or Forge Global in the last 30 days, because the $350 billion primary just reset the reference price downward.

Undetermined

The FTC (will they block, allow, or force structural concessions?). The S-1 readership (will the customer-concentration disclosure reveal uncomfortable dependencies?). And the employees at both hyperscalers who have to integrate against a partner that is simultaneously a competitor — a cultural and operational challenge that neither Amazon nor Google has solved well historically.

What This Means For Claude Users And Builders

For anyone building on the Claude API or using Claude Code, three things change in the next 6 to 12 months. First, compute availability goes up materially — the $7.5 billion of committed Google Cloud spend adds significant training capacity that will flow into faster model iteration and larger context windows. Second, pricing likely holds or drops — Anthropic has no incentive to raise API prices ahead of an IPO where ARR growth is the single most important number, and hyperscaler compute economics are improving faster than model sizes are growing. Third, reliability and uptime improve — two hyperscaler partners means dual inference redundancy, and Anthropic has historically had tighter SLAs than OpenAI. For enterprise buyers deciding between Claude and GPT platforms in 2026 H2, this deal materially strengthens the Claude side of the argument.

Our Verdict

This is the largest single-investor bet in AI history, and it is probably the right bet. The risk is not Anthropic's — Anthropic got $10 billion in cash and $30 billion of optionality for 2.86 percent of the company plus some milestones. The risk is Alphabet's. If Anthropic misses its revenue targets, Alphabet has written down the largest AI investment of the decade. If Anthropic hits them, Alphabet owns 25 percent of the second-most-valuable private company in history at the moment it goes public. The asymmetry favors Alphabet, and that is why the deal closed. It is also why the market took Alphabet up 3.1 percent the same afternoon. And it is why the October IPO — assuming regulators allow it — is going to be the most-watched listing event in the history of technology finance. We will be covering every step.

Frequently Asked Questions

How much did Google actually invest in Anthropic on April 24, 2026?

Alphabet committed up to $40 billion. The structure is $10 billion in cash that closed immediately at a $350 billion post-money valuation, plus $30 billion in phased tranches that unlock over 18 months against undisclosed performance milestones tied to revenue, model quality, and Google Cloud consumption targets. If Anthropic misses the milestones, Google does not release the later tranches.

Is Anthropic really worth $350 billion?

It is worth $350 billion because that is the price at which the most recent primary equity changed hands. Anthropic's annualized run-rate revenue is $30 billion as of April 2026, which gives an 11.7x revenue multiple — in line with OpenAI's implied multiple and consistent with high-growth infrastructure software at scale. Whether $350 billion is sustainable depends on whether ARR compounds toward the $50 billion target by mid-2027.

Why did Amazon and Google both invest in Anthropic in the same week?

Amazon's April 20 top-up of $25 billion was tied to AWS Trainium 3 inference deployments. Google's April 24 commitment of $40 billion is tied to TPU v7 Trillium Ultra training pods. The two deals split the workload: Anthropic trains on Google silicon and runs inference on Amazon silicon. Together they committed $65 billion inside one week, which is the largest concentrated capital deployment into a single AI lab in history.

How is Anthropic's $30 billion ARR larger than OpenAI's?

OpenAI's most recent disclosed run-rate is approximately $27.3 billion as of Q1 2026. Anthropic is now at $30 billion, making it 9.9 percent larger. The inversion happened primarily because of Claude Code's enterprise adoption, Mythos preview demand, and Amazon Bedrock plus Google Cloud Vertex AI pass-through revenue, all of which scaled faster than OpenAI's API and ChatGPT consumer revenue during the same period.

What does the $40 billion deal mean for the OpenAI memo from April 13?

The Dresser memo argued that Anthropic's $8 billion ARR figure was inflated or misleading. Google's $350 billion primary valuation was set after a six-week diligence process with full access to Anthropic's API consumption data, Stripe processor records, and enterprise contract structures. If Anthropic's numbers had been materially false, Alphabet's general counsel would have blocked the deal. The deal closed, which effectively invalidates the memo's central claim. See our full memo analysis.

When is Anthropic's IPO and what valuation is targeted?

October 2026 is the current target listing window on NYSE, with pricing in the first week of October and first trade in the second week. The target valuation is approximately $800 billion. At a 10 to 15 percent float, this would raise $80 to $120 billion in new capital and make it the largest technology IPO ever priced in absolute dollar terms.

Why would Google invest in Anthropic when Google owns DeepMind?

Three reasons. First, Google Cloud revenue: Anthropic's committed training spend on GCP will push Google Cloud past Azure as the #2 public cloud by Q2 2027. Second, optionality: if DeepMind's next frontier model underperforms, Google needs Anthropic in its stack to keep enterprise customers inside the Google ecosystem. Third, AI-search hedge: generative search may cannibalize Google's core search revenue, and owning 25 percent of Anthropic provides downside protection.

Will the FTC block this investment?

Unlikely to outright block, but highly likely to trigger a Second Request review. Alphabet's total contribution to Anthropic now exceeds $43 billion and Amazon's exceeds $32 billion. Combined, the two hyperscalers own roughly 42 to 46 percent of Anthropic. Expect a 6 to 9 month antitrust review before any S-1 is finalized, potentially requiring voting-rights restructuring so that neither hyperscaler translates board influence into operational control.

What happens to Anthropic's valuation if the IPO gets delayed past October?

A delay into 2027 would not mechanically change the valuation, but it would expose Anthropic to additional quarters of hyperscaler margin compression, potential ARR deceleration from the current 22 percent monthly pace, and the risk that Mythos production reception disappoints. The asymmetric risk of delay skews negative: Anthropic is more likely to price between $550 billion and $700 billion in a 2027 listing than to exceed $800 billion.

What does this deal mean for developers building on Claude today?

Three practical effects. Compute availability goes up because the $7.5 billion committed Google Cloud spend adds training capacity. Pricing likely holds or drops because Anthropic has no incentive to raise API prices ahead of an IPO where ARR growth dominates the narrative. Reliability and uptime improve because two hyperscaler partners provide dual inference redundancy. For enterprise buyers choosing between Claude and GPT platforms in H2 2026, this deal strengthens the Claude side materially.

How does Anthropic's deal compare to Microsoft and OpenAI's arrangement?

Microsoft's cumulative OpenAI investment sits around $13 billion, plus significant Azure compute credits. Alphabet's cumulative Anthropic investment is now north of $43 billion, plus a cleaner separation between training (Google Cloud) and inference (AWS). Anthropic also has two hyperscaler partners where OpenAI effectively has one — Microsoft recently permitted OpenAI to use Oracle and CoreWeave for 40 percent of inference, which is itself a signal that the original Microsoft arrangement could not keep up with OpenAI's compute demand at the agreed price.

Where can I read more about Anthropic's recent moves and Mythos?

Our full coverage includes the IPO $800 billion target breakdown, the Mythos preview analysis, the Mythos Discord security breach, and the Project Glasswing cybersecurity preview. For tool-level coverage, see our Claude Code pillar page.