SpaceX has agreed to acquire Anysphere, the company behind the AI coding tool Cursor, in an all-stock deal that values Anysphere at roughly $60 billion, the companies announced on June 16, 2026. Under the agreement, reported by CNBC, Reuters, and TechCrunch, Anysphere is set to merge with a wholly owned SpaceX subsidiary, with Cursor's shareholders receiving SpaceX stock rather than cash. The transaction is expected to close in the third quarter of 2026 and remains subject to regulatory approval, including antitrust review. For developers, the headline number matters less than a narrower question: what happens to Cursor as a coding tool once it sits inside Elon Musk's combined SpaceX and xAI empire — whether it stays model-neutral, gets pulled toward Grok, and how it now stacks up against Claude Code, GitHub Copilot, Windsurf, and OpenAI Codex.

We have covered Cursor's run to a roughly $50 billion private valuation and its plan to build its own model, its pivot to an agent-first IDE with Cursor 3, and the broader three-way coding war against Google Antigravity and Claude Code. This acquisition is a different story from the SpaceX flotation we tracked: it lands just four days after SpaceX's blockbuster Nasdaq debut, and it folds the most commercially successful independent AI coding company into the same organization that already absorbed xAI. Below is what is confirmed, what is still attributed reporting, and what it means for the tool you may actually code in every day.

What SpaceX actually agreed to buy

Anysphere is the San Francisco company that builds Cursor, an AI-native code editor that has become one of the most widely used AI coding tools among professional software teams. The company was founded in 2022 by four MIT graduates — Michael Truell, who serves as chief executive, alongside Sualeh Asif, Arvid Lunnemark, and Aman Sanger. From a standing start, Cursor grew into one of the fastest-scaling software businesses of the AI era, reaching enterprise adoption that placed it among the small set of AI products generating substantial recurring revenue from businesses rather than from hobbyist usage.

The deal announced on June 16 is an agreement to acquire — not a completed transfer of ownership. SpaceX and Anysphere have signed a merger agreement; the combination still has to clear closing conditions and regulatory review before SpaceX owns Anysphere outright. Until that close, expected in the third quarter of 2026, Anysphere remains an independent company operating Cursor, and the terms below describe a pending transaction rather than a finished one.

The deal at a glance

- Buyer: SpaceX (Nasdaq: SPCX), which merged with xAI in February 2026.

- Target: Anysphere, maker of the Cursor AI code editor, founded 2022.

- Value: roughly $60 billion implied equity value.

- Structure: all-stock; Anysphere merges with a wholly owned SpaceX subsidiary, and Cursor holders receive SpaceX stock.

- Timing: expected to close in the third quarter of 2026, pending regulatory approval.

- Context: announced four days after SpaceX's June 12, 2026 IPO.

The deal terms, attributed source by source

Because this is a market-moving merger, the figures deserve careful attribution. Here is what each tier of reporting establishes, and where the numbers come from.

The headline value and structure. CNBC, Reuters, and TechCrunch all report an all-stock deal valuing Anysphere at roughly $60 billion, with Cursor's shareholders receiving SpaceX stock. Reuters describes the structure as a stock-based merger between Anysphere and a wholly owned SpaceX subsidiary, a structure that, as Reuters notes, signals the proceeds SpaceX raised in its IPO are not being used to fund the acquisition. Reporting and the associated filing identify the merger vehicle as a SpaceX subsidiary, referred to in coverage as X67 Inc.

The April option. Both TechCrunch and Reuters report that, in April 2026, SpaceX secured an option that let it either acquire Anysphere for $60 billion in stock later in the year or pay $10 billion for a partnership instead. The June 16 announcement is SpaceX exercising the acquisition side of that option. This framing reshapes how to read the so-called break-up figure: the $10 billion was structured as the alternative to buying, not purely a penalty.

The termination fees. Reuters, drawing on the regulatory filing, reports a standard termination fee of $10 billion and a separate antitrust-related termination fee of $4 billion. Bloomberg's reporting on the same filing surfaced these figures from the merger exhibit rather than the body of the principal disclosure. We attribute both numbers to the filing as reported by Reuters and Bloomberg; they were not stated in the main body of SpaceX's headline disclosure.

Cursor's revenue. This is the figure most worth pinning down, because secondary coverage has cited a wide range. Reuters reports roughly $2.6 billion in annualized business-to-business revenue, citing company data shared earlier in June 2026 — a run-rate figure, not audited annual revenue. That is the most current, best-attributed number available. It marks a steep climb from the period when Cursor's annualized revenue first crossed the $1 billion mark in late 2025, as reported by CNBC at the time. Higher figures circulating in some market commentary are not as well sourced, so we anchor to the Reuters $2.6 billion run-rate and flag the trajectory rather than treating any single larger number as established.

Cursor's prior valuation. Before the SpaceX agreement, Cursor's last widely reported private valuation was around $50 billion, tied to a Series D round backed by investors including Andreessen Horowitz, Thrive Capital, and Nvidia. That round itself was a sharp step up from a Series C that valued the company near $29 billion in mid-2025. At roughly $60 billion, the SpaceX agreement represents a premium over that last private mark.

Why SpaceX is buying a coding tool four days after its IPO

The timing is the most striking part of the story. SpaceX went public on June 12, 2026, in a Nasdaq debut priced at $135 per share that surged on its first day and lifted the company's valuation above $2 trillion. Four days later, it announced a $60 billion acquisition. The all-stock structure is the connective tissue: a newly public company with a richly valued, liquid stock can use that paper as acquisition currency without spending its IPO cash, which is precisely what the Anysphere structure does.

The strategic logic runs through xAI. SpaceX absorbed xAI, the maker of the Grok model family, in February 2026 — a consolidation we covered when xAI was dissolved into the combined SpaceX entity and again in our analysis of the SpaceX and xAI merger. That move gave SpaceX a frontier model lab but not a flagship application with proven enterprise revenue. AI coding is one of the few categories where AI has converted into durable business spending, and Cursor is the category's most commercially successful independent player. Buying Anysphere hands the combined SpaceX-xAI organization an immediate, revenue-generating enterprise software franchise and a direct distribution channel for Grok into developer workflows.

In other words, the acquisition is less about SpaceX wanting to be in the IDE business for its own sake and more about giving xAI's models a foothold in the highest-value AI use case, with a paying customer base attached. That framing also explains the urgency: the longer Cursor remained independent and model-neutral, the more its default integrations favored rival labs.

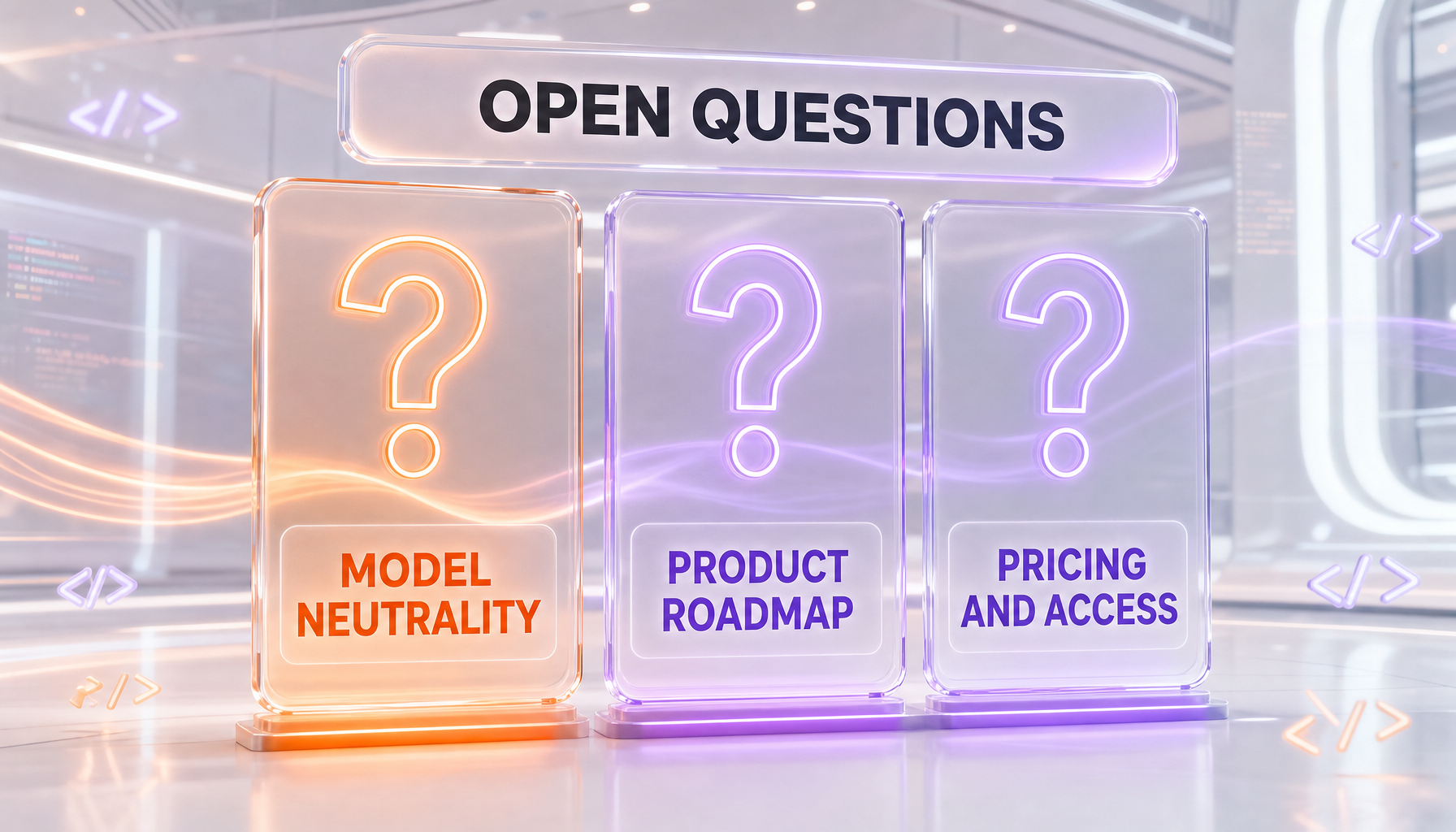

What happens to Cursor as a product

For the people who use Cursor every day, three product questions sit above everything else, and none has been fully answered by the announcement itself.

Will Cursor stay model-neutral? Cursor's appeal has rested partly on letting developers pick their underlying model — routing to Anthropic's Claude family, OpenAI's models, Google's Gemini, or Cursor's own in-house model depending on the task. A coding tool owned by a company that also owns a frontier lab has an obvious incentive to favor that lab's models. Whether Cursor preserves genuine multi-model choice or quietly nudges defaults toward Grok is the single most consequential product question for existing users, and it is unresolved as of the announcement.

Will the product roadmap stay intact? Cursor 3 reoriented the product around an agent-first workflow with parallel AI agents and cloud handoff. An acquirer focused on integrating its own model could either accelerate that roadmap with deeper compute access or redirect engineering effort toward Grok integration at the expense of model-agnostic features. SpaceX and xAI command large compute resources, which could be a genuine tailwind for Cursor's stated ambition to train its own models — or a reason to deprioritize that effort in favor of Grok.

Will pricing and access change? Cursor's pricing has been a moving target through its rapid growth. New ownership introduces the possibility of bundling, repricing, or tying premium tiers to Grok access. There is no announced change yet, but enterprises negotiating multi-year commitments should treat post-close pricing as an open variable.

The honest answer to all three is that the merger agreement is about ownership and economics; the product decisions follow integration, and integration follows the regulatory close. None of this is settled today.

The Grok question: independence versus integration

The central tension of this deal is whether Cursor is run as an independent product or absorbed as a Grok delivery vehicle. There is precedent on both sides of that line across the industry, and the outcome will shape Cursor's competitive position more than any single feature.

The case for keeping Cursor independent is commercial. Much of Cursor's enterprise value comes from teams that explicitly want a neutral surface so they are not locked into one model vendor. Forcing Grok as the default, or degrading rival-model integrations, would put that neutrality at risk and hand an opening to competitors who can credibly claim to be model-agnostic. A rational owner protecting a $60 billion asset has reason to preserve what made it valuable.

The case for integration is strategic. SpaceX did not buy a coding tool to run a neutral marketplace for its rivals' models; it bought distribution for Grok inside developer workflows. The likeliest path is somewhere in between — Cursor retains multi-model support on paper while Grok becomes the promoted default, the free tier, or the most deeply integrated option, with rival models available but less frictionless. That pattern would let SpaceX claim openness while still steering usage toward its own model. Until the company says otherwise, treat aggressive Grok integration as the base case and genuine sustained neutrality as the upside surprise.

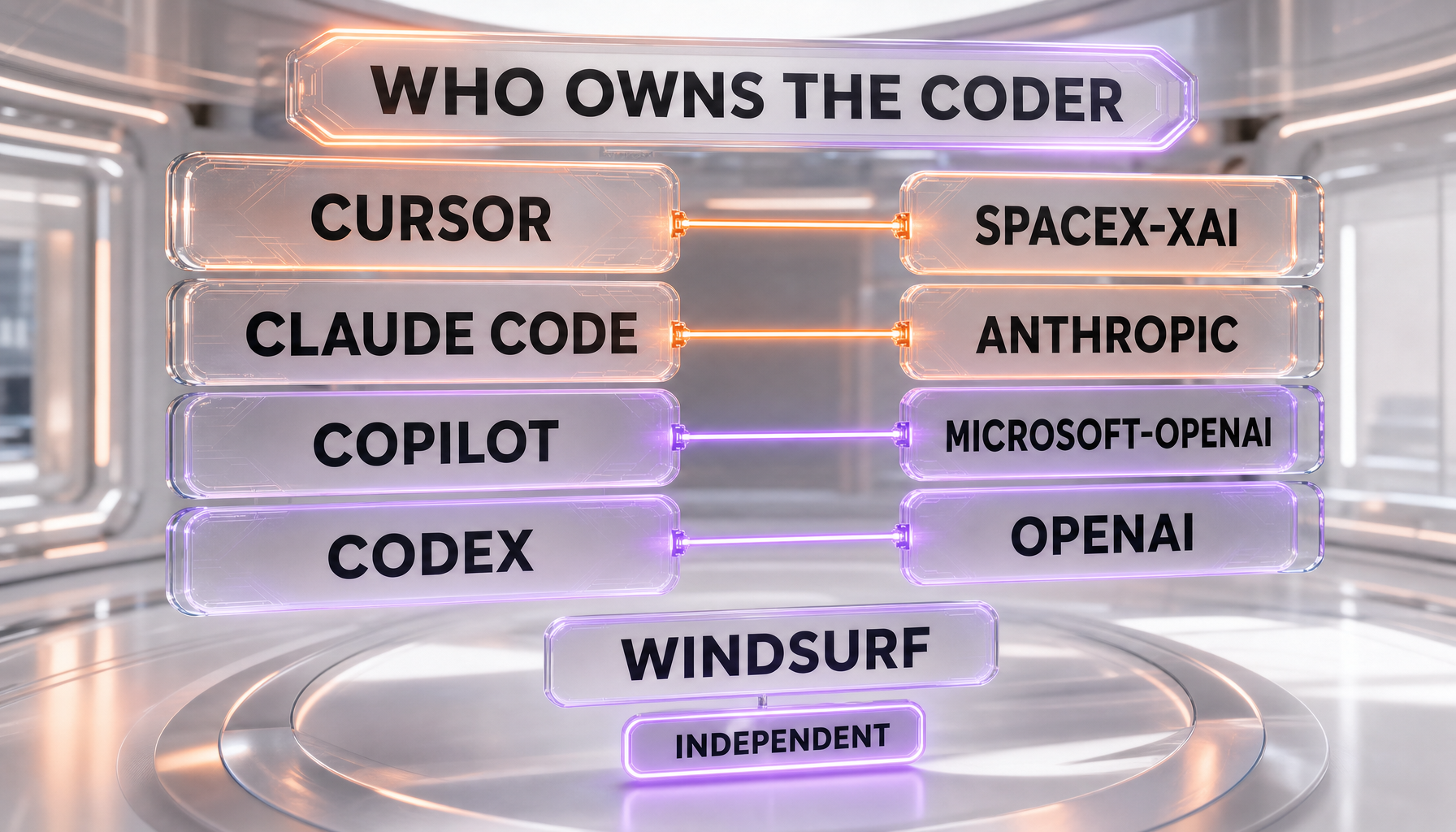

Cursor versus Claude Code, Copilot, Windsurf, and Codex

The acquisition reshapes the competitive map for AI coding tools, and it does so mostly by raising questions about Cursor's neutrality that its rivals will be quick to exploit.

Claude Code. Anthropic's terminal-native agentic coding tool is Cursor's most direct high-end competitor, and it benefits most directly from any perception that Cursor is becoming a Grok vehicle. Teams standardized on Claude for code generation now have a sharper reason to question whether Cursor's Claude integration stays first-class under an owner that competes with Anthropic. We compare the two directly in our three-way breakdown of Cursor 3, Google Antigravity, and Claude Code.

GitHub Copilot. Microsoft and GitHub's incumbent remains the default for a vast base of developers and is backed by an owner — Microsoft — that is deeply aligned with OpenAI. Copilot's pitch has always leaned on ubiquity and enterprise trust; a Cursor seen as tied to Musk's models lets Copilot lean harder on the stability-and-neutrality argument for risk-averse organizations.

Windsurf. Among the agent-first IDEs, Windsurf is Cursor's closest peer and the most natural destination for teams that want Cursor's workflow without exposure to the SpaceX-xAI ownership question. Expect Windsurf to position itself explicitly as the independent, model-neutral alternative.

OpenAI Codex. OpenAI's coding agent is both a competitor and a reminder that vertical integration cuts both ways: every major coding tool is now tied, directly or indirectly, to a model lab. Codex is openly an OpenAI product; the difference is that Cursor built its reputation on neutrality and is now owned by a lab, which is a harder narrative to manage than being a lab's product from the start.

The net effect: rivals do not need Cursor to get worse to gain ground — they only need enterprises to perceive added model-lock-in risk. That perception is now baked into the competitive conversation regardless of what SpaceX ultimately decides.

Governance, lock-in, and what enterprises should watch

For engineering leaders evaluating their AI coding stack, the acquisition introduces governance considerations that did not exist when Anysphere was independent.

The first is model-lock-in risk. An organization that standardized on Cursor partly to stay model-agnostic now has an owner with a clear incentive to promote one model. The mitigation is contractual: enterprises should seek explicit commitments on continued multi-model support and on data handling, rather than relying on today's defaults persisting after close.

The second is data governance. Code is among the most sensitive assets a software organization has, and ownership by a company with its own frontier-model ambitions raises legitimate questions about how prompts, completions, and repository context are used. None of this implies wrongdoing — it is the ordinary diligence any team should apply when a critical vendor changes hands, especially when the new owner trains models.

The third is concentration. With this deal, the combined SpaceX-xAI organization would own a frontier model lab, a flagship enterprise coding application, launch and satellite businesses, and a social platform under the broader Musk umbrella. That concentration is part of why the transaction will draw regulatory scrutiny, and it is also a reason buyers may want at least one credible independent alternative in their procurement mix.

The regulatory road to a Q3 close

The agreement is explicitly subject to regulatory approval, and the structure of the termination fees signals that both sides took antitrust risk seriously. A separate $4 billion antitrust-related termination fee, as reported from the filing, is the kind of provision parties include when they anticipate meaningful review and want to allocate the risk of a deal being blocked or delayed on competition grounds.

Several factors make scrutiny plausible. The acquirer already owns a frontier model lab, so combining it with the leading independent coding tool raises questions about whether rival model providers retain fair access to a major distribution channel for AI in software development. The sheer scale of the combined entity, and the prominence of its principal, tend to attract attention from competition authorities. None of this means the deal will be blocked — many large technology acquisitions clear review — but the third-quarter 2026 target is a planning estimate, not a guarantee, and the timeline could extend if regulators open an in-depth probe.

Until the transaction closes, the practical status is unchanged: Anysphere operates independently, and any integration with Grok or changes to Cursor's model routing would generally follow, not precede, the close.

What it means for developers right now

For day-to-day users, nothing about Cursor changes the moment this announcement lands. The agreement is pending, the close is months away, and product decisions follow integration. What changes is the calculus for the next decision you make about your AI coding stack.

If you are an individual developer, the pragmatic move is to keep using whatever tool is most productive while watching for two specific signals after close: any shift in Cursor's default model, and any change to how rival-model integrations are priced or surfaced. If those defaults tilt hard toward Grok, that is your cue to reassess.

If you are an engineering leader negotiating an enterprise contract, treat post-close model neutrality, pricing, and data handling as terms to secure in writing rather than assumptions to carry over. And regardless of where you land, the strategic takeaway is that AI coding tools are no longer neutral utilities sitting above the model layer — they are increasingly owned by the labs whose models they route to. Cursor's acquisition by SpaceX is the clearest expression yet of that consolidation, and it is a reason to value genuine optionality in your tooling more, not less.

We will update this analysis as the regulatory process advances and as SpaceX and Anysphere clarify Cursor's product direction under new ownership.

Frequently asked questions

Did SpaceX buy Cursor?

SpaceX agreed to acquire Anysphere, the company that makes the Cursor AI code editor, in an all-stock deal announced on June 16, 2026, valuing Anysphere at roughly $60 billion. The deal is not yet complete: it is expected to close in the third quarter of 2026 and is subject to regulatory approval, so SpaceX does not yet own Cursor. Until the close, Anysphere remains an independent company operating Cursor.

How much did SpaceX agree to pay for Cursor?

The agreement values Anysphere at roughly $60 billion in an all-stock transaction, according to CNBC, Reuters, and TechCrunch. Rather than paying cash, SpaceX is structuring the deal so that Anysphere merges with a wholly owned SpaceX subsidiary and Cursor's shareholders receive SpaceX stock. Reuters notes this structure means SpaceX is not using its IPO proceeds to fund the purchase.

Will Cursor still support models from Anthropic, OpenAI, and Google?

That is unresolved. Cursor has historically let developers choose among models including Anthropic's Claude, OpenAI's models, Google's Gemini, and Cursor's own model. Because SpaceX merged with xAI in February 2026 and owns the Grok model family, there is a clear incentive to favor Grok. The announcement did not commit to continued multi-model neutrality, so whether Cursor preserves genuine model choice or promotes Grok as the default is the key open question for users.

What are the termination fees in the SpaceX-Cursor deal?

According to the regulatory filing as reported by Reuters and Bloomberg, the agreement includes a standard termination fee of $10 billion and a separate antitrust-related termination fee of $4 billion. These figures were surfaced from the merger exhibit rather than stated in the main body of SpaceX's headline disclosure, so they should be attributed to the filing reporting rather than treated as headline terms.

How is this different from SpaceX's IPO?

SpaceX went public on the Nasdaq on June 12, 2026, in an offering priced at $135 per share that pushed its valuation above $2 trillion. The Cursor acquisition was announced four days later, on June 16, as a separate, all-stock transaction. The IPO made SpaceX a public company with a liquid, richly valued stock; the acquisition uses that stock as currency to buy Anysphere without spending the cash raised in the offering.

How does this affect Claude Code, GitHub Copilot, and Windsurf?

The acquisition raises a neutrality question that rivals can exploit even before any product change. Claude Code, from Anthropic, is Cursor's most direct high-end competitor and benefits if teams worry that Cursor's Claude integration weakens under an owner that competes with Anthropic. GitHub Copilot can lean on its ubiquity and enterprise trust, and Windsurf is positioned to court teams that want an agent-first IDE without the SpaceX-xAI ownership question. Rivals gain ground from perceived lock-in risk, regardless of SpaceX's eventual decisions.

When will the SpaceX-Cursor deal close?

The companies expect the transaction to close in the third quarter of 2026, but that date is contingent on regulatory approval, including antitrust review. The agreement's separate $4 billion antitrust-related termination fee signals that both sides anticipate meaningful scrutiny. If regulators open an in-depth investigation, the timeline could extend beyond the third quarter; the target date is a planning estimate, not a guarantee.

What was Cursor's revenue and valuation before the deal?

Reuters reports Cursor had roughly $2.6 billion in annualized business-to-business revenue based on company data shared in June 2026, a run-rate figure rather than audited annual revenue, up from crossing the $1 billion annualized mark in late 2025 as reported by CNBC. Before the SpaceX agreement, Cursor's last widely reported private valuation was around $50 billion, tied to a Series D round backed by investors including Andreessen Horowitz, Thrive Capital, and Nvidia.

Sources

- CNBC — SpaceX to buy AI coding startup Cursor for $60 billion

- Reuters via Yahoo Finance — SpaceX to buy Cursor parent Anysphere for $60 billion (deal structure, $2.6B run-rate, termination fees)

- TechCrunch — SpaceX to acquire Cursor for $60B in stock, days after blockbuster IPO (April option, IPO pricing)

- SEC EDGAR — SpaceX filings index (8-K)

ThePlanetTools.ai has no financial relationship with SpaceX, Anysphere, Anthropic, OpenAI, Microsoft, GitHub, or any company named in this analysis. This article is editorial reporting and analysis, not investment advice. Figures attributed to the regulatory filing reflect reporting by Reuters and Bloomberg and are subject to the definitive merger agreement.